Half-Year In-App Purchases Reach 105 Billion: The Most Lavish Starting Point and the Most Challenging Second Half

07/14 2026

07/14 2026

502

502

Author|Mao Xinru

The financing pace in the embodied AI sector over the past six months has been nothing short of frenetic.

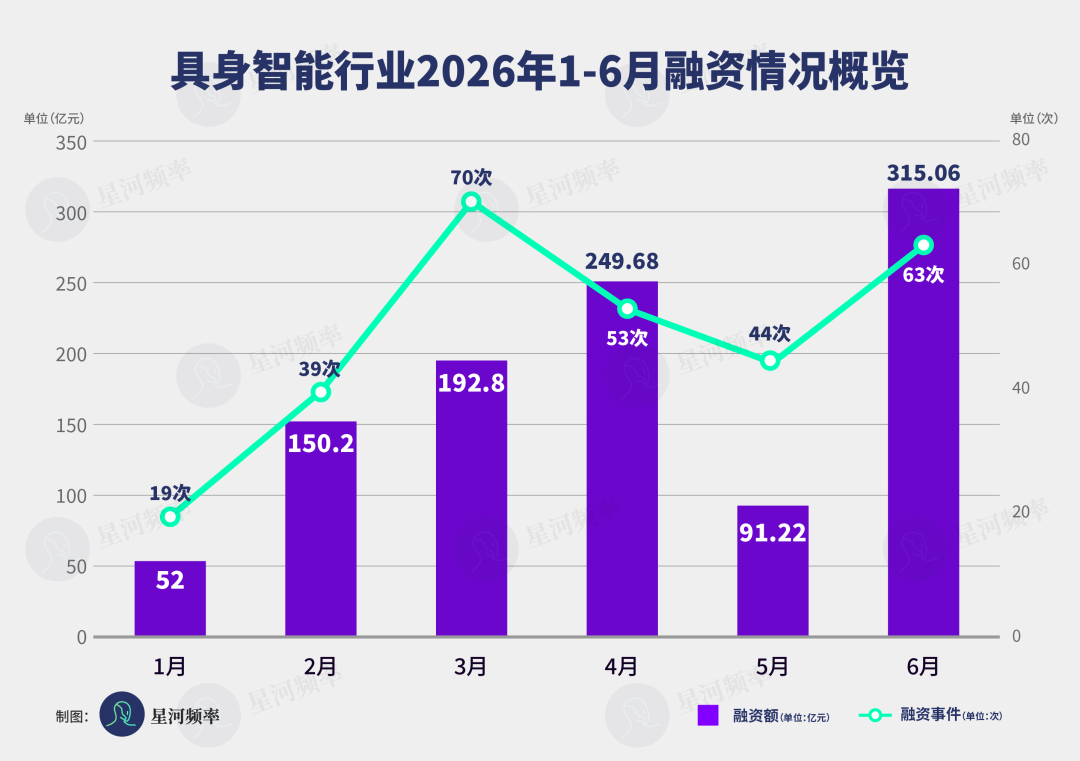

According to incomplete statistics, a staggering 105.096 billion yuan has been raised across 288 financing rounds, averaging 17.5 billion yuan per month and nearly 600 million yuan per day. This is the performance of the entire industry over six months in 2026.

Financing rounds worth a billion yuan have transitioned from being newsworthy events to daily occurrences, with companies valued in the tens of billions emerging in batches. Funding milestones for Series B, Series C, and even IPOs are being reached earlier and earlier.

The stance of capital has also evolved from exploratory strategic positioning last year to near-competitive, continuous bets.

However, this capital extravaganza is not a sign of mature industrial commercialization but rather a premium paid in advance by the capital market for the grand narrative of embodied AI replacing traditional AI and humanoid robots reshaping the ultimate future of industries.

While real money is betting on long-term potential, it also inevitably overdrafts the industry's short-term growth prospects.

Capital has set the most luxurious starting line but has also pushed the entire industry into the most challenging deep-water zone.

The ultimate test now is whether, with so much capital raised, truly functional robots can be produced.

Where Did the 105 Billion Go?

Last year, the total financing for the entire industry was 73.543 billion yuan, while this year, it has already matched last year's full-year figure in just six months, exceeding it by 40%.

The monthly pace is equally brisk. January saw 5 billion yuan, February jumped to 15 billion yuan, March reached 19.2 billion yuan, April soared to 24.9 billion yuan, May saw a brief decline, and June set a new monthly record with 31.4 billion yuan.

