Micron: AI's Popularity Can't Fill the 'Cycle Hole'

12/19 2024

12/19 2024

701

701

Micron (MU.O) released its fiscal 2025 Q1 earnings report after the U.S. market closed on December 19, 2024, Beijing time. The key points are as follows:

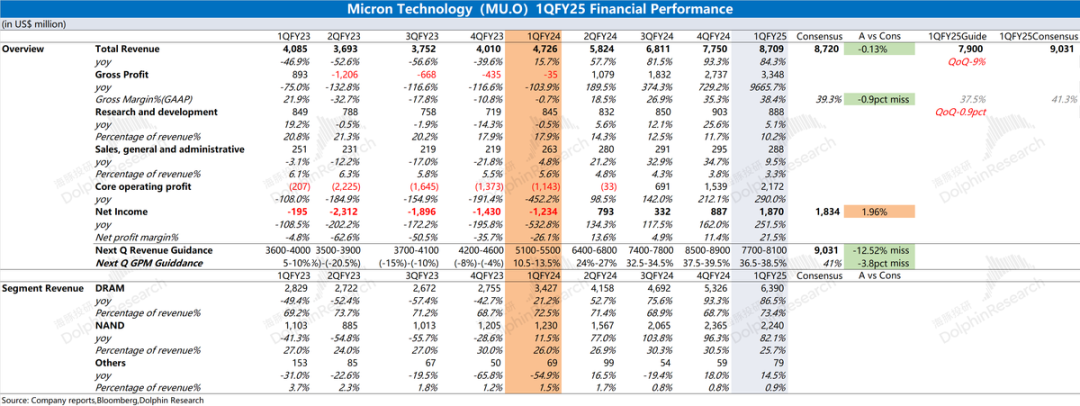

1. Overall Performance: Revenue targets met, but gross margin encountered obstacles. Micron's total revenue for the first quarter of fiscal 2025 was $8.71 billion, up 84.3% year-on-year, in line with market expectations ($8.72 billion). The continued accelerated recovery in revenue this quarter was driven by the growth of the company's DRAM business. Micron achieved a net profit of $1.87 billion in the first quarter of fiscal 2025, with continuous improvement on the profit side. Driven by the increase in HBM shipments and rising memory product prices, the company's revenue and gross margin have improved significantly, leading to a notable improvement in the company's final profit.

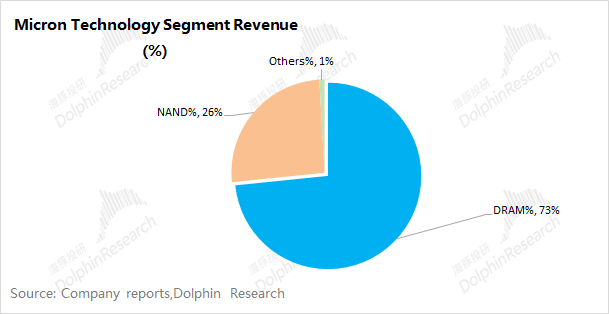

2. Business Segment: HBM is the main driver of performance. DRAM and NAND account for 99% of the company's revenue, and HBM was the main driver of revenue growth this quarter. Breaking it down, although the company's DRAM and NAND businesses both showed significant year-on-year growth this quarter, there was a clear divergence at the quarter-on-quarter level. Specifically, DRAM business still grew by 20% quarter-on-quarter, while NAND business declined by 5%. This is mainly because DRAM continued to grow driven by HBM, while weakness in demand in traditional sectors directly led to a quarter-on-quarter decline in NAND business.

3. Next Quarter Outlook: Revenue for the second quarter of fiscal 2025 is expected to be $7.9-8.1 billion (a 9% quarter-on-quarter decline), lower than market consensus expectations ($9 billion); quarterly gross margin (GAAP) is expected to be 36.5% to 38.5%, also declining quarter-on-quarter and lower than market consensus expectations (41.3%).

