Micron Technology Financial Report Analysis: Achieving All-Time Highs in Revenue and Profit!

06/26 2026

06/26 2026

394

394

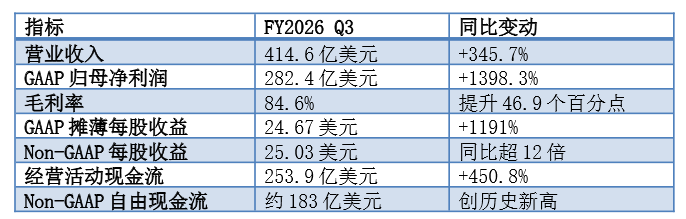

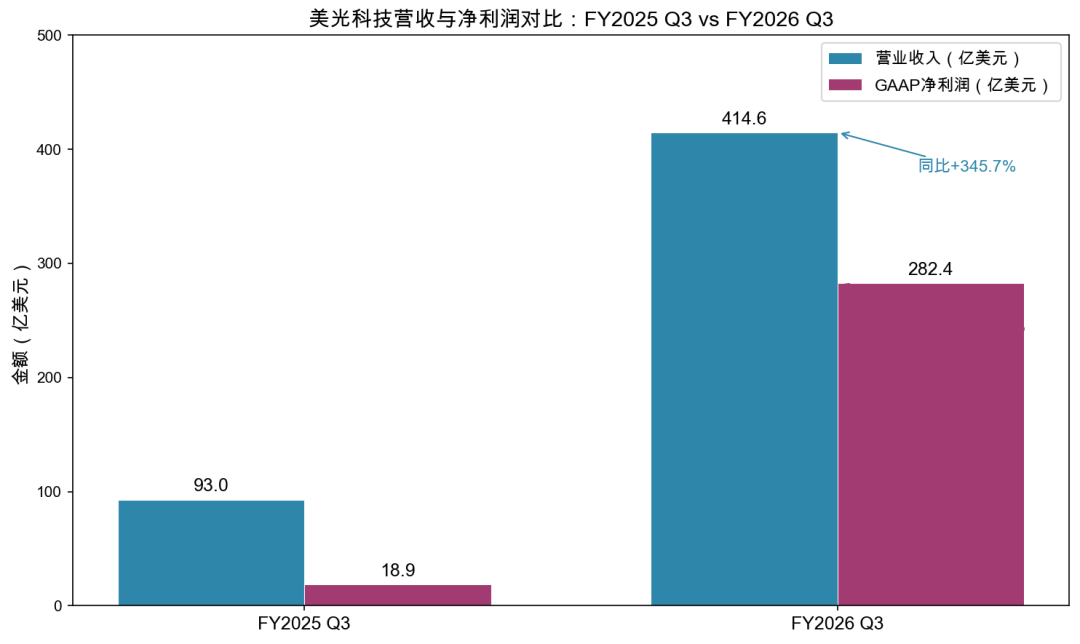

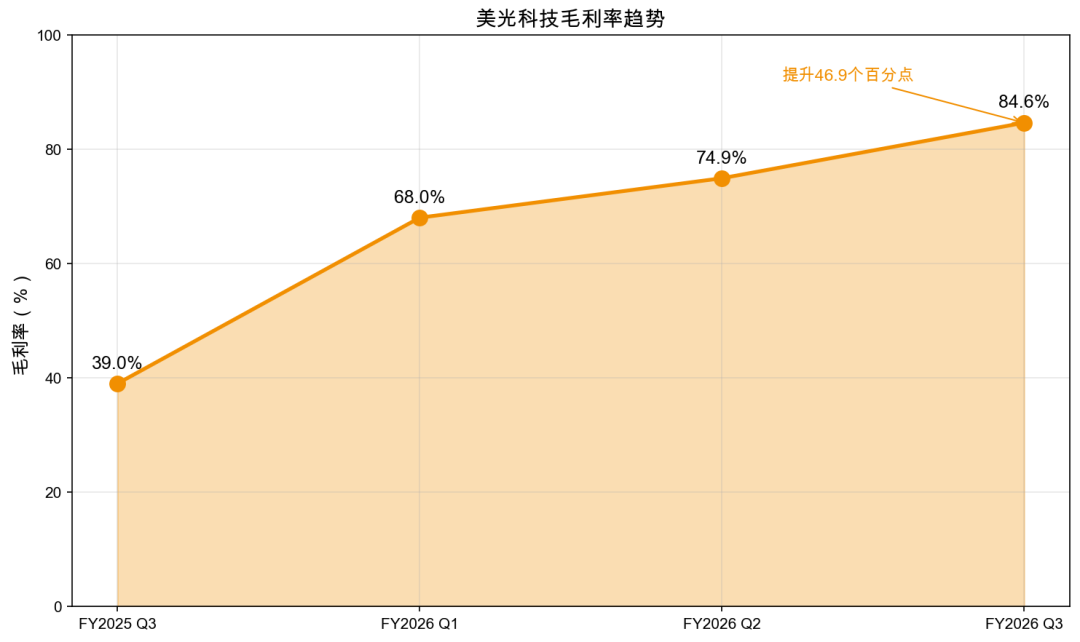

On June 24, 2026, Micron Technology (MU) unveiled its financial results for the third quarter of fiscal year 2026, showcasing quarterly revenue of $41.46 billion, marking a significant year-on-year surge of 345.7%. The GAAP net profit attributable to the parent company soared to $28.24 billion, a remarkable 1398.3% increase from the previous year. Additionally, the gross profit margin reached an impressive 84.6%, all establishing new benchmarks for the company.

