Every AITO Sold Contributes 136,000 Yuan to Huawei: Seres Faces Its Compaq Moment

07/14 2026

07/14 2026

481

481

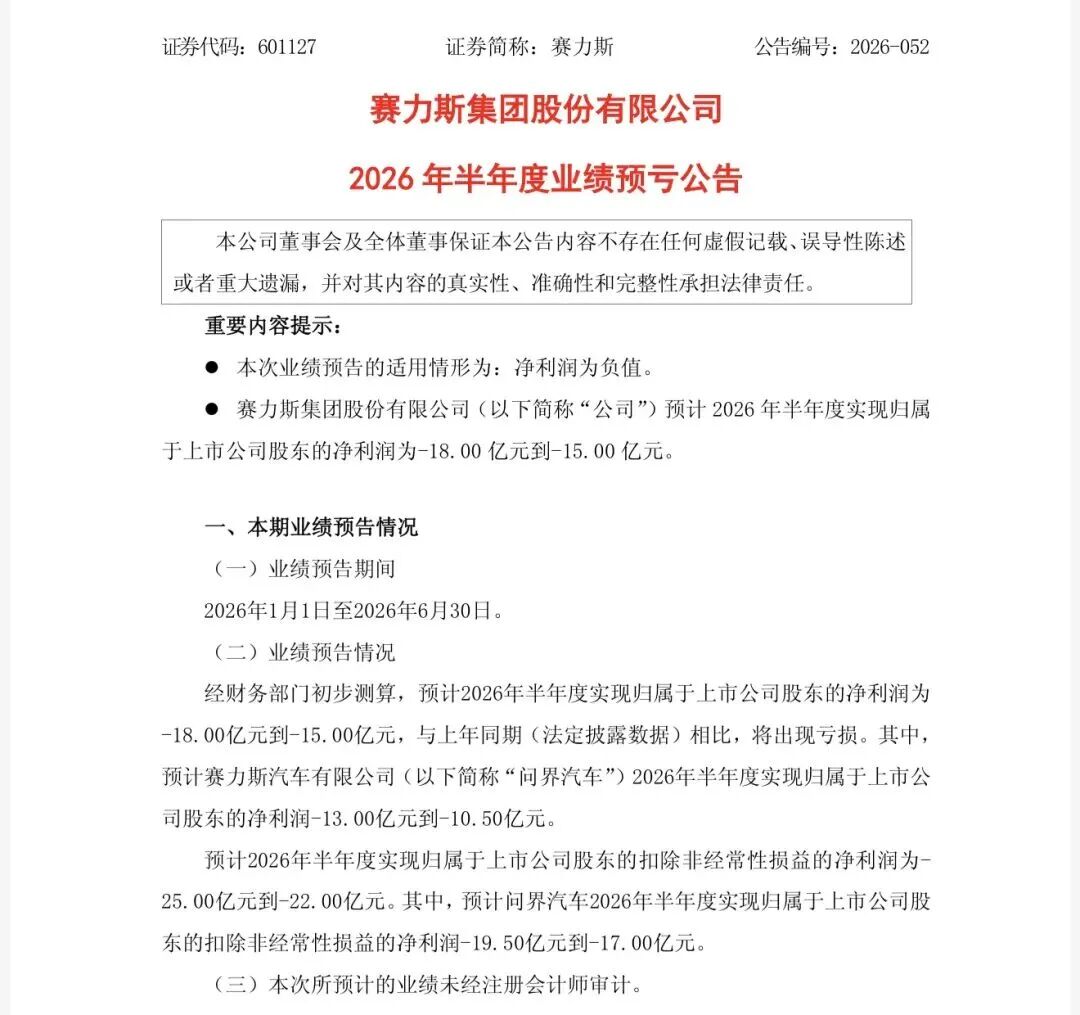

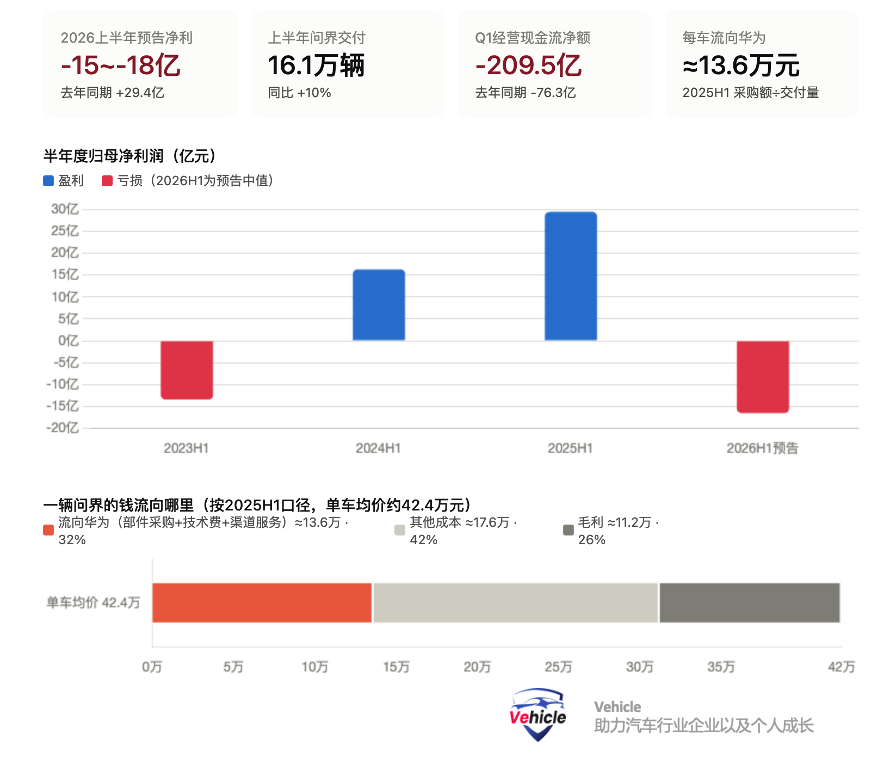

On the evening of July 11, 2026, Seres released its earnings forecast, revealing a net loss of 1.5 to 1.8 billion yuan attributable to shareholders (of the parent company) for the first half of 2026, alongside a non-recurring loss of 2.2 to 2.5 billion yuan. This starkly contrasts with the 2.941 billion yuan profit reported in the same period last year, marking a dramatic swing of over 4.5 billion yuan from profit to loss. The next day, the stock price plummeted to its daily limit (-9.98%), capping off seven consecutive months of declines and shrinking the market capitalization by over 100 billion yuan.

The counterintuitive reality is that AITO delivered approximately 161,000 vehicles during the same period, marking a 10% year-on-year increase. The M9 model topped the sales charts for luxury SUVs priced over 500,000 yuan for multiple consecutive months, including over 30,000 deliveries in June alone. This scenario exemplifies the paradox of "strong sales but poor financials."

1. Financial Breakdown: How Losses Accumulated Despite Strong Sales

By analyzing the Q1 2026 financial report alongside the mid-year forecast, we can deduce the complete loss structure:

Step 1: Hidden losses surfaced in Q1. Revenue in Q1 reached 25.746 billion yuan (+34.46%), with net profit attributable to shareholders at 754 million yuan, seemingly still growing (+0.89%). However, non-recurring net profit was only 103 million yuan, a 73.87% year-on-year drop. Despite a 30% revenue increase, core business profits nearly vanished, indicating that the "bicycle economy" (per-vehicle profitability) collapsed in Q1, masked by non-recurring gains.

