Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

07/13 2026

07/13 2026

521

521

Much Ado About Nothing

Written by / Chen Dengxin

Edited by / Li Ji

Layout by / Annalee

The AI revolution is poised for a significant leap forward.

In June 2026, internet behemoths such as JD.com, Tencent, and Alibaba began focusing on AI-driven payments, aiming to bridge the 'last mile' of AI commercialization.

After all, the era of intelligent agents necessitates a closed-loop transaction ecosystem.

However, after nearly a month of intense competition in AI-driven payments, the battlefield remains surprisingly calm, lacking the fierce clashes anticipated by outsiders. Even the rivalry among major players has failed to create significant waves.

Why, then, is there so much hype about AI-driven payments with little to show for it?

AI and Payments: A Perfect Match

The limits of traditional payments are becoming increasingly apparent.

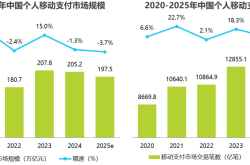

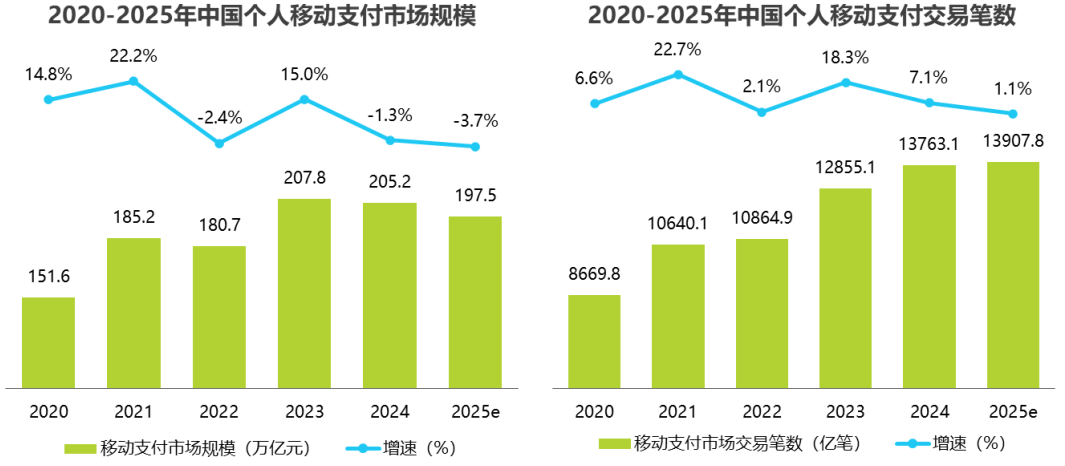

According to iResearch Consulting, in 2025, China’s personal mobile payment transactions reached 1,390.78 billion, marking a 1.1% year-on-year increase, while the market size of personal mobile payments was RMB 205.2 trillion, a 3.7% decrease year-on-year.

Source: iResearch Consulting

This indicates that the traditional payment market is nearing saturation, urgently requiring new growth drivers.

Lin Jian, General Manager of Starpay, commented, "With the advancement of AI technology, the business chains of various stakeholders connected through payments will encounter historic opportunities for user experience optimization and business model reconstruction."

Coincidentally, AI is also in search of practical applications.

In previous years, the industry equated the scaling of large model parameters with the emergence of intelligence, leading to a focus on increasing model parameters from billions to trillions.

The problem lies in the fact that practical application is the core logic of large models. For AI to transition from being merely usable to truly effective, intelligent agents are essential.

Jensen Huang, founder and CEO of NVIDIA, stated on stage at GTC Taipei 2026, "Useful AI has arrived, and the era of intelligent agent AI is in full swing."

Against this backdrop, intelligent agents have become a super traffic entrance for AI, prompting major internet players to increase their investments, aiming to gain greater industry influence and secure a higher position in the AI ecosystem.

Thus, the collaboration between AI and payments is a natural fit.

More importantly, in 2026, AI is stepping into real-world task scenarios. Platforms like Doubao, Yuanbao, and Qianwen can now perform a series of daily tasks for users, bringing 'one-sentence shopping' to the forefront.

AI Steps into Real-World Task Scenarios

Take Qianwen as an example. Six months after integrating payment capabilities into AI conversations, it completed 300 million intelligent agent payments, supporting 95% of general intelligent agent frameworks.

WeChat Pay officially stated, "Enabling intelligent agents with complete payment service capabilities is a crucial step in expanding AI intelligent agents from efficiency tools to consumer scenario capabilities."

As a result, user habits have subtly changed.

As users gradually become accustomed to fulfilling their daily needs through conversations with AI, the payment process becomes the 'last mile.' Driven by the convergence of demand and technology, AI-driven payments are no longer an option but a necessity.

In short, AI-driven payments have bridged the commercial loop of 'one-sentence shopping,' achieving an integrated payment chain.