Dolphin's Overall View: This quarter's earnings report was passable, but next quarter's guidance was 'disappointing'. Micron's revenue and gross margin continued to recover this quarter, but the gross margin performance fell short of market expectations. Although HBM still contributed incremental growth to the company, some memory product prices declined this quarter due to the impact of traditional downstream markets such as mobile phones, which in turn affected gross margin performance.

In terms of business segments, the company's DRAM business still grew by 20% quarter-on-quarter this quarter. Driven by HBM, the DRAM business continued to experience volume and price increases; however, the company's NAND business declined by 5% quarter-on-quarter this quarter. This was mainly due to the impact of inventory adjustments in downstream sectors such as mobile phones, automobiles, and industry, leading to a slight quarter-on-quarter decline in shipments and average prices of related memory products.

Compared with this quarter's earnings report, the company's next quarter outlook is truly 'poor'. It not only interrupted the company's continuous revenue growth for seven consecutive quarters but also experienced a near-$800 million decline quarter-on-quarter, and the gross margin may also decline quarter-on-quarter. This undoubtedly adds more concerns to the market: 1) Has the current storage upcycle ended for the company? 2) Is the company's HBM business growth hindered? This directly led to a 16% decline in the company's share price after the market close.

Combining the industry and the company's operating conditions, Dolphin believes that the decline in revenue in the next quarter is still mainly affected by sectors such as mobile phones and automobiles. From several perspectives: 1) Traditional sectors are still in the inventory adjustment phase, and the company expects to gradually stabilize after the second half of fiscal 2025 (after March 2025 in the calendar year); 2) The company has further increased its expectation for the total HBM market size next year to $30 billion (originally expected to be $25 billion), which demonstrates the company's confidence in the HBM business; 3) Recent rumors that NVIDIA is adjusting the shipment structure of B200 and B300 will also affect the pace of Micron's HBM to some extent.

Overall, Micron's current business includes both traditional storage demand and AI-related demand such as HBM. However, the company's current performance fundamentals are still affected by traditional businesses, and the current downturn in traditional sectors will directly impact the company's upcoming business. Regarding the growing HBM business that the market is concerned about, although its current revenue share is still less than 10%, the company's growth expectations for next year continue to be revised upwards. Therefore, the company's performance will be under pressure in the first half of fiscal 2025, but with downstream inventory liquidation and the increase in HBM shipments, the company's performance is expected to see a significant improvement again in the second half of the year.

Below is a detailed analysis:

I. Overall Performance: Revenue targets met, but gross margin encountered obstacles

1.1 Revenue Side

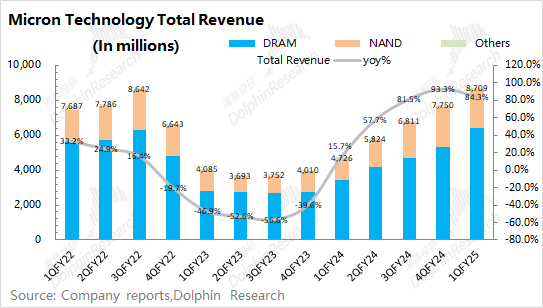

Micron's total revenue for the first quarter of fiscal 2025 was $8.71 billion, a year-on-year increase of 84.3%, in line with market expectations ($8.72 billion). The year-on-year recovery in revenue this quarter was mainly driven by price increases in the company's memory products, with both DRAM and NAND products experiencing year-on-year increases of over 60% in average shipping prices.

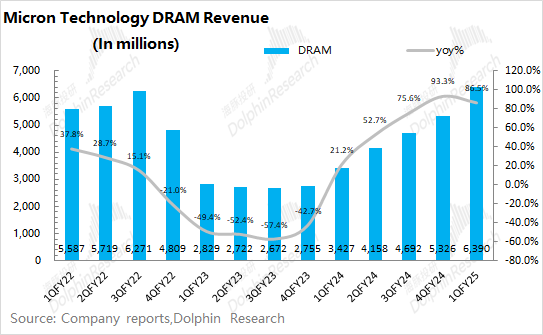

From a quarter-on-quarter perspective, the company's revenue grew by 12.4% this quarter. Among them, the DRAM business still grew by 20% quarter-on-quarter driven by HBM demand, while the NAND business declined by 5% quarter-on-quarter, mainly due to the drag of inventory adjustments in downstream sectors such as mobile phones, automobiles, and industry.

