Surplus Capacity Leasing vs. Aggressive Expansion: Is Meta's 'Dual Strategy' a Deliberate Move?

07/13 2026

07/13 2026

574

574

Following Meta's exploration into leasing computational power, which has raised questions about the maturity of the computational power industry chain, and amidst market debates on whether this is a temporary shift or a long-term strategy, Meta has made three significant moves to underscore its commitment to the computational power sector.

Expanding data centers is the most straightforward preparatory step, while mass-producing its own ASIC chips aims to balance costs and achieve a higher return on investment (ROI). The newly launched large model, Muse Spark 1, is where Dolphin Research sees the true potential for exceeding expectations.

These three developments are expected to drive a continued increase in short-term capital expenditures (Capex), inevitably putting pressure on earnings per share (EPS). However, what is becoming clearer is a shift in Meta's strategic focus—from a 'cost-centric' approach to consumer AI (C AI) to a 'profit-oriented' business-to-business AI (B2B AI). Investors are likely to overlook the short-term fundamental pressures due to upfront investments and raise expectations for direct AI monetization.

While numerous organizational challenges persist, amidst the current controversies, the market's sentiment towards Meta's valuation is poised for a more defined adjustment.

Large Model 'Overhaul': Room for Surprises?

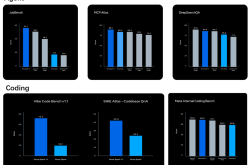

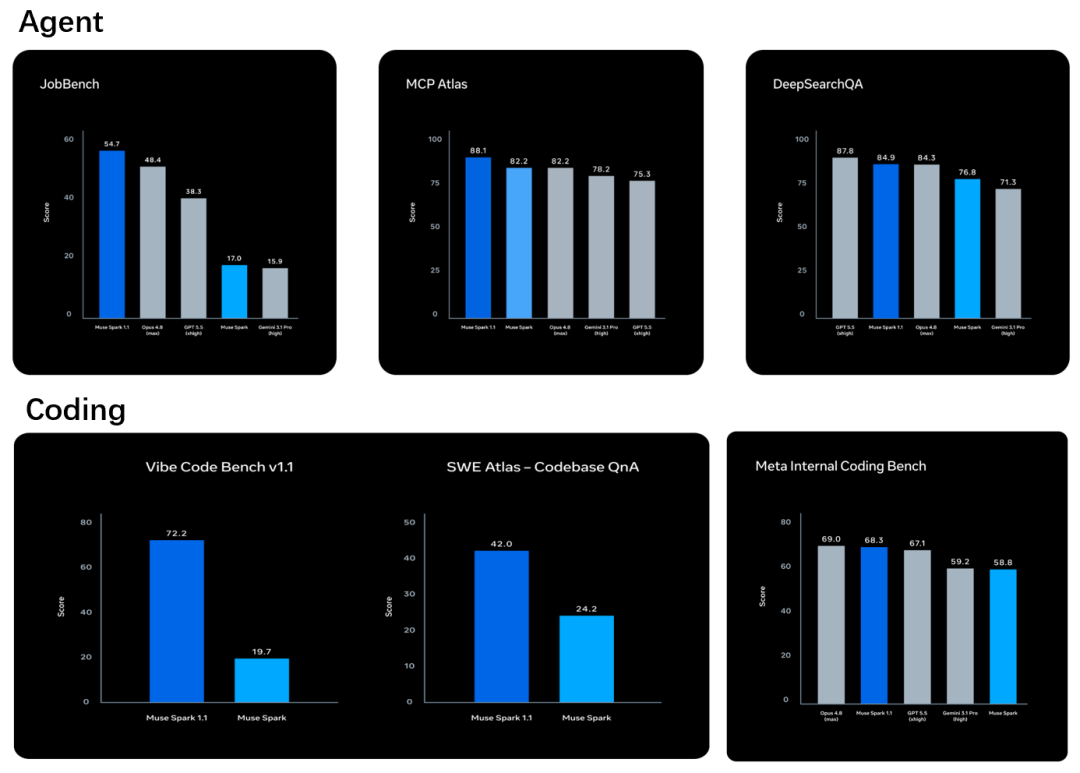

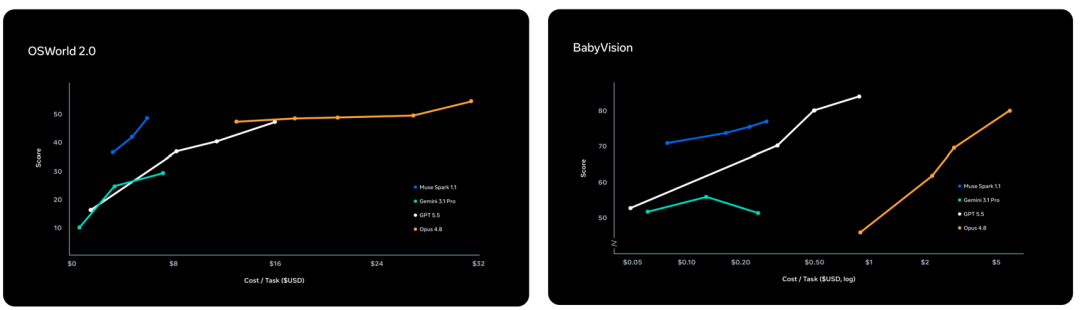

From Dolphin Research's perspective, the release of Muse Spark 1.1 last night truly surpassed expectations, as large model technology is pivotal for Meta's long-term organic growth, especially given the current organizational challenges. To some extent, it eases market concerns about Meta's organizational vitality.

Muse Spark 1.1 represents a significant upgrade from the Muse Spark model released earlier this year. It is a multimodal model tailored for Agent tasks, featuring notable improvements in intelligence, coding, and multimodal understanding.

With a top-tier model in place, subsequent computational power leasing will not just involve renting out bare chips but offering complete, value-added solutions, such as bundling large model capabilities with Agent functionalities.

