TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

07/16 2026

07/16 2026

502

502

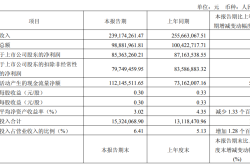

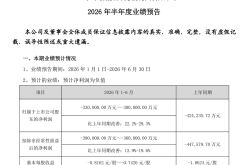

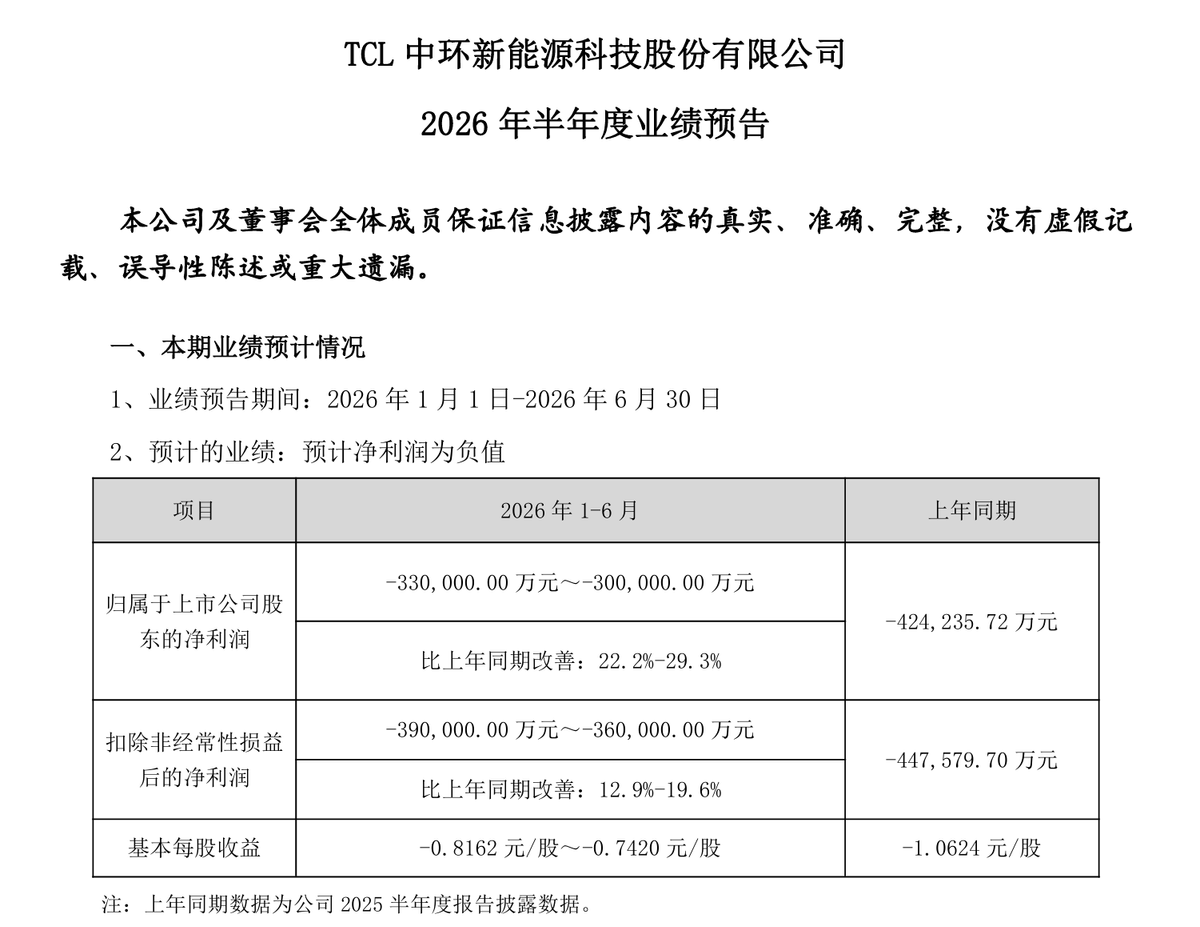

On the evening of July 13, TCL Zhonghuan unveiled its performance forecast for the first half of 2026, projecting a net loss attributable to shareholders ranging from RMB 3 billion to RMB 3.3 billion.

