After 300 Billion, How Far Has Chery's 'Value Leap' Progressed?

03/27 2026

03/27 2026

641

641

Introduction

Overseas Revenue Exceeds Half, Securing 'Global Leader' Status; Breaking Through Domestic Premiumization Becomes the Next Major Challenge

If a single theme were to define Chery's 2025, it would be 'pursuing value leap inward while achieving global deepening outward.'

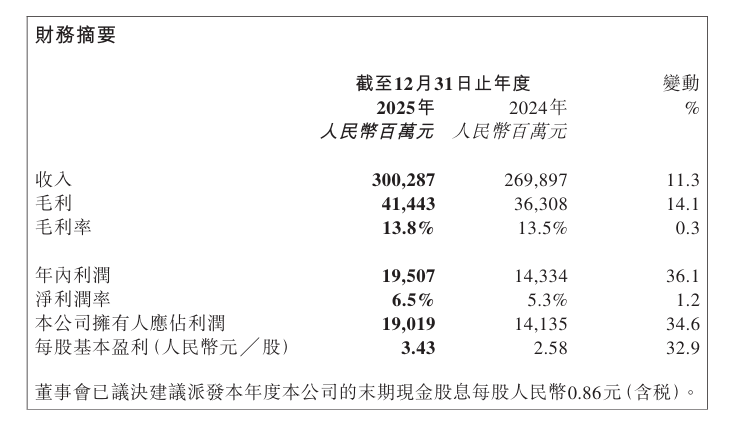

Judging by Chery Automobile's first annual financial report since going public, its revenue surpassed 300 billion for the first time, with net profit surging by 36.1%. Both new energy and overseas businesses experienced explosive growth. Against the backdrop of intensifying competition in the automotive market in 2025, Chery has undoubtedly charted a steep growth trajectory.

However, beneath the shining data lies a financial report that clearly outlines the strategic choices and potential challenges faced by a traditional giant during a period of intense transformation. To understand Chery's 2025, one must recognize the strength of its dual-wheel drive while also examining the potential roadblocks encountered at high speed.

Three Major Growth Poles Take Shape, Transformation Enters Harvest Phase

Chairman Yin Tongyue once mentioned during the Two Sessions that 'Chery does not engage in low-level price wars. Instead, we hope to move away from the intensely competitive zone and into the profit zone through technology, management empowerment, and quality improvement.' This perhaps best encapsulates Chery's development in 2025.

Chery's total annual revenue reached 300.29 billion yuan, with a net profit of 19.51 billion yuan, a year-on-year increase of 36.1%. This profit growth rate significantly outpaces its 14.6% sales growth and 11.3% revenue growth. More critically, the net profit margin rose from 5.3% to 6.5%. This set of data indicates that Chery's growth has shifted from mere volume-driven success to a new phase that balances scale and quality, with its overall profit structure being optimized.

From a product perspective, new energy has become the primary sales driver, successfully entering the first tier.

2025 can be considered the first year of Chery's new energy rise. New energy vehicle sales reached 826,500 units, soaring by 72.5% year-on-year, with revenue accounting for 32.6% of total revenue. Since November, its wholesale new energy vehicle sales have consistently ranked among the top three in the industry. This means Chery has not only caught up in electrification but has also successfully entered the most fiercely competitive mainstream market with popular models like the Fengyun series (e.g., Fengyun A9L, T11). The gross profit margin of the new energy business surged to 8.8%, proving its initial profitability and achieving a crucial leap from 'burning money to expand the market' to 'self-sufficiency.'

From a market perspective, the quality of globalization is undergoing a qualitative transformation, with Europe becoming the key to new growth.

Chery exported 1.2944 million vehicles, with overseas revenue reaching 157.42 billion yuan, accounting for 52.4% of total revenue—surpassing the domestic market for the first time and solidifying its position as China's leading automotive exporter.

However, what deserves even greater attention is the qualitative transformation of its globalization. European market sales soared by over 200% year-on-year. This indicates that Chery's overseas expansion has successfully upgraded from early product trade in Asia, Africa, and Latin America to brand deepening in the high-value European market. This not only drives sales but also represents a comprehensive upgrade in brand value and compliance capabilities.

In 2025, as electrification and intelligence reshape the industry, Chery's performance is the best reward for its long-standing commitment to 'technology-driven enterprise development.' With 14.715 billion yuan in R&D investment, a year-on-year increase of 39.6%—a remarkable rise—the funds were directed toward five key areas: Mars Architecture, Kunpeng Power, Lingxi Intelligent Cockpit, Falcon Intelligent Driving, and Galaxy Ecosystem, forming a reserve of over 400 core technologies.

At a recent Battery Night event, Chairman Yin Tongyue bluntly stated, 'Chery is a green energy company, a battery company, and a high-tech company disguised as an automaker.' This signifies that Chery's competitive dimension has shifted from vehicle manufacturing to the construction of an energy ecosystem, which is crucial for its brand elevation and capital market valuation.

Advances and Challenges Under the Main Theme

Chery has proven the victory of long-term technological pragmatism through solid profit growth and outlined a new paradigm for Chinese automakers' globalization with over half of its revenue coming from overseas markets.