Beyond technical enhancements, Muse Spark 1.1 stands out for its cost-effectiveness. It delivers intelligence comparable to Opus 4.8 at just one-fourth the cost, seemingly outperforming even GLM-5.2 in terms of value.

Within a week, OpenAI, Grok, and Meta sequentially unveiled new models, with rumors suggesting Google will soon follow suit. Competition is intensifying, and even leading player Anthropic coincidentally reset user token limits (a form of temporary compensation).

Why Does Meta's Large Model Capability Seem to Be Back on Track?

Dolphin Research recalls a widely held belief regarding the potential for large model improvement—currently, the competition among leading large models increasingly hinges on data barriers (high-quality annotated data for core reinforcement learning from human feedback (RLHF) in the alignment phase), particularly real behavioral data from users' interactions with AI—recording every step of user operations, error corrections, decision-making logic, etc.

For instance, in the coding domain, it is influenced by de-sensitized programming trajectory data for business-end (B-end) applications. Both Anthropic and OpenAI have accumulated rich data in this area, but Google, constrained by compliance red lines, lags behind in the volume of long-trajectory data 'usable for training' compared to its competitors.

The collection of process data and data annotation can be linked to Meta's unique activities over the past year:

On one hand, building an in-house annotation team represents a significant team adjustment following Meta's acquisition of Scale AI and is one of the main reasons for internal employee dissatisfaction (employees believe data annotation lacks technical content, yet refusal to comply with job adjustments leads to layoffs).

On the other hand, recent reports of Meta employees complaining about the company collecting workflow data through computer screens and mouse movements align with the aforementioned demand for long-trajectory data.

Therefore, does this imply that Meta has opportunities for latent breakthroughs and overtaking competitors? Dolphin Research will continue to monitor, especially whether there can be more resolutions to internal organizational issues, which directly affect Meta's future ability to 'flex its muscles' continuously.

Computational Power Target Doubled, but Cash Flow Remains a Concern

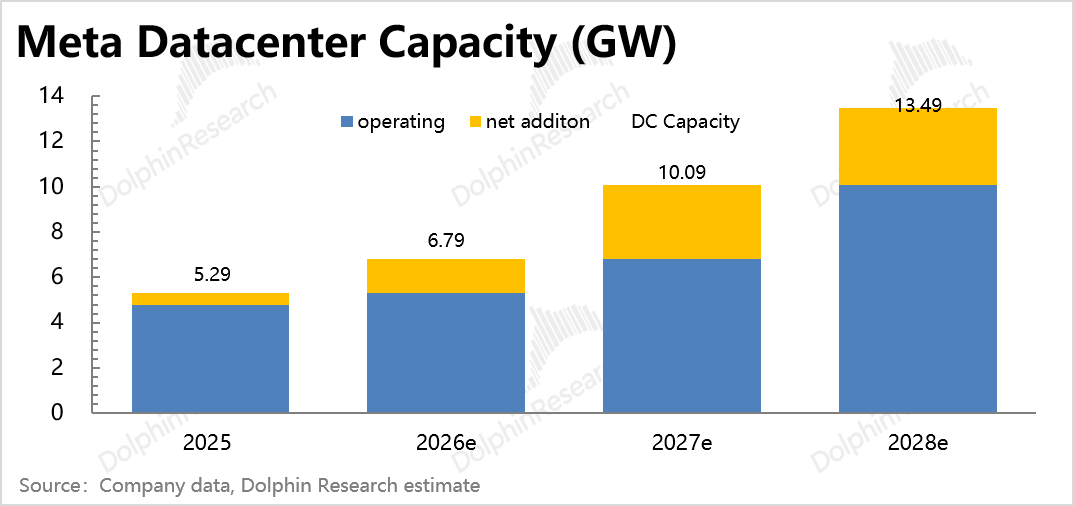

The most significant news for the AI industry chain last night was Meta's plan to double its data center computational power reserves, alleviating concerns about major clients cutting Capex.

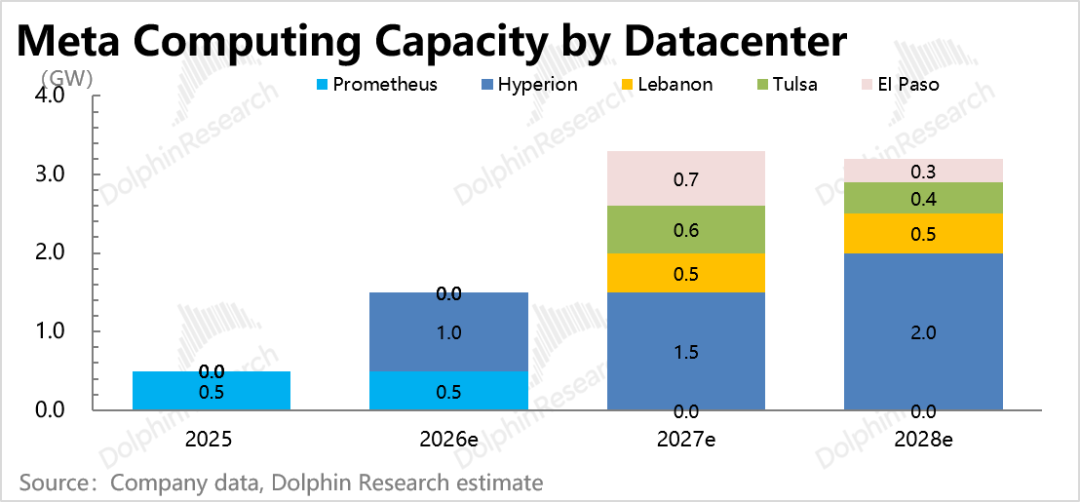

Reuters reported that Meta's computational power deployment target for next year reaches 14 gigawatts (GW), doubling from the end of this year. Previously, Dolphin Research estimated around 7GW for 2026 based on Meta's data center construction plans, with projections for the end of 2027 at around 9-10GW. This falls short of Reuters' report by a net difference of 4GW.

However, two issues arise: one is whether Meta has sufficient funds, and the other is whether the plans can be executed and operationalized on schedule.

The latter involves too many variables to quantify, so the market tends to overlook it when optimistic in the short term. However, based on past experiences, there is often a gap between data center planning and actual implementation, a point that requires caution, though Dolphin Research will not dwell excessively on it.

Nevertheless, the first issue can be addressed briefly. We discuss it in several sub-points:

(1) How much will it cost to expand computational power capacity next year?

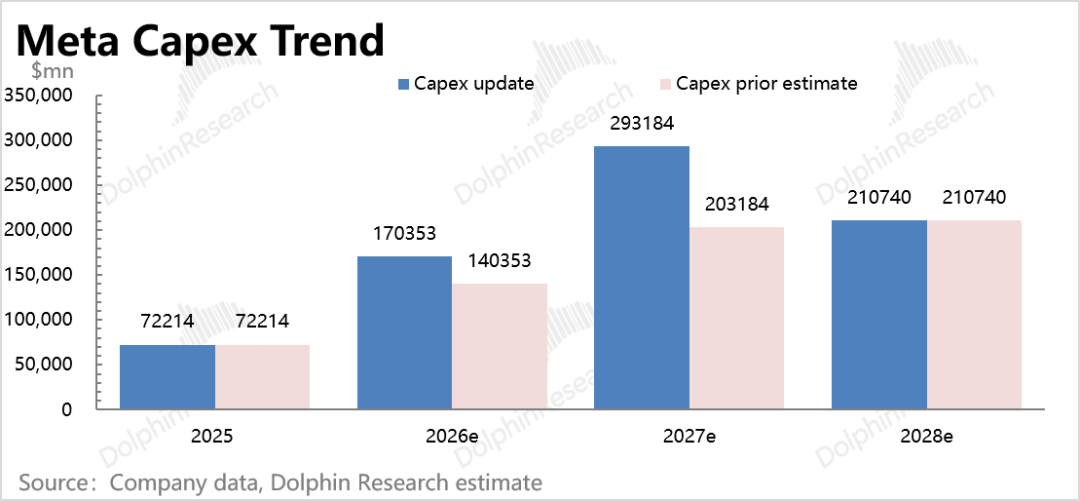

Dolphin Research directly breaks down Meta's Capex into computational power investment expenditures and other expenditures. Computational power investment is calculated based on an average deployment cost of 35 billion yuan per GW and the cyclical plans of various campuses (while excluding off-balance-sheet financing with Blue Owl and averaging over five years). The remaining Capex expenditures are projected to grow at a normal rate of 20% after 2027.

Our original expectation was Capex expenditures of 140 billion/203 billion yuan for 2026/2027. However, if we add the net difference of 4GW underestimated for 2027, even considering partial procurement of tensor processing units (TPUs) + self-developed ASIC chip Iris to lower comprehensive costs, calculated at 30 billion USD/GW, an additional 30 billion * 4 = 120 billion USD would be needed over these two years.

Another significant information bias is that if 14GW refers only to the plan by the end of next year (2027) rather than the requirement for complete deployment, the additional 120 billion USD for 2026-2027 can be further amortized into 2028 or even 2029.

Dolphin Research leans towards it being a planning target for 2027 rather than requiring full deployment by the end of the year. Otherwise, given a construction cycle of 1-2 years, we should already see new data centers beyond the five currently under construction commencing, construction teams mobilizing, and electricity suppliers being sought.

Therefore, a middle ground suggests it will likely fall within the range of our previously expected Capex, i.e., 140-170 billion yuan this year and 200-290 billion yuan next year.

An observation signal is whether Meta's Q2 earnings report at the end of the month will continue to raise this year's Capex and whether the tone regarding the 14GW computational power deployment during the earnings call is aggressive.

(2) Does Meta have sufficient liquidity?

