Xiaomi: From Heaven to Hell in a Plunge, What Sustains the Faith?

03/25 2026

03/25 2026

518

518

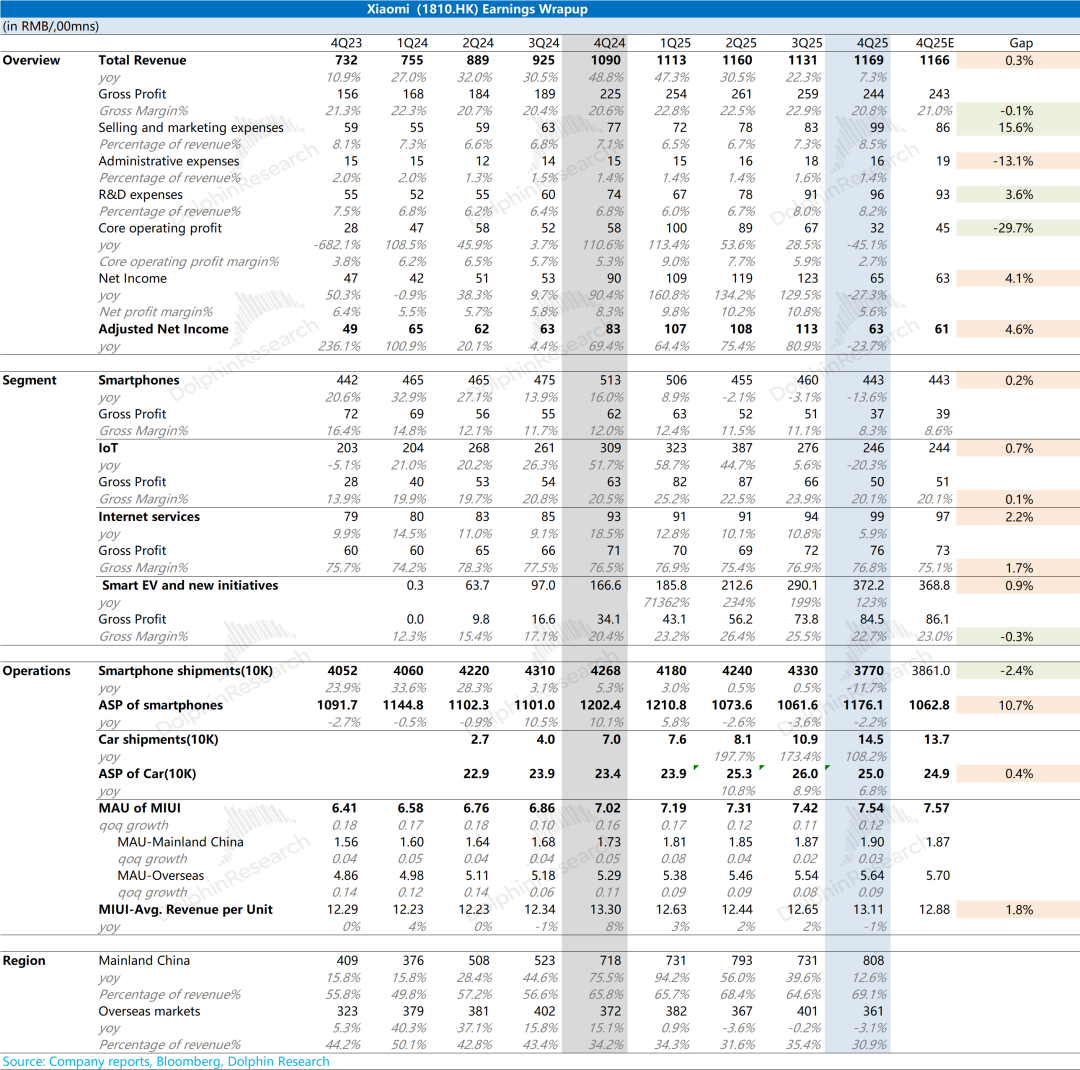

Xiaomi Group (1810.HK) released its financial report for the fourth quarter of 2025 (ending December 2025) after the market close in Hong Kong on the evening of March 24, 2026, Beijing time. Key points are as follows:

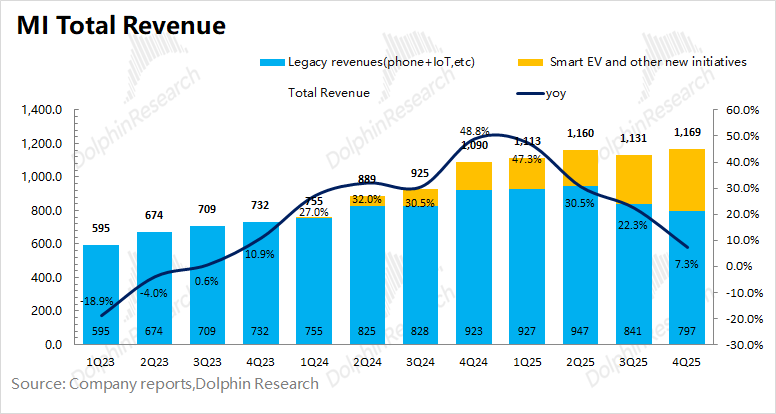

1. Overall Performance: Revenue reached RMB 116.9 billion, a year-on-year increase of 7%, with all revenue growth driven by the auto business, while the company's traditional businesses (smartphones x AIoT) saw a 13.7% year-on-year decline in revenue.

