Quarterly Report | All-Channel Online Laptop Sales in China Plummet by 19% in Q1 2026; Lenovo, ASUS, Apple, HP, and Mechrevo Dominate with 80% Market Share

05/13 2026

05/13 2026

494

494

Data Release

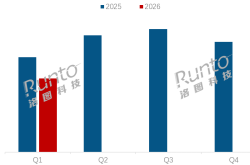

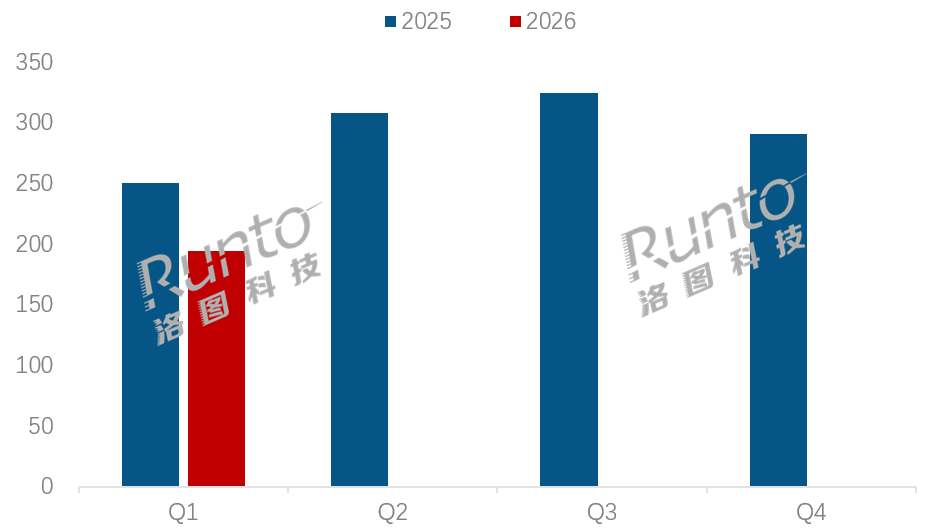

According to Runto, in the first quarter of 2026, online laptop sales across all channels in China amounted to 2.3 million units, marking a 19.2% year-on-year decline. Correspondingly, sales revenue reached RMB 14.8 billion, a 14.7% decrease.

On China's traditional mainstream e-commerce platforms, Lenovo, ASUS, Apple, HP, and Mechrevo emerged as the top five sellers, collectively capturing a 79.8% market share, a 9 percentage point increase from the previous year.

The average retail price on online platforms stood at RMB 6,431, reflecting a roughly 2.5% rise from the same period in 2025 and continuing a multi-quarter upward trend.

AI PC adoption reached 48%, with an average price approximately 20% higher than the overall market at RMB 7,718.

According to Runto's latest "China Notebook Computer Online Retail Market Monthly Tracker" report, in Q1 2026, online laptop sales across all channels in China hit 2.3 million units, down 19.2% year-on-year, with sales revenue at RMB 14.8 billion, a 14.7% decline.

This nearly 20% decrease marks the worst start to a year in a decade. Runto attributes this downturn to a combination of "high costs, a high base from the previous year, and low demand."

In the first quarter of this year, a supply chain crisis triggered by memory chips erupted. AI servers absorbed a significant portion of memory production capacity, causing consumer laptop costs to surge. DRAM and SSD prices tripled from their 2025 lows, while Intel's CPUs saw across-the-board price increases. Additionally, the production of low-end processors was reduced to prioritize server and AI chip supply.

The high base and low demand are interconnected. The widespread implementation of national subsidies in 2025 drove over 20% growth in the first quarter of that year, prematurely depleting market demand for 2026.

Another factor contributing to the early release of demand was the rush to upgrade enterprise and personal devices triggered by the end of Windows 10 support in 2025. Furthermore, subsidies dropped to 15% with quotas in 2026, significantly reducing their effectiveness in stimulating demand.

