Can the Hong Kong Stock Market Pay for World Models? Dissecting Momenta's Prospectus

06/30 2026

06/30 2026

488

488

Graphic | Sister Tang

On June 29, Momenta released its global offering documents and officially launched its IPO. The offering price is set at HK$295.6 per share, aiming to raise approximately HK$5.89 billion. It plans to list on the Hong Kong Stock Exchange on July 8 under the stock code "6880," and is widely regarded as the "first physical AI stock."

Currently, Momenta is leading in autonomous driving, experiencing significant expansion from 2023 to 2025. Its revenue surged from RMB 743 million to RMB 2.413 billion, more than tripling, while its gross margin soared from 17.5% to 71.6%, reaching levels typical of software companies. Although it's not yet a true giant in terms of scale, its growth trajectory and profitability are impressive.

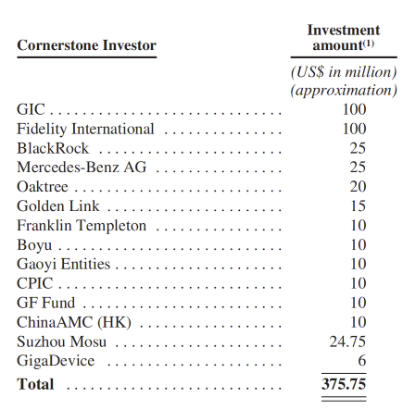

The most telling aspect of this IPO is its cornerstone investor lineup. Fourteen institutions have subscribed approximately US$376 million in total. GIC and Fidelity International each led with US$100 million investments, with BlackRock and Oaktree Capital following suit. Even Franklin Templeton, which had never participated as a cornerstone investor in Hong Kong stocks, made its debut. Domestic top-tier private equity, public funds, and insurance capital were also present, including Gaoyi Asset, Boyu Capital, China Asset Management, Guangfa Fund, and China Pacific Insurance. Industry heavyweights Mercedes-Benz and BYD, both existing shareholders and partners, reappeared, along with GigaDevice, a partner in Momenta's supply chain, which has seen significant A-share price increases recently.

GIC has invested in Anthropic and TSMC, while Fidelity has backed AI computing stocks like Cambricon. These investors, known for targeting high-growth tech stocks, are attracted to Momenta's AI capabilities. Mercedes-Benz and BYD, as both investors and partners, are doubling down by serving as cornerstone investors again.

Momenta's true ace lies in its world model outlined in the prospectus—a foundational capability born in the automotive sector but potentially applicable beyond it. The ability to transfer this capability to other scenarios represents the company's true potential, ultimately determining whether it should be valued as an automotive parts supplier or a large model company.

01 Steady Growth in the "Shovel-Selling" Business

Momenta operates in the autonomous driving sector, with revenue surging from RMB 743 million to RMB 2.413 billion from 2023 to 2025, more than tripling, and its gross margin rising from 17.5% to 71.6%, reaching levels typical of software companies.

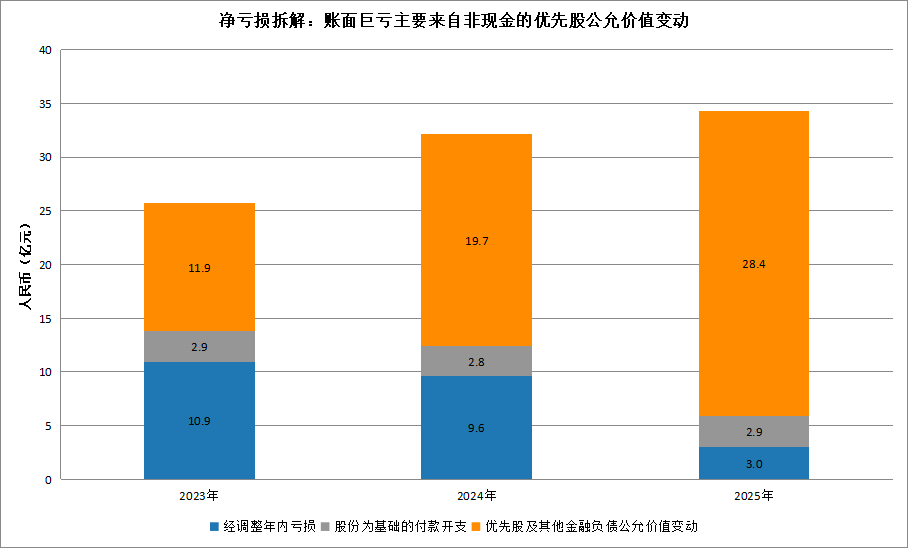

However, those reading the prospectus may first notice a discrepancy. The company reported a net loss of RMB 9.2 billion over three years, with R&D expenses consuming about 77% of revenue. These figures resemble a money-burning, far-from-profitable company. Yet, when examining operating cash flow alone, despite a book loss of RMB 3.46 billion in 2025, the actual cash outflow was only RMB 280 million, having narrowed by nearly 75% over three years.