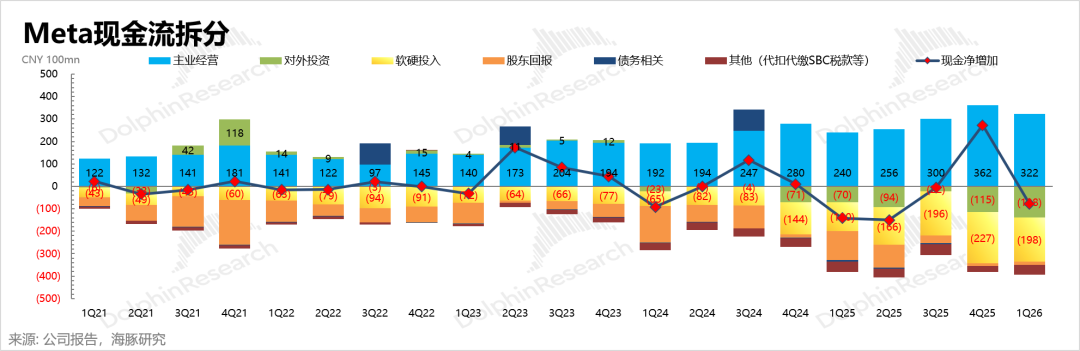

The 14GW plan is a target, but we must assess whether Meta has the capacity to achieve it. After all, Zuckerberg has a history of making bold promises, with strategic drifts and internal conflicts not unprecedented.

Firstly, Meta's core advertising business is showing strong growth momentum. Despite fluctuations in the current U.S. economic environment, it is likely to support subsequent high growth. However, without computational power leasing, under our original Capex expectations, the Capex-to-revenue ratio for 2026 and 2027 would reach 55% and 65%, respectively.

This figure is relatively high. Considering operating cash flow/revenue at 50-60%, it implies that nearly all cash flow generated from daily operations over the next two years will be invested in computational power.

Although Meta has maintained a 'Cash Neutral' cash management habit, a single Capex item could exhaust its operating inflows. Adding other external investments, debt interest, etc., would result in negative cash flow for two consecutive years, undoubtedly detrimental to the company's operational stability.

Of course, as a leading tech giant, Meta doesn't need to deplete its cash flow and can leverage its credit to secure low-cost financing, such as issuing corporate bonds at the end of last year and off-balance-sheet financing with private credit institutions.

However, with the expected revenue from computational power leasing, the pressure on Meta's investments will be relatively alleviated.

For instance, assuming 30% of the capacity is leased out in 2026 and 2027, i.e., 2 and 4GW, respectively, and calculating based on annualized revenue from bare chip rentals at 10-15 billion yuan/GW, this would add at least 20 billion and 40 billion yuan in revenue over the two years, increasing the original revenue expectations by 8% and 12%, respectively. If bundling large model and Agent capabilities, the increment would be even greater.

As shown below, after considering the additional investments required for the computational power of new data centers and the revenue from leasing 30% of the capacity, the overall pressure on Capex relative to revenue is somewhat eased.

However, due to upfront investments, short-term utilization of deposits and cash reserves (currently 81 billion yuan in cash + short-term investments and 59 billion yuan in long-term debt) will be necessary. Therefore, if the 14GW plan for next year is realized, subsequent debt financing will still be essential.

Compared to the previous pure cost item (AI's role in advertising growth is not the main driver), at least now, when Meta pushes for debt financing to bet big on AI, it will face relatively less resistance from shareholders.

ASIC Mass Production Imminent, Primarily for Self-Use to Reduce Costs

Last night also brought news that the fourth-generation MTIA chip (Iris) is set for mass production in September, having completed testing without significant bugs. At this pace, Iris will undoubtedly be a crucial component of next year's total computational power of 14GW.

Iris is an ASIC chip independently designed by Meta for both training and inference (though primarily for inference, we predict), with Broadcom responsible for co-design and physical implementation and TSMC for manufacturing. A software company venturing into chip development essentially stems from frustration over the high prices of NVIDIA GPUs.