Following the release of the financial report, Micron's stock price surged by over 14% in after-hours trading, reaching $1,194.

The significance of this financial report extends far beyond the mere numbers.

A year prior, Micron's revenue for the third quarter of fiscal year 2025 stood at a mere $9.3 billion, with a gross profit margin of 39%. Fast forward a year, and revenue for the same fiscal quarter has skyrocketed 4.5 times, while the gross profit margin has climbed by 46 percentage points.

The memory chip industry is currently undergoing a structural shift, fueled by the burgeoning demand for AI computing power, and Micron stands as one of the primary beneficiaries of this transformation.

1

All-Time Highs in Revenue and Profit

Micron's key financial metrics for the third quarter of fiscal year 2026 are as follows:

The company's prior forecast for the third quarter anticipated revenue of $33.5 billion (± $750 million), a gross profit margin of around 81%, and EPS of $19.15 (± $0.40).

Actual performance far exceeded these projections, with revenue surpassing the midpoint of the guidance by approximately 24% and EPS by about 31%. Non-GAAP EPS reached $25.03, about 22.1% higher than the consensus estimate of $20.49.

2

Growth Across All Sectors, with AI-Driven Businesses Contributing Over 60%

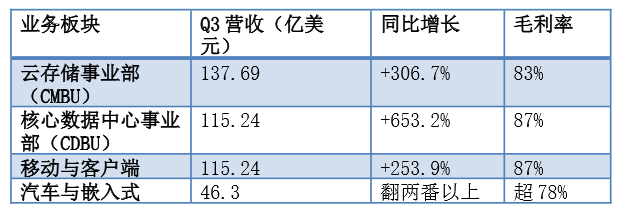

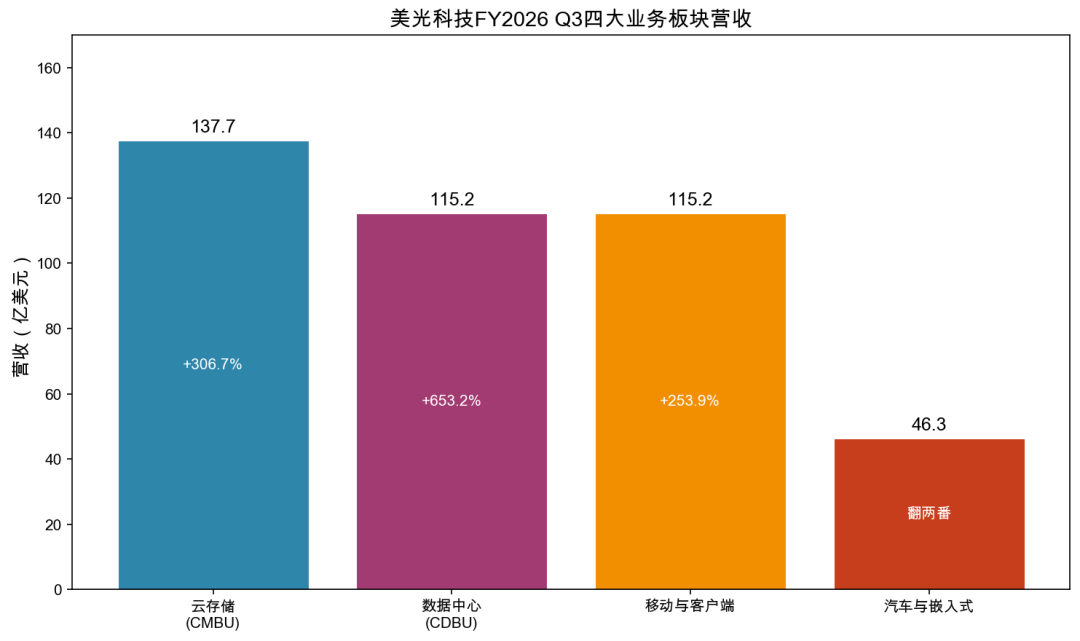

Micron categorizes its business into four segments, all of which experienced rapid growth this quarter, with gross profit margins exceeding 78%.

The combined revenue from the two AI-related segments—cloud storage and data centers—amounted to approximately $25.29 billion, accounting for over 60% of total revenue. The core data center business witnessed a staggering 653% year-on-year growth and a 102.5% quarter-on-quarter increase, making it the fastest-growing segment.

From a product standpoint, DRAM revenue more than tripled year-on-year, NAND flash revenue more than doubled, and high-bandwidth memory (HBM) revenue surpassed $1 billion for the second consecutive quarter. As a crucial component of AI GPUs, HBM demand is growing at a significantly faster rate than traditional memory products.