Sluggish demand was also attributed to rising terminal prices and prolonged consumer weakness. Affected by soaring component costs like memory, some mainstream laptop prices rose by up to 20%, deterring price-sensitive students and home users. Additionally, tablets, smartphones, and cloud computers have long been diverting users, with substitution effects intensifying. High-end tablets now approach laptop performance, offering lighter, cheaper alternatives that meet 70% of mobile office needs. Flagship smartphones now match mid-range 2020 laptop performance, fully replacing simple office and entertainment tasks, further compressing market demand.

Overall, the market in the first quarter of 2026 appeared to enter a demand vacuum.

However, amid broader market pressure, structural upgrades became prominent. AI PC adoption continued, and OLED panels saw accelerated adoption, driving the product mix toward premium and AI-driven iterations. This signals an industry trend: laptops are shifting from "essential office tools" to "professional productivity devices," with the market contracting but moving upmarket.

I. Channel Structure:

Traditional Mainstream E-Commerce Dominates; Emerging E-Commerce Gains Share

Runto categorizes online channels into traditional mainstream platforms (JD.com, Tmall, Suning.com) and emerging platforms (Douyin, Kuaishou, Pinduoduo).

Traditional mainstream e-commerce dominates the 3C product market, accounting for about 85% of online sales in the first quarter of 2026, with 1.94 million units sold, a 22.6% year-on-year decline. Meanwhile, sales revenue fell 20.7% to RMB 12.5 billion.

Conversely, emerging e-commerce's sales share rose to 15%, becoming a key battleground for brand growth.

Quarterly Online Laptop Sales in China (2025-2026Q1)

Source: Runto online monitoring data (unit: 10,000 units)

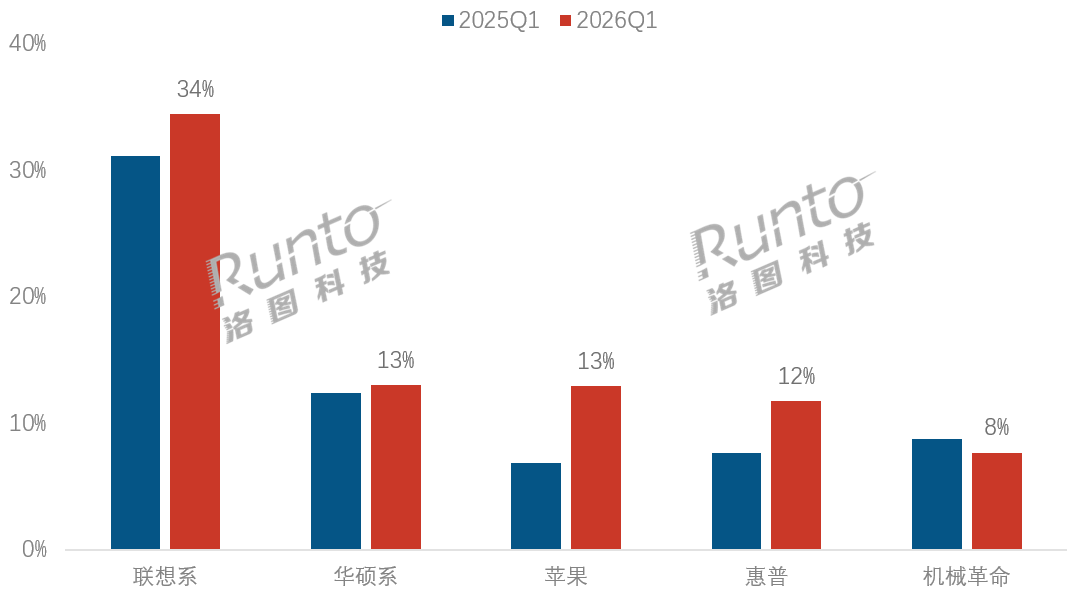

II. Brand Competition:

Top 5 Brands Account for Nearly 80% of Sales; Lenovo Leads with Over 30% Share, Apple Surges

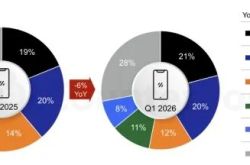

According to Runto's online data, market concentration continued to rise in the first quarter of 2026 on traditional mainstream e-commerce platforms. Lenovo, ASUS, Apple, HP, and Mechrevo ranked as the top five sellers, collectively holding a 79.8% market share, a 9 percentage point increase from the previous year.

Lenovo firmly led with about a 34% online share, leveraging deep supply chain integration to expand its lead amid rising component costs.

ASUS and HP ranked second and fourth, respectively, with traditional PC giants' extensive channel coverage and mature brand experiences forming core barriers to market position.

Apple was the standout performer this quarter: its sales share on mainstream e-commerce platforms rose to 13%, up about 6 percentage points year-on-year. The new MacBook Neo sold well immediately after launch, bringing the MacBook series down to the RMB 4,000–5,999 mainstream price range and driving explosive growth in this segment. Combined with cost advantages from its in-house M-series chips and macOS ecosystem appeal, Apple's market share jumped significantly.

Mechrevo ranked fifth with about an 8% share, targeting price-sensitive gamers with cost-effective offerings.

Top Brands' Online Sales Share in China's Laptop Market (Q1 2026)

Source: Runto online monitoring data (unit: %)

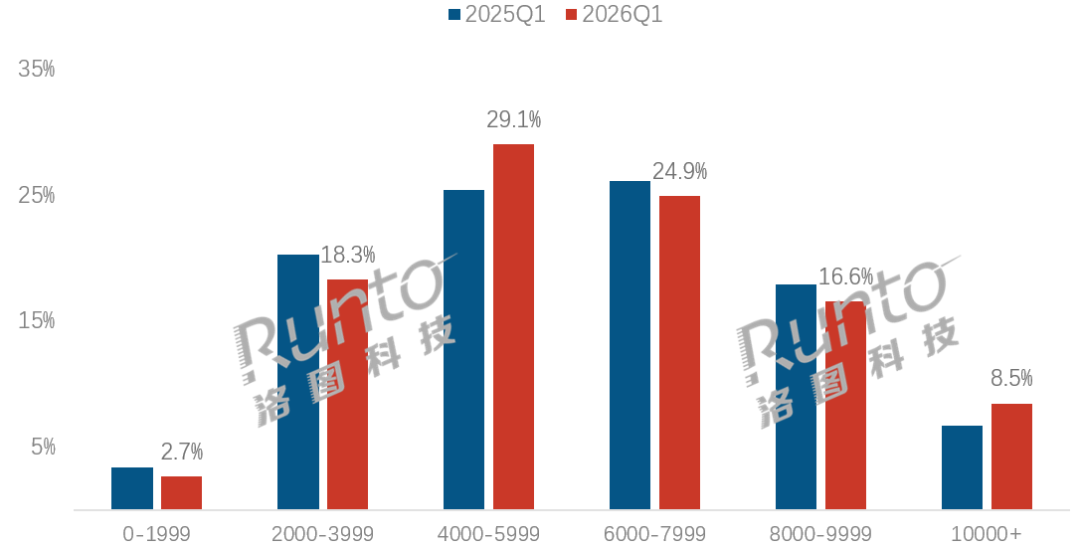

III. Market Pricing:

Average Prices Rise for Multiple Quarters; Sales Share of Models Over RMB 10,000 Rises to 8.5%

According to Runto's online data, the average retail price of laptops on traditional mainstream e-commerce platforms was RMB 6,431 in the first quarter of 2026, up about 2.5% year-on-year, continuing a multi-quarter upward trend.

The premium segment (over RMB 10,000) benefited from full subsidies (15% subsidy ratio, capped at RMB 1,500) and professional demand, with its sales share rising to 8.5%, up about 2 percentage points year-on-year. Ecosystem flagship models were the main drivers in this price range.

The RMB 4,000–5,999 segment saw significant share growth to 29.1%, driven by Apple's hot-selling models. The RMB 6,000–9,999 segment's share declined 2.6 percentage points to 41.5%.

Price Segment Sales Share in China's Online Laptop Market (Q1 2026)

Source: Runto online monitoring data (unit: %)

IV. Product Trends:

AI PC Penetration Rises to 48%; OLED Panels Set for Mass Production

AI PC has been the core driver of market evolution over the past year, with sales performance defying the notion of being "overhyped but underperforming."

