Huang Renxun's Gambling

07/14 2026

07/14 2026

396

396

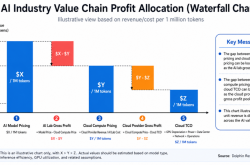

When it comes to the current AI craze, what comes to mind for most people are either the model races among top-tier vendors or TSMC's round-the-clock wafer fabs and NVIDIA's soaring revenue and stock price.

Everyone is fixated on chip production capacity. Many intuitively believe that as long as chips can be manufactured, AI development will skyrocket.

The reality is far more complex. The bottleneck in this massive computing power infrastructure drive is shifting. While TSMC and memory manufacturers still face demand outstripping supply, maintaining this trend is becoming increasingly untenable.

It's common knowledge that building massive AI computing clusters is extremely capital-intensive. However, the sheer scale of the funding required defies common understanding.

According to industry tracker SemiAnalysis, by 2029, the global unpaid debt for purchasing AI equipment and building supporting data centers will exceed $7 trillion.

Apple achieved record-breaking profits in its 2025 fiscal year, netting approximately $112 billion for the entire year. At this earning pace, even if Apple used all its net profits to repay the debt, it would take over 60 years to clear it.

Faced with such a terrifying financial black hole, even traditional tech giants are feeling overwhelmed.

In the past, funding for computing power construction primarily relied on the self-financing of a few tech giants like Amazon, Google, Meta, and Microsoft.

Now, the entire industry urgently needs to find new funding sources; otherwise, the AI computing power expansion engine will stall due to lack of funds.

Since the super giants cannot single-handedly support this endeavor, a group of astute 'gold prospectors' has naturally emerged in the market. Many emerging AI cloud service providers (known as Neoclouds) are attempting to step in and act as 'computing power contractors.'

Their plan is to borrow money from financial institutions to purchase NVIDIA graphics cards, build computing clusters, and then flexibly lease them to various AI startups.

If this path proves viable, the computing power construction dilemma could be alleviated. However, ideals are plump (Chinese term meaning 'plump' or 'full,' often used metaphorically for optimistic expectations), while reality is harsh. These new players have immediately hit a wall upon entry, finding themselves in a dilemma.

If no one can afford to build new computing power clusters, who would be the biggest loser? Undoubtedly, it would be NVIDIA, which is thriving on selling graphics cards.

To preserve this money-printing business and prevent the computing power channel from being completely monopolized by several established giants developing their own chips, NVIDIA has made a rare and ambitious cross-border decision.

It has decided to stop being just a well-behaved hardware supplier and instead directly dive into Wall Street's financial games.

The Contractor's Shackles

These emerging AI cloud service providers (Neoclouds) face a deadly triangle. To successfully build a computing power cluster, they must simultaneously accomplish three things:

Funding (bank loans), off-take agreements (customer leases), and data centers (machine room space). These three elements form an interlocking cycle.

Banks take a very pragmatic approach. In the eyes of financial institutions, AI startups starving for funding could collapse at any moment due to an inability to secure the next round of financing. Leasing expensive GPU computing power to these high-risk, short-term tenants offers no guarantee for the safety of hundreds of millions of dollars in loans.

To absolutely mitigate risks, Wall Street banks have established an extremely stringent rule. Emerging cloud providers seeking loans must first submit a 'letter of commitment.'

This means they must secure a five-year computing power off-take agreement with a tech giant possessing an 'investment-grade' credit rating (such as Microsoft, Meta, or Oracle).

When approving loans, banks completely ignore the business potential of the emerging cloud providers themselves; what they truly value is merely the massive balance sheet of the tech giant standing behind them as a guarantor.

One might wonder: Why would Microsoft or Meta, themselves super cloud providers with vast resources, seek to rent equipment from these startup 'computing power contractors'?

The reason is that during the current AI boom, demand for computing power is growing insanely fast. These giants' own data center construction speeds, power approval progress, and team expansion rates cannot keep up with the surging demand.

To seize the initiative, the giants simply opt to both lease and purchase, directly 'snapping up' the clusters built by emerging cloud providers.

This has led to an absurd and ironic situation. The original vision of emerging cloud providers was to serve a broad range of entrepreneurs and become partial alternatives to traditional giants.

However, financial pressures have forcibly transformed them into 'computing power sublandlords' or even 'bottom-tier workers' for the giants.

Consequently, the vast number of AI startups and inference service providers genuinely needing flexible short-term leases still face a dilemma of having no available GPUs. This is because a significant portion of GPU capacity on the market has been locked up by the giants.

When genuinely needing flexible short-term leases, the vast number of AI startups come knocking, but emerging cloud providers simply cannot spare extra graphics cards.

If emerging cloud providers want to bypass the giants, sign one-year short-term agreements directly with startups, and seek bank loans, banks will impose even more outrageous conditions.

For example, requiring startups with no credit rating to pay the entire year's substantial rent upfront as collateral.

Securing funding and customers is merely the beginning of this nightmare. Even if emerging cloud providers reluctantly accept the giants' 'co-optation,' they still face the stringent picky (Chinese term meaning 'picky' or 'demanding') of data center operators.

These landlords, who control physical machine rooms, equally dislike risks. In their eyes, leasing precious machine room space and power quotas to emerging cloud providers is extremely risky.

Landlords prefer to sign stable, long-term leases of ten to fifteen years directly with traditional giants.

To compensate for this so-called high risk, landlords demand higher premiums from emerging cloud providers, resulting in rental costs (yield requirements) for these new players being 3% to 5% higher than those for the giants.