This does not resemble an industry still in its exploratory phase but rather a train accelerating faster and faster.

However, numbers are just the most superficial indicator.

In terms of financing volume, 113 rounds occurred in the mid-range of 100 million to 1 billion yuan, accounting for over half; 42 rounds were large-scale financings exceeding 1 billion yuan; and 55 rounds were below 100 million yuan.

This presents a standard spindle-shaped structure—large in the middle and small at both ends—appearing quite "healthy" on the surface.

But when considering the amounts, the picture changes. Twenty percent of companies secured 74% of the financing, with the Pareto principle (80-20 rule) taking the lead in the financing market.

In short, financing in the first half of this year was spindle-shaped in volume but inverted T-shaped in amount.

This is not a healthy structure but rather a clear siphon effect where leading companies dominate funding. The Matthew effect is not only present on this track but also continuously self-reinforcing at a visible pace.

Behind this pattern lies a rather rational judgment by capital: prioritizing bets on leading players with technological barriers, data accumulation, and potential for implementation, as well as rapidly rising dark horse companies.

Galaxy General, Qianxun Intelligence, Zhipingfang, Autovariable Robotics, and Xinghaitu, among others, have continuously secured large-scale financings thanks to their early technological accumulation and industrial resources.

Among them, Qianxun Intelligence completed four financing rounds between February and June, totaling nearly 5 billion yuan; Autovariable Robotics secured four rounds in just over two months, with Sequoia China, Xiaomi Strategic Investments, ByteDance, and Meituan Dragonball all participating, totaling nearly 7 billion yuan; Zhipingfang raised nearly 5 billion yuan, with its valuation exceeding 20 billion yuan.

Meanwhile, new contenders are also emerging.

Wujie Power's angel round series has accumulated over 400 million USD in financing; Sudu Technology secured 500 million USD in its Pre-A round, with CATL, Alibaba, Tencent, and Ant Group all backing it; Kunlun Xing became a unicorn in less than 90 days since its establishment, with billions in funding.

Such a pace would have been nearly unimaginable in the hard tech sector three years ago.

Further breakdown reveals that currently, the most capital-favored embodied AI companies often possess three types of characteristics simultaneously.

First, the team. The background of founding teams has upgraded from early robotics practitioners to cross-domain top-tier resume combinations.

Autonomous driving, AI large models, overseas research institutions, and serial entrepreneurship experiences have become almost standard. Capital bets, in essence, are on who is more capable of truly implementing complex systems.

Second, the business. Companies are no longer just telling stories around technological routes but must answer a more practical question: where will products be implemented, and how will they generate revenue?

Keywords like entering factories, ToB scenarios, and replacing human labor are increasingly appearing in financing narratives. To some extent, capital is no longer paying for robots that can move but for whether robots can make money.

Third, the narrative. Embodied AI remains a highly narrative-driven industry, but the narrative itself is also evolving.

Shifting from single-point capabilities to systemic capabilities, from single products to ecosystem construction. Whoever can place themselves within the framework of next-generation intelligent infrastructure is more likely to receive valuation premiums.

Thus, the financing surge in the first half of 2026 is not just a scale expansion but also a significant acceleration of screening.

Funds are no longer evenly distributed but are rapidly concentrating on companies that most resemble future winners.

Billion-Dollar Valuations and Series B Boom: The Industry Enters a Pre-IPO Phase

Another crucial clue in financing is the overall rise in valuations and financing rounds.

