After Kuaishou's Kling Secures $20 Billion in Funding, Cheng Yixiao 'Yields Seat' to Gai Kun

07/17 2026

07/17 2026

345

345

In the late hours of July 2, Kuaishou filed a 38-page announcement with the Hong Kong Stock Exchange, carving out an AI business previously consolidated within the group's financial statements into a standalone entity that can be separately valued by the capital markets.

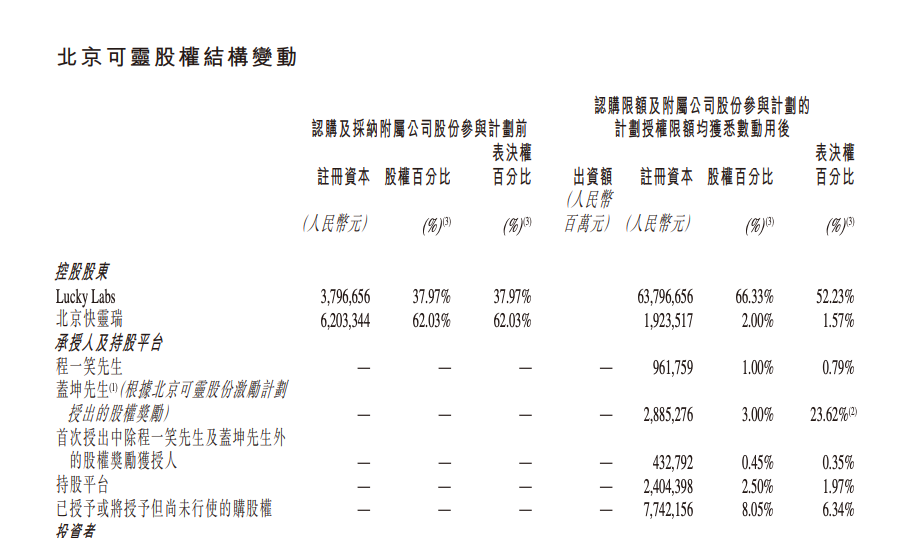

The market's first focus was on the money. The announcement disclosed locked-in subscription amounts of approximately RMB 19.047 billion, with an additional RMB 1.4 billion reserved for subsequent investors, bringing the total subscription ceiling to RMB 20.447 billion (approximately $3 billion). Signed investors span state-owned capital, industrial capital, and private equity firms, with even the "BAT" trio rarely appearing together. Based on a pre-money valuation of $15 billion, Kling's valuation would reach approximately $18 billion once all funds are in place. Calculated against the closing market capitalization on July 2, this equals roughly three-quarters of Kuaishou's total Hong Kong-listed market value.

The valuation provides market pricing clarity, while voting rights offer a new governance model. Under a fully diluted basis after utilizing the subscription ceiling and share participation plan, Kuaishou's ecosystem still holds approximately 68.33% of Kling's equity and around 53.8% of voting rights. Investors hold about 16.7%, with up to 15% reserved for employees and core management.

Notably, Kuaishou founder and CEO Cheng Yixiao acquired a 1% equity stake at zero cost, corresponding to 0.79% voting rights. Kling AI division head Gai Kun received a 3% stake with tenfold voting rights, currently translating to 23.62% voting power. Additionally, he gained a 1% share option, which, if exercised, could designate shares with tenfold voting rights. Such a structure is rare in subsidiary governance among major corporations.

The tenfold voting rights deeply bind Gai Kun to the CEO role. All special voting rights automatically lapse if Gai Kun ceases to be Kling's CEO; if he transfers shares, the corresponding special voting rights terminate. The equity arrangement includes restrictions: relevant shares cannot be disposed of for at least three years and prior to Kling's IPO.

Over the past two years, Gai Kun has made several costly strategic choices for Kling. Initially, failure costs were absorbed by Kuaishou's group budget; post-funding, strategic decisions, incentives, and outcome constraints are embedded in equity, voting rights, and repurchase agreements. Two years ago, he led a project competing for computational resources within Kuaishou; now, he oversees a $18 billion-valued company with an IPO deadline.

After the 2024 Spring Festival, Kling's team gathered in a Kuaishou office in Beijing's Xierqi district to discuss responding to OpenAI's Sora.

A report on the team's early days labeled the room "1405." OpenAI had just released Sora's demo video, showcasing generative models handling extended motion, camera work, and physics. Domestic teams faced a stark choice: continue refining existing technology or rebuild a video generation pipeline from scratch.

Gai Kun chose the latter, predicting OpenAI would temporarily refocus on language models, creating a several-month market window. By his recollection, the team aligned technically within days post-Spring Festival, pivoting fully to DiT and aiming for full model-to-product readiness by May. Kling launched on June 6, despite lacking sufficient top-tier NVIDIA GPUs, relying partly on AMD and other vendors' chips. Gai Kun's goal was to launch a user-friendly product before Sora's public release.

On June 6, 2024, Kling 1.0 debuted as one of the earliest video generation products open to general users, directly competing with Sora. This timing elevated Kling's status within Kuaishou, transforming it from a resource-constrained experimental project into Kuaishou's primary gateway into video generation model competition.

The first strategic choice was relatively clear. Sora had set the direction; Kling needed to catch up swiftly and transition demos into products.

By 2025, Kling had secured users, revenue, and industry positioning. The team could either enhance image quality and stability along established text-to-video and image-to-video paths, with predictable product feedback for each improvement, or overhaul the model's input-output framework to integrate motion, sound, reference images, and video editing into a unified system. The latter meant starting anew.

Existing capabilities had to be dismantled, new technical paths lacked complete solutions, and the team risked slowing iterations on current products. Gai Kun ultimately chose an All-in-One approach. Subsequent releases, Kling O1 and 3.0, progressively unified generation, reference, editing, audio, and video into a multimodal system. Kuaishou's Q1 2026 results showed Kling 3.0 supporting full-modal input-output for text, images, audio, and video.

These pivotal strategic shifts illuminate the rationale behind special voting rights: Kuaishou aims to retain not only Gai Kun's executive prowess but also his ability to make directional judgments when technical paths remain uncertain.

In recommendation, growth, and commercialization, Kuaishou has long relied on data feedback, A/B testing, and internal competitions to resolve issues. However, video large models entail higher training costs and longer validation cycles, precluding decisions pending complete data. Gai Kun frames this shift as moving from "experiment-driven" to "vision-driven": a few propose directions, then resources concentrate on validation.

In April 2023, Kuaishou established the Kling AI division, reporting directly to founder Cheng Yixiao—Kuaishou's only new first-tier business unit in three years. That August, Gai Kun additionally assumed technical leadership, unifying product, algorithm, and R&D processes.

Special voting rights formalize this organizational approach into the company structure. Gai Kun's 3% stake carries tenfold voting rights. As long as he remains Kling's CEO, this stake provides 23.62% voting power; upon his departure, all special voting rights lapse; if he transfers shares, only the transferred portion reverts to ordinary voting rights.

Tenfold voting rights, in a sense, institutionalize the shift from "betting on probability through volume" to "betting on direction through judgment." This conditional authorization doubles as a clearer accountability framework. Kuaishou retains ultimate control, while Gai Kun gains greater strategic influence than a typical professional manager.

Commercially, Kling has evolved into a standalone AI company. It is no longer merely a consumer subscription-based creative tool: Kuaishou disclosed that Kling's Q1 2026 revenue exceeded RMB 650 million, up over 300% year-on-year; as of March, annualized revenue approached $500 million.

Despite steep growth, losses remain tangible. Kuaishou's funding announcement revealed that, assuming restructuring completion, Kling's 2025 revenue would reach approximately RMB 1.1 billion, with an unaudited net loss of around RMB 1.9 billion. By end-2025, total assets would stand at RMB 244 million, total liabilities at RMB 253 million, and negative equity at RMB 9 million. Computational procurement, R&D team expansion, and global expansion represent ongoing fixed costs—a key reason for Kuaishou's push for Kling's independent funding.

