9 Billion Yuan Pours In: Capital Doubles Down on AI Glasses and the 'Shovel Sellers' | Mid-2026 Special Report

07/03 2026

07/03 2026

491

491

Capital Flows Reveal Industry Shifts

By VR Gyroscope, Ran Qixing

Changes in capital flow often expose shifts in industrial focus earlier than market hype.

As the third quarter of 2026 begins, VR Gyroscope reviews the XR industry's first half as usual. This report focuses on global VR/AR, AI glasses, and related supply chain investments, aiming to clarify capital priorities through financing volume, amounts, and project distributions.

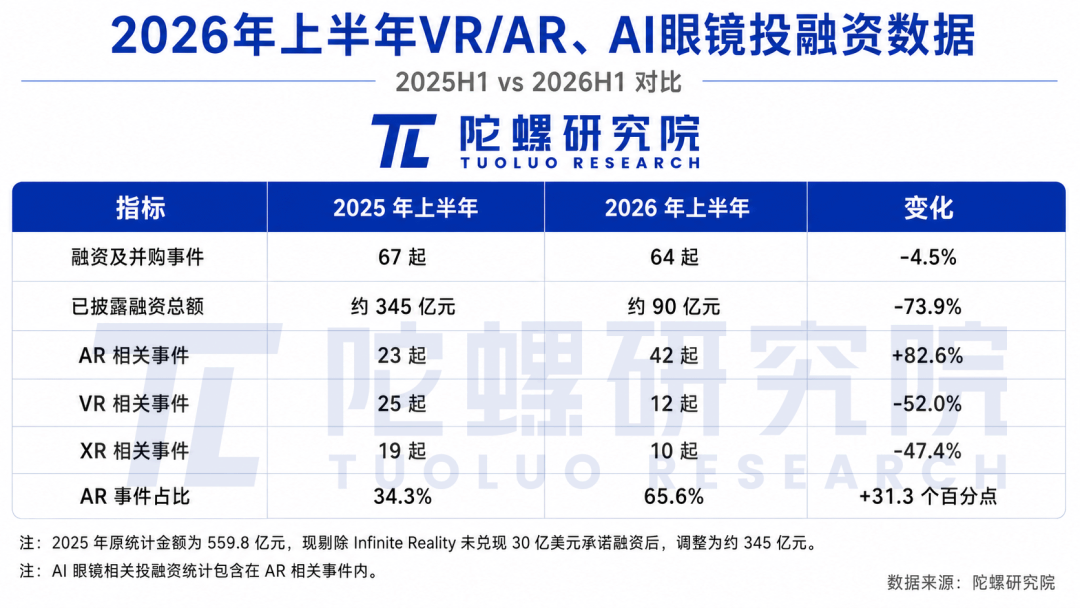

According to Gyroscope Research Institute data, the first half of 2026 saw 64 global financing, M&A, and strategic investment events across VR/AR, AI glasses, and related supply chains, with disclosed amounts totaling approximately 9 billion yuan. Some project amounts remain undisclosed. Event volume remained nearly flat compared to 67 events in H1 2025.

Financing amounts declined in H1 2026 versus H1 2025, primarily due to two major overseas investments and M&A deals in 2025. Notably, Infinite Reality's claimed $3 billion financing never materialized—confirmed by late 2025 as funds failed to arrive, with the company acknowledging unfulfilled commitments to employees. Excluding this, the industry's disclosed H1 2025 financing adjusted from 55.98 billion yuan to approximately 34.5 billion yuan.

Structurally, AR-related events dominated with 42 deals (65.6% share), while VR-related events shrank to 12, a significant decline year-on-year. AI glasses brands, AR waveguide displays, and Micro-LED microdisplays emerged as the most active investment areas. Few new VR/MR brand entrants appeared, with related financing concentrated overseas.

01 42 Financing Rounds Flow to AR, Capital Concentrates on Leading AI Glasses Brands

The explosive growth of AI glasses sales in 2025 set the stage for continued capital inflows in H1 2026.

Notably, Thunderbird Innovation secured over 1 billion yuan in Series C+ funding early in the year, one of China's largest AI glasses deals. Investors included China Mobile's Chain Leader Fund and CITIC-affiliated capital, signaling that AI glasses are now seen not just as a consumer electronics trend but as a hardware gateway capable of driving telecommunications, device, and ecosystem synergies.

Around the same time, INMO completed its Series C1 round with investors including Chengdu Science and Technology Innovation Investment, Nanshan Strategic Emerging Industry Investment, and Pufeng Capital. Beyond traditional VCs, local industrial funds are becoming key players in AI glasses financing, focusing not only on brand growth but also on terminal manufacturing, optical supply chains, and regional smart hardware clusters.

Policy signals are also strengthening. In June 2026, eight ministries including the Ministry of Commerce issued the "Implementation Opinions on Accelerating the Development of 'AI + Consumption'," promoting R&D and commercialization of AI glasses and their integration with AR/VR/MR technologies. AI glasses have transitioned from a venture capital darling to a focus of consumer policy and local industrial strategies.