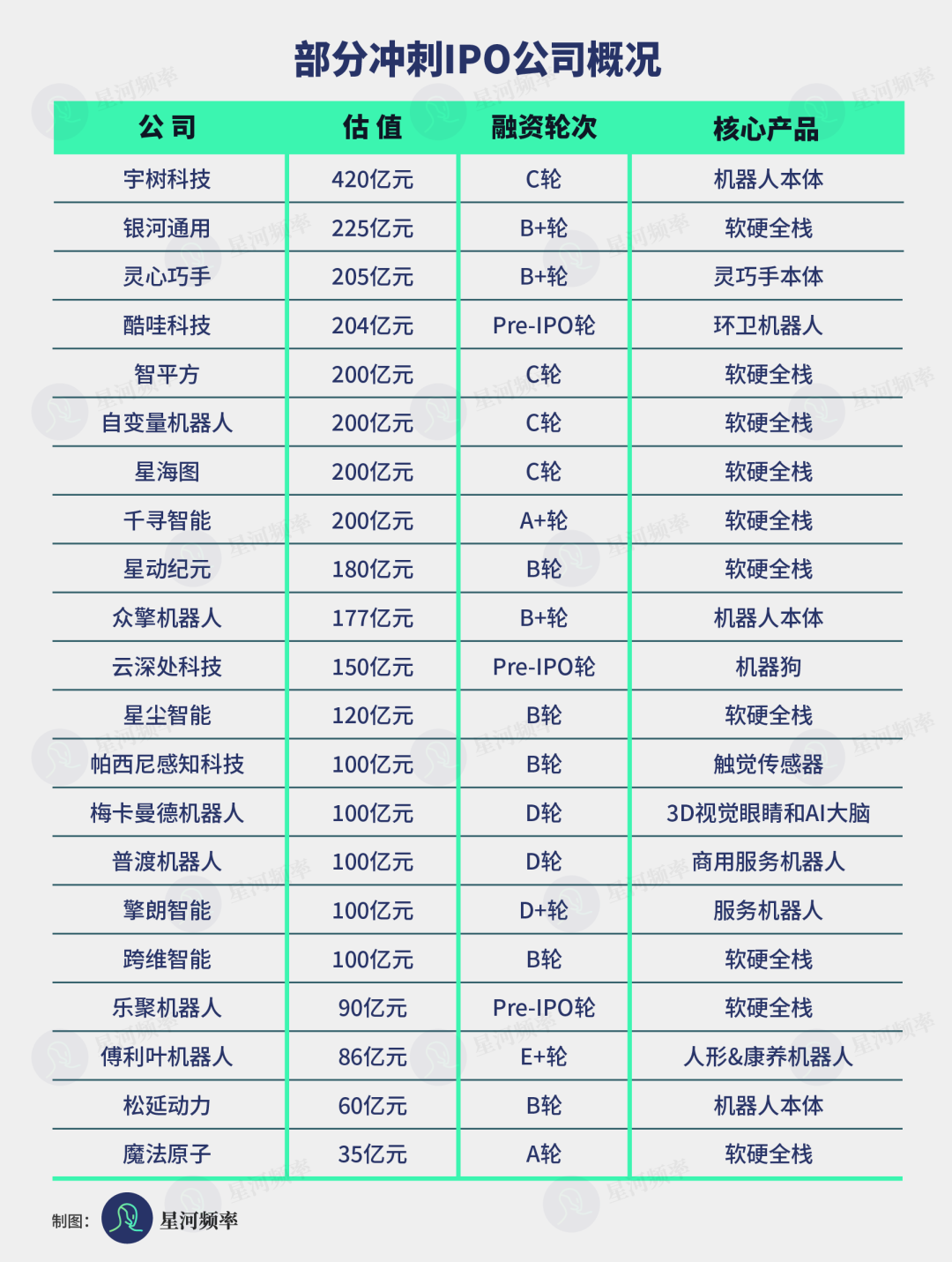

In the first half of 2026, billion-dollar valuations began to emerge in batches in the embodied AI sector, with some companies approaching or even surpassing 20 billion yuan.

Leading companies like Galaxy General, Zhipingfang, Autovariable, and Xinghaitu have already crossed the 20 billion yuan valuation mark.

Meanwhile, a group of companies preparing for IPOs has advanced to Series B financing, including Zhipingfang, Jijia Vision, Lingxin Qiaoshou, Autovariable Robotics, Zhongqing Robotics, Paxini Perception Technology, and Xingdong Era.

Among them, only Qianxun Intelligence remains at Series A+, but with a cumulative financing scale of nearly 5 billion yuan, the financing round essentially matters less.

Behind this is not just that capital is more willing to invest but also that the industry stage is changing.

First, Series B is becoming the IPO outpost for embodied AI.

In the traditional hard tech path, Series A resolves technological feasibility, while Series B begins to align with future capital market requirements, including revenue structure, customer stability, and organizational capabilities.

Once entering Series B, a company is no longer a research project but a pre-IPO asset.

This is why many companies actively introduce industrial capital and big tech resources at the Series B stage to bolster their commercialization capabilities.

Second, Series B signifies the emergence of scaling thresholds.

Unlike software, embodied AI's commercialization path is highly dependent on hardware production capabilities.

Mass production capacity, supply chain management, quality control, and after-sales systems—issues previously downplayed—will quickly become core constraints after Series B.

The expansion of financing scale is essentially paving the way for future scale-up.

Third, high valuations are beginning to serve as anchors for valuation.

When a group of billion-dollar companies emerges within the industry, the pricing logic for other companies is lifted overall.