Step 2: Massive losses emerged in Q2. The projected half-year loss of 1.5–1.8 billion yuan, minus Q1's +754 million yuan, implies a Q2 loss of approximately 2.25–2.55 billion yuan. The announcement disclosed that AITO incurred a net loss of 1.9–2.15 billion yuan in Q2. This means nearly all losses came from AITO, the best-selling business, rather than from secondary operations.

Step 3: Four key sources of losses, all pointing to the same issue—"lack of control over core operations":

Rigid "ecosystem taxes" paid to Huawei.

According to Hong Kong IPO disclosures, Seres procured 75 billion yuan worth of goods from Huawei over three and a half years; 20 billion yuan in H1 2025 accounted for 33% of total procurement and nearly 30% of total revenue for the same period (62.36 billion yuan). This translates to approximately 136,000 yuan per AITO sold flowing to Huawei (for smart cockpits, intelligent driving hardware, ~2% technology licensing fees, and ~8% sales/channel service fees). These payments are unaffected by Seres' profitability—acting as profit-sharing in good times but as profit extraction in bad times.

Inability to internally absorb raw material price hikes.

Lithium carbonate prices surged from 80,000 to 180,000 yuan/ton (+125%), while storage chip prices quadrupled. AITO models come standard with multiple LiDAR and advanced intelligent driving hardware, requiring far more electronic components than ordinary electric vehicles, adding 15,000–20,000 yuan per vehicle in costs. BYD can offset such hikes with in-house battery and chip production, but Seres relies on external suppliers (batteries from CATL, intelligent systems from Huawei), forcing it to absorb price increases. 160,000 vehicles × 15,000–20,000 yuan ≈ 2.4–3.2 billion yuan, roughly matching Q2's loss magnitude.

Asset impairments from model transitions borne solely by Seres.