The majority of this book loss stems from an obscure item called "fair value changes in preferred shares and other financial liabilities." These are convertible redeemable preferred shares, essentially a tool provided to investors during pre-IPO financing. Upon listing, these rights convert into ordinary shares as agreed, rendering the previous debt arrangement with principal and interest repayments null and void.

Before conversion, these preferred shares are not considered the company's own capital in accounting terms but rather a liability owed to investors, subject to revaluation as the company's valuation rises. The higher the company's value, the larger the recorded liability, with the annual increase directly include, count, enter into earnings as a loss. However, the company has not paid out any actual cash for these so-called losses; they are merely book figures.

This accounting treatment is not unique to Momenta. Zhipu, which listed in Hong Kong in January as the "first large model stock," raised over RMB 8.3 billion across eight financing rounds using preferred shares. With Zhipu's successful listing, these liabilities were transferred to equity, ceasing to impact the income statement. Such book losses stemming from preferred shares are common among Hong Kong-listed tech companies pre-IPO and are not taken seriously by those who understand financial statements.

Source: Momenta's prospectus, compiled by Tangping Index

Once the bookkeeping issues are clarified, what truly determines the company's value is the business itself, which has grown increasingly stable. China's new energy vehicle penetration rate continues to rise, and the market is becoming increasingly crowded, with over 500 new models launched in the first half of this year alone. Intelligent driving has become a critical differentiator for automakers, who dare not fall behind in this area.

However, developing a complete high-end intelligent driving system from scratch is costly and time-consuming. Building a top-tier team and achieving mass production pose significant challenges for automakers with limited intelligent driving experience. Momenta has chosen a different path—instead of competing with automakers in vehicle manufacturing, it sells intelligent driving "shovels" to all players in the market.

This approach is being validated by the market. According to CIC, independent suppliers' share of intelligent driving installations was less than 10% globally in 2022, rising to 28% in 2025, and is expected to reach nearly 75% by 2030. More and more automakers are realizing that it may be wiser to entrust core intelligent driving systems to leading professional suppliers and focus on building better vehicles rather than doing everything themselves.

Moreover, developing a vehicle from concept to mass production takes several years. Once an intelligent driving solution is selected, it becomes deeply integrated into the vehicle's development. Switching suppliers midway would essentially mean starting over, a risk few automakers are willing to take. As a result, licensing fees are paid throughout the vehicle's lifecycle based on installation volumes. This recurring revenue, characterized by high customer stickiness, predictable income, and higher gross margins, mirrors the most valuable aspects of the subscription model used by large model companies.

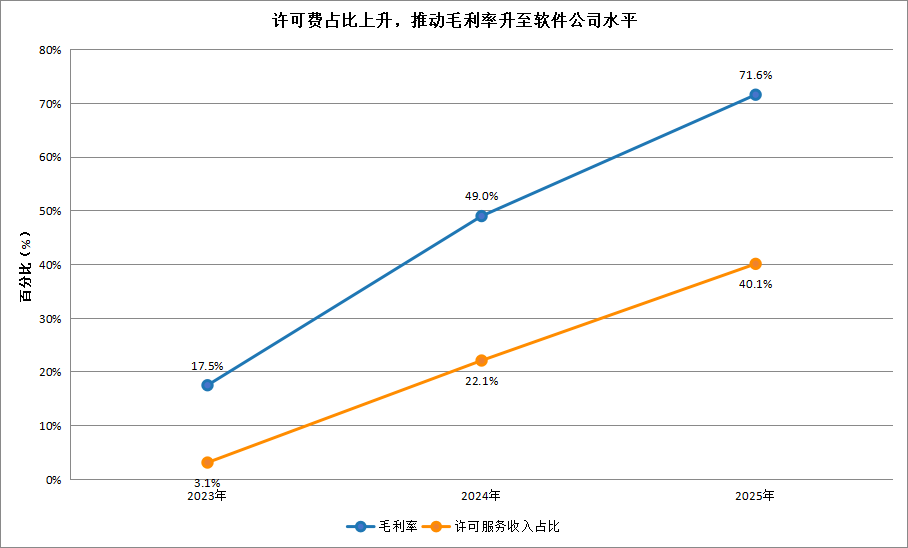

In 2023, Momenta primarily relied on project-based technical development service fees, earning revenue based on manpower with low gross margins. Licensing fees accounted for only 3.1% of revenue, with a gross margin of 17.5%. By 2025, licensing fee revenue had surged to RMB 968 million, accounting for 40.1% of revenue, a nearly 42-fold increase over two years, driving the gross margin up to 71.6%.

The average licensing fee per mass-produced model also increased, from approximately RMB 2.9 million in 2023 to about RMB 14.2 million in 2025. Benefiting from this business model, the company's adjusted net loss narrowed from RMB 1.09 billion in 2023 to RMB 300 million in 2025. Its rapid growth in recent years is attributed not only to the overall expansion of the intelligent driving sector but also to its successful implementation of the licensing fee model and achieving the largest market share among independent suppliers.

Source: Momenta's prospectus, compiled by Tangping Index

Furthermore, Momenta's absolute gross profit has increased 13-fold over the past two years, while R&D spending has only risen by about 46%. In 2023, R&D investment even exceeded annual revenue by 72%, but by 2025, gross profit had caught up to 92% of R&D spending. The narrowing adjusted loss is not due to R&D cuts but rather to the increasing gross margin brought about by a superior business model.

The growth potential of this business model is supported by Momenta's high-quality customer base. Its solutions have been installed in 24 global automakers, covering nine of the top ten global automaker groups, with Mercedes-Benz, SAIC, Toyota, and General Motors as shareholders. Among independent intelligent driving suppliers, Momenta leads in urban navigation assist sales with a market share of approximately 65%.

Moreover, its revenue sources are becoming increasingly diversified. The combined share of revenue from the top five customers has decreased from 86.7% in 2023 to 62.6% in 2025. Even if Momenta is viewed solely as an intelligent driving supplier, its business alone is robust enough.

02 The Model is the Gateway to Valuation

Momenta's true core beneath intelligent driving is a world model, positioning itself as a builder of foundational models for physical AI.

A world model fundamentally differs from past rule-based AI. Simply put, it enables machines to build an understanding of how the real world operates and predict what will happen next. In April, Momenta's R7 world model achieved mass production, marking the first time this capability was integrated into mass-produced vehicles.

Training this world model involves three main steps.

First, it is fed vast amounts of real-world driving data to imprint physical laws, common sense, and causal relationships, enabling it to understand how the real world functions. Second, a simulated training ground is created where the model can explore how different driving behaviors alter road conditions. Third, reinforcement learning is repeatedly applied within this training ground, akin to providing a highly realistic sparring partner, forcing the model to develop steadier judgment than even experienced drivers in extreme scenarios. Momenta is the first global independent intelligent driving company to implement such reinforcement learning in mass-produced vehicles.

Among independent intelligent driving suppliers, Momenta has achieved several such "industry firsts": It was the first to commercialize end-to-end autonomous driving in 2024 and the first to roll out mapless urban NOA nationwide. Supporting these achievements is a research and development team of 1,157 people, accounting for nearly 82% of the company's total workforce, with over two-thirds holding master's degrees or higher, along with cumulative R&D investment of RMB 4.66 billion over the past three years.

The value of the world model lies in its ability to become increasingly intelligent with use. Every mass-produced vehicle equipped with Momenta's solution collects real-world driving data. According to the company's latest disclosure, over 900,000 vehicles are already on the road, having accumulated more than 12 billion kilometers of real-world driving data. Moreover, Momenta has secured design wins for over 210 models, with future installations and data collection still to come.

As this data is fed back, the model becomes stronger, attracting more automakers to choose it, leading to further installations and widening the gap with competitors. To catch up, latecomers would need a fleet of similar scale, which they cannot achieve without a sufficiently advanced system.

The true scalability of this world model lies in its focus not on a fixed route but on general capabilities in perception, decision-making, and control within the physical world, making it applicable in other scenarios. Thus, Momenta can use the same world model for both passenger vehicle assistance and robotaxi services, currently extending to autonomous logistics vehicles and planning to expand into autonomous trucks by 2027.

In China, Momenta has partnered with Enjoy Ride, obtaining a driverless operation permit in Shanghai in January. Overseas, it has conducted testing in Munich, Germany, with Uber, secured testing permits in Abu Dhabi, and launched the world's first premium robotaxi service in collaboration with Mercedes-Benz. Its mass-production solutions have also been deployed in over a dozen countries and regions across Asia, Europe, Oceania, Latin America, and North Africa.

