Back to square one, where is the redemption for Chinese assets?

11/26 2024

11/26 2024

688

688

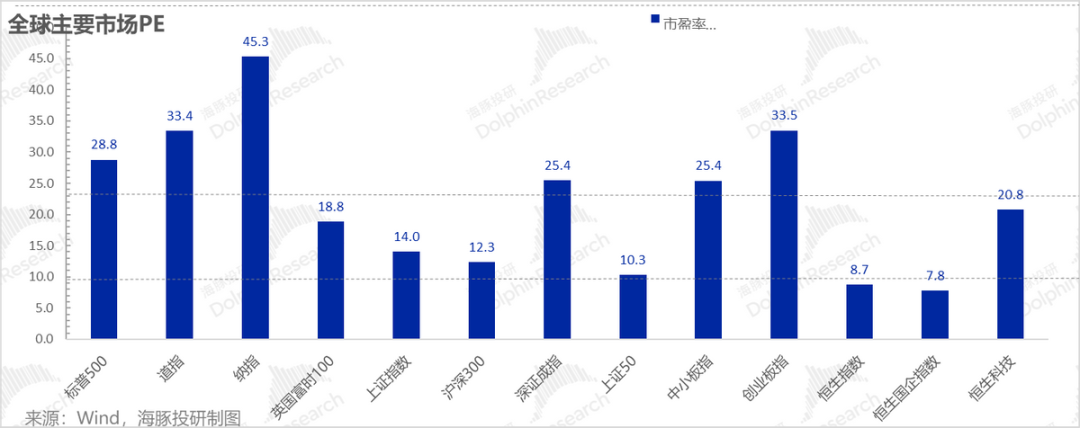

By the end of last week, the third-quarter earnings season for China and the United States had largely come to a close. This earnings cycle was particularly interesting. Starting from National Day, Chinese concept stocks rapidly evolved from underlying currents to a surge of enthusiasm. However, as the earnings season for this quarter ended and the enthusiasm waned, the market seemed to have slipped back to square one again, with the market value of Chinese concept assets falling back to around 10X PE.

I. Chinese Concept Stocks: Growth Has Become Absolutely Scarce

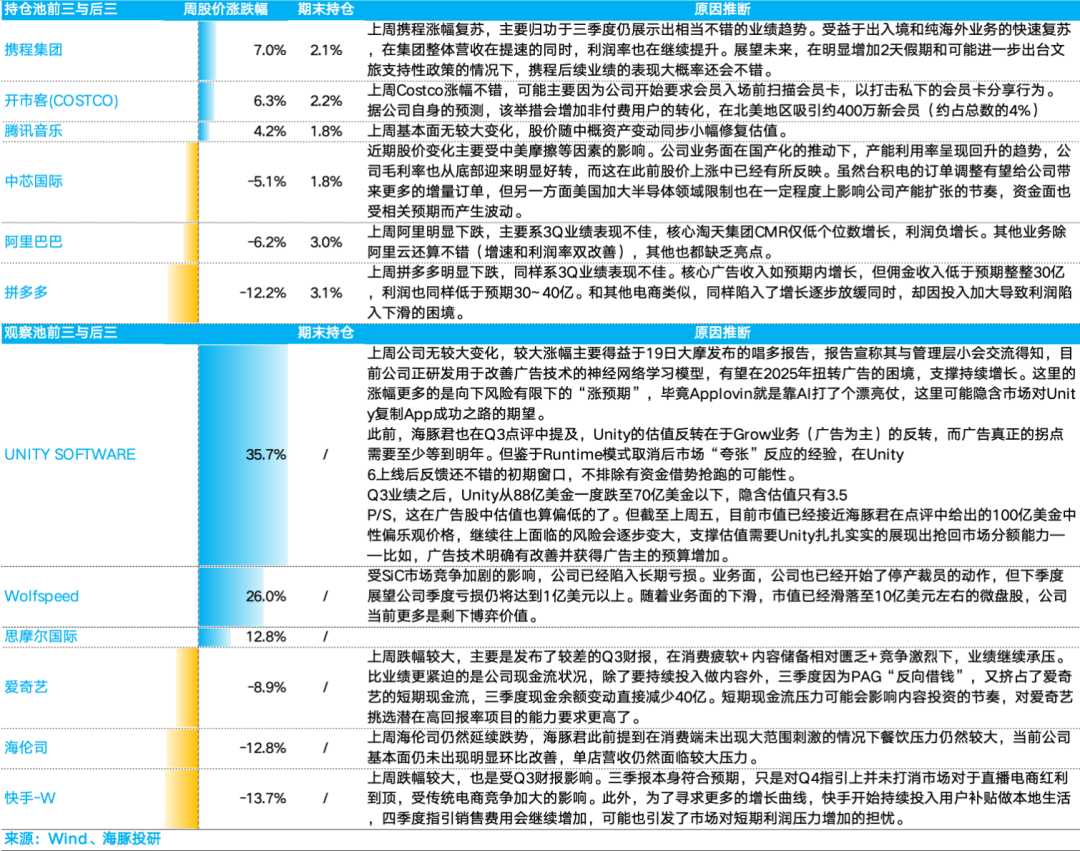

Among the Chinese assets covered by Dolphin Research, whenever there is no "overseas" presence (no overseas business), growth in the third quarter has become a scarce asset that requires a telescope to find:

a. Among advertising stocks, Baidu's advertising revenue fell by 5% year-on-year in the third quarter, and may fall by 10% in the fourth quarter; Focus Media's advertising revenue increased by 4.5% year-on-year; Weibo's advertising revenue increased by 5% year-on-year; there are few opportunities for growth exceeding 10%+ - Tencent's advertising revenue increased by 17%, Bilibili's advertising revenue increased by 28% year-on-year, and Kuaishou's advertising revenue increased by 20% year-on-year.

b. Among e-commerce stocks: Alibaba's e-commerce GMV is estimated to have increased by 2-3% year-on-year; JD.com's self-operated retail revenue increased by 5%; Kuaishou's GMV increased by 15% year-on-year; Pinduoduo's GMV should have increased by 20%+, and its advertising revenue increased by 20%+.

c. Among product stocks: Tencent's domestic games increased by 14% year-on-year during a strong product cycle; NetEase Games barely achieved zero growth; others, such as vertical niche leader Tencent Music, saw a 20%+ increase in subscription revenue.

After the earnings season, a clear fact emerged: Internet companies without a second growth curve, without overseas markets, and without establishing a solid business barrier for their original businesses have become cyclical stocks that are entirely dependent on external factors. Just like live-streaming stocks that stopped growing years ago, Internet stocks without growth potential are now valued closer to 10x PE.

Even some Internet economy stocks that can still achieve 15-20% growth, such as Pinduoduo and Kuaishou, are valued very stingily as long as the market does not see obvious business barriers.

II. What to Do When "Weather Conditions" Are Unfavorable During a Cyclical Business?

Having gradually lost their own Alpha and become cyclical stocks dependent on external factors, the "weather conditions" for individual stocks have become exceptionally important. The valuation of these companies is heavily influenced by changes in the economic cycle, in addition to their own struggles.

Therefore, in the current Internet economy, macro policy trends are just as important as individual stock efforts. Looking back at policy signals since the September 24 meeting:

a. It is progress that the policy attitude has shifted from initially denying deflation to now mentioning the goal of "reflation"; b. A debt swap plan of 10 trillion yuan has also been announced on the policy front; however, after a period of policy anticipation and implementation, looking back: a. The policy remains relatively restrained (strictly controlling new local debt); b. Stimulus on the demand side, apart from equipment replacements and sporadic consumption vouchers, has been slow in other areas; c. With Trump in power, external demand pressure may increase next year; d. With Trump in power, the duration of high-interest US dollar rates may extend, which may indirectly suppress domestic monetary and exchange rate policy space.

Moreover, companies like Baidu and KE Holdings, which concluded the Chinese concept earnings season, practically demonstrated to the market what the performance evolution path of individual stocks might look like if the cycle continues to remain at the bottom. Therefore, the corresponding result is that although Chinese concept stocks are indeed undervalued, an undervaluation without a fundamental inflection point is not a reason to buy.

In the absence of a substantial macroeconomic upturn, the current investment strategy for Chinese concept stocks has effectively become: a. Identifying relatively reliable companies from the underperformers based on financial reports, looking for companies with relatively solid ecosystem positions and undamaged competitive landscapes, such as Tencent Music; or product-cycle companies with essential R&D capabilities, such as NetEase, preferably with generous dividends, or companies with upward product cycles, such as Bilibili and Tencent.

Then, during the macro policy game's downturn, wait for these relatively high-quality companies to reach relatively low positions and for the next round of macro policy expectations and implementation games to drive stock price recoveries. Meanwhile, select a few dividend-paying value stocks, such as China Mobile, to smooth out strategy fluctuations.

For the rest of the time, it is better to focus more on U.S. stocks and assets with greater overseas expansion opportunities.

III. Portfolio Adjustment and Returns

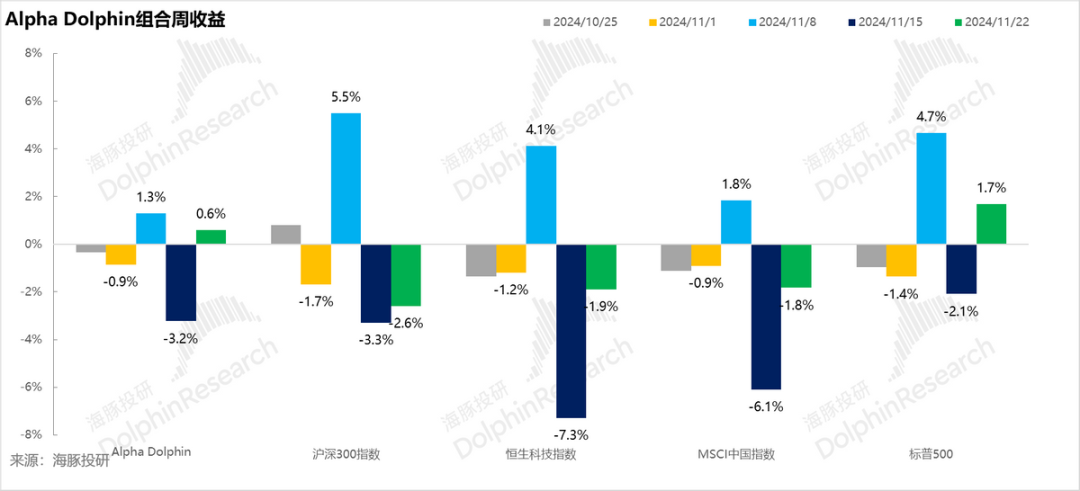

There was no portfolio adjustment last week. The Alpha Dolphin portfolio's floating return was 0.6% last week, outperforming the Hang Seng TECH Index (-1.9%), MSCI China (-1.8%), and CSI 300 (-2.6%) but underperforming the S&P 500 (+1.7%).

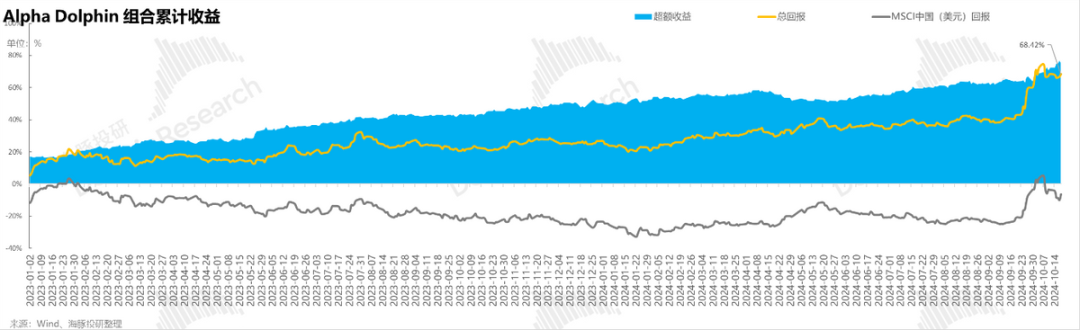

From the start of portfolio testing (March 25, 2022) to last weekend, the portfolio's absolute return was 64%, with an excess return of 78% compared to MSCI China. From an asset net worth perspective, Dolphin Research's initial virtual assets of $100 million exceeded $166 million as of last weekend.

IV. Individual Stock Profit and Loss Contributions

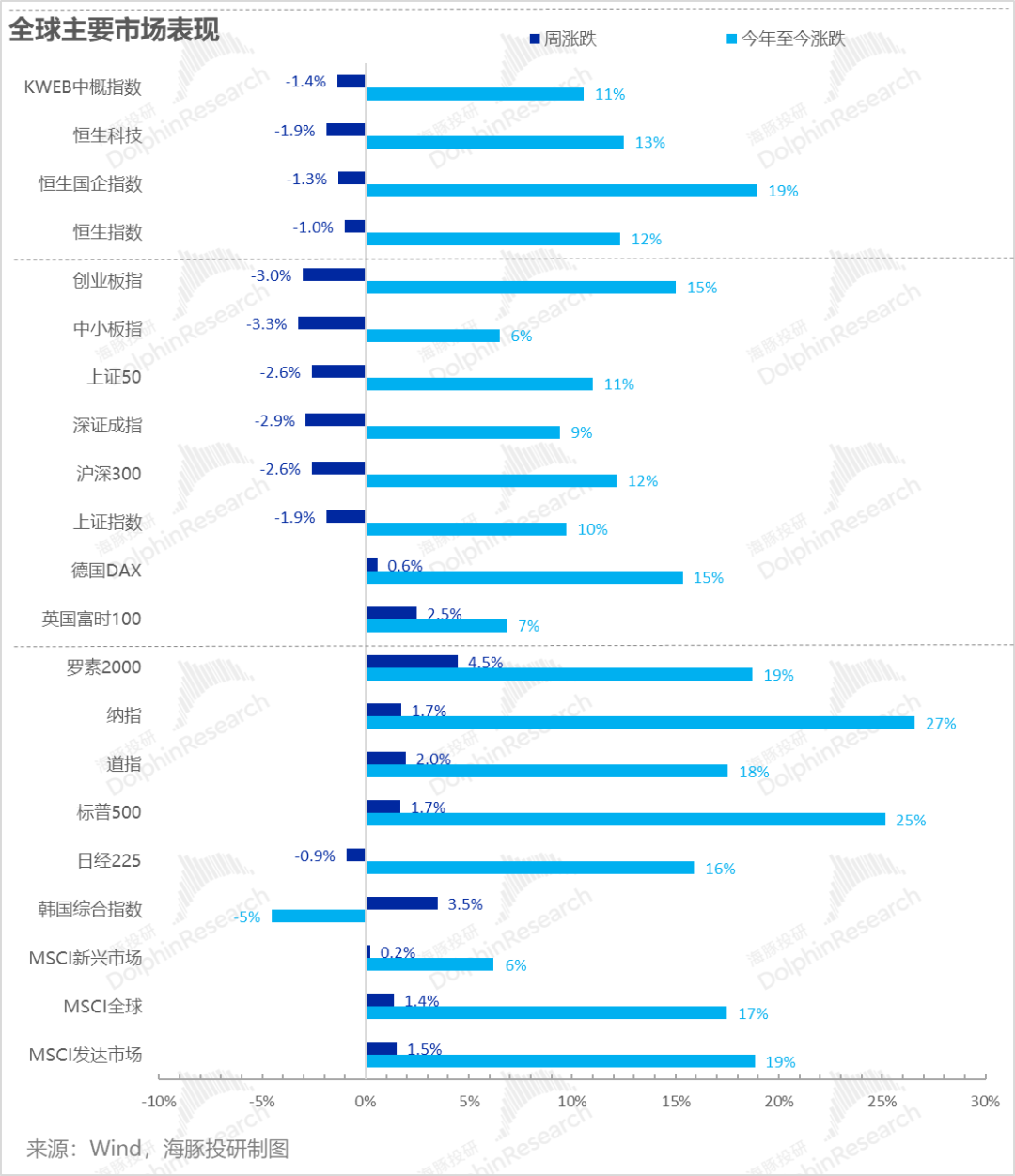

Last week, Chinese concept stocks were generally in a state of fluctuating correction, while U.S. stocks were generally on an upward trajectory, with the Russell 2000 index of small-cap stocks performing particularly strongly.

Among Dolphin Research's holdings, top-heavy stocks such as TSMC and Nongfu Spring performed relatively stably, and Ctrip also performed well with the release of its earnings. The main underperformers were Alibaba and Pinduoduo, both due to weak earnings. A detailed analysis is as follows:

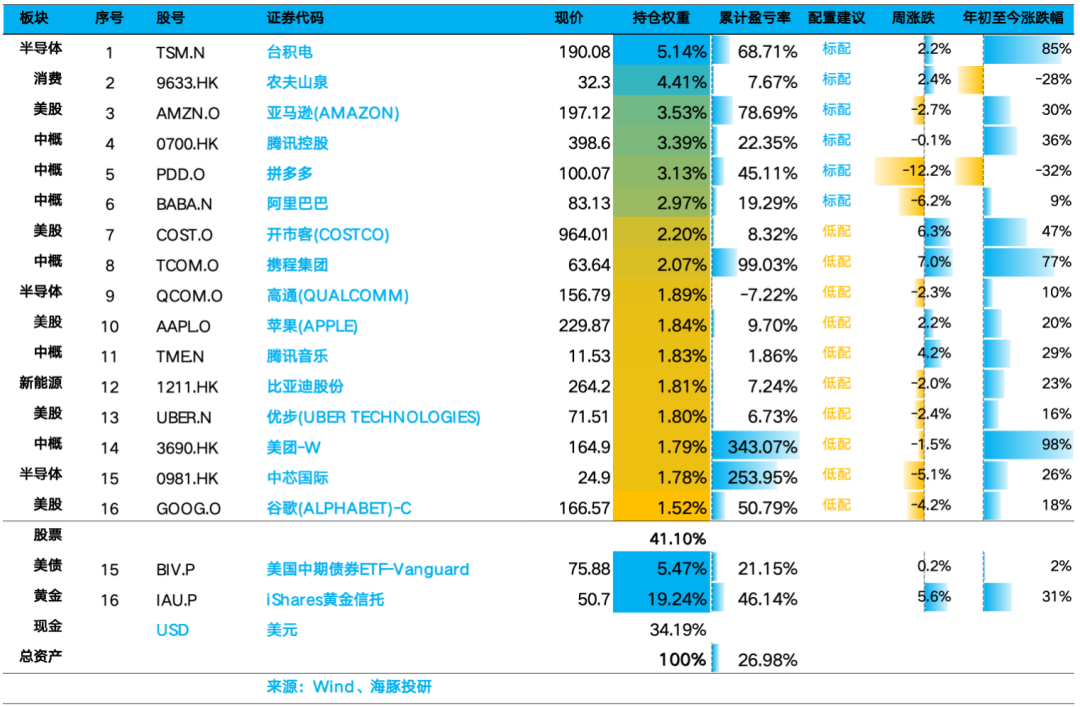

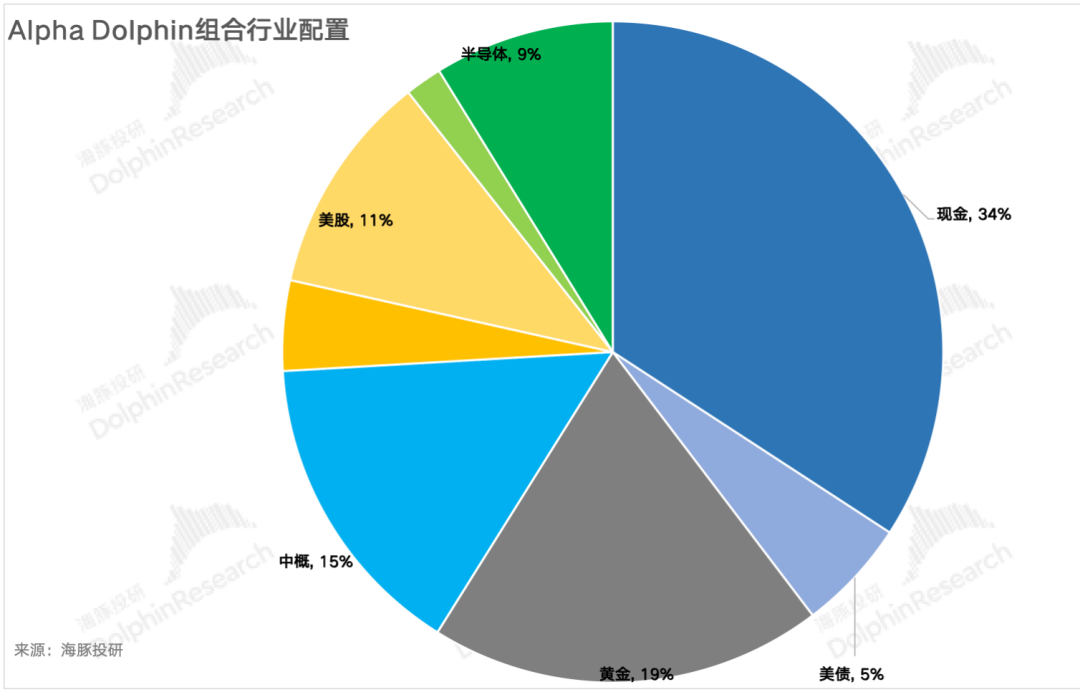

V. Asset Portfolio Distribution

The Alpha Dolphin virtual portfolio holds a total of 14 stocks and equity ETFs, with 3 standard configurations and 8 equity assets under-allocated. The rest are distributed in gold, US Treasuries, and US dollar cash. As of last weekend, the Alpha Dolphin asset allocation and equity asset position weights were as follows:

VI. Key Events This Week

This week, the Chinese concept earnings season has basically ended, with Meituan being the only major company left to report. Additionally, hotel leader Huazhu will also release its earnings, mainly to observe the decline in the domestic hotel and travel industry in the fourth quarter.

- END -

// Reprint Authorization

This is an original article by Dolphin Investment Research. For reprinting, please obtain authorization.

-

![]()

Legal Disputes, Share Unlock, and Pricing Controversies Converge: Insta360 Reaches a Pivotal Juncture

-

![]()

Litigation, Share Unlock, and Pricing Disputes Converge: Insta360 Faces a Pivotal Moment

-

![]()

Wenxin Integration by Baidu and Doubao’s Subscription Model: The Strategic Showdown Between Baidu and ByteDance

-

![]()

Why Are Automakers Flocking to Embodied AI?

-

![]()

The Illusion of Recovery in China's Commercial Rockets: Pre-Designed Endgame Capabilities

-

![]()

Will Choosing the Wrong Technical Route Between World Model and VLA Lead to Elimination?

-

Meituan, with RMB 390 Billion Valuation, Ensnared in the 'Silence Spiral' of Low Stock Prices

-

![]()

iPhone 18 Introduces an Unusual "9GB" Memory Spec—Does Apple Truly Deserve the Title of "Precision Marketing Master"?