1.2 Gross Margin

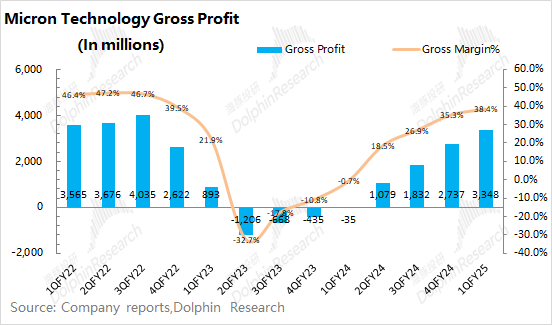

Micron achieved a gross profit of $3.348 billion in the first quarter of fiscal 2025, with the company's quarterly gross profit continuing to recover.

The company's gross margin for this quarter was 38.4%, lower than market expectations (39.3%). The increase in gross margin was mainly due to the increase in the average price and proportion of DRAM products, but the weakness in some downstream sectors affected the magnitude of the gross margin recovery. Although the company's current inventory is $8.705 billion, a quarter-on-quarter decline of 1.9%, with the recovery of sales and the liquidation of some downstream inventories, the company's inventory turnover speed has accelerated, further adjusting the company's inventory structure.

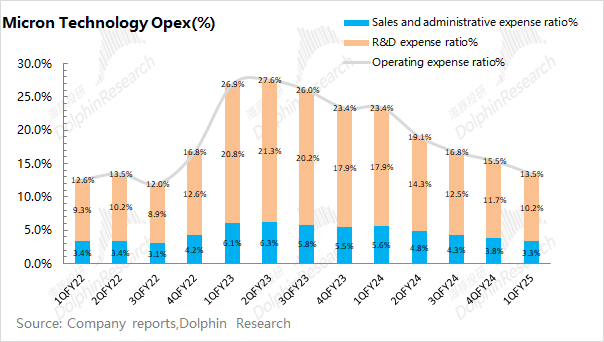

1.3 Operating Expenses

Micron's operating expenses for the first quarter of fiscal 2025 were $1.176 billion, a year-on-year increase of 6.1%. With revenue growth, the company's operating expense ratio for this quarter declined to 13.5%.

In terms of individual expenses:

1) Selling and administrative expenses: This quarter was $288 million, a year-on-year increase of 9.5%. The selling and administrative expense ratio was 3.3%, a year-on-year decrease of 2.3 percentage points, mainly due to the increase in revenue. There is a certain relationship between selling expenses and revenue performance, while administrative expenses are relatively rigid;

2) Research and development expenses: This quarter was $888 million, a year-on-year increase of 5.1%. Research and development expenses are the largest source of the company's operating expenses, and the research and development expense ratio for this quarter declined to 10.2%. As a technology company, the company places greater emphasis on R&D capabilities, and its R&D expenses remain at a relatively high level.

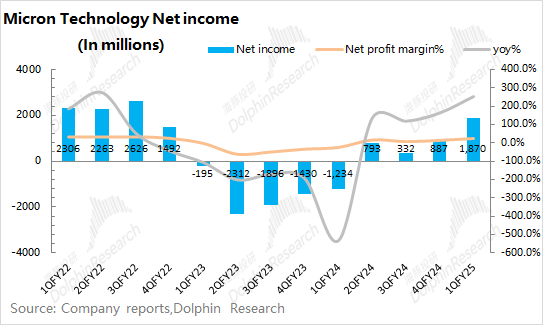

1.4 Net Profit

Micron achieved a net profit of $1.87 billion in the first quarter of fiscal 2025, in line with market expectations ($1.83 billion). The company's profit growth this quarter was mainly due to the growth of the DRAM business and the improvement in gross margin. In this quarter, the company's net profit margin was 21.5%, and its profitability improved significantly. Among them, the company's operating profit this quarter reached $2.1 billion, which has reached a relatively high position in previous cycles.

