From Stacking Parameters to Balancing the Books: The Commercial Turning Point for AI Draws Near | Business Wave

07/16 2026

07/16 2026

379

379

Editor | Yang Xuran

Like nearly all commercial sectors, AI, as an industry, has reached its own watershed moment this year.

Doubao and WorkBuddy have begun testing paid services, while ChatGPT and Anthropic have validated the token subscription model overseas. Companies like UBTECH, Unitree, and Tashi Zhihang are also exploring practical applications for humanoid robots.

Judging by the consistent actions of key players, the critical period for AI commercialization is approaching. Especially after the industry collectively navigates through the 'valley of death' for large models, the focus has shifted to generating revenue.

In 2026, the Scaling Law, which the industry once followed, has hit a wall: the benefits of simply accumulating computing power and increasing data volume to enhance model capabilities are diminishing. Spending billions of dollars to train the next generation of super-large models has not resulted in significant performance leaps.

"For a startup, betting massive resources on training models with ultra-large parameter scales is not a pragmatic choice due to the extremely low cost-effectiveness," Li Kaifu once reflected.

In the capital markets, investors are no longer rushing to assign equally high valuations. The stock price divergence between Zhipu and MiniMax, along with Kimi's frequent financing, illustrates this point.

At this juncture, the AI industry chain is moving away from '0 to 1' and seeking the '1 to 100' commercial inflection point. All judgment and evaluation criteria are changing.

This article is a in-depth valuable piece from the Business Wave content team. Feel free to follow us on multiple platforms.

The Wall

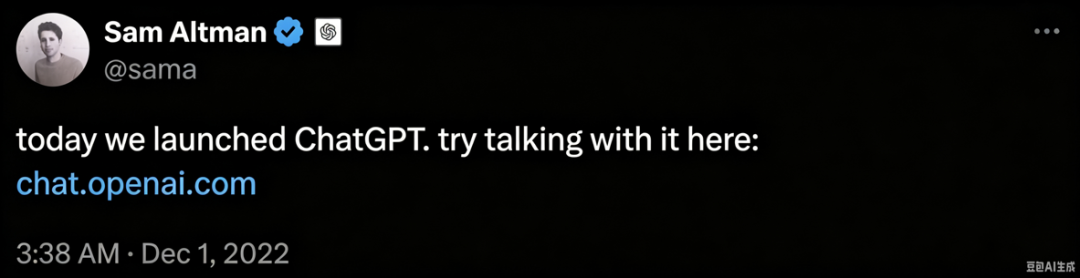

In the early morning of November 30, 2022, Sam Altman quietly posted a tweet: ChatGPT was officially launched. At that time, OpenAI was still a small startup known only to a few insiders, and Altman did not have high expectations for the initial version of GPT. However, just five days later, the goal of 1 million users was easily surpassed; two months later, over 30 million users flocked to ChatGPT.

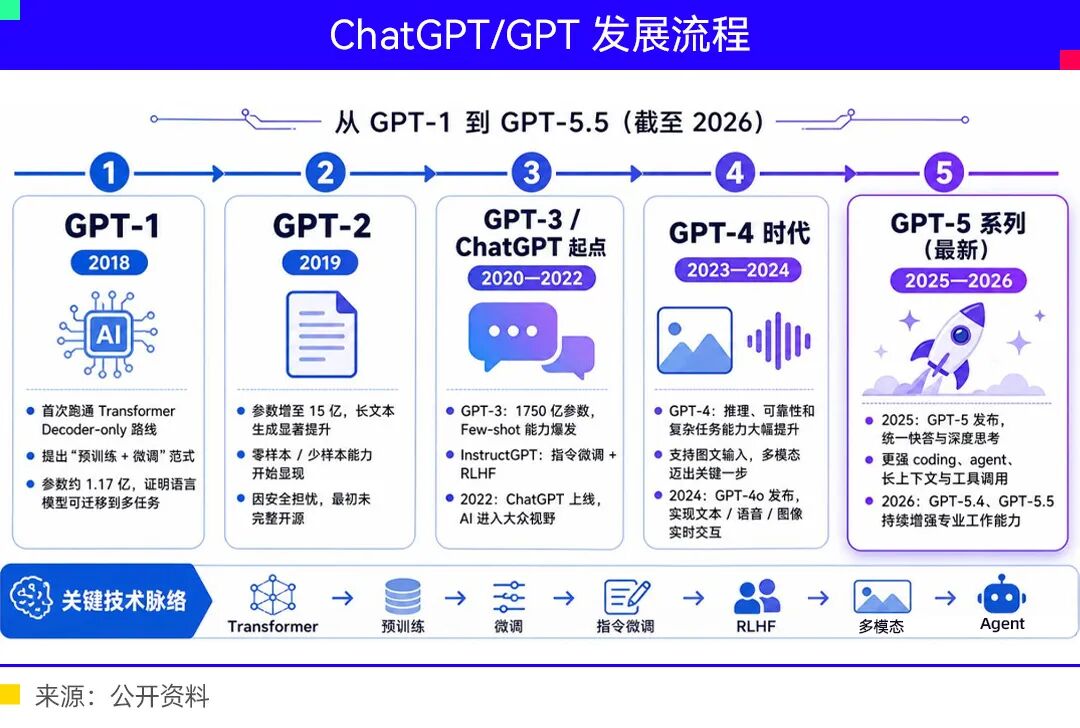

As early as 2020, OpenAI proposed the Scaling Law: the larger the training parameters and the more computing power, the better the model performance. Over the next three years, AI large models advanced along this path, with those having more parameters, greater computing power, and higher benchmark scores securing more financing and higher valuations. From GPT-3's 175 billion parameters to GPT-5.6 Sol's approximately 3 trillion (3T) total parameters, 'stacking parameters' became the industry's development creed.

Anthropic took this to the extreme, with its 'too powerful to disclose' Mythos model boasting 10 trillion parameters and an estimated training cost of $10 billion.

The tech giants simultaneously unleashed their 'money power' to hoard chips. It is estimated that Meta alone possesses more GPU computing power than all AI companies in China combined, while Google's total AI computing power is equivalent to 5 million NVIDIA H100s, accounting for a quarter of the global total.

However, the issue arises when funding and computing power chips hit bottlenecks, causing the growth curve of large model performance to flatten. For Chinese companies, which face restrictions on high-end chips and have insufficient financial reserves, there is a greater need to reevaluate the Scaling Law.

Early last year, Li Kaifu, founder of 01.AI, reflected, 'We have realized the diminishing marginal returns of the Scaling Law. Betting massive resources on training models with ultra-large parameters is not a pragmatic choice for startups due to the extremely low cost-effectiveness.'

01.AI subsequently shifted its approach, with Yi-Lightning adopting a Mixture of Experts (MoE) architecture, activating just over 20 billion parameters while achieving superior model performance. DeepSeek also leveraged MoE architecture optimization, open-source strategies, and distillation techniques to achieve training costs less than one-twentieth of ChatGPT's.

Abandoning the pursuit of super-large models in favor of creating 'small but beautiful' pragmatic products may be the consensus among Chinese large model companies after experiencing the 'hundred-model battle' and 'price war.' The shift from 'building larger models' to 'using models to create profitable businesses' signifies that the era of geek-driven innovation is giving way to commercial pragmatism.

Closed Loop

Although the competitive strategies for large models in China and the U.S. differ, they converge at the commercialization level.

On June 24, ByteDance's Doubao officially introduced a paid model with three subscription tiers: Standard at 68 RMB/month, Enhanced at 200 RMB/month, and Professional at 500 RMB/month. The charge (paid) model is backed by staggering cost expenditures: as of March 2026, Doubao's average daily token usage surpassed 120 trillion, doubling in the past three months and reaching 1,000 times the volume since its initial launch in May 2024.

Zheshang Securities estimates that ByteDance's capital expenditures in 2025 will reach approximately 150 billion RMB, with 90 billion allocated for AI computing power procurement, resulting in daily expenditures of 438 million RMB. However, Doubao's exploration of the 'AI + e-commerce' model currently generates only limited revenue, making income from the Professional tier even more critical.

Around the same time, Tencent also accelerated its commercialization efforts. Its Buddy AI (including WorkBuddy, CodeBuddy, etc.) announced subscription upgrades, effective July 1, with three pricing tiers: Standard at 99 RMB/month, Premium at 199 RMB/month, and Flagship at 999 RMB/month.

The direct driver of the paid model is the explosion in usage. WorkBuddy saw a tenfold increase in per-user token consumption within three months. Although Tencent emphasizes that AI remains in its 'strategic investment phase,' the launch of the paid model confirms that as AI services transition from novelty to high-frequency use, cost expenditure characteristics will force the formation of a commercial closed loop.

Across the ocean, OpenAI adopted a multi-pronged approach, introducing a combination of 'advertising + subscription + token-based payment.' In February 2023, it launched the Plus subscription (20 USD/month) and this year introduced the more affordable ChatGPT Go (8 USD/month), with paid users increasing from 47 million at the end of last year to 55 million in the first quarter.

ChatGPT even plans to offer advertising services to business owners, charging free and Go users based on impressions.

Despite these efforts, its revenue still cannot cover massive cost expenditures, resulting in prolonged losses.

Anthropic developed a unique business philosophy: focusing on government and enterprise clients, with no free tiers, no advertising, and no price reductions. Starting in April, it banned subscription quotas for third-party tools like OpenClaw, forcing users to adopt API-based pay-as-you-go models, thereby filtering high-value users from subscription models into enterprise channels.

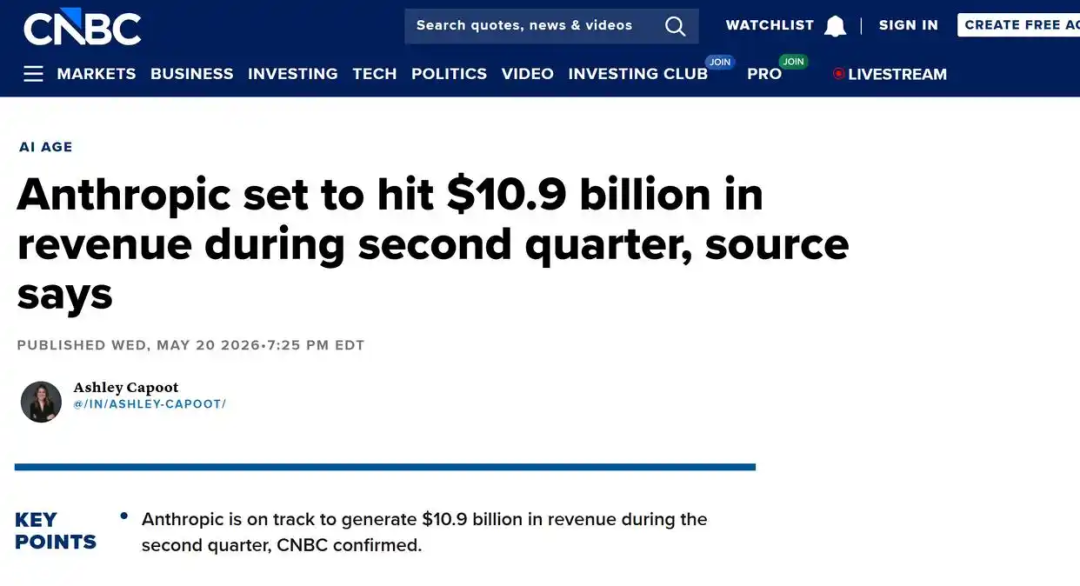

By the end of 2025, Anthropic's Annual Recurring Revenue (ARR) reached approximately 9 billion USD, swelling to 30 billion USD by April 2026. In February, only over 500 companies were willing to pay more than 1 million USD annually, but by early April, this number exceeded 1,000.

At the Code with Claude conference, Dario Amodei stated that the company had initially prepared for up to 10x annual growth, but revenue and usage growth rates reached 80x in the first quarter (annualized).

Superior product strength and unique business strategies helped Anthropic's revenue (projected) rise to 10.9 billion USD in the second quarter of this year, while achieving an operating profit of 560 million USD. It is poised to become the first profitable global large model company, with its valuation nearing 1 trillion USD.

Overall, competition in the AI industry chain has shifted from pure performance battles to an era emphasizing commercialization.

Divergence

Valuation benchmarks for AI companies in primary and secondary markets are shifting from technical capabilities to commercial capabilities, leading to divergent valuations among firms.

The most notable case is Zhipu and MiniMax. These two large model companies, which went public around the same time, have recently seen Zhipu's valuation reach approximately 10 times that of MiniMax, drawing significant attention.

Initially, the market favored MiniMax's multimodal and consumer-facing AI applications, while Zhipu's narrative of localized government and enterprise deployments was less appealing to investors.

Just three months later, their performances completely reversed. On July 9, MiniMax faced a 'lock-up expiration' test, with its stock price plummeting 18% that day and continuing to decline sharply, falling 83% from its mid-March peak and losing approximately 340 billion HKD in market value. Zhipu, whose lock-up expired the day before, remained resilient, surging 30% over two consecutive days.

Looking back, the turning point in their market performances occurred on June 1 this year.

On that day, MiniMax released the M3 model, switching from a subscription model to token-based billing. Negative sentiment soon emerged: the company canceled the 29 RMB/month Starter plan without user consultation. Developers reported that token consumption far exceeded expectations for equivalent tasks, with costs rising from 49 RMB to 175 RMB in high-token scenarios.

Users dubbed this behavior a 'betrayal-style' price hike, causing MiniMax's stock price to plummet 16% that day. Yan Junjie promptly announced he would forgo his salary and allocate 4% of his personal shares for talent incentives.

However, short-term promotions attempting to retain users with low prices failed to meet expectations after the promotion ended, leaving MiniMax facing the dual dilemma of 'unable to raise prices or retain users.'

Since June, the narrative logic in the large model sector has accelerated toward Vibe Coding and Agents, with Anthropic leading the way and to B (business-oriented) capabilities gaining investor favor. In contrast, Zhipu's GLM-5.2 not only delivered strong performance but also increased API call pricing by 83% in the first quarter, with call volumes still growing 400% and even facing supply shortages.

The degree and effectiveness of commercialization in the AI field are now directly linked to capital market valuations. From this perspective, those still obsessed with AI as purely a 'geek' domain need to reevaluate the entire industry.

Commercialization is equally critical in AI terminals.

Beyond large models, intelligent driving is seen as the first commercial sector where AI will be widely implemented and the fastest pathway to physical AI applications. Indeed, commercial applications in this field are rapidly maturing.

Compared to humanoid robots, intelligent driving offers more practical advantages. First, market demand is clearer, with well-defined payment scenarios. High-frequency travel needs drive willingness to pay for assisted driving features, and ride-hailing platforms are eager to deploy autonomous driving technologies. Second, hardware and software can be mass-produced to standard specifications, enabling cost reductions through scale and clarifying the commercial closed loop. Moreover, once vehicles are on the road, they form a natural data collection flywheel, with real-world driving data aiding AI algorithm iteration and continuously improving product experiences.

Currently, high-level assisted driving (L2/L2+) pre-installed in consumer vehicles has become almost essential for new energy vehicle brands, with Tesla's FSD and Huawei's ADS (Qiankun Intelligent Driving) leading the sector. Meanwhile, Level 4 autonomous driving (Robotaxi, autonomous freight, etc.) is also approaching commercialization, with Baidu's Apollo Go, WeRide, Momenta, and Waymo actively deploying their services.

Smart glasses are also maturing. Previously, products like Humane AI Pin and Rabbit R1 gained temporary popularity but ultimately failed due to lacking commercial ecosystems. Today, Meta's Ray-Ban smart glasses have succeeded thanks to a mature ecosystem, selling over 7 million units in 2025 and targeting production capacity of up to 20 million units this year.

Summary

The shift from 'showcasing skills' to 'selling products' represents the shared expectations of capital, markets, and even consumers for the entire AI industry chain.

We observe that from the primary market paying for 'imagination' to ARR becoming the valuation anchor, the entire AI sector is undergoing a profound transformation from 'geek culture' to 'commercial integration'.

The year 2026 is destined to be a pivotal year for AI's transition from technological validation to large-scale commercial adoption, a path that all emerging tech industries in commercial history have traversed.

-

![]()

The Dead End of GoPro: Unveiling the Decisive Factors in DJI and Insta360's Competition

-

![]()

The Dead End for GoPro: Unveiling the Key to Victory in DJI and Insta360's Competition

-

DeepSeek Targets A-share IPO Amid RMB 480 Billion Valuation Debate

-

![]()

WPS Meitu XiuXiu: The Threat to Its Market Position from AI Large Models

-

![]()

After Seres Reports Losses, What Is the Capital Market Really Worried About?

-

![]()

Honor, Stepfun, and Nubia Vie for 'Pioneering' Status: The Fierce Contest Among AI-Powered Smartphones

-

![]()

Glory, Stepfun, and Nubia Vie for the Pioneering Position: AI-Powered Smartphones Engage in Intense Competition

-

![]()

Apple AI Gains Approval but Faces Outdated Challenges