At first glance, this is clearly not a report card that would thrill the market. However, when viewed through the lens of two key comparisons, the significance of these figures shifts. Compared to the same period last year, losses have decreased by 22% to 29%. Furthermore, compared to the first quarter, losses in the second quarter have continued to shrink sequentially by nearly 9%. Against the backdrop of accelerated consolidation across the entire photovoltaic supply chain, this reduction in losses itself sends a significant signal.

Over the past two and a half years, the domestic photovoltaic manufacturing sector has been undergoing consolidation. TCL Zhonghuan's losses in 2024 and 2025 were primarily attributable to its massive silicon wafer production capacity and sluggish adjustments in utilization rates, resulting in significant short-term impacts.

However, amid these changes, the company has made a series of strategically significant adjustments for the long term. These include accelerating its expansion into downstream module production to absorb silicon wafer capacity, massively expanding its overseas markets to alleviate concentrated competition, and leveraging mergers and acquisitions during the industry downturn to make a significant bet on next-generation BC technology.

Meanwhile, a semiconductor silicon wafer business, which has been overshadowed by the photovoltaic narrative for years, is quietly contributing positive profits. This business is experiencing a simultaneous increase in volume and price amid the global rise in 12-inch silicon wafer prices. From TCL Zhonghuan's trajectory, we can discern not only marginal improvements at the corporate level but also early signs of the entire industry transitioning from disorderly consolidation to orderly integration.

I. The Logic of Improvement in the Photovoltaic Market Has Shifted

Historically, each round of consolidation in the photovoltaic industry has been driven by different dominant factors. The consolidation in 2012-2013 was triggered by a demand-side shock, with macroeconomic market disruptions overlapping a sharp decline in global installation demand, washing out second- and third-tier companies with thin profit margins. The consolidation in 2018 stemmed from the end of subsidy incentives. A common feature of these two rounds of consolidation was their swift onset and resolution. In fact, many companies survived, and most resumed profitability.

However, the current round of consolidation, which began in 2023, is fundamentally different. Perhaps precisely because there were too many companies in the market previously, the expansion of photovoltaic manufacturing capacity over the past three years has far outpaced the growth in global installations. Capacity scales for silicon wafers, cells, and modules all exceed twice the global demand.

Industry observers have long recognized that the key to consolidation is no longer waiting for demand to recover but waiting for supply to consolidate. Sufficient capacity must be permanently shut down or exited for supply and demand to rebalance.

Public data shows that global photovoltaic module capacity was approximately 50GW in 2012, with about 20% of capacity exiting after consolidation, and relative balance was restored in about 18 months. By 2026, the capacity base had exceeded 1,000GW, and even if 30% of capacity exits, the remaining capacity would still far exceed global demand. This marks the first time in the photovoltaic industry's history that consolidation is occurring against such a massive capacity base.

At this juncture, every detail that might be associated with positive signals becomes particularly important.

TCL Zhonghuan's loss reduction is a case in point. According to the announcement, the narrowing of losses in the first half of the year primarily resulted from efforts in three areas: non-silicon costs for silicon wafers decreased by more than 13% year-on-year, revenue from the module segment increased by nearly 40% year-on-year, and partial silicon wafer capacity was absorbed through self-production and self-use. Additionally, overseas module shipments increased fourfold year-on-year.

As long as the company is actively adjusting its cost structure, product mix, and market structure to reduce losses, it implies that there is greater room for coordination within the industry. Previously, the market's concern was that the entire industry was too passive, lacking strategic flexibility and unwilling or unable to proactively achieve effective regulation.