XREAL further marked an industry milestone by filing for a Hong Kong IPO after securing new funding in early 2026. When a brand enterprise in a sector pursues an IPO, it typically signals a critical transition from rapid growth to capitalization and standardization. While XREAL's successful listing remains uncertain, its prospectus revealed sales, revenue, losses, and cash flow data, offering the first comprehensive financial view of a leading AR glasses company.

Rokid attracted multiple strategic investors from listed supply chain firms in H1 2026, including Conant Optical, Highpower Technology, Awinic Electronics, and Fibocom. Within five months, Rokid's registered capital surged from 2.875 million yuan to 35.708 million yuan. Unlike pure financial investments, these shareholders cover optics, batteries, and communication modules, deepening Rokid's ties with upstream suppliers.

VITURE announced $100 million in Series B+ funding in H1 2026, bringing its six-month total to over $200 million. As a North America-focused XR glasses maker, VITURE is expanding into China and enterprise markets. In May 2026, it launched the consumer-grade VITURE Beast in China, followed by the industrial-grade VITURE Helix at AWE in June. Shifting from consumer AV displays to industrial AI terminals, VITURE aims to broaden its product scope to meet post-funding growth expectations.

Tribute to the Unknown stood out as one of the few AI glasses makers betting on vertical scenarios in H1 2026. In February, the company secured over 100 million yuan in Pre-A funding from investors including Skyworth Investment, Boyu Capital, Lenovo Capital, and Guangfa Qianhe. Since 2025, it has pivoted from general-purpose AI+AR glasses to AI sports glasses, launching BleeqUp. The product now operates in over 20 countries and thousands of stores. Sports scenarios offer clearer usage frequency, functional boundaries, and target demographics, providing a differentiated path for new brands.

Another vertical-focused player, Lightin Technology, completed nearly 100 million yuan in Pre-B funding in March 2026. Beyond AR swimming goggles, it began collaborating with traditional eyewear makers to develop outdoor AI glasses. Both firms aim to bypass direct competition in general-purpose AI glasses by building product moats in sports and outdoor segments.

02 Waveguide Displays and Micro-LEDs Attract Capital, Supply Chain Becomes Secondary Focus

Parallel to AI glasses brands, upstream supply chains are heating up.

H1 2026 saw a surge in financing for XR optics, waveguide displays, and Micro-LED microdisplays, with some projects reaching billion-yuan scales. Unlike single-terminal brands, upstream firms can serve multiple clients and scale orders with terminal shipments.

Seeya Technology's 2025 IPO also provided clear valuation and exit benchmarks for optical and microdisplay companies. At a stage where terminal forms remain fluid, firms supplying cross-brand, cross-product core components are becoming capital's second major focus.

In AR optics, Goertek Optics stood out. In June 2026, Goertek and Ningbo Sunny Optics injected 500 million yuan each into Goertek Optics, totaling 1 billion yuan. Goertek Optics now offers one of China's broadest XR optical solution portfolios, covering diffraction waveguide displays with glass, resin, and silicon carbide substrates, as well as display technologies like mono-green, full-color Micro-LED, and LCoS for AR, and Micro-OLED with Pancake optics for VR/MR.

ZhiGe Technology secured billion-yuan-level funding in H1 2026. CEO Meng Xiangfeng told VR Gyroscope, "Our sales ceiling this year depends on production capacity, so we're accelerating expansion." Among leading waveguide suppliers, capacity constraints are now critical for order fulfillment. As Alibaba Qianwen and other tech giants enter AI glasses, supply chain anxieties are shifting toward mass-production capabilities—provided the technology remains competitive.

Tianyancha data shows Guangna Siwei secured new funding in June 2026 from investors including Guangzhou Industrial Investment Group, Guangzhou Emerging Industries Fund, and Chengdu Science and Technology Innovation Investment Group. As an AR optical supplier, Guangna Siwei supplies Even G1, Coray Air2, and iFlytek AI glasses.

Other optical players like Kunyou Optoelectronics, Guangzhou Semiconductor, Lipai Optical, and Aotizan Optical also secured new funding in H1 2026. Diffraction waveguides, geometric waveguides, and volume holographic waveguides all attracted capital.

The microdisplay sector remained active. Saphlux completed 300 million yuan in Series C funding in H1 2026 to advance full-color Micro-LED mass production. Qiushui Semiconductor raised nearly 200 million yuan across multiple rounds for an 8-inch hybrid bonding production line. Sitantech secured nearly 100 million yuan to commercialize Micro-LED displays in AR glasses. Mojo Vision, which pivoted from AR contact lenses to Micro-LED displays, raised $17.5 million in strategic funding—its second external investment after a $75 million round in 2025.

JBD, though silent on new funding in H1 2026, remains a key player. VR Gyroscope noted its official WeChat account renamed from "Xianyao Display" to "Xianyao Holdings" in recent months. Tianyancha shows JBD transformed from a "limited liability company (Hong Kong-Macau-Taiwan investment, non-solely funded)" to a "joint-stock company (Hong Kong-Macau-Taiwan investment, unlisted)" in December 2025. Joint-stock restructuring often precedes corporate governance standardization and capital operations. With sustained AI glasses demand, JBD may become China's second XR microdisplay IPO after Seeya Technology.

From a capital perspective, upstream firms offer clearer investment logic. Device brands face uncertainties in product definition, channel building, inventory management, and market competition. Core component and optical firms serve multiple clients, diversify revenue streams, and can extend technologies to automotive, projection, and other display categories.

However, upstream is not low-risk. Different technical routes entail varying costs, yields, mass-production challenges, and application boundaries. With terminal forms still evolving, supply chain firms must navigate route selection, capacity investment, and customer concentration issues—competition is no less intense than at the brand level.

03 VR Financing Shifts to Application Layers, New Hardware Brands Scarce

Shifting focus from AI glasses to VR/MR, financing hasn't vanished but has clearly moved away from consumer hardware brands toward application-layer projects with clear monetization paths.

H1 2026 saw 12 VR-related financing events, concentrated overseas. Funds flowed to medical, training, education, immersive content, virtual avatars, and motion peripheral projects. For example, ORamaVR, a computational medical extended reality solutions provider, secured $4.5 million in seed funding in February.

At the device level, new consumer VR/MR headset startups struggle to attract financing. After years of hype cycles and market corrections, user education, content ecosystems, supply chains, and channels require sustained investment.

For startups, headsets remain capital-intensive, long-return-cycle hardware categories difficult to differentiate through single features. In March 2026, MR hardware maker Lynx's manufacturer SL PROCESS entered judicial liquidation, highlighting the operational pressures on independent hardware startups.

Currently, the brands that can still remain in the VR/MR sector can be roughly divided into two categories. One type is those backed by major companies, where VR/MR is just one of their product lines, such as Meta and PICO. These companies possess stronger cash flow, supply chain resources, and content ecosystem capabilities, enabling them to endure longer investment cycles and wait for the next product milestone.

The MR industry line of Wanchu Mengxiang follows a similar pattern. As a group with mature business segments like Wangyu Internet Cafe, its MR product line is not the sole source of revenue for the company. While other businesses continue to contribute revenue, the group can also provide more stable support for the long-term R&D, channel construction, and market cultivation of MR hardware, enabling it to withstand longer product investment cycles.

The other type consists of companies that have already formed their own business closures. For instance, companies like DPVR and Pimax, although lacking the capital strength of super platforms, can at least maintain a relatively healthy business cycle by relying on niche markets, overseas sales, enterprise clients, offline scenarios, or hardware reputation. These companies may not be making rapid progress, but they have a realistic foundation to remain in the game.

It is noteworthy that since 2026, manufacturers such as PICO, DPVR, and Pimax have been actively exploring solutions related to embodied intelligence. The spatial positioning, motion tracking, environmental perception, and remote interaction capabilities accumulated by VR/MR companies over the long term are being reintegrated into the chains of robot training, remote operation, and spatial data collection.

The development of industries often follows cycles. VR/MR, which is temporarily placed on the back burner by capital today, may not return in its original form as a 'consumer-grade headset' in the future. Instead, it could re-enter the capital spotlight as infrastructure for embodied intelligence, tools for robot training, and entry points for spatial data.

04 In Conclusion

In the AI era, glasses naturally occupy the first-person perspective, continuously capturing information about what users see, hear, and the environment they are in. Therefore, they are being pushed to the forefront of a new round of competition in smart hardware. Capital's attention to AI glasses is also rapidly spreading to the optical, display, chip, lens, and manufacturing ends, accelerating the entire AR industry chain.

Of course, this round of changes does not mean that the VR/MR industry has stagnated. Existing manufacturers are extending their capabilities to more defined commercial scenarios. Large-scale entertainment, remote robot operation, and embodied intelligence data collection are becoming new business pillars. Relying on domestic and international markets, offline projects, and industry orders, some manufacturers have already established sustainable business closures.

It can be observed that in the first half of 2026, AI glasses are opening up incremental markets, while VR/MR continues to seek sustainable revenue in deeper scenarios. The two paths are diverging but may also converge again in the next technological cycle.

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan

-

A Single-Day 40% Plunge! AI-Themed New Listings: The Cruelest 'Slashes' for Retail Investors in Hong Kong Stocks

-

China’s Fourth-Largest Token Factory Accelerates IPO Plans Amid -24% Gross Margin and AI Infrastructure Reduced to a "Traffic Business"

-

![]()

Humanoid Robots Take Center Stage at Electronica Munich: Auto Chip Titans Embrace Robotics Revolution

-

![]()

Purchasing the Casket and Sending Back the Pearl: Meta's Foray into Computing Power Business

-

![]()

AI Computing Power is Pushing Global Power Grids to Their Limits