The increasing concentration of computing power resources among a few oligopolies poses a fatal (Chinese term meaning 'fatal') threat that NVIDIA most wishes to avoid. These tech giants, controlling crucial channels, are all secretly investing heavily in developing their own custom AI chips. If computing power infrastructure is allowed to be monopolized by the giants, NVIDIA's market control will be weakened.

Faced with this interlocking predicament, traditional hardware sales strategies have completely failed. Jensen Huang must immediately step in personally and use an unprecedented financial force to directly shatter this deadly triangle that has trapped countless players.

NVIDIA Becomes the Central Bank of Computing Power

NVIDIA's solution is 'debt support,' which can be classified as a financial innovation. In a sense, NVIDIA assumes a role similar to that of a 'central bank' in the traditional financial system.

Many might be unfamiliar with the concept of a 'central bank as lender of last resort.' In traditional financial crises, when commercial banks face runs and all financial institutions refuse to lend to each other due to extreme panic, the entire financial system's capital chain can snap instantly.

At this point, the central bank, based on its legal currency issuance function, acts as the 'lender of last resort' to inject liquidity into the market.

This absolute credit endorsement can significantly alleviate market panic and restart capital flow.

What NVIDIA is doing now is precisely the 'central bank backstop' in the computing power realm.

Faced with Wall Street banks' risk aversion toward the computing power leasing market, NVIDIA has decided to step in personally and act as the 'final buyer' and credit guarantor for the entire AI computing power credit system.

Specifically, the support agreement NVIDIA signs with emerging cloud providers is a sophisticated mechanism binding interests and risks, far more complex than simple 'guarantees.'

First, a six-year 'floor commitment.' NVIDIA provides these emerging cloud providers with a minimum revenue guarantee typically lasting six years, a duration that precisely matches the lifecycle and depreciation schedule of heavy-asset hardware in data centers.

Second, an all-encompassing 'take-or-pay' mechanism.

What if, after emerging cloud providers build their computing power clusters, market fluctuations lead to insufficient demand for renting graphics cards from third-party AI startups?

NVIDIA promises that, in the worst-case scenario, it will personally lease back these idle GPU computing power at pre-agreed price curves (or directly make up the revenue shortfall) using its own funds.

This means that even if the computing power market cools, emerging cloud providers can still secure an extremely stable guaranteed cash flow, sufficient to repay both principal and interest on their bank loans.

Warren Buffett said that the first rule of investing is to preserve capital. Banks operate similarly when lending; their top concern is not whether you can earn substantial profits in the future, as your earnings, no matter how high, are predetermined in terms of principal and interest.

They only care about whether you can still repay the loan in the worst-case scenario.

With NVIDIA providing the ultimate guarantee, Wall Street has taken a reassuring pill and is willing to bypass traditional tech giants, directly approving hundreds of millions of dollars in loans to emerging cloud providers.

Of course, NVIDIA is absolutely not engaged in charity; it achieves 'killing two birds with one stone' through this model.

This leads to the third key point of the agreement: Step division (Chinese term meaning 'staged profit-sharing') of excess profits. Since NVIDIA assumes the backstop risk, it also has the right to demand a greater share of the revenue (Chinese term meaning 'proceeds' or 'returns').

According to the agreement terms, rental income from emerging cloud providers within the guaranteed quota belongs entirely to them.

However, if computing power is in short supply and they flexibly lease it at higher market premiums to various clients, NVIDIA will take a significant portion (e.g., 40% income sharing on a pro-rata basis) of the excess profits above the guaranteed threshold.

Through this mechanism, NVIDIA has successfully constructed a perfect 'computing power circulation financial system.'

On the front end, it still receives substantial hardware payments from emerging cloud providers purchasing GPUs, ensuring ample cash flow for its core business.

On the back end, it gains a continuous stream of long-term cloud service income through cloud rental revenue sharing.

The more profound strategic significance of this arrangement is liberating emerging cloud providers from the long-term contract control of traditional giants.

They no longer need to be forced to 'wholesale' their computing power to a few large firms but can flexibly divide it into smaller portions and lease it monthly or annually to AI startups genuinely needing computing power.

This not only prospers the entire AI underlying innovation ecosystem but also binds a large number of entrepreneurs to NVIDIA's ecosystem, preventing large firms' self-developed chips (such as Google's TPU) from eroding the market.

However, this model is not without flaws. Essentially, NVIDIA is engaging in a disguised form of 'supplier financing.'

It leverages its massive balance sheet to generate and sustain market demand for its own chips.

This is akin to walking a tightrope. If global real-world inference and training demand for AI large models fails to meet expectations in the coming years, leading to overcapacity in the computing power market, NVIDIA will have to dip into its own pockets to fill these massive revenue gaps.

NVIDIA's willingness to voluntarily absorb market volatility and credit risks, stepping out of the passive role of a traditional hardware vendor, essentially relies on its industry dominance and strong capital foundation to secure long-term market leadership.",

-

![]()

AI Computing Power: From Feast to ‘Leftover Feast’?

-

![]()

AI Computing Power: From Feast to 'Leftover Feast'?

-

![]()

The Stock Competition Era Unveils the True Nature of All Brands

-

![]()

India's New Energy Vehicle Dream: From Tata Leak to Tesla's Exit - A Closing Argument

-

![]()

The 'Last Millimeter' of Interaction Between Robots and the Physical World

-

![]()

Every AITO Sold Contributes 136,000 Yuan to Huawei: Seres Faces Its Compaq Moment

-

![]()

Huang Renxun's Gambling

-

![]()

Is Seres Truly Being 'Bled Dry' by Huawei?