However, in the face of such a prolonged cycle, the current landscape is far from reaching its conclusion. The reasons for this have been extensively discussed in the industry. When prices fall below the cash costs of most companies, theoretically, a significant amount of capacity should exit. In practice, however, there are too many instances of artificially prolonged exit periods, leaving only time to create space.

The good news is that TCL Zhonghuan's overall operating conditions are controllable, with its operating cash flow remaining positive in the first quarter of 2026, giving it greater endurance than competitors relying solely on external funding.

II. Integration and BC Transformation: More Than Just Following Trends

A persistent issue in the photovoltaic manufacturing chain is profit distribution. During industry upswings, upstream polysilicon and silicon wafer companies capture most of the profits. During downturns, the module segment, closest to end users, enjoys relatively thicker profit margins—not because modules are highly profitable but because upstream advantages have diminished.

This cyclical shift in profit gravity often prompts silicon wafer and cell companies to accelerate their expansion into downstream segments during industry downturns, not for offensive purposes but for defensive ones. When silicon wafers are hard to sell, having a module channel to absorb them is essential.

TCL Zhonghuan exemplifies this logic. In the first half of 2026, revenue from its battery and module business accounted for more than 50% of total photovoltaic revenue for the first time, with overseas module shipments increasing fourfold year-on-year.

Additionally, on July 2, TCL Zhonghuan officially completed its strategic acquisition of DAO Solar, using capital to swiftly fill its downstream manufacturing capabilities from cells to modules. After the acquisition, it announced an investment of RMB 2.6 billion to retrofit production lines for the BC technology route, indicating that this is not just capacity expansion but a proactive technological positioning.

Why BC? In the TOPCon race, TCL started late and had a weak brand foundation, relying solely on price leadership to capture market share in module tenders, which clearly cannot support long-term sustainable operations.

From publicly available information, TCL Zhonghuan's TOPCon module quotes have been low in multiple centralized procurement projects by central enterprises, several cents lower than those of first-tier companies. This does not align with the company's long-term healthy development needs, and BC technology offers a window for differentiated competition. If it can achieve low-cost mass production on the BC route first, it can shed its low-price label in the module segment and migrate toward high-end and overseas premium markets.

Of course, the core challenge of BC technology lies in the lengthy engineering ramp-up required to transition from laboratory efficiency to scalable mass production. Leading companies in the industry have each taken at least one to two years to achieve relatively stable mass production. From a broader industry integration perspective, TCL Zhonghuan's acquisition of DAO Solar and its full pivot to BC reflect a microcosm of the "post-integration era" consolidation underway in the entire photovoltaic industry.

Like most manufacturing industries, the dominant narrative in photovoltaics has been specialized division of labor—polysilicon, silicon wafers, cells, and modules each operate independently, earning profits from their respective segments. However, intense competition exposes the most vulnerable aspect of specialized division of labor: when supply exceeds demand, companies in single segments lack buffer space.

For example, if silicon wafers are hard to sell, they simply are; if cells face price pressure, they do; upstream price fluctuations translate directly into losses downstream. In contrast, integrated companies can absorb price fluctuations internally, adjust capacity coordination across multiple segments, offset silicon wafer losses with module revenue, and wait for the industry to recover.

Thus, integration may not be the most efficient solution, but it is the best survival solution. It is through such resource aggregation that companies can better control their costs and navigate the prolonged industry consolidation process.

III. The Semiconductor Assets Overshadowed by the Photovoltaic Narrative

When discussing TCL Zhonghuan, most market analyses label it as a "photovoltaic silicon wafer company." This label has influenced its valuation trajectory in recent years. However, both its performance forecast and its strategic business layout reveal a highly valuable business asset: semiconductor silicon wafers.

