Xiaomi Auto’s Profits Skyrocket, Revenue Tops 100 Billion Yuan, Gross Margin Hits 24%, Marking Fastest Path to Profitability

03/27 2026

03/27 2026

674

674

Emerging as the Second Growth Engine

Author|Wang Lei

Editor|Qin Zhangyong

The fastest profitable new entrant in automotive history has arrived.

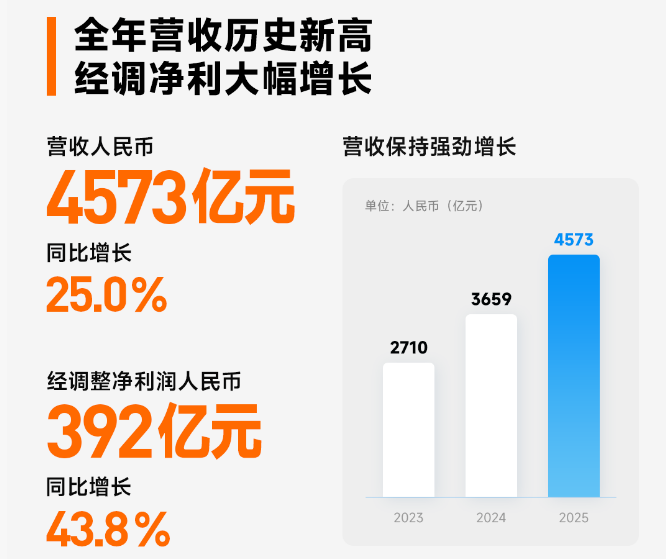

Last night, Xiaomi Group officially released its Q4 2025 performance report and full-year financial results, revealing total annual revenue of 457.3 billion yuan and adjusted net profit of 39.2 billion yuan—both record highs.

The spotlight falls on its automotive business, with revenue surpassing 100 billion yuan for the first time, reaching 106.1 billion yuan, up 223.8% year-on-year. More critically, in 2025, Xiaomi’s auto segment achieved its first full-year operating profit of 900 million yuan, transitioning from annual losses to profitability.

Undeniably, Xiaomi Auto’s growth trajectory is the envy of competitors. Less than two years after its debut vehicle launch, the auto business achieved full-year profitability, officially breaking free from the cycle of losses.

However, behind the automotive segment’s meteoric rise lies pressure on Xiaomi’s core smartphone business.

01

Revenue Tops 100 Billion Yuan

From an annual perspective, Xiaomi’s recently released financial performance is truly remarkable.

Total revenue reached 457.287 billion yuan, up 25.0% year-on-year. While the growth rate slowed from 35.04% in 2024, the absolute figure marked a historic high, surpassing 400 billion yuan for the first time. Adjusted full-year net profit hit 39.2 billion yuan, up 43.8% year-on-year—clearly the best performance in company history.

The 43.8% profit growth far outpaced the 25% revenue growth, signaling that while expanding scale, Xiaomi significantly optimized operational efficiency and product mix.

The driving force behind Xiaomi’s record-breaking 2025 performance? A dual surge in premium smartphones and smart electric vehicles (EVs).

Notably, the smart auto business achieved a milestone leap from losses to profitability, contributing positive adjusted profit for the first time in 2025.