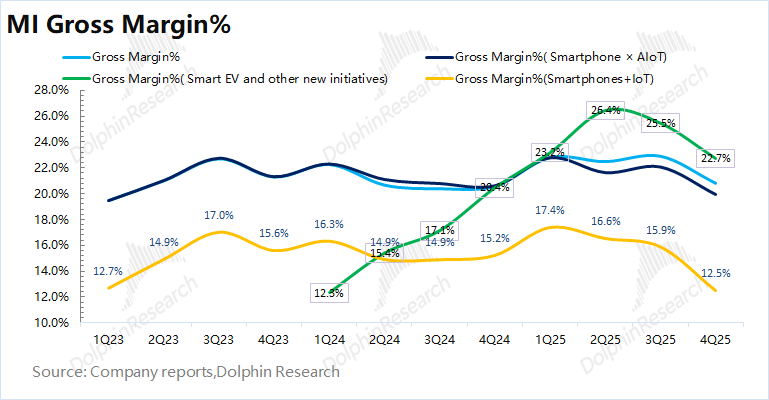

The gross profit margin dropped to 20.8%, primarily due to a significant decline in the gross profit margins of smartphones and IoT, while the gross profit margin of the auto business also began to decline this quarter.

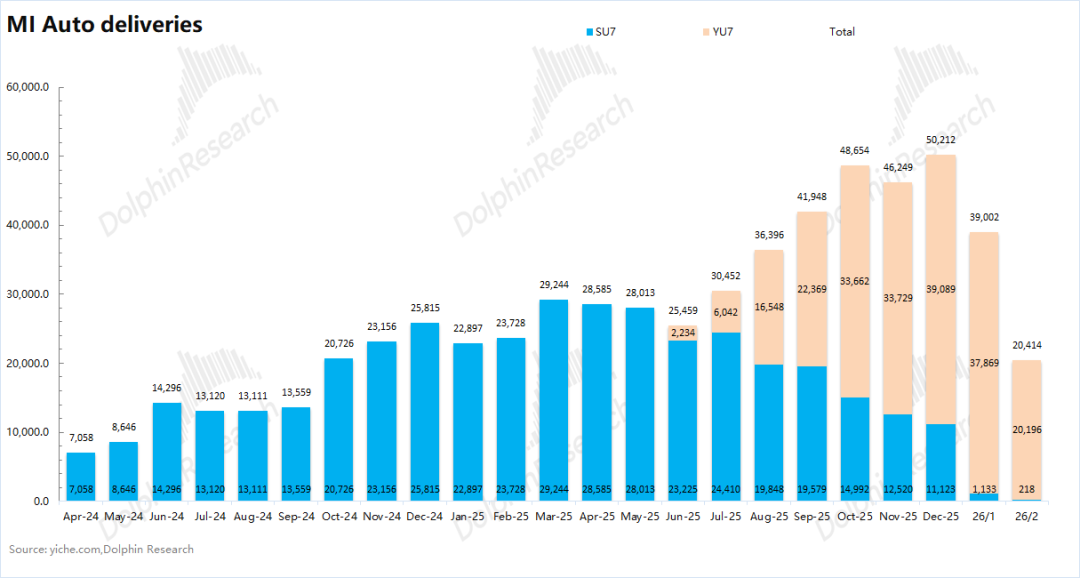

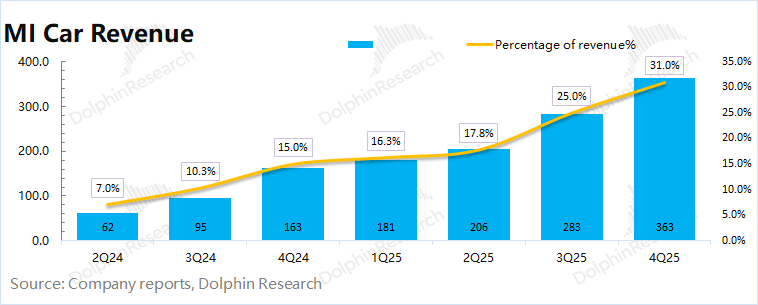

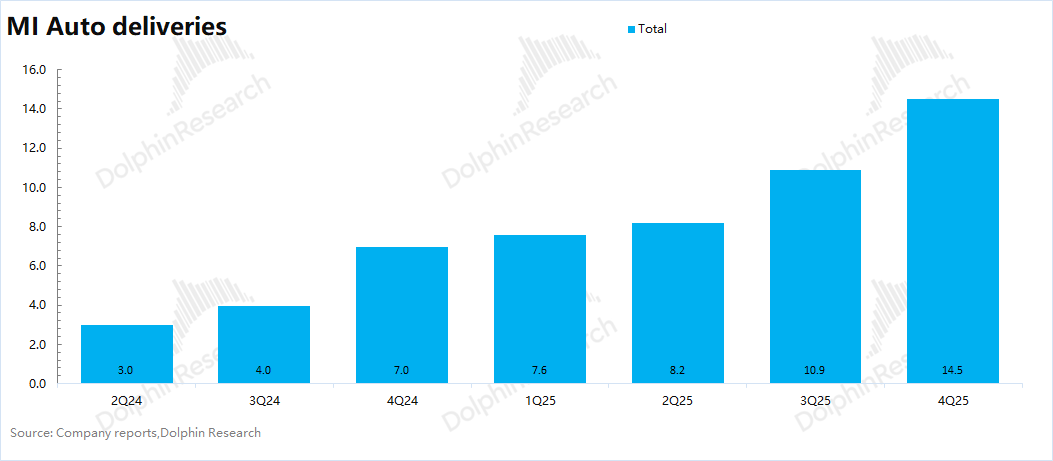

2. Auto Business: Revenue from auto-related businesses this quarter was RMB 37.2 billion, largely in line with expectations. The company shipped 145,000 vehicles this quarter, with the average selling price per vehicle dropping to RMB 250,000, mainly due to a decrease in the proportion of the relatively high-priced SU7 Ultra this quarter.