However, there are dissonant notes amid the melody.

Amid the financial report's overwhelming success, a potential question arises: Has Chery's brand image and visibility among domestic consumers kept pace with its performance growth? Despite ranking third in new energy vehicle sales, it cannot be denied that its domestic media presence still lags behind BYD, Geely, Huawei-affiliated brands, NIO, XPeng, and Li Auto.

This does not imply failure but rather represents the most critical and challenging phase of its 'value leap' journey.

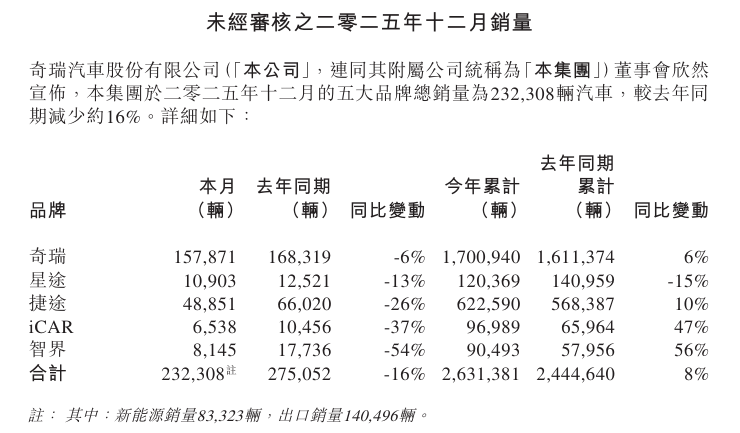

From a product standpoint, the Exeed brand, tasked with premiumization, sold only 120,400 units in 2025, a 15% year-on-year decline. Highly anticipated models like the Exeed ET received a lukewarm market response.

In terms of average pricing, according to JLRC's 2025 review of brand pricing in China's passenger vehicle market, Luxeed's average sales price is highest in the 200,000-300,000 yuan range, while Exeed, Fengyun, Jetour, and iCAR are concentrated in the 100,000-200,000 yuan range. Chery's main brand falls below 100,000 yuan.

The Luxeed brand, in collaboration with Huawei, sold 90,500 units in 2025, a 56% year-on-year increase. However, 2026 got off to a rocky start, with Luxeed sales reaching only 5,451 units in January-February, a 76.3% year-on-year decline. Despite Huawei's support, it has failed to stand out even within Huawei-affiliated brands like Aito and Avatar.

Chery's overall structure is imbalanced. In 2025, Chery's main brand sold 1.7 million units, and Jetour sold 620,000 units, with average prices of 97,000 yuan and 130,000 yuan, respectively, accounting for 88% of total sales. These two main brands firmly dominate the market below 150,000 yuan. Meanwhile, the market above 200,000 yuan is almost entirely controlled by new forces like Li Auto, Aito, and NIO, as well as models like BYD's Han and Tang.

Evidently, Chery lacks a dominant 'blockbuster' product to reshape consumer perceptions. Its technological prowess and overseas success stories have yet to fully translate into strong brand premium in the domestic market.

For Chery to achieve a true value leap, breaking through in the domestic premium market is a strategic imperative. Currently, the Luxeed brand, developed in deep collaboration with Huawei, carries this core mission. Although its market performance still requires longer-term validation after initial adjustments and explorations, it has been designated as the group's 'top priority strategic project.' This itself points to the strategic direction: All efforts must be concentrated on propelling the Luxeed brand to break through the 300,000 yuan average price ceiling, thereby establishing a new high-tech premium image and driving brand momentum across the entire group.

Meanwhile, the company must also ensure clear resource allocation and brand synergy. While focusing on Luxeed's premium breakthrough, it should effectively integrate and differentiate sub-brands like Fengyun, Jetour, and iCAR, which target the 100,000-200,000 yuan mainstream market, to consolidate the foundation and create synergies.

The ultimate goal is to build a well-defined, mutually supportive brand hierarchy spanning from the mainstream to the premium market, ensuring that the 'arrow' of premiumization has a solid and broad 'base,' systematically elevating overall brand value.

Overall, Chery's 2025 financial report is a solid and impressive 'mid-transformation report card.' It proves through data that its dual-wheel drive strategy of 'new energy + globalization' has achieved phased success, not only scaling up but also improving profit quality and structure.

Its strengths are evident: solid manufacturing capabilities, strong cost control, an early and deep global network, and a reputation built on practical technology routes like hybrid vehicles. These form its stable foundation.

What capital markets and industry observers expect is not just a one-year outbreak (breakout) but the construction of sustained, steady growth and risk resilience. For Chery, the challenges ahead include converting its high overseas market share into high and stable profits, achieving a complete leap in brand perception in the domestic market, and forging truly dominant core competitiveness across all technological track (segments). These will be the critical thresholds it must cross to move from 'good' to 'exceptional' and transform from an 'automotive company' into a 'global tech mobility enterprise.'

The 2026 race will only become more intense. Chery's offensive mode has shifted to a higher-difficulty level.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?