If Momenta can gradually solidify these scenarios, it will tap into a market far larger than automotive parts. According to CIC, the global market for mass-production assisted driving and higher-level intelligent driving will expand from approximately US$20.4 billion in 2025 to about US$305.9 billion in 2030. The robotaxi market, encompassing autonomous taxis, logistics vehicles, and trucks, will reach nearly US$200 billion by 2030.

As a company with stable performance, honed in the highly competitive and challenging global automotive market, Momenta is now bringing its world model to even larger markets and is about to go public. At this stage, it is no longer just an automotive parts company but more akin to a newly prominent physical AI company.

03 Conclusion

How a company is valued depends not only on what it sells today but also on its position in the industrial chain. CATL has already demonstrated this logic: while automakers engage in price wars upfront, the company holding critical technologies and profit distribution rights may be the one behind the scenes.

Momenta aims to tell a similar story.

According to public reports, the overall valuation for this IPO is approximately US$9 billion. Based on 2025 revenue of RMB 2.413 billion, the PS ratio is about 26 times, which is not low within the automotive chain, where complete vehicle companies typically have single-digit PS ratios and traditional automakers even lower. However, it is precisely this high multiple that attracts top-tier cornerstone investors, as they see something greater in Momenta.

Thus, the question is not whether the Hong Kong stock market is willing to accept this valuation but how Momenta can persuade the market to do so.

Its argument cannot rely solely on "autonomous driving." What truly elevates the valuation framework is Momenta's creation of a real-world data flywheel through mass-produced vehicles and its deployment of world models in the physical world. Vehicles are merely its first application scenario; the model is what the market can reprice.

Financially, Momenta is not a company reliant on continuous financing to survive. As of the end of 2025, it holds over RMB 10 billion in cash reserves, with net operating cash outflows of only RMB 280 million in 2025, which are still narrowing. More importantly, the share of licensing fees has risen from 3.1% in 2023 to 40.1% in 2025. If it continues on this path, achieving profitability will be straightforward.

Looking ahead, the penetration rate of urban NOA in new Chinese vehicles was only 11.3% in 2025, expected to rise to 62.4% by 2030, according to CIC. L3 commercialization may not truly begin until around 2027. Robotaxis, autonomous logistics vehicles, and trucks—more distant scenarios—have not yet been fully realized but provide Momenta with a narrative boundary larger than just being an "intelligent driving supplier."

This is where the company will truly be tested after going public: If the market prices it solely based on the automotive chain, US$9 billion may seem expensive. If it can progressively demonstrate that world models can extend beyond mass-produced vehicles to more physical scenarios, this valuation may only be the beginning.

Statement: This article is for learning and communication purposes only and does not constitute investment advice.

Welcome to like, share, and repost. Your support is our motivation for updates! Related Reading: Hynix is too expensive, but high price is not a reason to be bearishA U.S. ban has thrust China's open-source models into the spotlightAI chip market loses trillion in a day: Non-farm payrolls are just an excuse, overcrowding is the real reasonAI demand surges towards infrastructure, this small company is quietly selling waterHow can JD.com be so tough on merchants when it's making the most money?SpaceX Prospectus Overview: The Market Isn't Buying Rockets and AI, It's Buying Musk HimselfWhen all investment groups are talking about storage, what should you consider?

-

![]()

5G Standalone Private Network Policy Breaks the Ice, Creating an Exclusive 'Nervous System' for Physical AI in Industrial Scenarios

-

![]()

Two Investments Totaling 700 Million Yuan! Sunny Optical Sets Its Sights Beyond Lens Supply, Launching a Strategic Move in the XR Optics Arena

-

![]()

Xianyu Initiates Internal Testing of 'Yu Maimai' and 'Yu Maimai': Can AI Revolutionize Secondhand Transactions?

-

![]()

The Dullest 618 in History, with AI Being the Busiest

-

![]()

Shenzhen’s Most Mysterious Robot Startup Secures 1 Billion Yuan in Funding, Targeting a 150 Billion Yuan Market

-

![]()

Why Are Celebrities So Keen on Diving into the AI Realm?

-

Can WeChat AI Sidestep the Quandary Faced by Doubao Phone?

-

![]()

Luxury Lineup, Highly Anticipated! The Pioneer of Physical AI Gears Up for Hong Kong Stock Exchange Debut!