After all, "Zhonghuan" originated from the Tianjin Semiconductor Materials Factory established in 1988, with its semiconductor business predating its photovoltaic business. Today, this segment is independently operated by its subsidiary, Zhonghuan Leading, which generated approximately RMB 5.7 billion in revenue in 2025, up nearly 22% year-on-year, with a gross margin of about 19%, achieving a positive gross profit of over RMB 1 billion.

For comparison, another STAR Market-listed company, National Silicon Industry Group, which focuses on semiconductor silicon wafers, reported only about RMB 3.7 billion in silicon wafer revenue during the same period, with a negative gross margin. Currently, National Silicon Industry Group has an enterprise value of approximately RMB 130 billion, while Zhonghuan Leading's revenue is 1.55 times larger and already profitable. TCL Zhonghuan holds approximately 33% of Zhonghuan Leading's shares.

Using the most conservative revenue-based valuation, the overall value of Zhonghuan Leading alone exceeds RMB 200 billion, with TCL Zhonghuan's stake valued at nearly RMB 70 billion. Yet, as of recently, TCL Zhonghuan's total market capitalization as a listed company is only around RMB 37 billion.

This suggests that the market has priced TCL Zhonghuan as if its photovoltaic business were a negative asset, while almost entirely ignoring the value of its semiconductor silicon wafer business. Although such pricing logic is not uncommon in secondary markets, it does not necessarily make it correct.

This cognitive dissonance has its causes. The photovoltaic business, with its large scale and deep losses, naturally dominates investor attention. The semiconductor silicon wafer business has not been independently listed, lacking a direct market price anchor. Additionally, the overall photovoltaic sector is mired in extreme pessimism, with the valuations of any companies associated with photovoltaics being uniformly pressed down.

However, the global semiconductor silicon wafer industry is currently in a clear upswing. In May, giants such as Shin-Etsu Chemical, SUMCO, and GlobalWafers uniformly raised prices for 12-inch silicon wafers by 5% to 8%, with higher increases for premium wafers used in AI computing. The multi-layer stacking processes of HBM high-bandwidth memory chips and the wafer bonding processes of 3D flash memory chips continue to increase silicon wafer consumption, providing a solid demand foundation for this round of price hikes.

Thus, while the semiconductor silicon wafer upswing cannot solve the problems of the photovoltaic business—the funding systems of the two segments are relatively independent, and semiconductor profits cannot directly subsidize photovoltaic losses—the existence of semiconductor assets at least provides TCL Zhonghuan with a dual value anchor. It supports its valuation floor during the photovoltaic industry's darkest hours and offers profit elasticity once the industry recovers.

The gap between its sustained profitability and its nearly zero valuation weight in current pricing constitutes an intriguing disjunction.

The cyclical history of the photovoltaic industry has repeatedly proven: during high-growth periods, corporate value is measured by profit scale; during consolidation periods, it is measured by asset quality. Although TCL Zhonghuan's interim report still shows losses, the continuation of its loss-narrowing trend, structural breakthroughs in downstream modules and overseas markets, and the value floor provided by its semiconductor assets are all releasing positive signals. The night is not yet over, but the horizon is whitening, and it is time to look ahead.

Source: Songguo Finance

-

![]()

Is Tencent AI Heading in the Right Direction?

-

Latest Update! Jinding Optics’ GEM IPO Review Now “Under Inquiry”

-

![]()

VOYAH’s CBO Sets Ambitious Target: Secure Top 3 Spot in Luxury BEV Market Within Two Years, Launch 4 New Models to Cover All BEV Segments

-

![]()

Sehwa Technology Invests 740 Million Yuan, Eyeing the Lucrative Optical Film Market!

-

![]()

150 Million Users, $40 Million ARR: AIShige Technology Enters the Final Round of AI Video Competition

-

![]()

StepOn Star Forays into Smartphone Manufacturing: A Rationally Sound Yet High-Risk Endeavor

-

![]()

TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

-

![]()

Forty Years On: From Volkswagen’s State-Backed Entry into China to BYD’s Hiring of a Former European Foreign Minister