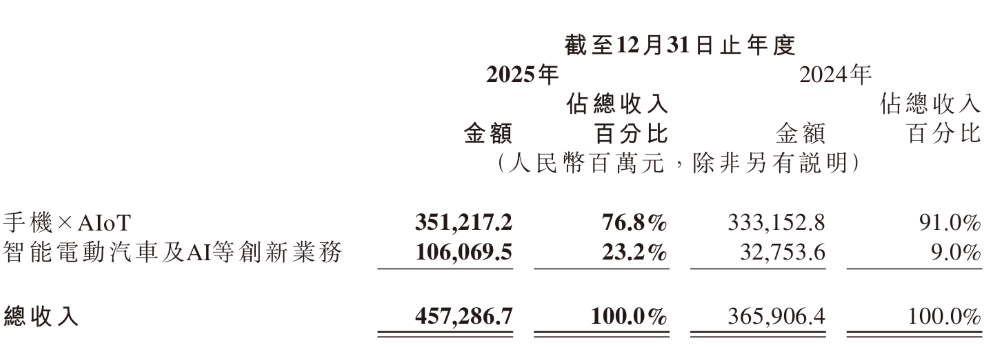

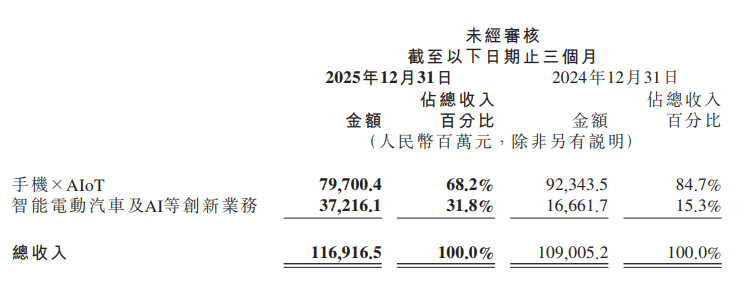

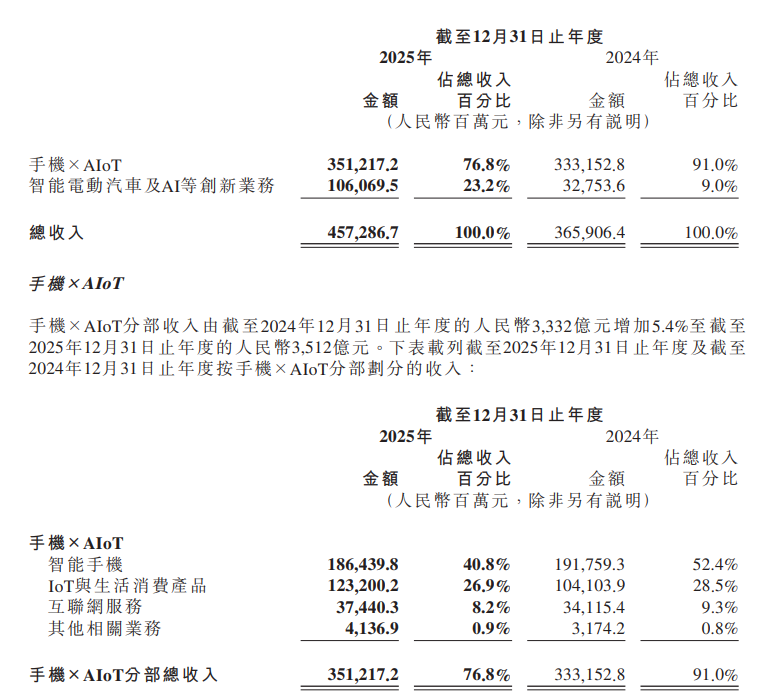

Specifically, in 2025, Xiaomi’s smart EV and AI innovation segment generated 106.1 billion yuan in revenue, up 223.8% year-on-year. Within this, smart EV revenue reached 103.3 billion yuan, soaring by 71.2 billion yuan from 32.1 billion yuan in 2024—a 221.8% year-on-year increase. Related business revenue accounted for just 2.8 billion yuan.

This positions the smart auto business as Xiaomi Group’s undisputed second growth engine. In 2025, smart EVs and AI innovation accounted for 23.2% of total revenue, up sharply from 9.0% in 2024.

Xiaomi attributed this to increased auto deliveries and rising average selling prices (ASPs). In 2025, the company delivered 411,082 vehicles, up approximately 274,200 units from 136,900 in 2024—a 200.4% year-on-year surge.

The financial report also highlighted that the Xiaomi SU7 ranked first in domestic sedan sales over 200,000 yuan in 2025, while the Xiaomi YU7 led domestic mid-to-large SUV sales for seven consecutive months.