Kling no longer lacks a "compelling business label." It has transitioned from model demos to paid products, with clients paying for video generation, professional tools, and API access. However, overall losses indicate current revenue insufficient to cover computational, R&D, product, and marketing investments. AI video has not yet reached a stage where a single version can generate sustained long-term revenue. Model capabilities, inference costs, generation speed, and professional workflows continue evolving; lagging in any area could impact next-quarter usage volumes.

The up to $3 billion in funding thus primarily serves as timing capital. It enables Kling to continue purchasing computational resources, expanding teams, and building global operations beyond Kuaishou's annual budget. Kuaishou retains majority control and benefits from valuation gains, while external capital shoulders future investments. The announcement explicitly states funds will support business expansion, daily operations, working capital, and team development.

Yet capital only extends the race; it does not choose the route. Video generation model competition has shifted from "can it generate" to "can it enter production." General users demand cheaper, faster video creation; professional clients require consistent characters, camera control, synchronized audio-visuals, and stability for integration into existing workflows. Kuaishou disclosed Kling's entry into marketing, e-commerce, film, short dramas, animation, and gaming, including contributing to overseas series "David Dynasty."

For API clients, model migration costs are relatively low; shifts in effectiveness, pricing, and stability can redistribute usage volumes. Video model firms must continually invest to maintain market positions. While $3 billion seems substantial, in a protracted competition spanning model training, product distribution, and global customer acquisition, it merely keeps Kling in the game.

Thus, Kuaishou concurrently allocated 15% of shares for participation plans. Initial equity awards and options represent about 7.45% of the enlarged share capital, with Gai Kun receiving 3%, Cheng Yixiao 1%, and the remainder allocated to core management and technical staff. The announcement straightforwardly explains the incentive plan: to attract, motivate, and retain individuals critical to Kling's development.

Independent equity aligns core employees' rewards with Kling's model capabilities, revenue growth, and standalone valuation, rather than Kuaishou's group performance in live streaming, e-commerce, and advertising. In an environment where talent can migrate with experience and technical judgment to rival large model firms, this binding is more enduring than bonuses and clearer than job titles.

Gai Kun's special voting rights elevate the talent issue to the governance level. Kling must retain not just engineers but also an organizational capacity for sustained strategic decision-making and execution. The 3% stake lets Gai Kun share in company value, while tenfold voting rights empower him to drive direction—tied to his tenure through disposal restrictions and lapse-upon-departure clauses.

In this funding round, Kuaishou reconfigured Kling: capital comes from external sources, valuation is calculated independently, employees receive standalone equity, the technical CEO gains greater voting power, and the parent company retains control. Kling remains within the group, but responsibilities now align more closely with individuals.

The repurchase clause truly sets this funding round on a countdown.

The announcement stipulates that if Kling fails to complete an IPO by the agreed latest listing date or October 30, 2031 (whichever comes first), investors may demand repurchase of all or part of their equity. If Kling submits a qualifying listing application before the deadline, the repurchase right temporarily suspends; however, if listing fails to complete within 12 months post-submission due to expiration, rejection, or voluntary withdrawal by Kling, investors may still demand repurchase.

The repurchase price includes the investment principal, simple interest at 8% annually, and unpaid dividends, minus any distributions already received by the investor. Kling directly assumes repurchase obligations. Thus, funding becomes capital with an IPO exit and minimum return requirement.

The funding does not remove Kling's losses from Kuaishou's financial statements. On a fully diluted basis, Kuaishou will still hold approximately 68.33% of Kling's equity, with Kling remaining consolidated in Kuaishou's financial reports. The change lies in external capital shouldering part of the next-stage investments, while Kling's revenue, valuation, and management responsibilities are now measured independently.