The gross profit margin of the auto business slipped to 22.7% this quarter, slightly below market expectations (23%). On one hand, it was affected by the decline in the average selling price per vehicle driven by the SU7 Ultra; on the other hand, the company sold a portion of its existing and display vehicles this quarter. Dolphin Research estimates that the core operating profit of Xiaomi's auto business this quarter was RMB 1.05 billion, achieving profitability for the second consecutive quarter.

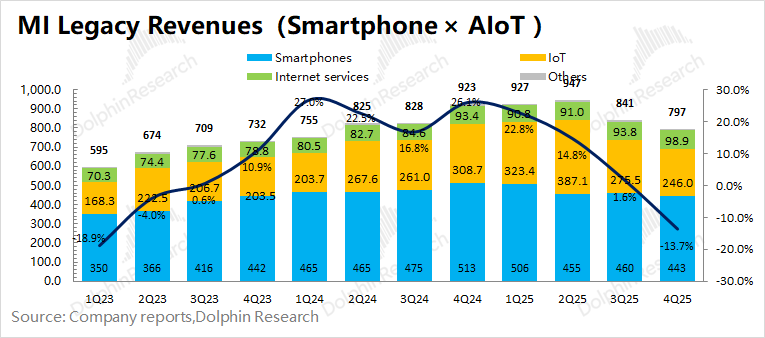

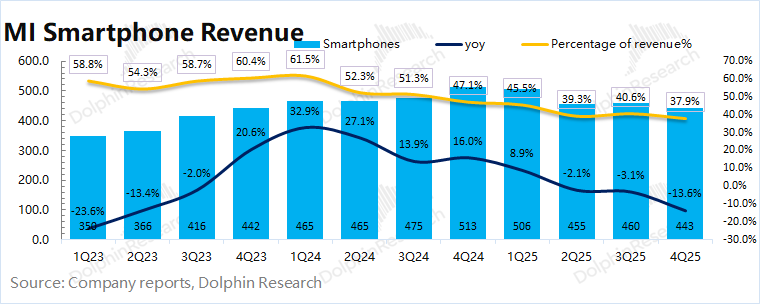

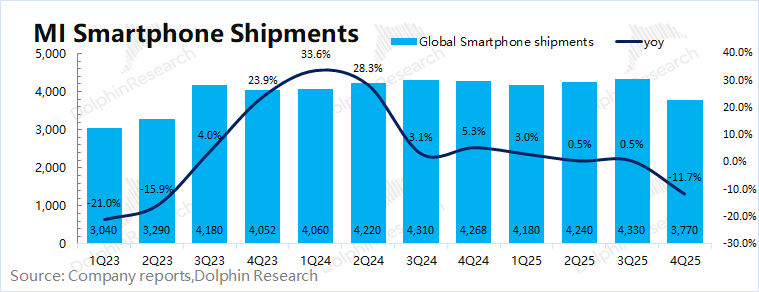

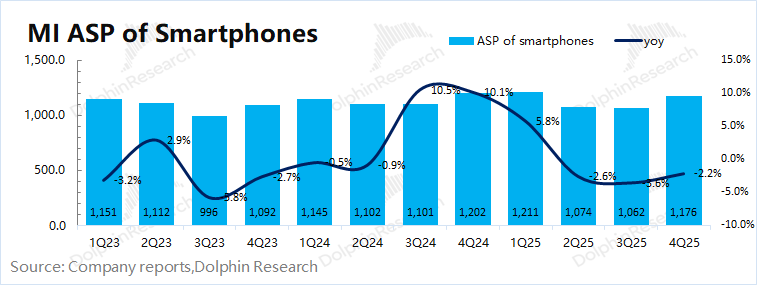

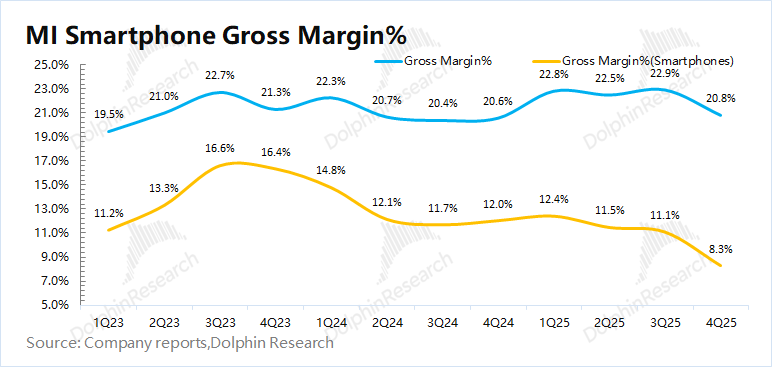

3. Smartphones: Revenue was RMB 44.3 billion, a year-on-year decline of 13.6%, in line with market expectations of RMB 44.3 billion. Xiaomi's smartphone shipments declined by 11.7% year-on-year this quarter, while the average selling price of smartphones declined by 2.2% year-on-year. Affected by market competition and tightened government subsidies, the gross profit margin of the smartphone business dropped significantly to 8.3% this quarter.

By market: Xiaomi's smartphone shipments in the domestic market declined by 18.2% year-on-year, while shipments in overseas markets declined by 8.8% year-on-year. The company performed worse in the domestic market this quarter. With continued rising storage costs, the gross profit margin of the smartphone business will continue to face pressure.

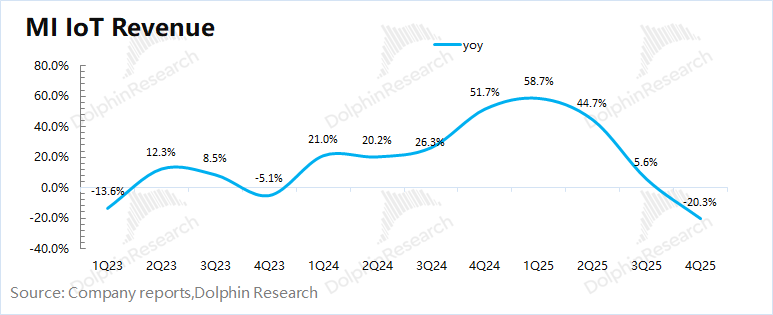

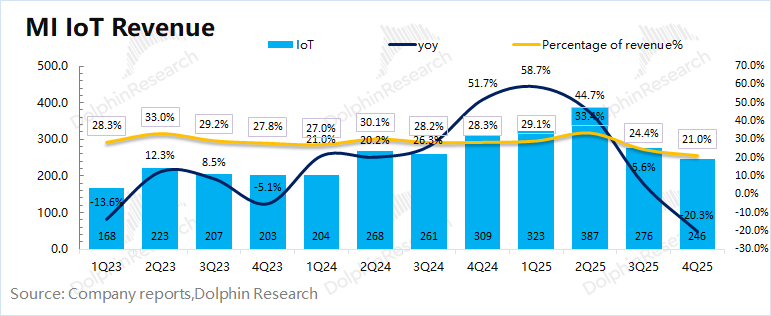

4. IoT: Revenue was RMB 24.6 billion, a year-on-year decline of 20%, in line with market expectations of RMB 24.4 billion, mainly due to the impact of reduced government subsidies and increased competition. In particular, the company's major appliance business was more significantly affected by government subsidy policies (some product subsidies may have reached RMB 1,000-2,000), with a 40% quarter-on-quarter decline this quarter.

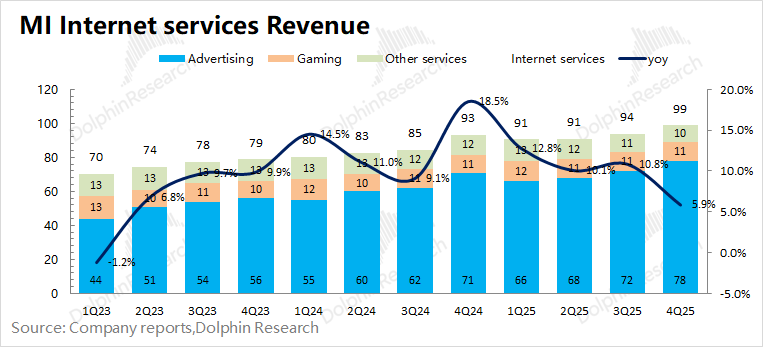

5. Internet Services: Revenue was RMB 9.9 billion, a year-on-year increase of 6%, slightly better than market expectations of RMB 9.7 billion. Growth was mainly driven by the advertising business, while value-added services saw a slight decline. The number of MIUI users increased by 7% year-on-year, while the ARPU value declined by 1% year-on-year.

By region: Overseas internet revenue was RMB 3.66 billion this quarter, while domestic internet revenue was approximately RMB 6.23 billion. The number of MIUI users in both domestic and overseas markets continued to grow this quarter.

6. Profit: Core profit was RMB 3.2 billion, and adjusted net profit was RMB 6.3 billion. The core profit of Xiaomi's traditional businesses was approximately RMB 2.14 billion, while the auto business achieved a profit of RMB 1.05 billion this quarter. The decline in the company's core profit this quarter was mainly due to the erosion of smartphone gross profit by rising memory costs and a significant decline in IoT revenue due to reduced government subsidies, leading to a 68% year-on-year decline in profit from traditional businesses.

Dolphin Research's Overall View: Traditional Businesses Under Continuous Pressure, Auto Business Needs 'Powerful' New Products

Xiaomi's financial report for this quarter is largely consistent with the previous Preview communication. Revenue growth this quarter was entirely driven by the auto business, while traditional businesses such as smartphones and IoT products faced significant pressure.

Based on the data from this quarter, Xiaomi is currently facing substantial pressure: (1) The gross profit margin of the smartphone business has dropped to single digits; (2) The IoT business has seen a double-digit year-on-year decline; (3) The gross profit margin of the auto business has declined, while weekly order data has also shown a noticeable drop.

Affected by factors such as continuously rising storage prices and tightened government subsidy policies, the company's stock price has dropped from HK$60 to around HK$30, reflecting market concerns about the company's auto and traditional businesses:

1) Auto Business: Annual Target of 550,000 Vehicles

Although Xiaomi Auto shipped 145,000 vehicles in the fourth quarter of 2025, sales in the first two months of 2026 have seen a 'cliff-like' decline, indicating that previous 'backlogged' orders have largely been digested.

During the previous financial report, Dolphin Research already mentioned the risks of Xiaomi Auto, noting that 'weekly orders for Xiaomi Auto had dropped to 4,000-5,000 vehicles, roughly corresponding to less than 20,000 new orders per month.' In early March, before the release of the new generation SU7, Xiaomi's weekly orders had dropped to around 4,000 vehicles.

From another perspective, the delivery lead time for the YU7 on Xiaomi Auto's official website has dropped to around 10 weeks, close to the normal waiting period, reflecting that a large amount of backlogged YU7 orders have been digested. The supply-demand relationship for Xiaomi Auto has shifted from 'supply falling short of demand' to 'supply exceeding demand.'

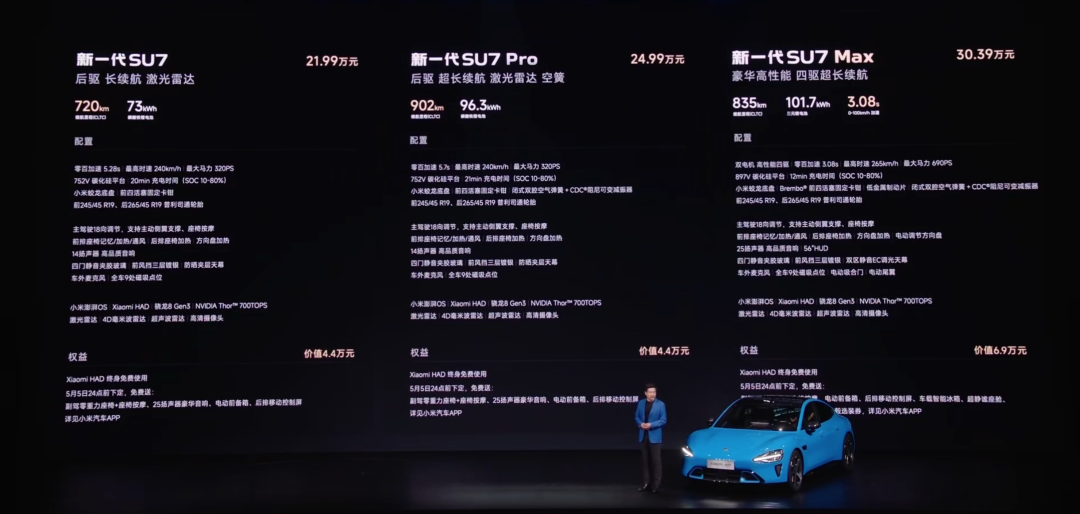

Regarding the recent new generation SU7, it is actually a 'mid-cycle refresh.' There are minimal changes in appearance, mainly hardware upgrades and a slight price increase. Based on the current estimated delivery time of around May-June on the official website, it is not a 'blockbuster product.'

For 2026, the company still sets a full-year auto sales target of 550,000 vehicles. With YU7 weekly orders dropping to a few thousand (equivalent to less than 20,000 vehicles per month) and a lukewarm response to the new generation SU7, the company needs to introduce more competitive models to achieve the above target, perhaps the highly anticipated extended-range models.

2) Traditional Businesses (Smartphones x AIoT): Dual Pressures from Tightened Government Subsidies and Rising Storage Costs

(1) Smartphone Business: Both shipments and gross profit margins declined significantly this quarter, mainly due to intensified market competition and rising storage costs.

As Apple's iPhone 17 series adopted a 'more for less' strategy, Apple's smartphone shipments in the Chinese market increased by 20% year-on-year (while the market declined by 0.8% year-on-year), whereas Xiaomi's shipments in the Chinese market dropped significantly by 18% this quarter.

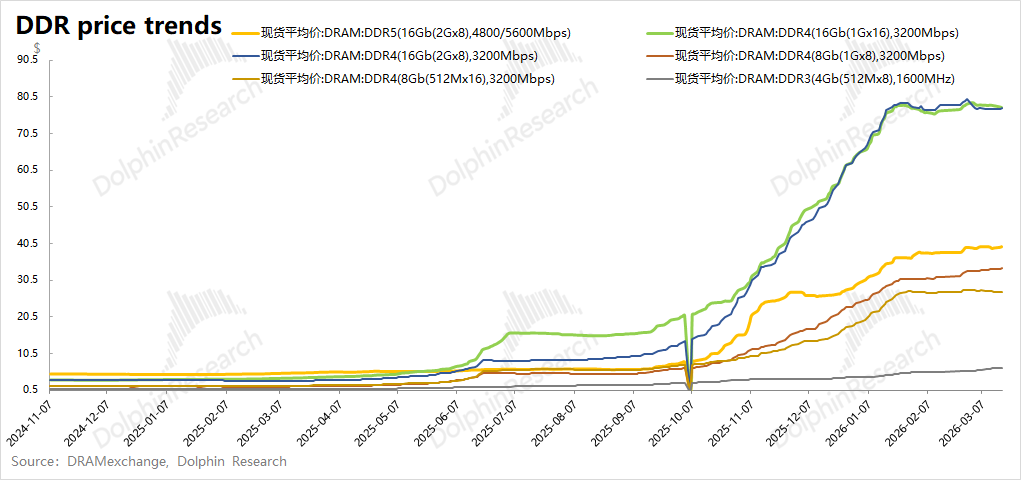

On the other hand, the sharp increase in storage prices has directly put cost pressure on Xiaomi smartphones. Based on communications with Qualcomm management, 'rising storage prices' have begun to escalate into a 'storage shortage,' which will directly impact smartphone market shipments.

(2) IoT Business: Tightened government subsidy policies have directly impacted IoT performance, with a significant decline (-20%) in IoT this quarter.

In the second half of 2025, various regions adjusted government subsidy policies to a 'coupon grab or lottery' format, effectively tightening the policies. As government subsidies for major appliances and other products can reach RMB 1,000-2,000, the tightening of subsidies directly affects purchasing demand in the terminal market, turning IoT from a 'growth driver' into a 'drag.'

Overall, the industry 'headwinds' faced by Xiaomi in traditional areas (smartphones and IoT) are difficult to avoid, and rising storage costs will continue to suppress the gross profit margin performance of traditional businesses. The company can only hope for 'better-than-expected performance from new vehicles' to support its business and stock price performance.

Under the current multiple pressures, Xiaomi's stock price has continued to decline. At this stage, it is relatively more important to estimate the bottom for Xiaomi.

Under a relatively pessimistic scenario (assuming a 15% year-on-year decline in Xiaomi smartphone shipments and a year-on-year decline in IoT), traditional businesses will see a single-digit year-on-year decline, while the auto business will achieve the company's target of 550,000 vehicles but with a decline in average selling price and gross profit margin. It is estimated that Xiaomi's core after-tax operating profit from traditional businesses in 2026 will be approximately RMB 12.9 billion, a 46% year-on-year decline; revenue from the auto business will be approximately RMB 140 billion, a 32% year-on-year increase.

As Xiaomi's traditional businesses face significant industry 'headwinds' in 2026, if storage prices subsequently decline, the company's traditional business performance will also rebound, making the 2026 performance relatively low.

Overall, Xiaomi is currently facing multiple industry 'headwinds,' including rising storage costs, tightened government subsidies, intensified competition, and a decline in auto orders. However, the company's stock price has continuously dropped from HK$60 to around HK$30, with some factors such as rising storage costs and tightened government subsidies already priced in.

As the company has 'potential' areas of focus such as new vehicles and large models, its medium- to long-term performance will depend on the stabilization of storage prices and the performance of subsequent new vehicles. A more detailed value analysis has been published in the article of the same name in the 'Updates - In-Depth (Research)' section of the Changqiao App.

The following is a detailed analysis:

I. Overall Performance: Auto Business as the Main Driver

With the addition of the auto business, Xiaomi's financial reports now include two new categories in addition to the previous 'Smartphones x AIoT': 'Auto and Innovation Businesses.'

Xiaomi's decision to disclose 'Auto and Innovation Businesses' as a separate category reflects the company's emphasis on the auto business. The company's market capitalization previously broke the trillion-dollar ceiling, mainly due to expectations from the auto business.

1.1 Revenue

Xiaomi Group's total revenue for the fourth quarter of 2025 was RMB 116.9 billion, a year-on-year increase of 7%, in line with market expectations of RMB 116.6 billion. Growth this quarter was mainly driven by the auto business.

1) Original Businesses - Smartphones x AIoT (Traditional Businesses): Revenue was RMB 79.7 billion, a year-on-year decline of 13.7%. Hardware business performance was 'very poor,' with smartphone revenue declining by 13.6% year-on-year and IoT revenue declining by 20% year-on-year.

2) New Businesses - Xiaomi's smart auto and other new businesses achieved revenue of RMB 37.2 billion this quarter, with growth mainly driven by increased shipments of the YU7.

1.2 Gross Profit Margin

Xiaomi Group's gross profit margin for the fourth quarter of 2025 was 20.8%, largely in line with market expectations of 21%. The gross profit margins of smartphones and IoT businesses declined significantly this quarter, while the gross profit margin of the auto business also decreased.

(a) The gross profit margin of Xiaomi's old businesses was 20%, a 2.1 percentage point decline quarter-on-quarter, mainly due to tightened government subsidies and rising storage costs. The smartphone business's gross profit margin dropped to 8.3% this quarter.

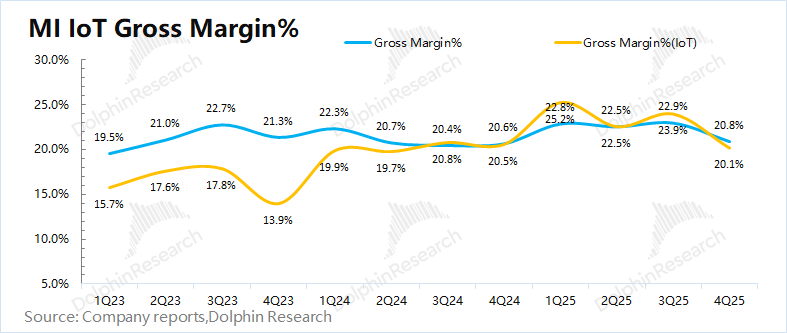

Other businesses within the company's traditional businesses continued to incur a gross loss of RMB 300 million this quarter, including services such as air conditioner installation. If this gross loss is included in the IoT business, the true gross profit margin of IoT should be around 18.9%.

2) The gross profit margin of new businesses such as auto was 22.7%, slightly below market expectations of 23%. The gross profit margin of the auto business declined quarter-on-quarter this quarter, affected by factors such as a decrease in the proportion of the relatively high-priced SU7 Ultra model and sales of existing and display vehicles.

II. Auto Business: Can the Annual Target of 550,000 Vehicles Be Achieved?

Revenue from the auto business was RMB 36.3 billion, and when combined with peripheral auto businesses, the total was RMB 37.2 billion, in line with market expectations of RMB 36.9 billion.

Shipments of 145,000 vehicles were largely as expected, with the average selling price per vehicle at RMB 250,000 this quarter, a RMB 10,000 decline quarter-on-quarter, affected by a decrease in the proportion of SU7 Ultra models and sales of existing and display vehicles.

The gross profit margin was 22.7% this quarter, a 2.8 percentage point decline quarter-on-quarter. The decrease in the proportion of SU7 Ultra shipments and sales of existing and display vehicles led to a decline in the average selling price per vehicle. The second-phase factory also contributed to increased depreciation and amortization, both of which led to a decline in the auto gross profit margin. ",

III. Smartphone Business: Gross Margin 'Collapse' and Loss of Market Share

In the fourth quarter of 2025, Xiaomi's smartphone business achieved revenue of RMB 44.3 billion, a year-on-year decline of 13.6%, primarily affected by rising storage costs, tightened government subsidies, and intensified competition.

Dolphin Research breaks down Xiaomi's smartphone business into volume and price components:

Volume: In this quarter, Xiaomi shipped 37.7 million smartphones, a year-on-year decline of 11.7%.

Breakdown by market: ① Domestic market: Amid tightened government subsidies, Xiaomi's domestic market share declined to 13.2% (losing 2.8% year-on-year), influenced by intensified market competition; ② Overseas market: Xiaomi's smartphone shipments declined by 8.8% year-on-year, with its overseas market share dropping by 1.2% year-on-year.

Price: The average selling price (ASP) of smartphones in this quarter was RMB 1,176, a year-on-year decline of 2.2%, primarily due to the decline in ASP in overseas markets.

The gross margin for the smartphone business in this quarter was 8.3%, a quarter-on-quarter decline of 2.8 percentage points, mainly due to the decline in ASP for overseas smartphones, rising costs of core components such as storage, and intensified market competition. With continued increases in storage costs, the gross margin of the company's smartphone business will remain under pressure.

IV. IoT Business: Tightened Government Subsidies Become a 'Drag'

In the fourth quarter of 2025, Xiaomi's IoT business achieved revenue of RMB 24.6 billion, a year-on-year decline of 20%. Affected by tightened government subsidies, the large appliance category within the IoT business declined by 40% quarter-on-quarter, significantly dragging down the IoT business.

The gross margin for the IoT business in this quarter was 20.1%, a quarter-on-quarter decline of 2.8 percentage points, primarily due to the decline in gross margins for products such as smart large appliances in the Chinese market.

V. Internet Services: A Relatively Stable Growth Driver

In the fourth quarter of 2025, Xiaomi's internet services business achieved revenue of RMB 9.9 billion, a year-on-year increase of 6%. The main growth driver this quarter was advertising:

a) Advertising services: Quarterly revenue of RMB 7.8 billion, a year-on-year increase of 10.5%. The core advertising scenarios dominated by Xiaomi's advertising—app distribution and pre-installed apps—are almost essential distribution taxes for major app developers, especially pre-installed apps, where advertising generates almost effortless revenue.

b) Value-added services: This mainly includes game distribution, Xiaomi's e-commerce platform—Youpin, and Xiaomi Finance. Revenue in this category was approximately RMB 2.1 billion, remaining roughly flat year-on-year, indicating stability in these value-added services.

Overall, this business segment still relies on the revenue logic tied to hardware shipments in the long term. In Xiaomi's reclassified revenue categories, it is generally grouped under Legacy business. Only by integrating software and hardware can the company, as a smartphone manufacturer, continue to justify the logic of internet monetization.

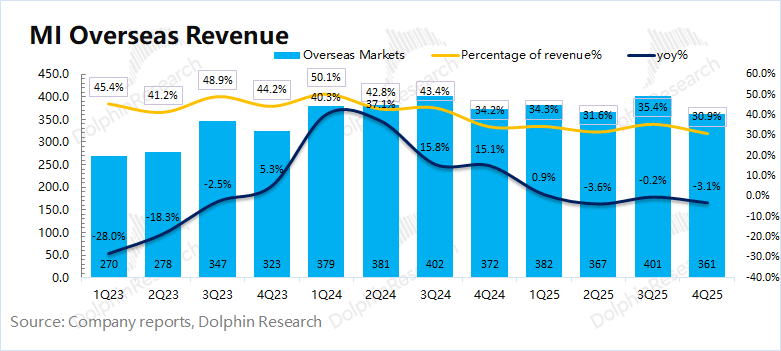

VI. Overseas Markets: Software Services Continue to Grow, Hardware Remains Sluggish

In the fourth quarter of 2025, Xiaomi's overseas revenue was RMB 36.1 billion, a year-on-year decline of 3.1%. With the growth of the domestic automotive business, the proportion of overseas revenue has declined to around 31%.

A detailed breakdown shows that Xiaomi's overseas internet business grew by 18% this quarter, reaching RMB 3.66 billion; however, the company's overseas hardware revenue declined by 5% year-on-year, marking a third consecutive quarter of year-on-year decline, reflecting continued weak demand in overseas hardware markets.

VII. Profit: Traditional Business Under Pressure, Automotive Business Remains Profitable

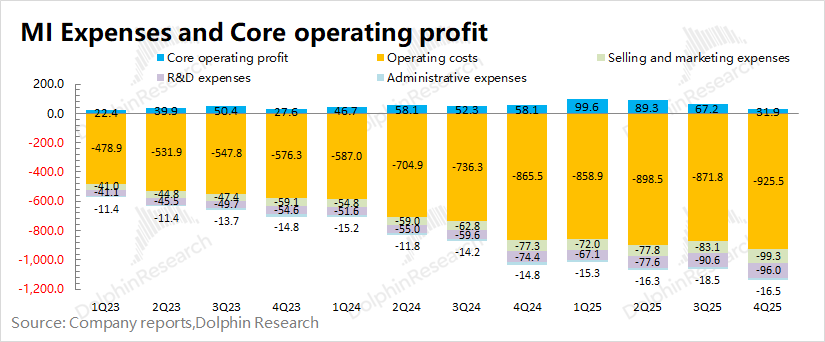

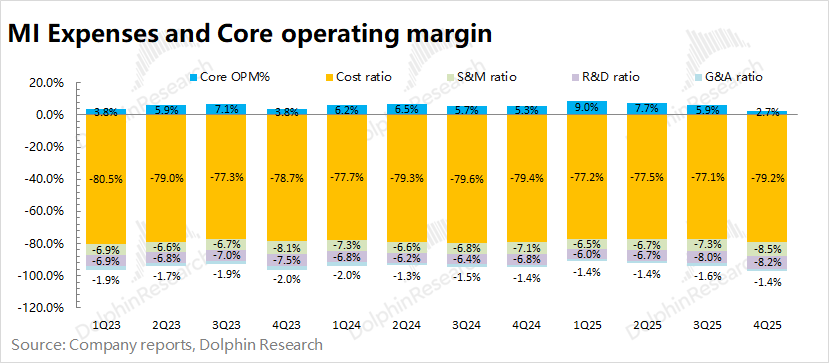

In the fourth quarter of 2025, Xiaomi's total operating expenses across three categories amounted to RMB 21.2 billion, with the expense ratio rising to 18%. Part of this increase was due to the automotive business, whose operating expenses rose to RMB 7.4 billion.

Excluding the automotive business, operating expenses for the traditional business segment were approximately RMB 13.77 billion, showing increases both year-on-year and quarter-on-quarter. The operating expense ratio for the traditional business rose to 17.3%, with the company further increasing R&D expenditures.

Adjusted net profit for the fourth quarter of 2025 was RMB 6.3 billion. However, Dolphin Research has consistently disagreed with Xiaomi's method of adjusting net profit—failing to exclude financial income and dividend income from invested companies. Even if sustainable, these do not represent the company's core business and cannot reflect long-term profitability.

Overall, Dolphin Research places greater emphasis on core operating profit (revenue - cost - operating expenses), as it more accurately reflects the company's ability to sustain profitability in its core business operations.

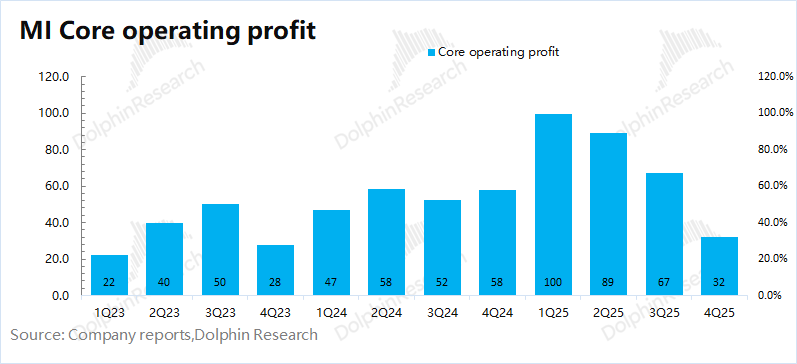

The company's actual core operating profit this quarter was RMB 3.2 billion, with a core operating profit margin of 2.7%, primarily due to pressure on hardware gross margins and increased expenses. Specifically, the core operating profit for the traditional business this quarter was approximately RMB 2.14 billion, while the core operating profit for the automotive business was approximately RMB 1.05 billion.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or opinions mentioned in this report shall not be regarded as an offer to sell or a solicitation to buy securities in any jurisdiction, nor do they constitute recommendations, inquiries, or endorsements of securities or related financial instruments. The information, tools, and data in this report are not intended for distribution to or use in jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations, or where Dolphin Research and/or its subsidiaries or affiliates are required to comply with registration or licensing requirements.

This report reflects only the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright owned solely by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once