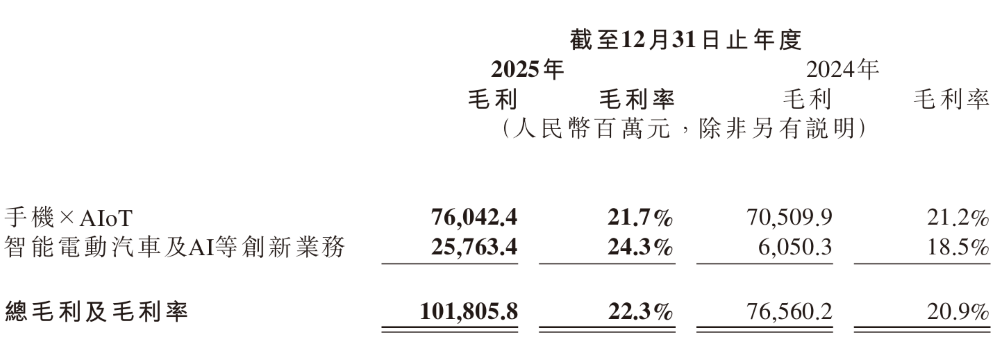

Moreover, higher sales volumes translated to stronger profitability. In 2025, the segment’s gross margin jumped from 18.5% in 2024 to 24.3%, achieving positive operating profit for the first time at 900 million yuan. This contrasts sharply with the adjusted net loss of 6.2 billion yuan in 2024 for Xiaomi’s smart EV and innovation segments.

What does a 24.3% gross margin signify?

For context, Li Auto—profitable for three consecutive years—reported a comprehensive gross margin of 18.7% in 2025. XPENG stood at 18.9%, Leapmotor at 14.5%, and NIO at 13.6%. Xiaomi even surpassed industry giants like BYD (17.5%) and Tesla (17.8%).

In China’s auto sector, only Seres matched Xiaomi’s gross margin, reaching 29.38% in the first three quarters of 2025 (though its full-year data remains pending).

This makes Xiaomi Auto the fastest profitable new entrant in automotive manufacturing, achieving profitability just two years after the SU7’s launch.

This success stems from deliveries of higher-ASP models like the SU7 Ultra and YU7 series. In 2025, Xiaomi Auto’s ASP reached 251,200 yuan, up 7.1% from 234,500 yuan in 2024. Financial data reveals Xiaomi earned roughly 61,100 yuan in gross profit per vehicle in 2025, with a net profit of 2,190 yuan per vehicle.

Additionally, Xiaomi Group’s 2025 R&D spending hit 33.1 billion yuan, up 37.8% year-on-year, driven by increased investments in smart EVs and AI innovation.

Notably, Xiaomi’s smart auto business is bundled with AI and other innovation segments. Given that AI remains in a high-cost phase, Xiaomi CFO Li Shiwei acknowledged that the segment’s profitability reflects a “delicate balance” between “auto scaling benefits” and “AI/robotics R&D investments.”

In other words, Xiaomi Auto’s standalone gross margin and profit may exceed surface-level metrics.