Q2 saw the launch of new M9 and M6 models, devaluing old production lines, molds, and parts, necessitating impairment charges (1.2 billion yuan already provisioned at the end of 2025). Critically, product definition and upgrade timing are controlled by Huawei, but fixed asset investments and impairment risks fall entirely on Seres. Huawei decides when to iterate; Seres foots the bill.

Cash flow reveals industry position.

Q1 operating cash flow was -20.95 billion yuan (vs. -7.63 billion yuan last year) due to "sales collections lagging supplier payments." Strong automakers (BYD, Tesla) generate positive operating cash flow by extending supplier payment terms; Seres does the opposite—lacking pricing power downstream (due to price wars) and payment leverage upstream (with Huawei and CATL), it faces squeezes on both ends.

Additional evidence: Q1 R&D expenses surged 70.7% year-on-year to 1.794 billion yuan. Ostensibly "increased investment," this actually reflects catch-up efforts—including spending 11.5 billion yuan to acquire a 10% stake in Huawei's Intelligent Automotive Solutions (IAS) unit and establishing Saindo Tech to integrate Doubao AI—all attempts to regain control over core technologies previously outsourced to Huawei.

Clarification: Seres' reported gross margins once reached 26.5%–29.4% (industry-leading), but this is due to accounting practices—Huawei's 8% channel service fees are classified as sales expenses rather than operating costs, inflating gross margins while net margins are eroded by expenses. Non-recurring net margins and cash flow better reflect its true financial health.

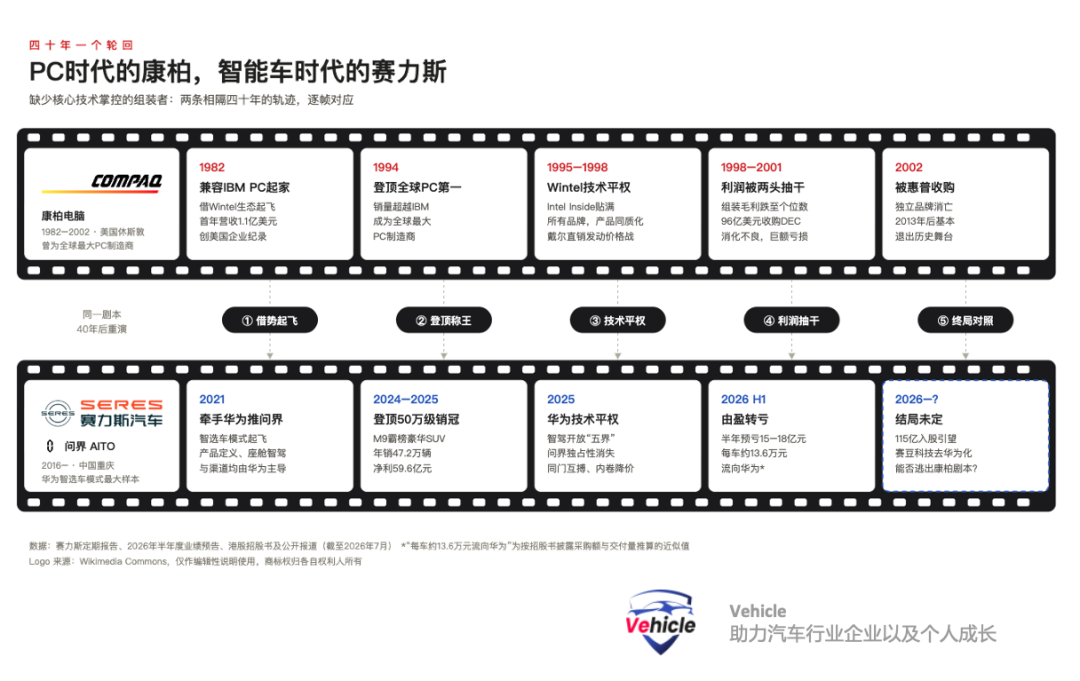

2. The Compaq Mirror: The Fate of Assemblers

Comparing Compaq's (1982–2002) trajectory with Seres' (2021–present) reveals near-identical patterns:

| Dimension | Compaq (1982–2002) | Seres (2021–Present) |

|---|---|---|

| Takeoff Strategy | Leveraged IBM PC compatibility and Wintel ecosystem to become #1 global PC seller by 1994 | Leveraged Huawei's Smart Selection vehicle model, with AITO M9 topping luxury SUV sales |

| Core Technology Ownership | CPUs from Intel, OS from Microsoft | Intelligent driving/cockpit/brand perception controlled by Huawei; batteries from CATL |

| Profit Distribution | Intel: 50%+ gross margins; Microsoft: 80%+; PC assemblers: 5–10% (and shrinking) | Huawei takes ~136,000 yuan per vehicle; Seres' non-recurring net margin approaches zero or negative |

| Fatal Blow | Intel/Microsoft supplied all vendors equally → product homogenization → Dell price wars | Huawei's technology opens to "Five Brands" (AITO, Luxeed, Enjoy, Zensect, Shangjie) and more automakers → AITO loses exclusivity → price wars |

| Struggling Moves | 1998: $9.6 billion acquisition of DEC to fill tech gaps → indigestion | 2026: 11.5 billion yuan stake in IAS, R&D surge, Saindo Tech to de-Huawei |

| Outcome | 2001: massive losses; 2002: acquired by HP, brand extinct | ? |

Compaq's lesson isn't that "assembly doesn't pay," but that when core technology platforms are equally accessible to all competitors, assembly differentiation vanishes, and profits are drained by upstream (technology) and downstream (channels/direct sales efficiency) players—the bottom of the smile curve.

Seres' situation is worse: Wintel only charged for technology, not channels; Huawei charges both technology licensing fees and 8% channel fees while controlling brand perception (consumers often believe they're buying a "Huawei car"). Compaq at least owned its brand; Seres lacks even that.

3. Structural Flaws in the Hongmeng Intelligent Driving Model

Seres is the best-selling, most deeply integrated, and only previously profitable example in Huawei's Hongmeng Intelligent Driving ecosystem. Its losses expose systemic issues with the model, not just company-specific problems:

"Technological democratization" backfires on pioneers.

Huawei's intelligent driving and cockpit technologies expanded from AITO exclusivity to Luxeed (Chery), Enjoy (BAIC), Zensect (JAC), Shangjie (SAIC), then to HI-mode partners like Avatr, Deepal, and Voyah, and various "Jing"-branded models. When "Huawei Intelligent Driving" becomes a standard selling point, AITO M7 faces competition from Luxeed R7 and Shangjie models—mirroring how Compaq lost pricing power after "Intel Inside" appeared on all brands.

Partners bear all heavy asset risks without product control.

Factories, production lines, molds, inventory, and impairments sit on automakers' books; redesigns, pricing, and channel policies are Huawei-led. Risks and decision-making are mismatched, making automakers natural shock absorbers in downturns.

If the top student loses money, others fare worse.

AITO sells 160,000 vehicles/year at an average price of 400,000+ yuan but cannot sustain the 136,000 yuan per-vehicle ecosystem cost. Luxeed, Enjoy, and Zensect, with a fraction of AITO's sales, face even worse financial models. This model guarantees Huawei profits (steady technology/channel fees) but gambles on volume for automakers. Many "brands" may not prioritize profitability, valuing market presence or volume instead.

Brand perception is hollowed out, with high exit costs.

Seres attempts to "de-Huawei" (with its own Magic Platform, Bluemotion brand, Saindo Tech integrating Doubao AI), but consumers pay for "Huawei." De-Huaweification risks losing sales—a deeper lock-in than Compaq faced.

4. Uncertain Ending: Three Differences Between Seres and Compaq

Fairly speaking, the script isn't finished. Seres holds three cards Compaq lacked:

A 10% stake (11.5 billion yuan) in IAS, securing a shareholder seat in Huawei's core technology platform—akin to Compaq investing in Intel. While profit distribution remains unchanged, it allows Seres to share upstream gains and gain some binding.

Huawei has pledged not to manufacture cars itself (due to commitments and sanctions), unlike Intel's choice not to build PCs out of disinterest. This leaves room for coexistence.

China's new energy vehicle market is still growing, unlike the stagnant PC market circa 2000. The time window remains open.

But the direction is clear: If Seres and peers cannot truly control at least one of batteries, intelligent driving, or branding, their fate will mirror Compaq's—either being consolidated or slowly drained to zero profit at the bottom of the smile curve. This half-year report's massive loss isn't an operational accident but the first complete billing of the model's flaws.

*Unauthorized reproduction or excerpting is strictly prohibited.

-

![]()

AI Computing Power: From Feast to 'Leftover Feast'?

-

![]()

The Stock Competition Era Unveils the True Nature of All Brands

-

![]()

India's New Energy Vehicle Dream: From Tata Leak to Tesla's Exit - A Closing Argument

-

![]()

The 'Last Millimeter' of Interaction Between Robots and the Physical World

-

![]()

Every AITO Sold Contributes 136,000 Yuan to Huawei: Seres Faces Its Compaq Moment

-

![]()

Huang Renxun's Gambling

-

![]()

Is Seres Truly Being 'Bled Dry' by Huawei?

-

![]()

Robot Brain: A Lucrative Business or a Challenging Pursuit?