This anchoring comes from both horizontal comparisons and competitive pressure within capital. Funds that miss out on top projects are forced to offer higher prices for secondary leaders.

However, at the same time, such high valuations are quietly altering the industry's pace.

Once a company enters the billion-dollar club, every step it takes will be magnified and scrutinized, with its commercialization speed directly determining whether valuations are sustainable.

In other words, in the first half of 2026, embodied AI is no longer an early-stage track but has begun evolving toward a stage driven by capital market expectations.

Diversifying Capital Camps: From Betting on Companies to Building Ecosystems

The capital frenzy in the embodied AI sector in the first half of 2026 is backed by the comprehensive entry of financial capital, industrial capital, and state-owned funds.

Overall, current investors in embodied AI can be clearly divided into three forces.

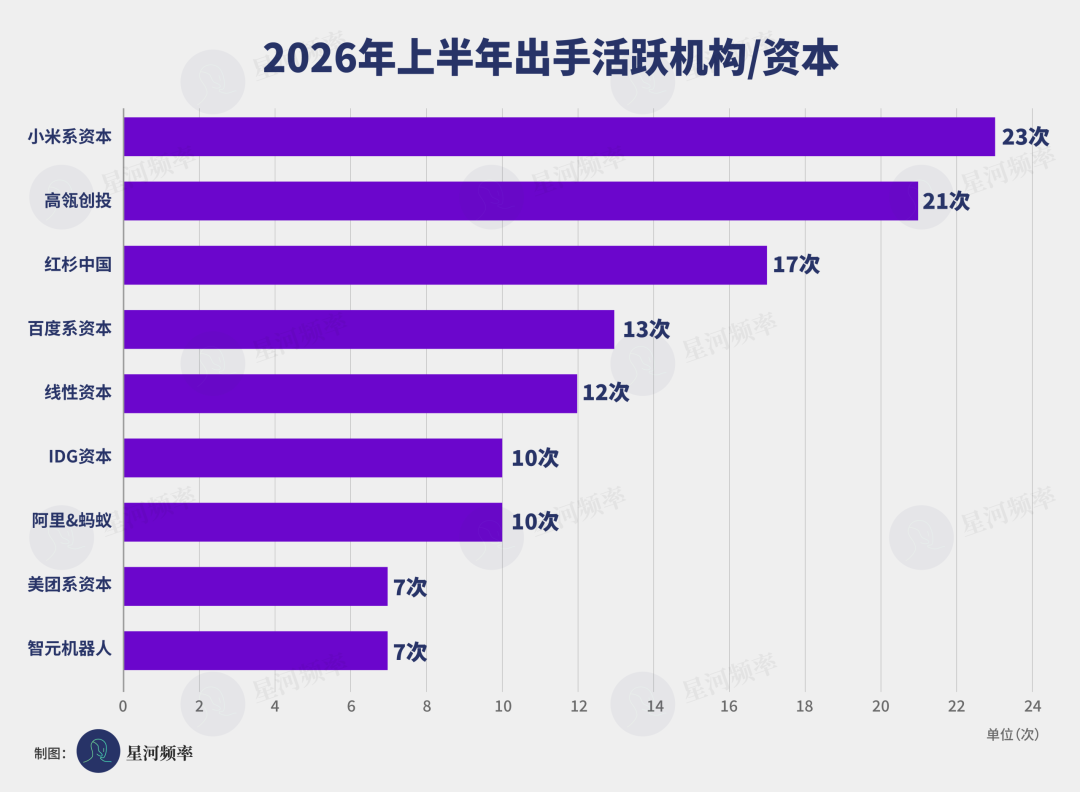

The most active investment force is capital from internet giant factions, leading the industry in frequency of bets, investment scale, and depth of strategic positioning, forming a clearly structured factional investment system.

Based on statistics from all financing events in the first half of the year, Xiaomi, ByteDance, Alibaba, and Baidu factions constitute the core investment main force in the sector, precisely positioning themselves with industry leaders and high-quality emerging targets.

Among them, Xiaomi faction capital, through Shunwei Capital and Xiaomi Strategic Investments, made the most frequent bets, with 23 moves in the first half; followed by Baidu faction capital, with 13 moves through Baidu Ventures, Baidu Strategic Investments, and Baidu itself.

For such capital, the core objective is not just financial returns but also securing future entry points and ecological niches.

Cloud service procurement, data interfaces, and computing power scheduling by invested companies may ultimately form synergies with the investors' core businesses.