In terms of hardware deployment, Meta has reportedly signed long-term agreements with key module manufacturers—Samsung and SanDisk—as well as procuring fiber optic equipment from Sumitomo Electric.

However, this chip is primarily for self-use, as TSMC's production capacity share is unsuitable for Meta to engage in the chip business. Therefore, the intention behind continuous chip R&D remains a cost-effectiveness issue—reducing inference costs and dependence on a few specific companies.

Summary

Overall, compared to the ambiguous statement a few days ago about 'considering leasing idle computational power,' the most significant change this time is the confirmation of Meta's long-term strategic commitment to the computational power leasing business.

More critically, the release of a new model capable of squeezing into the first tier (with promising paper specifications, though we will continue to monitor actual user feedback) has alleviated some of the market's concerns about Meta's recent internal organizational issues. It has also expanded the imagination space for the ROI of Meta's computational power leasing business—from merely leasing bare computational power and riding the industry beta to envisioning the bundling of large model APIs and even gradually providing additional cloud services.

It is worth mentioning that while Meta's shift in identity indirectly proves that short-term commercialization of AI for consumers (ToC) still faces obstacles, potentially weakening market expectations for Meta AI's C-end monetization, it remains overall favorable for Meta, whose investment sentiment has been suppressed for some time.

However, on the flip side, stepping out of Meta as an individual and looking from an industry perspective, with diminishing marginal utility improvements in large models and the likely siphoning effect of a single dominant player (Anthropic) despite sustained growth in annual recurring revenue (ARR), will Meta's entry into the computing power supply side accelerate the peak of industry chain investment?

As massive investments continue to pour into computing power, there is little doubt that 2027 and 2028 will be pivotal years for the expansion of the global computing power supply. Dolphin Research deems it essential to provide an updated analysis of the supply-demand dynamics within the computing power sector across the entire industry. This will help to assess the duration of the window-period dividend stemming from mismatched hardware production capacities, as well as to determine whether the marginal incremental space has begun to narrow. Stay tuned for further insights.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is strictly prohibited without prior authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for providing general comprehensive data and is designed for the general reading and data reference of users of Dolphin Research and its affiliated entities. It does not consider the specific investment objectives, preferences for investment products, risk tolerance levels, financial situations, or special needs of any individual recipient. Investors are strongly advised to consult with independent professional advisors before making any investment decisions based on the information contained in this report. Any individual who makes investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be held liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data presented in this report are sourced from publicly available materials and are intended for reference purposes only. Dolphin Research endeavors to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities, an invitation to buy or sell securities, or as advice, solicitation, or recommendation regarding relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for, nor are they to be distributed to, jurisdictions where the distribution, publication, provision, or use of such information, tools, and data would conflict with applicable laws or regulations, or would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, or to citizens or residents of such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant authors and does not represent the official stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and the copyright is exclusively owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual shall (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Even Li Auto Is Facing Challenges. Can Xiaomi Make a Mark in the Extended-Range Hybrid Vehicle Market?

-

![]()

Surplus Capacity Leasing vs. Aggressive Expansion: Is Meta's 'Dual Strategy' a Deliberate Move?

-

![]()

German Business Leaders Contemplate 'Embracing the 996 Culture,' While Chinese Auto Workers Simply Aspire to Clock Out On Time

-

Graduating with a Violin Serenade in a Luobo Kuaipao, Enjoying Yunba Rides, and Watching Football with Milu: Shenzhen's Seamless Integration of Driverless Cars into Daily Life

-

![]()

Shenzhen Unveils 331 Nighttime Autonomous Vehicle Routes in Three Months: Even Logistics Embrace Off-Peak Operations in the Vibrant City

-

![]()

Why Did the Lingguang App Lose Its Competitive Edge? A Strong Hand Played Poorly

-

![]()

Monthly Double Building Purchases for 3.8 Billion: Is Duan Yongping Still in Sync with Pinduoduo?

-

![]()

Tesla FSD’s China Debut: How Orbbec’s ‘AI Eyes’ Are Revolutionizing Intelligent Driving and Robotics