3

Dual Catalysts: AI Computing Power Demand and Supply Constraints

Micron's explosive performance can be attributed to two primary factors: the surge in AI-driven demand and structural supply shortages in the industry.

1. AI Demand: Accelerated Data Center Expansion, HBM Emerges as the Key Bottleneck

With the rapid adoption of large-scale model training, inference, and AI agent applications, the demand for memory capacity and bandwidth in AI servers has grown exponentially.

HBM (High-Bandwidth Memory), a vital component of AI GPUs, presents higher technical barriers and capacity concentration compared to traditional DRAM.

Micron CEO Sanjay Mehrotra stated during the earnings call that AI has emerged as one of the most significant growth drivers for the memory industry in decades, with the strategic value of memory and storage in data centers continuously on the rise.

2. Supply Side: Lengthy Capacity Expansion Cycles, Persistent Supply-Demand Imbalance

Expanding memory chip capacity entails a lengthy construction cycle.

Micron's two mega-fabs in Idaho and New York are not expected to achieve large-scale shipments until mid-2027 and 2028-2030, respectively. The newly constructed NAND flash fab in Singapore will not commence production until the second half of 2028.

SK Hynix's M15X line and Samsung's P5 line are also not anticipated to alleviate supply tightness until late 2027 to 2028.

Mehrotra made it clear that the HBM supply shortage across the industry will persist beyond 2027, and it is currently "impossible to predict" when supply will catch up with demand.

This supply-demand dynamic suggests that memory chip prices will remain elevated for the foreseeable future.

Micron has secured 16 long-term agreements (LTAs) with customers such as data center operators and automakers, locking in sales for the next three to five years—a rarity in the traditional memory industry.

4

Growth Momentum Expected to Sustain

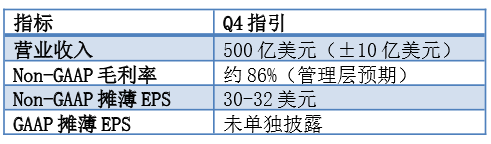

Micron provided the following guidance for the fourth quarter of fiscal year 2026 (ending August 2026):

The midpoint of the fourth-quarter revenue guidance stands at $50 billion, approximately 16% higher than analysts' previous expectations of $43.1 billion.

If the fourth-quarter guidance is met, Micron's full-year fiscal year 2026 revenue will approximate $139.2 billion (Q1 ~$23.86 billion + Q2 ~$23.86 billion + Q3 ~$41.46 billion + Q4 ~$50 billion), with GAAP net profit of approximately $51 billion.

On Wall Street, UBS raised Micron's target price from $535 to $1,625 (a 204% increase) on May 26-27, Deutsche Bank and Stifel raised it to $1,500, and Wedbush raised it to $1,300.

As of June 24, Micron's stock price stood at $1,194, up about 260% year-to-date and more than 8-fold over the past year, with a market capitalization exceeding $1 trillion.

5

Risks and Future Outlook

Despite Micron's strong performance, several risk factors warrant monitoring.

1. Cyclical Nature Not Fully Eliminated

The memory chip industry has historically been highly cyclical, with price surges often followed by oversupply and price declines.

The current high gross profit margins are largely contingent on supply-demand mismatches. Once capacity is released en masse, profit margins may face downward pressure.

2. Low Valuation Tolerance

At a current stock price of approximately $1,194, Micron's forward P/E ratio for fiscal year 2026 is about 6-7x (based on Non-GAAP EPS of approximately $80-85), which may appear low on the surface but assumes current profitability can be sustained.

If AI demand growth slows or competition intensifies, leading to price declines, valuations may face re-evaluation.

3. Technological Iteration Risks

HBM4 has commenced customer sample shipments, with mass production expected in 2027. 256GB DDR5 RDIMMs have completed sampling, and high-capacity 245TB QLC SSDs have begun shipping.

Product iteration progress directly influences Micron's compatibility with downstream customers such as NVIDIA and AMD.

4. Geopolitical and Supply Chain Risks

As a U.S.-based memory manufacturer, Micron enjoys certain strategic advantages amid global tech rivalries but also confronts uncertainties such as export controls and tariff policies.

From a longer-term perspective, the value of memory chips in AI hardware systems is structurally increasing.

Some institutions predict that the share of AI memory devices in the AI hardware BOM (bill of materials) will exceed 70% by 2027.

This signifies that memory chips are no longer traditional commodities but core components of AI computing infrastructure.

The long-term supply agreements (LTAs) Micron has signed with key customers mark the company's transition from a traditional cyclical stock to a growth-oriented tech stock.

-END-Disclaimer: This article is based on the public company attributes of listed companies and core analysis and research derived from information disclosed by the companies in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). Shiyu Xingkong strives for fairness in the content and viewpoints presented in the article but does not guarantee its accuracy, completeness, or timeliness. The information or opinions expressed in this article do not constitute any investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article. Copyright Notice: The content of this article is original to Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving