Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

06/25 2026

06/25 2026

364

364

Layout | Xiaoxi

In the fiercely competitive consumer electronics sector, a showdown in brick-and-mortar stores is almost inevitable.

On the evening of June 23, DJI's Osmo Pocket 4P Pocket Cinema Camera officially hit the shelves, with prices starting at 3,799 yuan. However, several DJI stores across domestic cities reported being out of stock. Meanwhile, on June 22, Insta360 responded to investor inquiries on an interactive platform, stating that its products are distributed globally through a blend of online and offline channels.

Over the past year, patent disputes between DJI and Insta360 have dominated tech headlines. From the Shenzhen Intermediate People's Court to the U.S. District Court for the Eastern District of Texas, the two companies have repeatedly clashed over technical patents related to drones and panoramic cameras. The outside world often assumes that products, technology, and patents are the primary battlegrounds for these two Shenzhen-based tech giants. However, few have noticed that a retail rivalry, centered around "people, goods, and places," has already begun in shopping malls and commercial districts nationwide and even globally. In essence, the competition has entered a phase of direct confrontation in terms of offline store positioning, distribution system rivalry, and customer mindshare capture.

For the consumer electronics industry, while online channels often drive short-term sales, offline presence is crucial for long-term market positioning. With a 50-fold increase in store count over three years, Insta360 is mounting a comprehensive challenge to DJI's decade-long offline dominance. The trajectory of this retail battle could significantly impact the growth trajectories of both companies.

| Insta360 Ramps Up Store Expansion to Address Weaknesses |

The smartphone industry's characteristic of having hundreds of thousands of offline terminals underscores that offline channels are the essential pathway for smart hardware products to transition from niche to mainstream markets. Insta360 is rapidly addressing this former weakness.

As is well known, DJI's offline布局 (layout) has been refined over nearly a decade, establishing the most mature retail network for consumer imaging products in China. Public data reveals that DJI boasts over 700 authorized retail stores and experience stores nationwide, covering core business districts in first-tier cities to digital malls in third- and fourth-tier cities, with channel penetration far exceeding the industry average.

In contrast, Insta360's offline journey commenced much later.

In early 2023, Insta360 had only five domestic specialty stores, relying almost entirely on online channels and third-party retail points for sales. By 2024, the company's online and offline sales were nearly balanced, with online sales accounting for 18.81% through its official website mall and 24.39% through third-party e-commerce platforms, while offline sales relied mainly on distribution, accounting for 44.37%.

By the end of 2025, the number of specialty stores had surged to nearly 300, representing a 50-fold increase in three years, achieving full coverage of all first- and second-tier cities in China. Moreover, the number of stores is likely to continue growing this year.

This aggressive expansion reflects Insta360's strategic decision to gain more market initiative. When asked about the rationale behind doubling down on offline presence, Li Qingchi from Insta360's China sales team stated, "The primary reason for opening larger stores is to respond to user demand. Insta360's user base is expanding, and more users want to experience products in their own cities and expect richer product offerings and better after-sales service from stores. This flagship store is designed to meet those expectations."

Li Ming (pseudonym), a consumer electronics industry expert, told Yidu Pro that Insta360's approach clearly aims to establish brand mindshare through offline experiences, transitioning from a niche hardware brand to a mainstream consumer brand. Moreover, considering that Insta360 is already competing with DJI across multiple product lines, including action cameras, panoramic cameras, and consumer drones, once product line parity is achieved, the focus shifts to catching up in store channel count.