Moreover, once embodied AI becomes the next-generation interaction terminal, big tech companies will naturally not be absent.

The second category is market-oriented VC and PE firms.

Among such capital, Hillhouse Venture Capital, Sequoia China, Linear Capital, and IDG Capital remain highly enthusiastic about the embodied AI sector.

These firms continue to play the role of price discoverers in the industry, driving up the valuations of leading companies through multiple rounds of follow-on investments and bets.

However, unlike the past, the space for pure financial investment is shrinking, with more firms introducing industrial resources to improve project success rates.

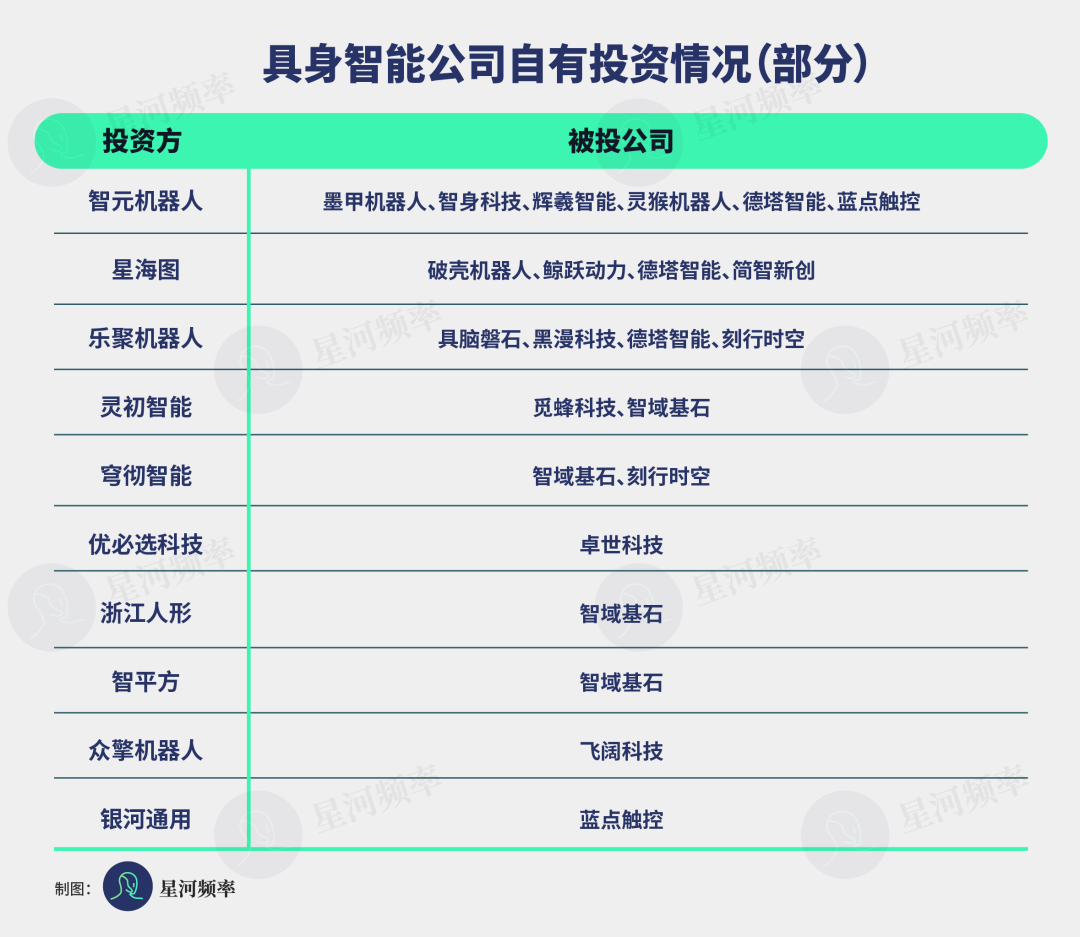

The third category, and the most noteworthy this year, is embodied AI companies themselves beginning to invest.

From publicly available information, many leading companies have participated in or led investments in data companies, sensor firms, and software platforms.

Behind this phenomenon lies a clear logic: the industry is shifting from point competition to ecosystem competition.

This trend is particularly evident at the data level.

2026 is widely regarded as the first year of large-scale data accumulation for embodied AI. Unlike large models, the data required for embodied AI must come from real-world physical interactions, with high collection costs and difficulty in standardization.

Thus, whoever controls data sources controls the upper limit of training capabilities.