II. Business Segment: HBM is the main driver of performance

From Dolphin's in-depth analysis of Micron in the past, "Micron: Has the Winter for Memory Chip Manufacturers Ended?", the company's largest source of revenue is memory chips. From the latest earnings report, DRAM and NAND are still the company's most important sources of revenue, accounting for a combined 99% of total revenue. Therefore, changes in Micron's business are mainly reflected in the performance of its DRAM and NAND businesses.

2.1 DRAM

DRAM is the company's largest source of revenue, accounting for over 70%. This quarter, the company's DRAM business revenue increased to $6.39 billion, up 86.5% year-on-year. Considering the performance of downstream sectors such as mobile phones and automobiles, Dolphin believes that the $1 billion increase in DRAM business revenue quarter-on-quarter this quarter was mainly driven by demand for cloud server DRAM and revenue growth from HBM.

In terms of volume and price performance: The company's DRAM business grew by 20% quarter-on-quarter this quarter, with shipments increasing by about 7% quarter-on-quarter and prices rebounding by about 8%.

The volume and price increase this quarter was mainly driven by demand from cloud servers, while some products in traditional sectors faced downward pressure on prices. Taking DDR4 16G (1G*16) 3200Mbps as an example, the product price rose from a low of $2.89 in September 2023 to a high of $3.81, gradually falling back to $3.09, and then rising again to the current $3.18 in December. The average price for this fiscal quarter was under significant pressure.

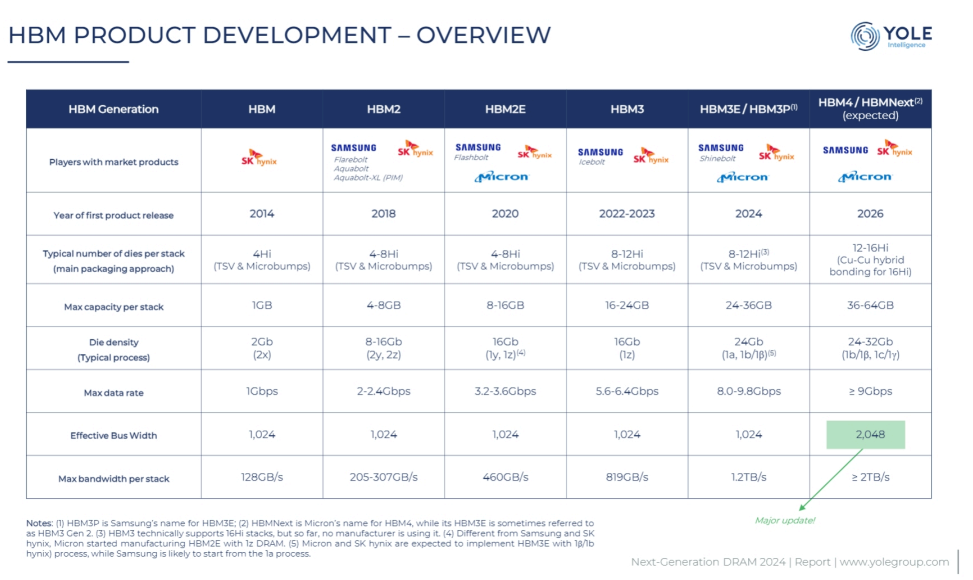

For the HBM sector, which the market is concerned about, the products of the current industry's top three manufacturers have all been iterated to the latest HBM3E, with SK Hynix and Micron's products already being supplied to NVIDIA. According to YOLE estimates, HBM products will be iterated to the next generation of HBM by 2026.

Regarding the market's concerns about the company: 1) The sustainability of HBM growth; 2) Competition from Samsung. Although it was previously reported that Samsung had completed NVIDIA's core certification, supply chain information indicates that Samsung's scalable production volume during the H200 product cycle is limited. As for the total addressable market (TAM) for HBM, the company has increased its 2025 expectation to over $30 billion. Currently, the company's share of HBM is only in the single digits, but in the future, the company expects to increase its share to around 20%, which is comparable to its DRAM market share.