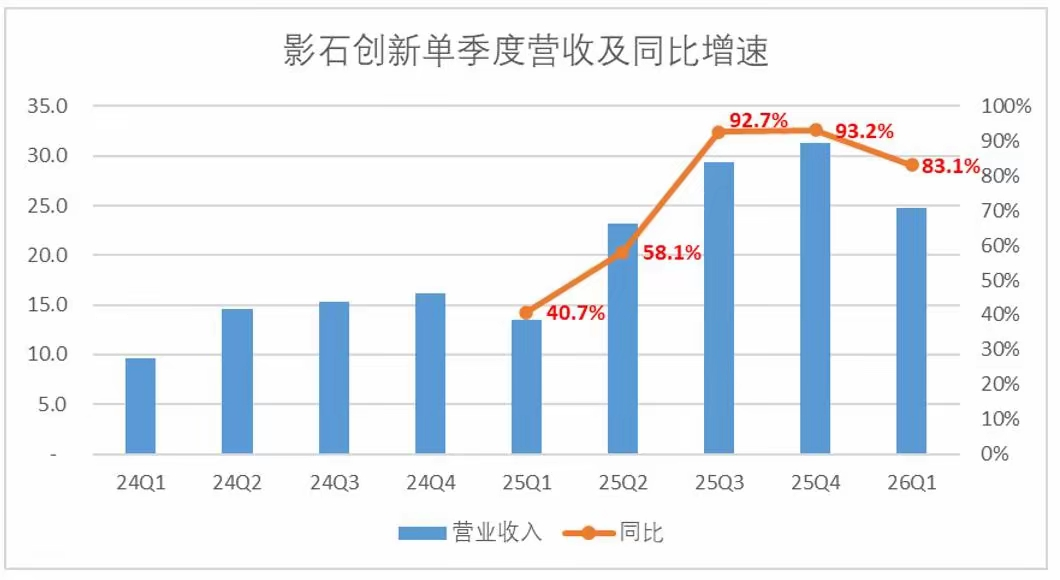

Under this logic, Insta360's revenue growth exceeded 80% in the first quarter. From a long-term perspective, Insta360's fastest-growing segment remains consumer-grade panoramic cameras, with core contributions coming from last year's launches of the Insta360 X5, Insta360 X4 Air, and the Antigravity A1 drone.

Given that Insta360's products, particularly drones encroaching on DJI's core territory, are strong experience-driven categories—where stabilization, grip feel, and operational logic require hands-on perception—expanding offline stores is essential to bridge the "last mile" gap between the brand and mass consumers, providing the necessary support for sustained high growth.

Financial reports corroborate this trend. Last year, Insta360 achieved total operating revenue of 9.858 billion yuan, a year-on-year increase of 76.85%. This growth is closely tied to Insta360's series of measures to address retail shortcomings, particularly its talent and resource investments, which even included poaching personnel directly from DJI.

In the second half of 2025, Insta360 recruited Zhang Bo, DJI's former core sales leader for China. Zhang had served under DJI's Sales Vice President Yuan Dong and had fully participated in DJI's distributor system reform, gaining deep expertise in channel control and dealer operations.

Additionally, Insta360 continues to strengthen its in-store operational capabilities.

Based on public job postings, Yidu Pro observed that Insta360 is recruiting for roles such as Regional Retail BP, Specialty Store Manager, and Retail Trainer, with responsibilities covering the entire chain of dealer network expansion, standardized store operations, staff product training, and regional marketing campaign execution. The goal is to establish a more complete offline retail management system.

Meanwhile, Insta360 is making substantial resource investments in retail. In the first quarter of this year, Insta360's sales expense ratio reached 18.1%, a 60% increase quarter-on-quarter. For the full year of 2025, sales expenses totaled nearly 1.68 billion yuan, a net increase of 850 million yuan compared to the same period in 2024, doubling the previous year's figure.

Taking 2025 as an example, a breakdown of sales expenses shows a 145.5% increase in marketing promotion fees, a 92.7% increase in expenses related to asset depreciation such as rent, and a 91.9% increase in sales staff salaries. Nearly all expense categories grew faster than revenue, indicating significant capital expenditure growth.

Although financial reports do not directly disclose sales expenditure on store expansion, from an industry perspective, industry insiders told Yidu Pro that store expansion involves complex processes such as dealer selection, site selection, store construction, supplier introduction, and hard terminal asset investments, all of which are essential expenditures for brand manufacturers.

That said, catching up in quantity is merely the entry ticket for offline competition. More critical are whether channel strategies are well-suited, store operations are efficient, and the dealer system is healthy.

| Can Store Supply Models Be Directly Replicated from DJI? |

Frankly speaking, Insta360's efforts to enhance store supply have dual implications. On one hand, it needs to learn from DJI's channel experience; on the other, it must explore more flexible policies and precise channel strategies.

Both DJI and Insta360 generally follow provincial agency distribution and authorization models similar to the smartphone industry, even adhering to unified brand standards in store location, décor, and product display.

In the specific context of competition between Insta360 and DJI, DJI's channels are more deeply entrenched and foundational. Sources familiar with DJI's operations note that in some regions, prospective dealers can only source products from existing distributors, as DJI is not adding new dealers. While DJI previously had store expansion targets, site selection required approval, and operationally, experience stores, specialty stores, and comprehensive stores all had performance metrics. If dealers failed to meet targets, replacement was not entirely out of the question.

Overall, DJI's channel and store system exhibit several typical characteristics: coexistence of agency and direct operations, strong control and management over dealers and stores, high channel entry barriers, and a current focus on stock operation (existing operations).

Insta360's current strategy is naturally offensive. After recruiting DJI's channel talent, it may adopt proven systems from its predecessor and could even see scenarios similar to the smartphone industry, where some dealers represent both DJI and Insta360.

However, in reality, top dealers may not necessarily choose to carry both brands, as circumstances vary by region. Moreover, while Insta360's recruited channel talent brings mature management methods, this does not equate to directly transferring DJI's core dealer resources. Some channel partners may view Insta360 as a valuable supplement (complement), but for top-tier dealers, DJI remains the unshakable foundation.

