Memory Sticks Become the "Electronic Moutai": Who's Paying the Price?

11/17 2025

11/17 2025

620

620

Author | Xiaoman

Disclaimer | The featured image is sourced from the internet.

Original article by Jingzhe Research Institute. Please leave a message to request permission for reprinting.

Recently, the new Redmi K90 series has sparked heated online discussions due to its pricing. Lu Weibing, President of Xiaomi Group's Mobile Phone Division, responded promptly, stating that the key factor affecting product pricing was "the storage cost increase far exceeding expectations and continuing to intensify." Subsequently, Lei Jun also publicly noted that "memory prices have risen too much."

The price changes triggered by the increase in mobile phone memory prices prompted public statements from both Lu Weibing and Lei Jun. Behind this seemingly simple hot topic lies a "super cycle" in the memory supply chain industry.

The Arrival of 'Electronic Moutai'

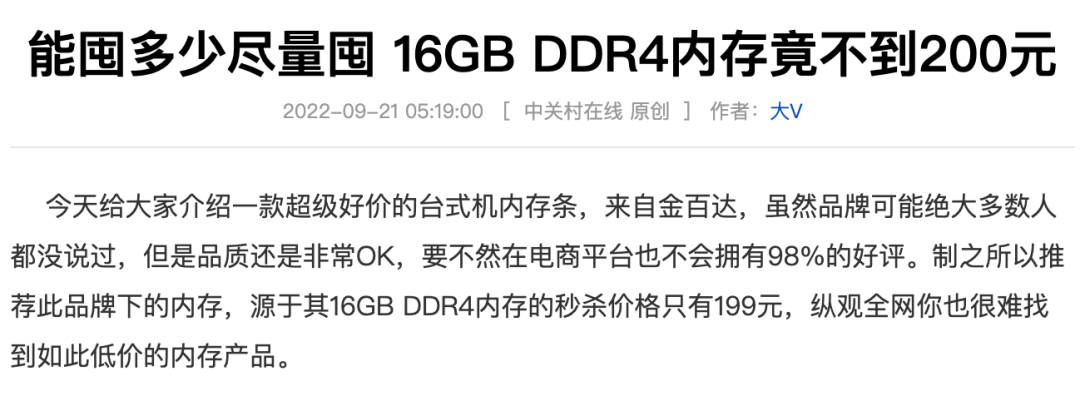

As early as September 2022, netizens on ZOL.com.cn called for "stocking up on memory sticks." At that time, the KingBank 16GB DDR4 memory was on sale for just 199 yuan. Unfortunately, this early call did not generate much attention, as, in everyone's eyes, it was merely a regular promotion for digital accessories.

Even in 2024, there was still an opportunity to catch the "last train"—a Lexar DDR4 16GB desktop memory stick was sold for just 179 yuan on an e-commerce platform. However, despite a 99% approval rating, no one realized that this would be the "swan song" of low prices.

It wasn't until the e-commerce promotion season at the end of October this year that consumers discovered a complete reversal in the market when they wanted to purchase memory in bulk.

According to a report by the Financial Investment News on November 6, at a digital supermarket in Chengdu, multiple computer assembly merchants stated that prices for products such as memory sticks had fluctuated greatly this year. The 16GB DDR4 memory stick, which could previously be purchased for over 200 yuan, now sells for over 400 yuan. On e-commerce platforms, the same Lexar DDR4 16GB memory stick, which was sold for just 179 yuan last year, now has an official flagship store price of 699 yuan, more than tripling in just over a year.

Not only "mainstream" DDR4, but since this year, some DDR5 memory sticks priced at over a thousand yuan have risen from over a thousand yuan to nearly two thousand yuan. For example, on an e-commerce website, the G.Skill Trident Z Royal 32GB DDR5-6000 is now sold for 2,500 yuan, the Acer Predator 48GB DDR5-6000 has risen to 2,000 yuan, and the Asgard Valkyrie 32GB DDR5-6000 is priced at 1,700 yuan, representing a 100% increase or even more compared to two months ago.

Data from TrendForce is even more direct: In the third quarter of 2025, DRAM (Dynamic Random Access Memory) prices soared by 171.8% year-on-year, while the international spot gold price increased by less than 110% during the same period—the profitability of memory sticks has even surpassed that of traditional safe-haven asset gold—earning them the nickname "Electronic Moutai" in full swing.

Wholesalers in Shenzhen's Huaqiangbei area had a premonition of this. In August, they noticed that memory prices were "changing daily," and even mobile phone flash memory was rising. Digital merchants in Hangzhou and Changsha confirmed that mainstream DDR4 memory stick prices doubled in August, with some models surging by 200%. Industry insiders stated frankly, "The supply shortage situation cannot be reversed in the short term."

In fact, not only are memory prices rising, but solid-state drive (SSD) prices are also following suit. The Financial Investment News also mentioned in its November 6 report that the average channel price of mainstream 1TB PCIe 4.0 SSDs has increased by over 60% compared to the beginning of the year, with some popular models rising by over 80%. When a consumer recently prepared to purchase a Kingston 1TB SSD, they found that it cost only 369 yuan on February 5 of this year, but by November 5, the price had risen to 579 yuan, an increase of about 57%.

Who's Hyping Up 'Electronic Moutai'?

In October, Chen Libai, Chairman of ADATA, a leading domestic memory stick brand, stated that the current situation of comprehensive shortages and price increases across the four major storage categories—DRAM, NAND flash memory, SSD solid-state drives, and HDD mechanical hard drives—was unprecedented in his over thirty years in the industry.

Behind this "super cycle" is not just simple market fluctuation but a spark created by the collision between the explosion of the AI industry and global capacity restructuring, compounded by multiple factors that make the depth and duration of the price increase far exceed previous instances.

Firstly, the rise of the AI industry is the largest source of incremental demand, with server demand in the industrial sector placed at the highest priority.

With the explosion in demand from the AI industry, AI model training and big data processing require massive amounts of high-bandwidth, low-latency memory support. Data shows that a single AI server requires eight times more DRAM than an ordinary server, and projects like OpenAI's "Stargate" require up to 900,000 DRAM wafer supplies per month, a figure close to 40% of global DRAM production—greatly driving up server memory demand.

A report by TrendForce proposes that the DDR4 market will continue to face supply shortages and strong price increases in the second half of 2025. Due to rigid server orders squeezing supply for the PC and consumer markets, PC OEM manufacturers have to accelerate the adoption of DDR5 solutions, while consumer-grade manufacturers face challenges of high prices and difficulty in obtaining materials. The tight supply-demand situation in the DDR market has also driven up contract prices for mobile DRAM.

Secondly, structural contraction on the supply side has amplified the supply-demand imbalance, with the capacity strategic shifts of global storage giants becoming a key variable.

Public reports show that Samsung and SK Hynix of South Korea, which control about 70% of the global DRAM chip market, have accelerated their shift towards high-end chips such as HBM and DDR5, directly squeezing the capacity space for DDR4 and reducing DDR4 production, leading to supply shortages in the market.

Chen Libai also specifically mentioned that the three major international storage manufacturers have decided to stop producing DDR4 and have dismantled relevant old equipment, meaning it is almost impossible for them to resume DDR4 production, thus the market supply gap will continue to widen.

Regarding the continuous price impact on the market caused by supply-side production cuts, a September survey by TrendForce showed that the three major DRAM (mainstream memory chip type) manufacturers—Samsung Electronics, SK Hynix, and Micron—are continuously prioritizing capacity allocation to high-end server DRAM and HBM (High Bandwidth Memory), directly leading to squeezed capacity for memory chips needed in consumer electronic devices such as mobile phones and PCs. Combined with differentiated demand for terminal products, the institution judged at the time that price increases for old-process DRAM in the fourth quarter of 2025 would still be significant, while price increases for new-generation products would be relatively moderate.

At the same time, analyst Xu Jiayuan also pointed out that original manufacturers' capacity is being prioritized for high-end server DRAM and HBM, squeezing the supply of old-process products such as DDR4 and LPDDR4X needed in traditional consumer electronics. The shortage of DDR4 may persist until the first half of 2026.

Thirdly, the recovery of the consumer electronics market and demand growth in emerging intelligent fields have further exacerbated the supply-demand contradiction.

After hitting a low in 2023, the consumer electronics market finally saw a recovery at the end of 2024. Coupled with mobile phone manufacturers waving the promotional banner of "upgrading standard storage capacity," it directly raised the demand threshold for storage chips among users.

At the same time, the explosive growth in the fields of smart cars and autonomous vehicles has also brought greater pressure on the demand for mobile DRAM—driven by smart cockpits, ADAS, and autonomous driving technologies, vehicle storage capacity is breaking through from 512GB to 1TB.

Fourthly, market speculative behavior has amplified price fluctuations.

As netizens have said, if they had known earlier and stocked up on 16GB DDR4 memory, it would now be equivalent to holding "Electronic Moutai," achieving complete financial freedom.

Earlier, industry insiders revealed that in early 2025, many dealers predicted through industry channels that storage particles would increase in price and began massive purchasing and hoarding to lock in prices. By the second quarter of 2025, the spot circulation volume of DRAM in the Huaqiangbei market had significantly decreased, with some merchants even "locking up" DDR4 and DDR5 memory sticks, waiting for subsequent price increases before selling.

On e-commerce platforms, some merchants also used "memory as an investment" as a gimmick for marketing, artificially creating a tense atmosphere and driving up prices irrationally. Although the speculative behavior of merchants triggered resistance from consumers, leading e-commerce platforms to quickly clean them up, the trend of rapid upward price fluctuations in the memory market had become irreversible.

A Get-Rich-Quick Opportunity or a Speculative Trap?

Will "Electronic Moutai" continue to rise? The answer is yes.

From a market perspective, the shift from DDR4 to DDR5 and HBM is irreversible, just as the transition from feature phones to smartphones was in the mobile phone market. From a capital perspective, the continuous rise in the memory market will bring more profit opportunities, and speculators will inevitably not let the market cool down easily.

However, not everyone has the ability to become a "speculator." Similar dramas have already played out among speculators who hyped up gold.

In April 2013, the international gold price suddenly experienced a "frightening plunge," falling from $1,550 per ounce to around $1,320, with a maximum single-day drop of $135 and a total drop of over 10% in just a few days. When this "bottom-fishing opportunity" was discovered by "Chinese aunties," they spent tens of billions of yuan to sweep up 300 tons of gold in just 10 days, causing foreign media to exclaim that "Chinese aunties are taking on Wall Street alone."

However, after the collective bottom-fishing by "Chinese aunties," the gold price did not rebound as expected but continued to fall, reaching a low of $1,049 per ounce at one point. The aunties who bottom-fished not only got "flash-backed" but were also trapped for a long time from 2013 to 2019.

The current speculation in the memory market is even more perilous than gold speculation. After all, from a temporal perspective, the recent gold market has been sufficient to allow the aunties who entered in 2013 to fully recover and even achieve significant profits. However, memory product upgrades stem from the overall iteration of the technology industry, and the price transmission chain in the storage industry is long, often taking time to spread from the industry side to the consumer market. By the time ordinary consumers know that "memory prices are rising," the so-called "speculative opportunities" have already passed, leaving only the "pitfalls" for "bag-holders."

For ordinary people, the answer to the question "How to face 'Electronic Moutai'?" is actually simple: If it's a rigid need for assembling a computer or upgrading equipment, there's no need to overthink short-term price fluctuations—buy early, use early, and have peace of mind early. However, if you want to follow the trend and hoard goods for speculation, you will likely end up with losses outweighing gains.

Memory is ultimately a core accessory serving technology products, not "Electronic Moutai" for speculation. Understanding the logic behind industry fluctuations and seeing clearly the trend of AI-driven technological changes is far more meaningful than quibbling over a few hundred yuan in price differences.

Raising the perspective to the industry level, this price surge also hides opportunities for domestic storage to break through. Counterpoint predicts that Changxin Technology's DRAM shipments are expected to increase by 50% year-on-year in 2025, with its global market share rising from 6% in the first quarter to 8% in the fourth quarter. Yangtze Memory Technologies plans to increase its monthly production capacity to 150,000 wafers by the end of 2025 and reach a total capacity of 300,000 wafers per month by 2028, aiming to occupy 15% of the global NAND market share.

The process of domestic substitution is accelerating. When domestic production capacity continues to release and AI demand enters a stable period, the bubble of hoarding and speculation will eventually burst. By then, both merchants with a speculative mindset and individuals who follow the trend may become "memory bag-holders," facing huge losses.

This "super cycle" in the storage industry will ultimately return to rationality. The ones who will truly laugh last are not those hoarding goods for speculation but enterprises that master core technologies and steadily expand production, as well as ordinary people who see the trend and consume rationally.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan