Review of the Token Industry Cycle: The Upstream Peak Has Passed, and the Middle and Downstream Sweet Spots Have Arrived

06/26 2026

06/26 2026

420

420

I recently delved into a research report and gained profound insights, which I will briefly share with you today.

This is a research achievement by the Galaxy Securities team led by Wu Yanjing, which organizes the seven major US stock technology companies through the Token industry chain.

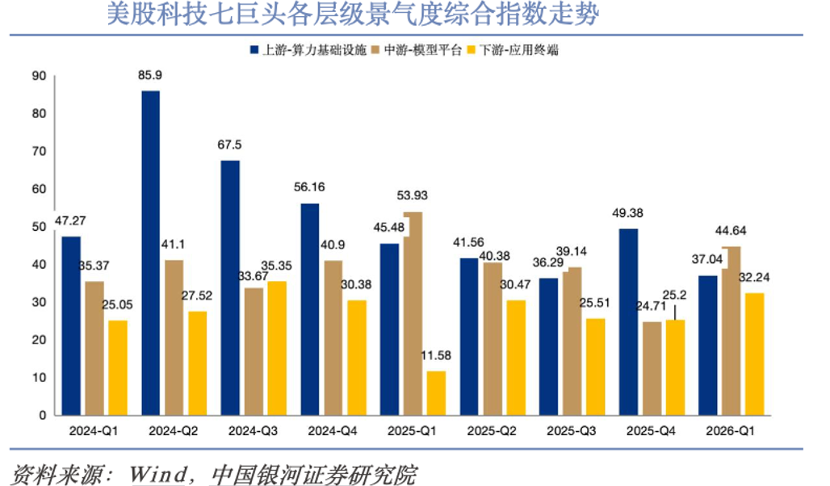

The comprehensive prosperity index for each level is set to be composed of three weighted sub-indices: revenue growth rate (weight 40%, reflecting demand prosperity), ROIC change (weight 30%, reflecting return improvement momentum), and CapEx/D&A change (weight 30%, reflecting investment expansion intensity). The results are shown in the following figure:

The following conclusions can be drawn from this:

1) From the trend of the comprehensive prosperity index at each level, the prosperity of the upstream computing infrastructure layer peaked in the first half of 2024 (with a comprehensive index exceeding 85.9), then entered a high-level decline channel, dropping to about 37.04 by 2026Q1;

2) The prosperity of the midstream model platform layer shows a characteristic of first rising and then stabilizing. The team believes that the midstream cloud computing layer has gradually transformed from a 'follower beneficiary' of the AI wave to a 'mainstay,' with its prosperity no longer entirely dependent on the supply pull from upstream chips but increasingly driven by downstream AI application demand;

3) The prosperity trend of the downstream application terminal layer is moderate. Unlike the rapid expansion of upstream chips and midstream cloud platforms, the penetration of AI in terminal applications is a gradual process that requires the coordinated advancement of product iteration, user education, and ecosystem construction, gradually increasing from 25.05 at the beginning of 2024 to 32.24 in 2026Q1, reflecting the gradual nature of AI application implementation.

What is even more noteworthy is the convergence of growth rate scissors between the upstream, midstream, and downstream sectors. In the first half of 2024, the upstream growth rate was about 20 times that of the midstream and about 35 times that of the downstream, indicating a huge scissors gap. By 2026Q1, the upstream growth rate (65.47%), midstream (18.73%), and downstream (21.64%) showed that the upstream growth rate was about 3.5 times that of the midstream and 3 times that of the downstream, with the gap significantly narrowing.

All these indicate that the investment clock is now pointing to the middle and downstream sectors: the high prosperity of the upstream has been fully priced in, and the growth rate inflection point has passed, while the middle and downstream sectors are in the early stages of a prosperity reversal upwards. In the Token economic industry chain, the current best investment sweet spot has shifted from upstream computing power to midstream model platforms and downstream application terminals.

Through the analysis of the indicators of the seven major companies, the report derives investment strategy recommendations corresponding to the Token industry chain:

Strategically bullish on the downstream: The decline in computing power costs + the inflection point in revenue growth rate = a Davis double play for downstream application profit margins. Focus on application giants with massive user scenarios and the ability to monetize Token consumption.

Tactically allocate to the midstream: Midstream cloud providers will enjoy the scissors dividend of falling procurement costs + cloud service price increases during the downward cycle of computing power prices, with profit margins expected to continue to exceed expectations.

Cautious approach to the upstream: Although the absolute growth rate of the upstream is still not low, the decline in ROIC and the implied fall in computing power prices indicate a cyclical inflection point, requiring caution against the risk of valuation declines due to worsening competitive dynamics (AMD/self-developed chips).

Through the rhythm of value transmission between the upstream and downstream, the report also divides the Token economic cycle into four phases:

Phase 1 (2023-2024): Innovation explosion period. Chat GPT triggers the AI singularity moment, and Token demand explodes from zero;

Phase 2 (2025-2026H1): Upstream investment enthusiasm period (current phase), with excess profits inducing huge capital expenditures and driving high prosperity in upstream infrastructure supporting products to continue;

Phase 3 (2026H2-2027E): Midstream industry chain integration period. During this phase, as Token production is essentially a high-intellectual-density + high-energy-consuming industry, Token intellectual output per watt and throughput will become the core competitiveness indicators for the midstream. The characteristics of elimination and integration will be significant, with small and medium-sized providers unable to bear high computing power expenditures exiting the market. Midstream cloud service providers (such as AWS, Azure, Alibaba Cloud, etc.) will fully shift to a MaaS usage-based billing system centered on Token consumption, with capital expenditures becoming more rational, self-developed chip substitution rates rising, and the supply-demand gap significantly narrowing;

Phase 4 (2028E+): Downstream application monetization period, with huge capital expenditures in the early stages driving a surge in scenario-side applications, infrastructure transforming into complete 'Token factories,' and the industry entering a stable return period.

The same is true for China as it is for the United States. Recently, the valuation of model-level companies in the midstream of the industry has skyrocketed, with market capitalizations surging and frequently refresh (shuā xīn, meaning 'refreshing') market perceptions. This can also be seen as an effect of the rotation of the value transmission wheel. Next, both the valuation and performance of cloud computing and large model providers are worth anticipating.

Some friends may still be concerned about the foam (pào mò, meaning 'bubble') in the large model industry and whether high capital expenditures will affect performance. Personally, I believe:

1) From the US experience, midstream companies in the industry are increasingly gaining pricing power, and the cost burden of inputs will decrease marginally;

2) A large number of companies will fail in the early stages of value transmission, with the industry passively squeezing out bubbles and consolidating. Leading cloud computing and model companies will gain higher pricing power, and investments will ultimately translate into returns.

The gears of value rotation have begun to turn. What will happen next? Let's wait and see.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving