From Commission Wars to Efficiency Wars: How Domestic OTA Platforms Leverage the Global Market?

02/28 2025

02/28 2025

672

672

Recently, major global OTA platforms have successively released their latest financial reports for the full year 2024. Among them, Expedia, Booking, Airbnb, and other international OTA giants continue to maintain high profit margins. Meanwhile, domestic OTA enterprises such as Ctrip are showing robust growth while exhibiting lower commission rates and higher operational efficiency.

Industry report data shows that the commission rates of international OTA platforms like Expedia, Booking, and Airbnb typically range between 12%-15%. In contrast, the comprehensive commission rate of domestic OTA platforms like Ctrip is 4.4%, roughly one-third of that of international OTA giants, while their GMV performance remains on par with international giants. This means that Ctrip provides partners with business of the same scale with only one-third of the commission charged by Booking, implying that partners can achieve the same level of business with just one-third of the cost.

OTA platforms serve as third-party service providers matching supply and demand in the tourism industry, with their primary revenue source being commissions charged for facilitating transactions between merchants and customers. Therefore, the commission rate becomes a crucial indicator measuring the operational efficiency of OTA platforms and affecting the relationship between platforms and merchants. It is also a key point in the 'game of interests' among platforms, merchants, and users.

For merchants, commissions represent the cost of the traffic, technical support, and user reach services provided by the platform. For consumers, the level of commission rates also indirectly affects the final prices of flights and accommodations, as well as the overall travel cost.

Compared to international OTA giants, there is a notable difference in commission rates between domestic and foreign OTA platforms.

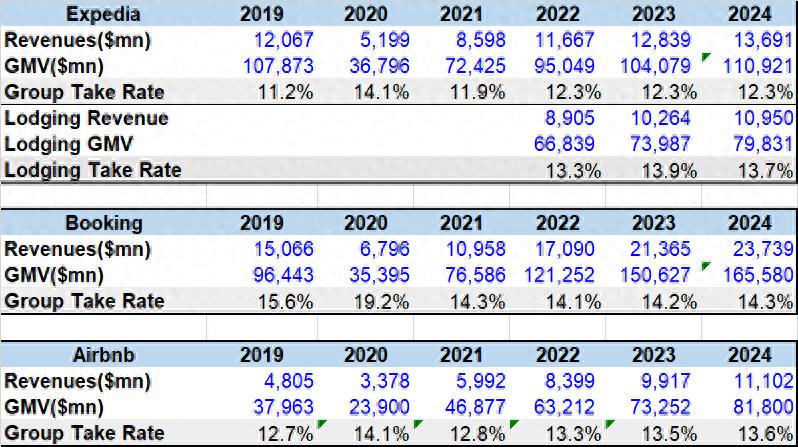

According to the latest financial reports, in 2024, Expedia's total revenue was $13.691 billion, with a transaction volume of $110.921 billion; Booking's total revenue was $23.739 billion, with a transaction volume of $165.58 billion; Airbnb's total revenue was $11.102 billion, with a transaction volume of $81.8 billion. Given that commissions are the primary revenue source for OTA platforms, the overall commission rate can be roughly calculated by dividing the platform's revenue by its transaction volume. Based on this calculation, the comprehensive commission rates for the three platforms are 12.3%, 14.3%, and 13.6%, respectively.

Extending the time frame to the past three years, Expedia has maintained a commission rate above 12%, Booking's comprehensive commission rate has remained above 14%, and Airbnb has maintained a rate above 13%.

In contrast, the performance of domestic OTA platforms, as reflected in Ctrip Group's latest financial report, shows that in 2024, the platform achieved a transaction volume of 1.2 trillion yuan, with a net revenue of 53.3 billion yuan and a comprehensive commission rate of 4.4%, which is only one-third of that of international OTA giants. Another domestic OTA platform, Tongcheng, reported a revenue of 13.106 billion yuan and a GMV of 201 billion yuan for the first three quarters of 2024, with a comprehensive commission rate of 6.5%, which is also less than half of that of international OTA giants.

This significant difference indeed surprises many, prompting the question: Why do domestic and foreign OTA platforms exhibit such a large gap in commission rates despite being in the same industry?

In the view of Chen Liteng, a digital life analyst at the E-commerce Research Center of the China Internet Economy Institute, 'Domestic consumers have been deeply influenced by e-commerce, forming a more mature habit of price comparison and a cost-effectiveness-oriented consumption pattern, which has a significant impact on the commission rate space of OTA platforms. The habit of price comparison makes consumers pay more attention to price factors when choosing accommodation, transportation, and other services. To attract and retain users, OTA platforms often need to offer coupons, discounts, and other incentives to attract consumers.'

As Chen Liteng stated, this stark contrast also illustrates the unique development logic and competitive landscape of domestic OTA platforms.

From a market competition perspective, the degree of competition in the domestic OTA sector far surpasses that of foreign markets. Platforms such as Ctrip, Tongcheng, and Meituan are vying for users and traffic, engaging in relentless competition on pricing and services. In such a fiercely competitive environment, once a platform raises its commission rate, it actively disrupts the competitive balance, causing a large number of users to quickly flow to rival platforms with lower commissions.

Conversely, the international trio of Expedia, Booking, and Airbnb have established dominant positions in their respective regions of strength. For example, Booking holds a major advantage in Europe due to its deep brand heritage and abundant accommodation options, allowing it to set commission rates relatively autonomously.

Additionally, differences in operating models are a crucial factor. Domestic platforms pursue a diversified and comprehensive service approach. For instance, Ctrip has deeply integrated ticketing, hotel reservations, car rentals, and other local life services, constructing a vast ecosystem. Through this diversified marketing strategy, the consumption behavior of a single user can drive growth across multiple business segments, realizing multi-channel profitability.

At the same time, domestic OTA platforms benefit from China's labor dividend, with relatively low labor costs, and the scale effect of a large, unified market, enabling lower-cost operations. This allows them to maintain the healthy development of the platform with lower commission rates. It's somewhat similar to the difference between DeepSeek and ChatGPT, where the former achieves similar functionality at a much lower cost.

As a result, the platform's dependence on single commission income decreases, naturally giving it the confidence to lower commission rates. Although foreign OTA platforms are also expanding their businesses, their diversification is not as advanced as that of domestic platforms, and their primary revenue still comes from accommodation booking commissions. Therefore, they are more cautious when adjusting commissions.

Nowadays, as competition intensifies among domestic OTA platforms, low commissions enable them to offer more affordable flight and accommodation prices to users, aligning with consumers' current demand for cost-effectiveness and diversified travel experiences, thereby attracting a large number of users. At the same time, a large number of small and medium-sized merchants are willing to join the platform due to low commissions, enriching product supply and creating a virtuous cycle.

It is undeniable that in the past, 'Commission Wars' were a primary means for OTA platforms to rapidly expand. To attract hotel and airline partners, platforms lowered their commission rates, competing for market share with low-cost advantages. This strategy worked in the short term, but as the market gradually matured, the drawbacks of commission wars became apparent.

In particular, while low commissions can attract merchants, they also significantly compress the profit margins of platforms and partners, leading enterprises into a 'low-price competition' dilemma. When platforms primarily rely on low commissions to attract merchants and low prices to attract users, merchants prioritize reducing operating costs over improving service quality.

In fact, the domestic OTA industry has long realized that relying solely on low commissions to capture market share is not a sustainable growth model. Therefore, faced with the drawbacks of commission wars, the OTA industry has begun to shift towards 'Efficiency Wars', leveraging technological innovation, user experience optimization, and diversified revenue models to enhance overall operational efficiency and build a healthier business ecosystem.

In this 'Efficiency Wars', AI and big data technologies have become key drivers.

Domestic OTA platforms actively apply new technologies such as artificial intelligence and large models. For example, AI applications are used to improve user decision-making efficiency, with intelligent robots answering customer questions. The improvement in operational efficiency also allows platforms to maintain lower commission rates.

According to 'Interesting Business Insights', on the Ctrip platform, 80% of inquiry questions can be resolved by AI, with after-sales service automation exceeding 70%, and 95% of needs being responded to within 20 seconds.

These phenomena undoubtedly demonstrate the significant efficiency improvements of domestic OTA platforms. However, 'Efficiency Wars' do not solely rely on AI and big data technologies; they also involve comprehensive optimization of domestic OTA platforms' service experience and systems. Especially to reduce dependence on single commission income, domestic OTA platforms have begun exploring various profit models such as membership systems, advertising revenue, and supply chain integration.

Currently, domestic OTA platforms have transitioned from a simple 'information matching' role to that of supply chain managers, helping merchants optimize resource allocation and enhance overall operational efficiency. Whether it's the construction of membership systems or the integration of supply chains, domestic OTA platforms are exploring more sustainable growth models to ensure profitability under the low commission strategy and enhance overall industry efficiency.

Zhang Shule, an internet industry commentator, believes that 'How OTA platforms flatten channels, increase transaction rates, and extend the user consumption chain are efficiencies that must be achieved in the context of entering a stock market. Especially during a stage of more competitors and intense competition, it is necessary to make consumers feel cost-effective and convenient throughout the process, and even provide unexpected value-added services beyond travel plans to sustain long-term success.'

Today, the growth rate of the Chinese OTA market cannot be underestimated. Data shows that by 2025, China's online travel market size is expected to exceed 1.5 trillion yuan, becoming one of the fastest-growing markets globally. Behind this growth lies the continuous recovery of domestic tourism consumption, as well as the upgrading of the OTA industry from 'Commission Wars' to 'Efficiency Wars', enhancing user experience and platform profitability through innovative means such as AI and big data technologies.

The next competition among OTA platforms will no longer be about 'who has lower commissions' but 'who provides better services, higher efficiency, and superior user experience'. Zhang Shule believes that 'In the future, if domestic OTA platforms can further penetrate the entire tourism industry chain and use the power of the internet to drive changes in the consumer experience of traditional tourism through big data, cloud computing, and artificial intelligence, or even transform some traditional tourism models, they may continue to open up incremental markets.'

As the global tourism market gradually recovers, the domestic OTA industry will also usher in a golden period of development. Leveraging efficiency advantages and business model innovations, domestic OTA platforms are expected to stand out in the fierce market competition and lead the industry towards a new stage of development.

-

![]()

Enflame Tech's IPO Journey: Navigating Over 5.9 Billion Yuan in Losses and Soaring Debt in Q1 This Year

-

![]()

Trillion-Yuan Giant Li Shufu 'Streamlines': Could Levc Be the Casualty?

-

![]()

AI Competes for Electricity and Generates Power in the Gobi Desert

-

![]()

The First Batch of Victims of the AI Bubble: Programmers

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'