The funding materials set aggressive growth targets: Kling's annualized revenue is projected to reach $1 billion by December 2026 and $2 billion by December 2027. These figures are forecasts within the funding model, not realized results or official Kuaishou financial guidance. As products like Seedance 2.0 enter professional creation and API markets, Kling faces rising pressure on model effectiveness, pricing, and client retention; however, public data remains insufficient to gauge the competitive impact on its revenue to date.

Kuaishou also drew a boundary. From restructuring completion until the later of five years post-signing or when Kuaishou no longer meets control thresholds, Kuaishou cannot control another entity primarily engaged in video generation model business. While retaining control over Kling, Kuaishou concentrates its AI video technical routes within one company, reducing space to support alternative approaches.

This agreement ultimately allocates different risks to different parties: investors protect exits via repurchase rights, major matter approval rights, and IPO deadlines; employees' rewards tie to Kling's standalone valuation; Gai Kun gains greater strategic influence but bears consequences for erroneous choices; Kuaishou retains control and majority equity benefits while continuing to consolidate Kling's operating results.

Four days after the funding announcement, Tencent reduced its Kuaishou stake by approximately 273 million shares via off-exchange block trades, lowering its ownership from 15.68% to 9.37%. Concurrently, two Tencent-controlled investment vehicles acquired direct equity exposure to Kling, though their combined fully diluted stake stands at merely ~1.12%. No evidence links these transactions directly, yet they concurrently highlight Tencent's dual investment relationships with Kuaishou Group and Kling AI.

Kling used to be the most imaginative business within Kuaishou. Now, it has independent shareholders, independent incentives, special voting rights, and a public timeline. Independent financing hasn't eliminated the risks; it has merely made their ownership and timeline clearer.

In the spring of 2024, Gai Kun's judgment propelled Kling to the main table of global video generation models. Two years later, the same judgment could no longer be made from a single office. The computational power consumed in one training session far exceeded past levels, with the product now targeting consumers, developers, and professional content companies simultaneously. External shareholders demand returns, Kuaishou needs to control losses, and core employees need to see the value of an independent company. Thus, Kuaishou incorporated its project decision-making approach from those years into a corporate governance structure.

In the past, Kling was Kuaishou's most imaginative AI business; now, it has transformed into a quasi-independent company with external shareholders, independent incentives, special voting rights, and a countdown to listing. Cheng Yixiao still maintains influence through Kuaishou's controlling stake, and Kuaishou has not completely let go, as the group's financial statements still consolidate Kling's profits and losses. Gai Kun has been pushed to the forefront of directional judgment and commercial outcomes.

This does not mean Kuaishou admits Kling is underperforming. For businesses like AI video, which are high-investment, high-risk, and deeply reliant on technological route judgments, it is difficult to rely solely on the original processes and resource allocation of large companies for support. It requires someone willing to shoulder immense uncertainty in exchange for greater power—and heavier responsibility.

*The featured image and illustrations in the text are sourced from the internet.

-

![]()

Ali Secures Apple! Qwen Achieves Major Breakthrough!

-

![]()

Shocking! Anthropic Discovers Unknown Subconscious Space J-space in Large Models

-

![]()

From 54GB to a Mere 4GB! Apple Collaborates with PrismML—Is Model Compression Tech on the Verge of a Breakthrough?

-

Silicon Flow Sprints Towards Hong Kong Stock Exchange Listing: Behind Its RMB 7.7 Billion Valuation, the 'First Token Factory Stock' Struggles with Negative Gross Margins

-

![]()

The Real-World 'Real Steel' Has Arrived! Zhongqing's Humanoid Robots Step into Freestyle Battle

-

![]()

Storage Price Hike Drags Down Smartphone Sales, Yet Huawei and iPhone Defy Trend with Remarkable Growth

-

![]()

After Kuaishou's Kling Secures $20 Billion in Funding, Cheng Yixiao 'Yields Seat' to Gai Kun

-

![]()

OnePlus Stays in China, realme Goes Global: OPPO Group Ends Internal Competition