From dealers' perspectives, the respective strengths and weaknesses of the two brands are clear. For example, DJI's advantages include high brand recognition, stable traffic, and strong user willingness to pay; Insta360's advantages lie in its rapid offensive expansion and increasingly diverse product portfolio.

On the retail store front, in some core business districts, the proximity between the two brands' stores has narrowed to the point of direct competition. For instance, in Chengdu's Chunxi Road commercial district, the straight-line distance between Insta360 and DJI authorized stores is just a hundred to two hundred meters, allowing consumers to easily compare experiences between the two. Similar scenarios have emerged in core commercial districts like Shanghai's Huaihai Road and Shenzhen's One Avenue. The once-distinct market boundaries are being broken down by Insta360's rapid expansion.

Last year, an Insta360 store sign in Changsha was reportedly removed due to an "exclusivity agreement." Subsequently, Insta360 founder Liu Jingkang likened it to "just the tip of the iceberg of challenges we face at different levels," highlighting the intense competition between the two brands in the market.

To expand its offline advantages, Insta360 has begun adopting differentiated store strategies.

Earlier, Insta360 opened its largest global city flagship store in Shenzhen's One Avenue. The store features a completely new design, incorporating the brand philosophy of "Think Bold." It includes China's first inverted mirrored micro-model, offering a 360° panoramic reproduction of product usage scenarios like cycling and skiing, and for the first time, fully implements an integrated "sales and service" model.

Consumers can receive after-sales inspections in-store and directly exchange devices for new ones within over ten minutes (a dozen minutes), completing a full closed loop (closed loop) from experience to purchase to after-sales. Insta360 revealed plans to accelerate the rollout of similar stores, making after-sales service as convenient as purchasing products, with a goal of opening 10 more city flagship stores this year.

Insta360 clearly aims to differentiate itself from DJI through unique urban flagship experiences. However, DJI currently holds a significant advantage in total store count. Therefore, the real challenge lies in catching up to DJI's terminal store quantity at the dealer authorization level, not just domestically but globally.

| Global Retail Competition Ultimately Hinges on Efficiency |

For DJI and Insta360, the domestic market represents their foundation, while the global market is the core growth area for the future.

Both companies are typical success stories in overseas expansion: In 2025, Insta360's overseas revenue reached 6.676 billion yuan, accounting for 69.03% of total revenue, with products sold in hundreds of countries and regions worldwide. DJI dominates the global consumer drone market, holding over 70% market share. Although DJI has not disclosed detailed 2025 revenue figures or overseas market income, industry estimates suggest that overseas revenue accounts for approximately 80% of its total revenue.

Additionally, the Luna Ultra represents Insta360's flagship entry into the handheld gimbal camera market, long dominated by DJI's Pocket series, which has shipped 10 million units. In 2025, global shipments of handheld smart cameras reached 16.65 million units, up 83% year-on-year, with DJI leading at 62.4% market share and Insta360 second at 20.4%. By launching Luna directly into DJI's core profit zone, Insta360 is likely to intensify competition and conflicts between their retail stores in the future.

Similar to the early days of Chinese smartphone brands going global, online channels can quickly open markets but only reach core tech-savvy users. To truly penetrate mass markets, establishing localized retail networks is essential.

Currently, Insta360's sales network covers over 10,000 retail stores worldwide, with deep partnerships with Apple Store retail locations, Best Buy, B&H, and Suning. DJI's global retail network was established earlier, covering more countries and regions, with mature agency systems and branded stores in major Western markets, giving it far deeper offline channel penetration than Insta360.

However, when it comes to offline competition on a global scale, operational efficiency is the ultimate determinant of success. DJI, after a decade of channel development, has established a sophisticated system that synergizes its supply chain and distribution channels. This has positioned the company at the forefront of the industry in terms of single-store operational efficiency and inventory turnover speed. On the other hand, Insta360, which is still in its expansionary phase, continues to invest heavily in channel development, and the impact of its scaling efforts is yet to be fully assessed.

As the global market competition looms, one of the primary challenges for Insta360 will be to transition from rapid store expansion to refined operations. This entails establishing stable dealer systems in more mature markets and converting the increase in store numbers into tangible sales growth and enhanced brand recognition. For DJI, the focus will be on fortifying its channel defenses in mature markets while maintaining its competitive edge in emerging ones, leveraging its efficiency advantages to counterbalance the speed advantages of its competitors.

The channel and store competition between DJI and Insta360 is set to continue. However, one thing remains clear: the company that can effectively translate its technological edge into retail prowess and transform its product capabilities into brand influence will emerge as the enduring victor.

Moreover, their retail skirmishes on street corners are only expected to escalate.

Image sourced from the internet. Rights reserved for the original author.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’