In this context, leading companies actively investing in data firms are essentially locking in future training resources.

Simultaneously, by investing in upstream and downstream enterprises, they can also build supply chain and technological synergies in advance, reducing uncertainties in future scale-up.

It can be said that the role of capital is changing, shifting from investing in individual companies to investing in a combination of capabilities.

After the Frenzy: Mass Production as the Ultimate Filter

If we only look at financing data, the first half of 2026 is undoubtedly a highlight moment for embodied AI.

However, after the influx of funds, a more fundamental question arises: Can this money ultimately be converted into real commercial value?

Currently, a clear contradiction exists in the industry: on the one hand, technological demos continuously refresh perceptions; on the other hand, actual orders have not surged accordingly.

Demos trapped in exhibition halls while factories wait for orders is becoming a consensus among many practitioners.

The most intuitive manifestation is the divergence between revenue and valuation.

Take TransDimension Intelligence as a case in point: its revenue for the first half of 2026 stood at approximately 100 million yuan, with an annual target of around 300 million yuan. Yet, its valuation has already surpassed 10 billion yuan, translating to a price-to-sales ratio exceeding 30 times.

This pricing rationale is not unique to growth sectors, but it hinges on the premise of sustained, rapid revenue expansion. Should growth fall short of projections, lofty valuations can swiftly turn into a liability.

Meanwhile, mass production is emerging as the new litmus test.

The industry anticipates that 2026 will herald the inaugural year of widespread adoption for embodied artificial intelligence, with multiple firms already unveiling plans to establish production lines. For instance, IntellinSquare has declared the launch of China's first production line for embodied humanoid robots, aiming for tens of thousands of units.

However, mass production entails more than just duplicating lab prototypes; it signifies the creation of a holistic industrial ecosystem: a robust supply chain, a manageable cost framework, dependable quality benchmarks, and a thorough after-sales network.

These facets have been somewhat neglected in the financing narratives of the past year.

Once the industry transitions to mass production, financing prowess will no longer be the sole differentiator; organizational and engineering acumen will become equally vital.

Deeper challenges stem from exit strategies.

As a cohort of companies progresses to Series B funding rounds or even gears up for IPOs, primary market funds are starting to confront withdrawal pressures.

Yet, there remains considerable ambiguity regarding the capital market's capacity to uphold the valuations of hard-tech firms. Should IPO windows underperform or approval timelines stretch, this cycle of high-valuation financing could lead to a future bottleneck.

At that juncture, financial statements will undergo their inaugural public market scrutiny. Whether valuations bolstered by financing can find corroboration in revenue figures will soon come to light.

Reflecting on mid-2026, this half-year financing frenzy will have bequeathed three legacies to the embodied AI sector:

A cadre of well-capitalized frontrunners, a substantially raised valuation benchmark, and an unprecedented countdown to commercialization.

Ultimately, all participants must deliver results by 2027 that validate their lofty valuations.

The financing window will not remain ajar indefinitely, and the secondary market's patience is even more finite. When subsidy-driven rationale recedes and performance-driven logic takes precedence, the embodied AI industry will witness the emergence of clear winners and losers.

The culmination of this competition will not be a thriving ecosystem but rather a ruthless culling process.

Most contenders will be weeded out under the combined pressures of mass production and commercialization, with only a select few companies managing to bridge the chasm from financing to profitability.

The financing surge of the first half of 2026 merely lays the groundwork.

The true narrative commences with mass production and will ultimately culminate in the success or failure of commercialization.

-

![]()

The Voice in AI Hardware Industry is Quietly Shifting Amid Brain Drain

-

![]()

AI Enters Second Half: Buy the 'Cloud,' Not the 'Chip'?

-

![]()

Breaking the Monopoly! Trillion-Parameter Large Model Adopts Domestic Chips, Marking a Key Step Towards 'De-NVIDIA-ization' in AI Computing Power

-

![]()

Performance Drops Sharply, Seres Alerts 280,000 Shareholders

-

Behind the AI Boom: US Rakes in $314 Billion, South Korea $223 Billion, While China Lags at $26 Billion?

-

![]()

Volkswagen's 'Drastic Measures' to Cut Half of Its Models: Will China's Three Joint Ventures Be Affected?

-

![]()

It's already crowded in car manufacturing, yet Chunnan insists on joining in.

-

Confirmed: Fossil Fuel Vehicle Ban! Hainan Unveils New '15th Five-Year Plan', Weakening Passenger Vehicle Sector and Initiating Petroleum Asset Depreciation