02

Smartphone Business Decline

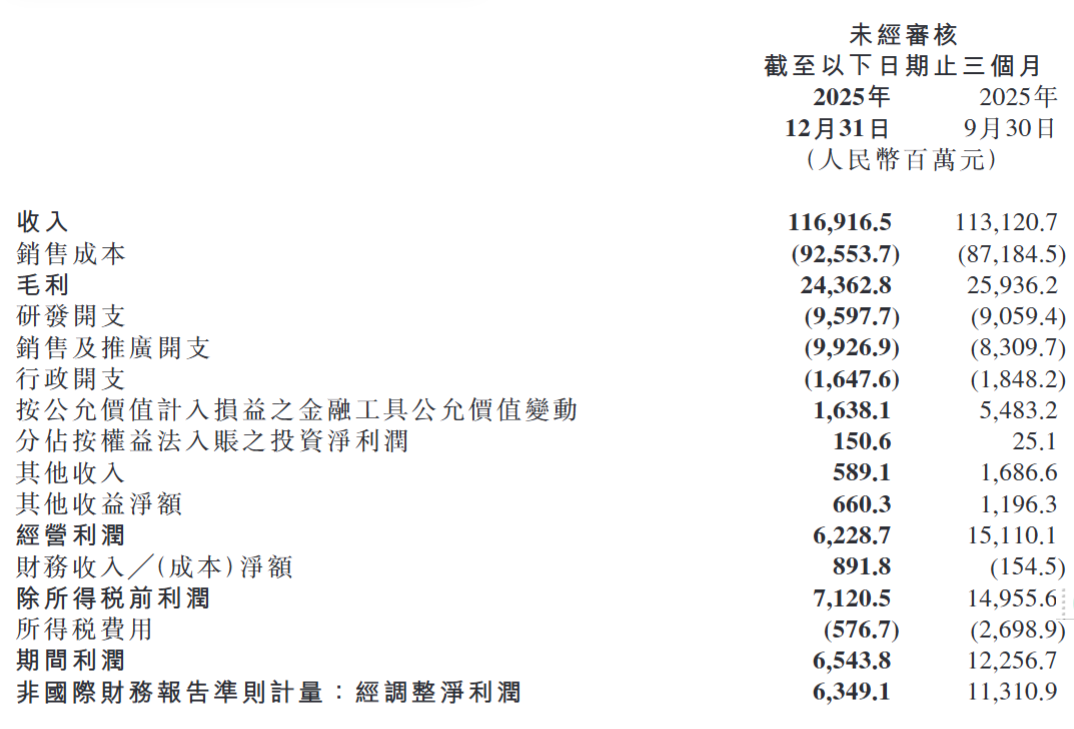

A closer look at Q4 2025 reveals a stark contrast: single-quarter operating profit fell to 6.229 billion yuan, down 29% year-on-year from 8.3 billion yuan in Q4 2024 and halved from 15.1 billion yuan in Q3 2025.

Q4 also snapped three consecutive quarters of record profits. Moreover, Xiaomi’s net cash from operating activities plummeted to just 614 million yuan.

The Q4 profit decline is easily explained: Xiaomi’s smartphone business contracted sharply. Shipments fell 11% year-on-year to 37.7 million units, with revenue at 44.3 billion yuan—declining both annually and quarterly. Smartphone gross margin sank to a historic low of 8.3%.

The primary culprit? A surge in memory chip prices since November 2025. Lu Weibing admitted during the earnings call that price hikes exceeded even aggressive industry forecasts.

This trend is industry-wide. Since Q1 2025, smartphone makers globally have raised prices due to soaring upstream memory costs.

Against this backdrop, Xiaomi Auto’s Q4 performance shone brightly. Smart EV revenue hit 36.3 billion yuan, up 20 billion yuan from 16.3 billion yuan in Q4 2024—a 122.0% year-on-year increase.

It accounted for over 30% of Q4 group revenue, nearing the smartphone segment’s 37% share.

Gross margin improved to 22.7%, contributing 1.1 billion yuan in operating profit—not only achieving quarterly profitability but also bolstering group earnings. In essence, Q4 revenue growth stemmed almost entirely from the auto business.

Annually, the smartphone × AIoT segment generated 351.2 billion yuan in revenue, up 5.4% year-on-year. However, smartphone revenue declined 2.8% to 186.4 billion yuan, with shipments falling from 168.5 million to 165.2 million units. Global market share dipped from a peak of 14% to around 11%.

Despite breakthroughs in premium models (3,000+ yuan segment accounting for 27.1% of sales), gross margin fell from 12.6% to 10.9%. This means smartphone profit contributions shrank from 24.254 billion yuan in 2024 to 20.266 billion yuan in 2025—a 16.4% decline.

Comparing gross margins, the smartphone × AIoT segment hit 21.7% in 2025, up 0.5 percentage points year-on-year but 2.6 points lower than the smart EV and AI innovation segment’s combined margin.

This underscores a clear shift: Xiaomi’s auto business is now more profitable and growing faster than its smartphone division.

It also signals Xiaomi Group’s transition from smartphone dependency to an “auto + smartphone” dual-drive model, with the auto segment even beginning to support the smartphone business.

Lu Weibing acknowledged at the earnings call that “memory price hikes, subsidy reductions, and intensified competition will create short-term pressure.” Last year, Xiaomi predicted memory prices would rise until 2027—already an aggressive forecast—but trends have exceeded expectations.

He also stated he understands why rivals are raising prices, as Xiaomi faces similar cost pressures. “If we can’t hold on, we’ll raise prices too. Xiaomi just lasted longer than others,” he said.

Additionally, while cars also use significant memory, the proportional cost increase is less severe. Memory price hikes affect auto margins but far less drastically than smartphones.

Clearly, Xiaomi has greater confidence in its auto segment than smartphones. During the earnings call, the company reiterated its 2026 target of delivering 550,000 vehicles.

With one business rising and the other declining, is Xiaomi approaching a “growth inflection point”?

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?