'Singularity Research Society' stated, "AI-driven payments are not a whimsical creation by major companies, nor are they a meaningless battle for market entry points, let alone a 'pseudo-demand' that users do not need. They represent an infrastructure upgrade driven by both technology and user habits, marking an inevitable evolution in the payment industry from 'transaction processing' to 'intelligent services.'"

Why Can't It Be Achieved Overnight?

Against this backdrop, internet giants are favoring AI-driven payments, but their approaches differ.

For instance, Alibaba launched an AI-driven version of Alipay, consolidating previously scattered services into a single conversational interface, using payments as a pivot to drive a new AI commercial ecosystem.

In short, the underlying logic of payments has shifted from users seeking services to services reaching users.

It is worth noting that Alibaba has been exploring AI-driven payments for years. As early as 2023, it began exploring intelligent transformation and launched the standalone app 'Zhixiaobao' in September 2024. However, due to various reasons, the initiative failed to gain traction. Subsequently, the focus shifted back to the main Alipay app, introducing a series of payment features such as AI Pay, AI Receive, Token Pay, and AI Wallet.

Payments Enter the Conversational Era

Thus, the AI-driven version of Alipay was not achieved overnight.

'LatePost' stated, "In terms of specific integration methods, Alipay adopted a 'dual-track' approach. On one hand, it encouraged willing merchants to proactively integrate, transforming their services into MCP/Skills directly callable by AI. On the other hand, with user authorization, AI performed 'screen-reading' operations to ensure compatibility with unmodified mini-programs."

Another example is Tencent, which launched an AI-exclusive card embedded within WeChat Pay, a payment feature specifically designed for intelligent agents. It has now been integrated with the intelligent agent WorkBuddy, covering high-frequency payment needs such as online shopping, food delivery, and afternoon tea.

Following a Dedicated Payment Route

Tang Daosheng, Senior Executive Vice President of Tencent Group, stated, "User habits have been evolving over the past 30 years, so our product teams are fully embracing these changes. For example, Tencent Docs has undergone several iterations in recent months, transforming its accumulated document processing capabilities into Skills, making them callable interfaces for WorkBuddy. This allows office users to access years of accumulated document processing capabilities while operating on a new intelligent agent platform."

It is worth mentioning that the AI-exclusive card and the AI-driven version of Alipay adopt different strategies.

The former functions as a virtual account, isolated from the main account and subject to spending limits, prioritizing security. The latter, however, reshapes service distribution logic, emphasizing its role as a super entry point.

Clearly, the AI-exclusive card adopts a conservative approach, prioritizing security in AI-driven payments, while the AI-driven version of Alipay ventures deeper, viewing AI-driven payments as a pivot for intelligent agents and embracing the Agent-native concept with an open stance.

'AIX Finance' stated, "When Taobao launched in 2003, no one dared to send money directly to strangers. Escrow transactions served as intermediaries. Today's AI Pay protocol is doing the same thing, using rules and standards to secure the foundation of the next-generation payment entrance. A delay could mean missing out entirely."

Nevertheless, AI-driven payments cannot be achieved overnight for three reasons.

First, trust issues remain unresolved.

Payment is not merely a technical issue but a matter of trust. Especially given AI's propensity for hallucinations and misunderstandings, complete trust is unwise.

Thus, even if AI successfully navigates high-frequency, low-cost commercial scenarios, final payments still require manual confirmation. This significantly diminishes the practical value of AI-driven payments, with some users even viewing it as unnecessary, preferring direct shopping on Taobao or using WeChat Pay instead.

Simply put, the inability to complete tasks in one step is the biggest weakness of AI-driven payments.

Second, cross-platform limitations exist.

For various reasons, payment interfaces developed by different platforms have long been incompatible, creating payment barriers. While this issue has largely been resolved, it has resurfaced with AI-driven payments due to the vast commercial interests involved, requiring time to coordinate.

This means that AI-driven payment chains will face cross-platform limitations in the short term.

Third, responsibility allocation remains ambiguous.

Although mainstream AI-driven payment systems have implemented self-regulatory measures to alleviate user concerns, ambiguity in responsibility allocation persists and requires further refinement.

For example, if AI-driven payments automatically deduct funds for an overpriced purchase, how should this be resolved? Different people have different definitions of 'overpriced,' so how can balance be achieved?

Another example is distinguishing between genuine and malicious refund-only requests. How can AI-driven payments differentiate between the two? When faced with malicious refund-only requests, how can merchant rights be protected?

In summary, payment methods continue to evolve, from QR code payments to facial recognition payments and now to contactless payments, culminating in AI-driven payments. Although AI-driven payments are still in their infancy and face challenges related to trust, regulations, and laws, making them unable to satisfy all users, the battle cannot wait. After all, delaying entry until the infrastructure is complete will result in higher costs, and no one wants to bear that burden.

Therefore, even if AI-driven payments are not fully operational, the battle for market entry points must continue.

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming