DJI and Insta360 Price War: Mutual Loss Better Than One-Sided Win

06/12 2026

06/12 2026

537

537

Having a Rival Brings Peace of Mind

At 8 PM on June 10, Insta360 officially released the Luna Ultra. The standard set, priced at 3,999 yuan after national subsidies, sold out within 5 minutes across multiple e-commerce platforms.

It seemed like a successful debut, but over a month earlier, DJI's Osmo Pocket 4 had already slashed its price to 2,999 yuan. Combined with technical upgrades, the new product offered "more for less" compared to its predecessor.

According to Sina Tech, DJI's Pocket 4P is set for official release on the evening of June 15, with the standard version priced at 3,799 yuan—exactly 200 yuan cheaper than Insta360's Luna Ultra. This suggests a price war is inevitable.

Insta360's timing for releasing the new product also carries another layer of urgency.

The following day, Insta360 Innovation would mark its first anniversary as a listed company, with 227 million restricted shares facing unlocking. This wave of unlocking, equivalent to 56.5% of the total share capital, would expand the free float from 32.8 million to 259 million shares—nearly a sevenfold increase. As expected, the stock price opened lower and continued to decline.

The long-planned price war between the two sides has left neither with a clear advantage, revealing an obvious dilemma: mutual loss is preferable to one-sided victory.

01

Insta360 'Loses' First on the K-Line

From panoramic cameras to action cameras, from invisible selfie sticks to AI editing, Insta360 excels at packaging hardware into content creation tools. Combined with a price far lower than the previously rumored overseas price of 5,299 yuan, it's no surprise the Luna Ultra sold out in 5 minutes.

But the product's success can't hide the financial embarrassment.

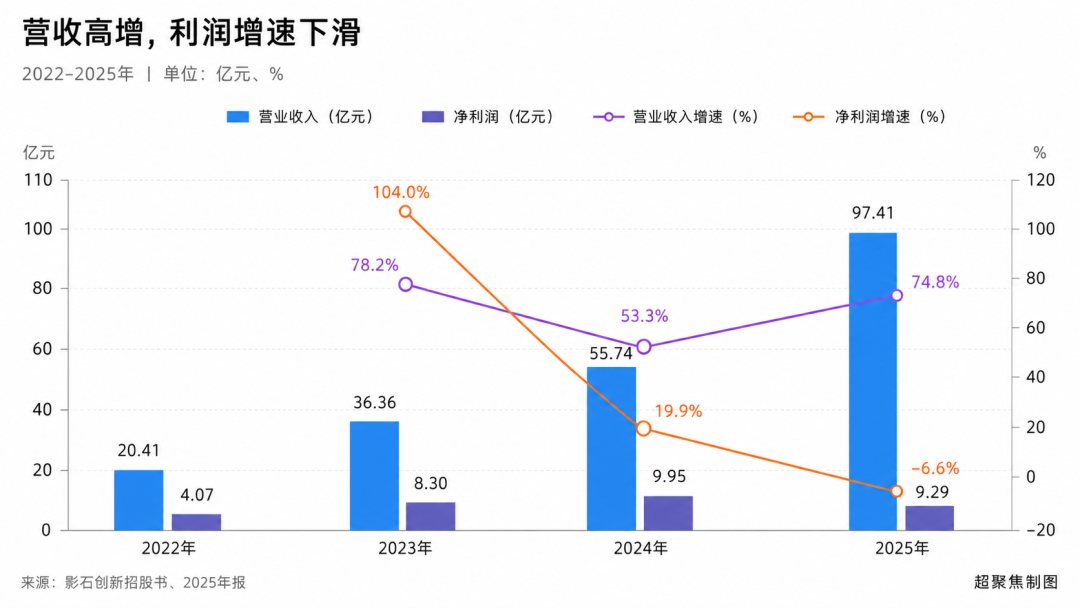

Annually, Insta360's revenue is still in the rapid-growth phase typical of startups, surging from 2.041 billion yuan in 2022 to 9.741 billion yuan in 2025—nearly quintupling in three years.

The issue is that revenue is racing ahead while profits lag behind.

Net profit was 407 million yuan in 2022, 995 million yuan in 2024, but fell to 929 million yuan in 2025. Revenue growth accelerated from 78.2% in 2023 and 53.3% in 2024 to 74.8% in 2025, while net profit growth plummeted from 104.0% in 2023 to 19.9% in 2024 and -6.6% in 2025.

More units are being sold, but profits are harder to come by.

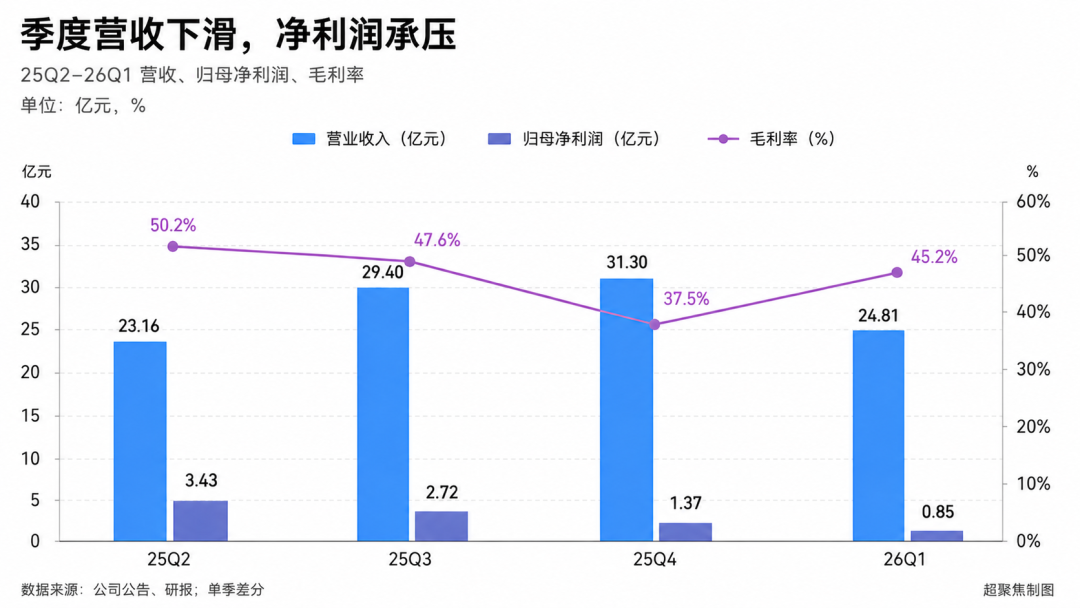

Quarterly data makes the problem clearer: from Q2 to Q4 2025, Insta360's revenue grew from 2.316 billion yuan to 3.130 billion yuan, but net profit attributable to shareholders dropped from 343 million yuan to 137 million yuan. By Q1 2026, revenue fell back to 2.481 billion yuan, with net profit at just 85 million yuan.

This is what the market truly fears: not that Insta360 can't sell, but that it's becoming increasingly costly to maintain sales.

After all, R&D, channel expansion, branding, and new product launches require investment. Moreover, DJI is a far tougher competitor than GoPro. While the Luna Ultra's sellout proves Insta360's product strength, declining profits show that strength is becoming more expensive.

This is also evident in gross margins: Insta360's domestic margin was 42.10% in 2025, lower than the 47.87% in overseas markets. The impact of the price war is already visible in financial reports.

Meanwhile, global memory chip price hikes are severely impacting vertical imaging devices. UBS estimates that due to chip inflation, Insta360's 2026 BOM costs will rise 9% year-on-year, dragging gross margins down by about 4 percentage points and net profit margins by approximately 2.9 percentage points.

If operational pressures are reflected in the income statement, the secondary market has already priced them directly into the K-line.

Market insiders note, "Insta360's situation resembles Roborock's a few years ago—both faced mass share unlocking after a year as a public company, coupled with intensifying competition and valuation pressure."

IDG Capital, an early investor in Insta360's Series A and B rounds, currently holds about 47.966 million shares after multiple equity changes, including VIE structure dismantling, capital increases, share reforms, and IPO. At the June 10 closing price of 163.45 yuan, this represents a market value of about 7.84 billion yuan (approximately $1.156 billion)—a paper gain of roughly 700 times.

IDG was also the second-largest shareholder of Three Squirrels. As soon as the lockup expired, it launched a reduction plan, selling shares at the maximum allowable level multiple times before fully exiting by Q1 2026. After Ecovacs' lockup expired, IDG similarly reduced its stake immediately and eventually cleared its position.

Qiming Venture Partners entered later, participating in Series B and C rounds with a total investment of $5.25 million for about 368,000 shares. By 2019, through equity transfers, Qiming had largely recouped its costs. Its current 33.84 million shares are worth about 5.5 billion yuan—almost entirely profit.

On Roborock's lockup expiration day, Qiming, along with GaoRong Capital, Shunwei Capital, and seven other shareholders, announced plans to reduce their stakes by 11.10%—worth over 7 billion yuan at the time. Roborock's market cap subsequently crashed from nearly 100 billion yuan to 20 billion yuan, with Qiming reducing its stake all the way down before exiting the top 10 shareholders.

One year after listing, Insta360's stock price has completed a full rollercoaster cycle. On its debut, the company's A-share market cap exceeded 70 billion yuan, peaking near 140 billion yuan before falling back below 70 billion yuan.

Currently, about 166 Insta360 employees hold 0.7% equity through strategic placements, with an issue price of 47.27 yuan and an average current market value of 3 million yuan per person. However, cash compensation before the IPO was below industry averages, and employee shares are locked for 36 months.

Senior executives have made substantial financial commitments: CEO Liu Liang invested 8 million yuan, director Jia Shun 5 million yuan, and board secretary Li Yang 4 million yuan—totaling 17 million yuan, or 12% of employee purchases.

Financial investors with extremely low holding costs, facing massive paper gains after a decade-long investment cycle, inevitably prefer to cash out.

02

DJI's Gates Are Surrounded by Familiar Faces

If Insta360's dilemma is "growth without profitability," DJI faces talent outflow and industry coevolution.

In March 2026, DJI filed a lawsuit with the Shenzhen Intermediate People's Court, claiming ownership of six core patents related to flight control, structure, and image processing.

DJI alleged that these patents were developed by former key R&D personnel within one year of their departure, with technical content "closely related" to their original roles at DJI, and thus should be considered work-for-hire inventions.

In two domestic patent applications involving drone flight control and structural design, Insta360 listed some inventors as "requesting anonymity" but disclosed their real names in corresponding international applications. These individuals were former core employees who had deeply participated in DJI's key drone R&D projects.

This patent dispute is just one facet of DJI's talent outflow.

Over the years, people leaving the DJI ecosystem have become external variables. According to IT tangerine ie, nearly 20 "DJI-affiliated" startups secured funding in 2025—a five-year high.

Tao Ye founded Bambu Lab, Zhang Junbin established Narwal Robot; Yishi Zhihang's founder Chen Yilun, formerly DJI's chief machine vision engineer, completed $120 million and $122 million funding rounds in March and July 2025; Xuandi Power, led by Ou Di, former head of DJI's Inspire series, focuses on quadruped robots; Kuangye Innovation's founder Gong Ding, a former DJI perception algorithm lead, shifted to outdoor smart vehicles...

DJI's countless alumni have practically occupied every track (track) DJI might enter.

Frank Wang (DJI founder) compares this to "shedding leaves": "Early on, everyone was a technical expert. As the company grew, some needed to transition to management roles, but many weren't suited or willing. With so much capital waiting outside, they left."

What the outside sees as "brain drain," DJI sees as "replacement." In 2025, DJI's revenue approached 80 billion yuan, expected to exceed 100 billion yuan in 2026. Product launches haven't slowed, with action cameras maintaining over 60% global market share and panoramic cameras capturing nearly half the market with a single model, the Osmo 360.

These figures suggest DJI's core innovation capacity continues to strengthen, making talent retention less critical.

However, the sustained talent outflow is objectively reshaping the smart imaging industry's competitive landscape. DJI's alumni, armed with its methodologies and technical know-how, are dispersing into various niches—some directly competing with DJI, others forming ecological complements in broader hardware fields.

From this perspective, DJI faces a different challenge than Insta360: how to maintain core technological barriers while exporting talent.

The industry's true rivals aren't each other.

Huawei ecosystem companies, OPPO, Vivo, Honor, and other smartphone brands are entering the imaging peripheral and gimbal market. These firms boast larger user bases, more mature brand recognition, and stronger supply chain integration capabilities. Xiaomi's "Pocket Eye" project is priced at half of DJI's equivalent products.

DJI and Insta360 are vying for the mid-to-high-end market targeting professional and semi-professional content creators. But smartphone brands aim for broader consumer users. If they can drive imaging peripheral prices below 1,000 yuan through ecological synergy, the entire market's pricing logic will be rewritten.

Neither DJI nor Insta360 can retreat from the price war, nor can they indefinitely sustain shrinking profit margins. Thus, their choices converge: pivot.

Insta360 opts to trade short-term profits for future growth. Its Q1 net profit margin fell to 1.31%, with R&D spending exceeding profits by over five times and inventory swelling to nearly 3.8 billion yuan. Yet CEO Liu Jingkang insists on advancing the "photography robot" strategy.

DJI chooses to trade profits for market share. The Pocket 4's 500-yuan price cut and upgraded specs aim to squeeze competitors' survival space and consolidate its market position. DJI's scale supports this strategy, but the cost is margin compression.

In consumer electronics—where technology iterates rapidly, product lifecycles are short, and price wars are normalization (normalized)—mutual loss often trumps one-sided victory. A firm that undercuts rivals to dominate the market then faces fewer players, slower innovation, and a lower industry ceiling.

GoPro's decline offers a cautionary tale. When competition enters a price-cutting phase, few survivors emerge unscathed. Both DJI and Insta360 understand this, but neither is willing to yield first.

Sigmaintell Consulting predicts gimbal camera shipments will reach 14.8 million units in 2026, growing over 16-fold in three years. The increment (increment) is large enough to accommodate multiple head players (market leaders).

The issue is that neither side currently intends to "coexist peacefully." DJI has positioned itself at 2,999 yuan, Insta360 at 3,999 yuan—leaving no clear safety zone for the other.

This suggests the price war may end not with one side collapsing, but with both reaching a fragile equilibrium at their respective cost tolerance thresholds.

- END -

-

![]()

Apple Shareholders Paid $230 Billion in 'Make-Up Exam Fees' for Apple's AI

-

![]()

Oracle Plummets? The Irreparable Flaws Beyond AI Infrastructure - 'High Interest, High Debt + Stagnant Software'

-

![]()

Oracle Plummets? The Irreparable Damage That AI Infrastructure Can't Fix—'High Interest, High Debt + Failing Software'

-

![]()

The Largest IPO in History Is on the Horizon: Why SpaceX Justifies a $1.75 Trillion Valuation

-

![]()

Cook's Gourd Holds No Magic Cure for Apple's AI Woes

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Can't Even Uber Sustain AI Token Costs?

-

Unitree Goes Public, Ushering in an Era of Capital Frenzy for Robots?

-

![]()

In-Depth Exploration of the Physical AI Industry Ecosystem