Regarding the competition between GPUs and ASICs, both require HBM. As long as the overall market grows, the demand for HBM will still increase. The specific difference lies in the performance iterations required: B200 and MI325X require HBM3E, while Google's TPU v6, for example, requires HBM3, with slightly slower performance iteration requirements.

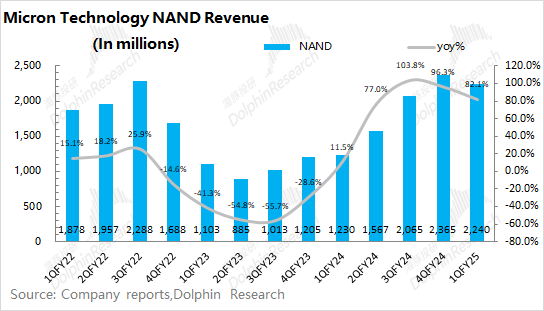

2.2 NAND

NAND is the company's second-largest source of revenue, accounting for 26%. This quarter, the company's NAND business revenue was $2.24 billion, up 82.1% year-on-year. The year-on-year growth in NAND was mainly driven by the recovery of average product prices from their lows.

However, on a quarter-on-quarter basis, a decline began this quarter, mainly due to weak demand in traditional downstream sectors such as mobile phones and automobiles. The market originally expected the company's downstream sectors to gradually emerge from the trough through inventory adjustments. However, based on current performance, the company's downstream inventory adjustments are still ongoing and may not improve until the second half of the next fiscal year.

In terms of volume and price performance: Micron's NAND business declined by 5% quarter-on-quarter this quarter, with NAND shipments declining by about 2% quarter-on-quarter and average NAND shipping prices declining by about 3%. From the performance of product prices in the market, NAND Flash (128Gb 16G*8 MLC) has fallen from a previous price of $4.9 to around $3.

Dolphin's Related Articles on Micron: Earnings Report Reviews

September 26, 2024 Earnings Review: "Micron: Ups and Downs, but Cyclical Trends Remain Key"

June 27, 2024 Earnings Review: "Micron: Price Hikes Fail to Meet Elevated Expectations"

March 21, 2024 Earnings Review: "Micron: Memory Prices Soar, Igniting the HBM3E Battle"

December 21, 2023 Earnings Review: "Micron Technology: Winter in Storage Ends, Prices Rise to Herald Spring"

September 28, 2023 Earnings Review: "Micron Technology: A Fleeting Recovery Amid a Lingering Downturn"

June 29, 2023 Earnings Review: "Micron Technology: The AI Wave Crests, but Has the Turning Point Arrived?"

March 29, 2023 Earnings Review: "Micron's 'Bleeding' May Not Be All Bad"

In-Depth Analysis

April 13, 2023: "Micron: GPT Cools Down, but Storage Market Bounces Back"

March 15, 2023: In-Depth Analysis of Micron: "Has the Winter for Memory Chip Manufacturers Finally Thawed?"

-

![]()

139 Institutions Conduct Research as Robotec Promptly Secures a Major Order Worth 129 Million Yuan!

-

![]()

Zeiss Boosts Investment to Expand 25,000-sqm Optical Plant, Elevating Its Exclusive EUV Optical Manufacturing Capabilities!

-

![]()

SAIC’s Four Key Divisions See Leadership Overhaul: Lu Xiao Moves to Passenger Cars, Xu Ping Takes Charge of GM, Wu Yun Leads Volkswagen

-

![]()

Nearly a Year On, Traffickers Still Reap Tens of Thousands by Selling Zeekr 9X in Russia

-

![]()

Apple’s New Business Model: Pay $39 a Month, But at What Cost to Your Wallet?

-

![]()

Tencent Places Its Bets on WorkBuddy: The Next Frontier in AI-Driven Office Solutions, Vying for the Smart Gateway

-

![]()

Apple Reclaims Global Market Cap Crown: Is a Strong Device the True Path for AI?

-

![]()

Apple Regains Global Market Cap Leadership: Are Smart Devices the Future of AI?