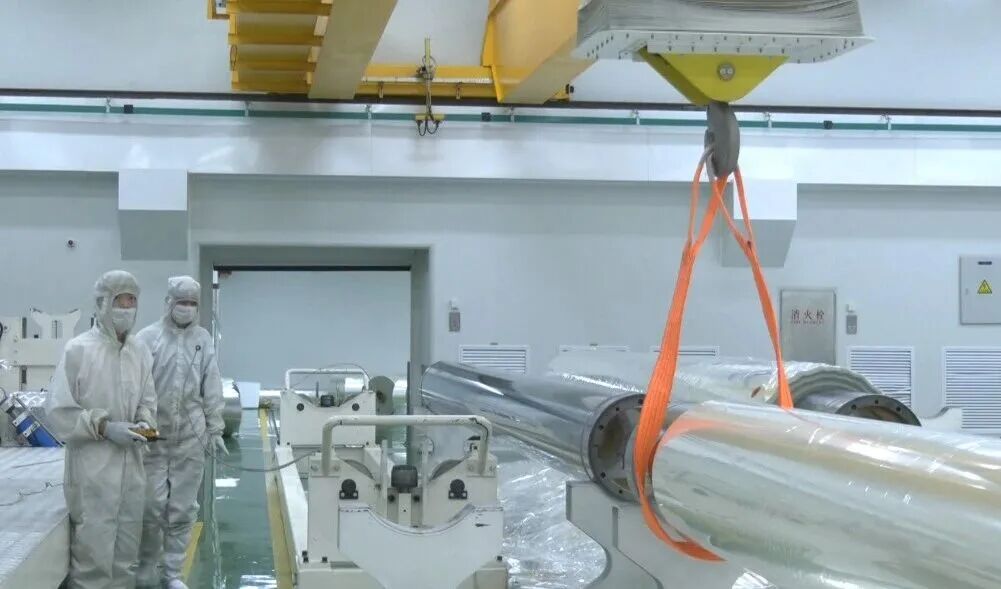

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

06/25 2026

06/25 2026

412

412

Recently, Jiangsu Dongcai New Material Co., Ltd. (hereinafter referred to as 'Jiangsu Dongcai') announced that it recorded RMB 920 million in invoiced revenue for the first quarter (Q1) of 2026, marking a 47% year-on-year increase. The company currently boasts an annual production capacity of 200,000 tons of optical-grade base films, with orders already secured extending into the latter half of the year.

What enables this national-level specialized, sophisticated, and innovative 'Little Giant' enterprise, headquartered in Haian, Jiangsu, to secure such a substantial volume of orders? What are the underlying background and business advantages of Jiangsu Dongcai?

A more comprehensive perspective emerges from the first-quarter report data released by Dongcai Technology, the parent company of Jiangsu Dongcai. In Q1 2026, the company achieved revenue of RMB 1.444 billion, a 27.24% year-on-year increase; net profit attributable to shareholders reached RMB 187 million, a significant 103.35% year-on-year surge; and net profit excluding non-recurring items amounted to RMB 116 million, a 41.74% year-on-year rise.

Within these figures, sales revenue from optical film materials reached RMB 353 million, a 17.63% year-on-year increase; sales revenue from electronic materials soared to RMB 537 million, a substantial 71.46% year-on-year increase, with high-speed electronic resins contributing a 131.42% year-on-year jump, generating RMB 258 million in revenue. This data set underscores the deep interplay between two key industrial sectors.

One of the fundamental drivers behind Jiangsu Dongcai's order growth is the ongoing deepening of domestic substitution. In niche areas such as polarizer release base films, thin MLCC release base films, and OCA optical adhesive base films, Jiangsu Dongcai has successfully broken the long-standing monopolies held by Japanese and Korean companies. Its OCA base films now command approximately 80% of the national market share, while its dominance in the optical-grade base films and electronic resins sectors remains unchallenged domestically.

Another, even more pronounced, growth trajectory stems from the incremental demand generated by AI computing infrastructure. The demand for high-end electronic resins and optical base films in AI servers is experiencing rapid escalation. According to estimates by Zhou You, Deputy General Manager of Dongcai Technology, the global market for high-speed resins used in servers is projected to reach approximately RMB 2 billion in 2025 and surge to between RMB 5 billion and RMB 8 billion by 2026. It is within this dynamic sector that Jiangsu Dongcai's electronic materials division achieved a 71.46% quarterly revenue growth.

The company's independently developed electronic-grade resin materials, including bismaleimide resin, active ester resin, hydrocarbon resin, and polyphenylene ether resin, have obtained certifications from leading domestic and international copper-clad laminate manufacturers such as Taiguang and Shengyi. These materials are now integrated into mainstream server systems from NVIDIA, Huawei, Apple, and Intel.

Throughout 2025, high-speed electronic materials generated sales revenue of RMB 591 million, a 125.07% year-on-year increase; entering 2026, the first quarter alone saw revenue reach RMB 258 million, with the growth rate further accelerating to 131.42%.

Accurate capacity planning and systematic capacity release have effectively translated market demand into tangible revenue growth. According to the company's 2025 annual report, the '25,000-ton-per-year optical-grade polyester base film project for polarizers' commenced production in January 2025, while the '20,000-ton-per-year technological transformation project for optical-grade polyester base films for ultra-thin MLCCs' began operations in December 2025.

These projects were duly transferred to fixed assets and established stable production capacities. Combined with the existing 200,000-ton-scale optical-grade base film production capacity, Jiangsu Dongcai now enjoys significant advantages in terms of large-scale supply capability.

Projects currently under construction also warrant attention. The '20,000-ton-per-year electronic materials project for high-speed communication substrates' at the Meishan base is expected to commence trial production by June 30, 2026, adding 3,500 tons of hydrocarbon resin production capacity. Currently, the company has achieved stable mass supply of M9-grade hydrocarbon resins, while M10-grade resins are undergoing active verification with key domestic and international customers.

The ecological benefits of the industrial cluster provide Jiangsu Dongcai with comprehensive support, spanning technological innovation to market validation. Haian has attracted 88 film industry enterprises, including 20 with revenue exceeding RMB 100 million and 5 national specialized, sophisticated, and innovative 'Little Giant' enterprises, forming the sole RMB 10 billion-scale polyester release film cluster in the Yangtze River Delta region.

From upstream petrochemical raw materials, chips, and base films to midstream coating and release processes, functional composites, and downstream applications in novel displays, new energy, and 5G modules, Haian has established a complete, closed-loop ecosystem. The collaborative model of 'leading enterprises + research institutes + universities' has enabled Haian to continually achieve breakthroughs in import substitution in areas such as polarizer release base films, thin MLCC release films, and OCA optical adhesive base films.

Jiangsu Dongcai's 47% growth is fundamentally a tale of strategic foresight. By positioning itself at the convergence of the enduring trend of domestic substitution and the burgeoning wave of AI computing power, the surge in orders represents a natural outcome rather than a mere coincidence when industrial trends align with capacity expansion. The company's management remains optimistic about the market outlook—orders are secured through to the second half of the year, the proportion of high-end products continues to rise, and overseas markets are expanding steadily.

Currently, 80% of the market for high-temperature-resistant, high-insulation release films still relies on imports, indicating that the battle for domestic substitution is far from over. In the high-speed resin sector, competitors are also ramping up their efforts. For Jiangsu Dongcai, the true challenge lies not in whether it can seize the current window of opportunity but in whether it can construct a sufficiently robust technological moat to sustain its leadership beyond it.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’