Monthly Report | Online Market of Home Surveillance Cameras in May: Declining Sales Volume, Rising Prices, and Structural Upgrades Dominate

06/24 2026

06/24 2026

435

435

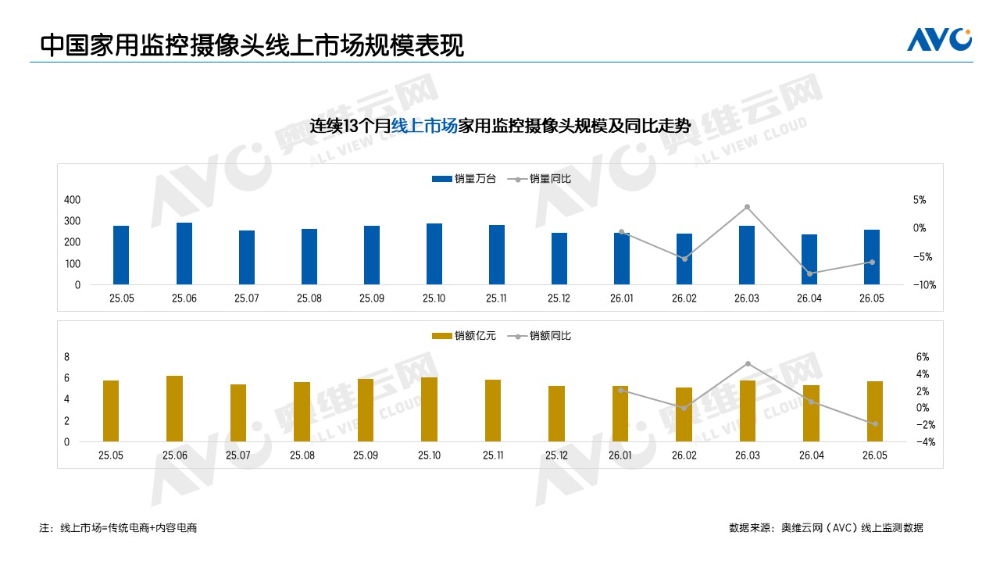

I. Scale Performance: Online Retail Volume Decline Narrows, Average Price Rise Supports Sales Value. According to the AVC Report on the Online Market of Home Surveillance Cameras in China, in May 2026, the online market for home surveillance cameras in China (including traditional e-commerce and content e-commerce, hereinafter the same) had a retail volume of 2.609 million units, a year-on-year decrease of 6%, and retail sales of 570 million yuan, a year-on-year decrease of 2%. With the 618 mid-year promotion starting in May, market vitality significantly rebounded compared to April this year, with retail volume increasing by 10.3% month-on-month.

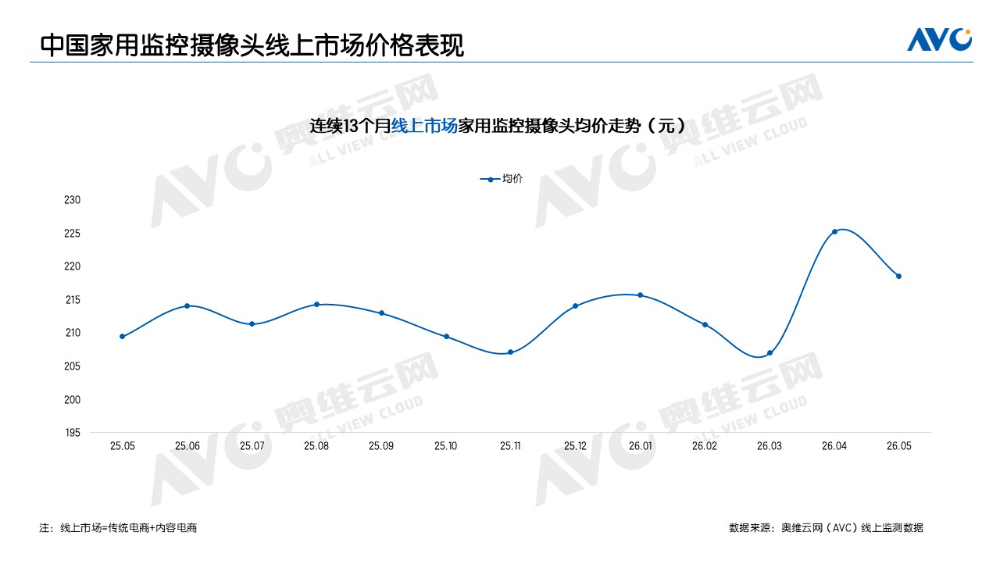

The year-on-year decrease in retail sales was smaller than that in retail volume, primarily due to the structural increase in the average price. Online monitoring data from AVC showed that the average market price of online home surveillance cameras in May reached 219 yuan, a year-on-year increase of 4%. The year-on-year increase in the average price was mainly driven by the rise in the proportion of mid-to-high-end products, with the retail volume share of the 300 yuan and above price segment reaching 16.3%, an increase of 4 percentage points year-on-year. During the promotion period, discounts increased, and while the average price in May increased year-on-year, it decreased by 3% month-on-month compared to April.

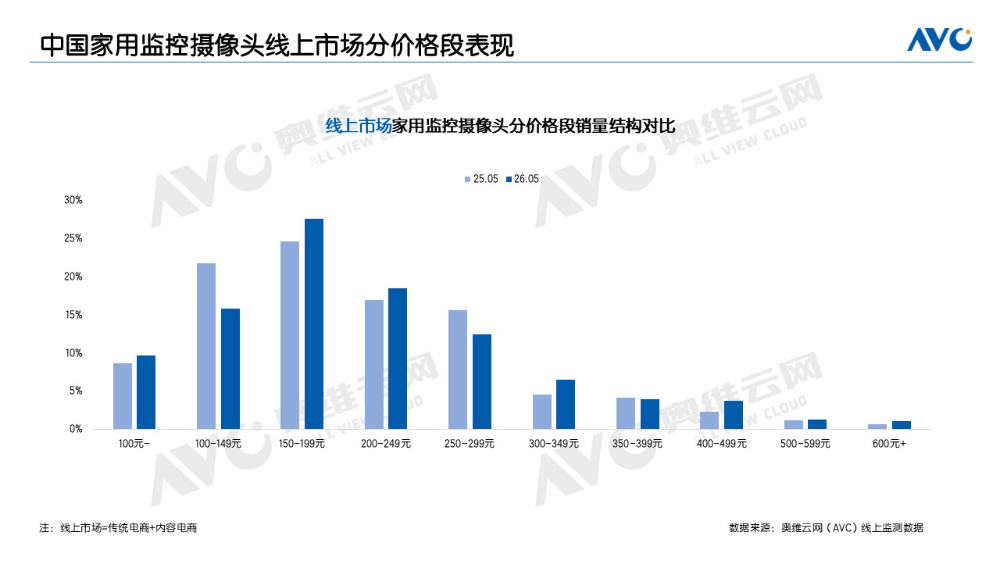

II. Price Structure: Some Price Segments Under Pressure, Product Structure Adjustments. From the perspective of the retail volume structure by price segment, the share of the below-100 yuan price segment was 9.6%, an increase of 1 percentage point year-on-year, mainly contributed by low-priced products for traffic attraction in content e-commerce, reflecting to some extent the resilience of demand in lower-tier markets. The 100-149 yuan price segment significantly contracted, accounting for 15.7%, a decrease of 6 percentage points year-on-year, facing pressure from both lower and higher price segments, with low-end users migrating to below 100 yuan and mid-end users upgrading to the 150-199 yuan segment. The 150-199 yuan price segment accounted for 27.6%, an increase of 3 percentage points year-on-year, becoming the main price segment in the market, with high consumer acceptance of mid-range prices.

The 200-249 yuan price segment accounted for 18.4%, a slight increase of 1.5 percentage points, mainly contributed by traditional e-commerce, promoting steady expansion of this price segment's market share. The 250-299 yuan price segment also faced pressure, accounting for 12.4%, a decrease of 3 percentage points year-on-year, with consumers' willingness to 'upgrade' in this price segment increasing, mainly shifting to the 300 yuan and above segment for structural upgrades. The overall share of the 300 yuan and above price segment reached 16.3%, with the 300-349 yuan and 400-499 yuan sub-segments showing relatively prominent growth, accelerating the expansion trend of the mid-to-high-end market.

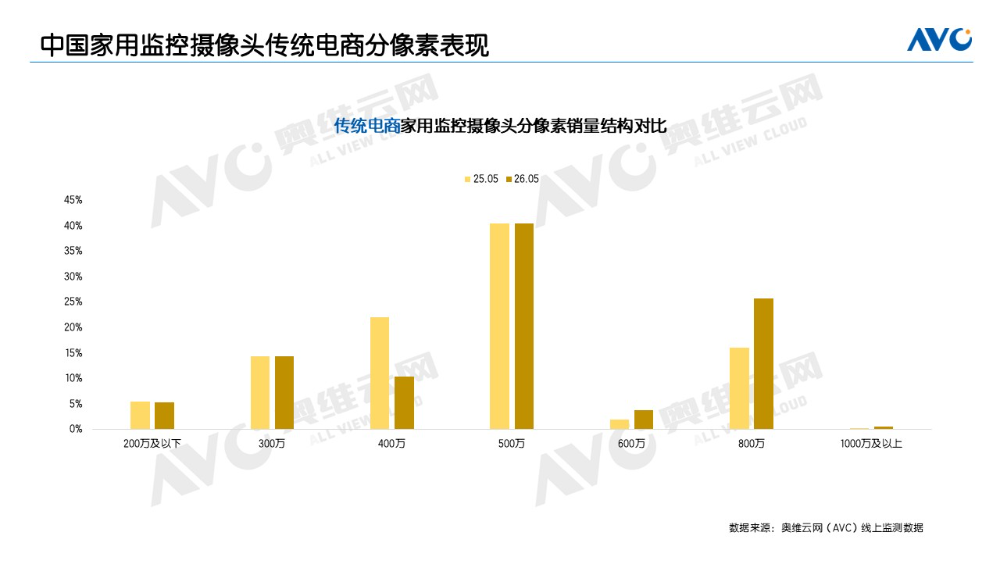

III. Product Trends: Rapid Penetration of High-Pixel Cameras, Steady Growth in Niche Segments. (I) Continuous Deepening of Pixel Upgrades. From the pixel distribution on traditional e-commerce platforms, the market in May was still dominated by 5-megapixel cameras, accounting for over 40% of retail volume. Consumer demand for high-definition image quality continued to rise, with 8-megapixel products rapidly growing, accounting for 25.6%, a significant increase of 9.5 percentage points year-on-year, becoming the second-largest pixel segment. The share of 4-megapixel cameras contracted by nearly 12 percentage points to 10.3%, with its market share being rapidly replaced by 6-megapixel and 8-megapixel cameras. Low-pixel products still had a certain existing market, with the shares of 2-megapixel and below and 3-megapixel cameras remaining largely unchanged year-on-year.

(II) Highly Concentrated Product Types. In terms of product types on traditional e-commerce platforms, indoor pan-tilt cameras remained the core purchase in May, accounting for over half of retail volume at 53%; outdoor dome cameras followed closely, accounting for over 32%, with the two categories combined accounting for over 85%. Portable cameras ranked third, accounting for 8% of retail volume, slightly contracting year-on-year.

(III) Accelerated Implementation of Niche Features. In terms of intelligent technology applications, in May, traditional e-commerce home surveillance cameras with pet detection functionality accounted for 27.5% of products, a significant increase of 11 percentage points year-on-year, showing strong growth momentum. This trend was driven by the continuous expansion of the pet-owning population and users' deepening demand for intelligentization (intelligent) household scenarios. Multi-camera products, through collaborative coverage from different angles, met users' monitoring needs for complex scenarios such as entire homes and courtyards, becoming an important direction for home security.

Online monitoring data from AVC showed that in May, the retail volume share of multi-camera products on traditional e-commerce platforms reached 37%, an increase of 4.2 percentage points year-on-year, and is expected to continue penetrating and growing in the future. In May, terminal flow products performed prominently in the traditional e-commerce market, accounting for 24% of retail volume, an increase of 5 percentage points year-on-year, representing a noteworthy incremental segment.",

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?