According to Runto's online data, AI PC penetration reached 48% on traditional mainstream e-commerce platforms in the first quarter of 2026, with an average price about 20% higher than the overall market at RMB 7,718.

Apple stood out with its in-house AI chips, seeing AI product sales surge 196% year-on-year. Its AI PC market share rose to 27%, up 15 percentage points year-on-year.

In display technology, OLED panel adoption reached 10% and is expanding to mid-range models. Among OLED products, the RMB 4,000–5,999 segment's sales share rose to 41%, up 15 percentage points year-on-year.

In the second and third quarters of this year, Samsung Display's (SDC) A6 line in Asan, South Korea, and BOE's B16 line in Chengdu will achieve mass production, with monthly glass substrate capacities of 15,000 and 32,000 units, respectively. This will directly drive OLED penetration to exceed 15% in 2026 and accelerate adoption in mid-range models. TCL CSOT's T8 and Visionox's 8.6-generation lines are expected to start mass production after the fourth quarter of 2027.

V. Market Outlook:

Annual Sales Decline Expected to Narrow to Less Than 15%

Looking ahead, China's laptop market will follow a trajectory of "short-term deep correction, mid-term recovery, long-term transformation." Key trends include: volume contraction, structural upgrades, AI-driven growth, and oligopolistic concentration, with the market shifting from "mass adoption" to "professional value."

In terms of scale, despite the upcoming mid-year "618" promotion in China, market prospects remain cautious. In the short term, recovery is unlikely as high costs and weak demand will persist into the third quarter. Insufficient subsidies and price hikes will prompt users to extend replacement cycles from 3–4 years to over 5 years.

Runto predicts that by the fourth quarter of this year at the earliest, memory production capacity may return to the consumer side, with price increases narrowing and gradually declining. Coupled with the launch of Intel/AMD's new AI processors, the market could reach a recovery inflection point, with full-year retail volume declines narrowing to -10% to -15%. In a less likely scenario, if the supply chain crisis extends to 2027, cost overruns would become the industry's core risk.

Moving forward, China's market faces two major opportunities: the AI revolution and domestic substitution. AI PCs could become standard by 2028, driving replacement cycles and creating new value, price bands, and growth periods. Additionally, domestic CPU/OS adoption in government and enterprise procurement will grow rapidly.

In the longer term, three to five years from now, laptops may no longer be a mass-market staple but will differentiate themselves by focusing on core high-value scenarios, positioning as specialized tools for professional creation, enterprise office, and geek/gaming segments. By then, the market will shift from "volume growth" to a new cycle of "price, quality, and profit upgrades."

Related Policies

In April this year, the State Council issued the "Opinions on Promoting Service Sector Expansion and Quality Upgrades," emphasizing the deep implementation of the "AI+" initiative. The "State Council Opinions on Deepening the Implementation of the 'AI+' Initiative" released in August 2025 mentioned "cultivating an intelligent product ecosystem, vigorously developing AI computers," and "increasing procurement of AI technology products and services through government purchases and first-purchase orders."

Thank you for reading. If you found this insightful, please like, share, and follow.

-

![]()

China Raytronics Secures Nomination for 2026 Optics Industry High-Growth Enterprise Award

-

![]()

A Regular and Periodic Exchange Mechanism to Be Set Up! North Opto-electronics and Costar Forge New Avenues for Intelligent Integration

-

![]()

After Joining NVIDIA’s Core Supply Chain, This Optical Company Secures Fresh Funding!

-

![]()

Quarterly Report | All-Channel Online Laptop Sales in China Plummet by 19% in Q1 2026; Lenovo, ASUS, Apple, HP, and Mechrevo Dominate with 80% Market Share

-

![]()

Who’s Encircling and Attacking OpenAI? A New Tech Giant War Has Begun

-

![]()

AI Application Integration Surges Eightfold in a Year! Your Job Might Be Vanishing Without Notice

-

![]()

Mobile Phone Manufacturers: The Time Has Come to Unveil True AI Phones

-

![]()

Kunlunxin's IPO: Is Baidu's Pricing Dilemma Lurking Beneath?