Auto Market in Q1 Declines by 17%, Calls for Radical Reforms

04/07 2026

04/07 2026

487

487

Introduction

A delayed market “shakeout” is preferable to a false boom.

The beginning of 2026 has not brought an “early spring” to China’s auto market.

According to data from the China Passenger Car Association (CPCA), retail sales in the first quarter (Q1) reached 4.236 million units, a 17% decrease year-on-year. This marks the weakest quarterly performance in a decade, excluding the extraordinary circumstances of the 2020 pandemic.

New energy vehicles (NEVs) faced an even harsher downturn, with retail sales dropping to 1.844 million units, a 24% year-on-year decline. The penetration rate of NEVs also fell from its peak in Q4 2025 to 47.3%.

While it is easy to succumb to doom-and-gloom sentiments, it is crucial to uncover the logic behind these figures and explore solutions for the industry.

Despite the grim numbers, they cannot obscure the underlying logic. This situation is more akin to a radical yet health-restoring shakeout rather than a market collapse.

Over the past two years, China’s auto market has been plagued by price wars, causing industry profit margins to plummet to 2.9%—less than half the average for industrial enterprises. It is widely acknowledged that this subsidy-fueled prosperity is unsustainable.

On one hand, there is a reliance on policy incentives and discounts to sustain sales volume. On the other, market competition and consumer choice are essential for maintaining a natural ecosystem. Extremes lead to decline; a balanced approach is necessary for a sustainable future.

While policies are being scaled back, they are not entirely abandoned—the goal is to wean the market off crutches, but not before it can fully recover on its own. As price bubbles deflate, the market begins to self-correct.

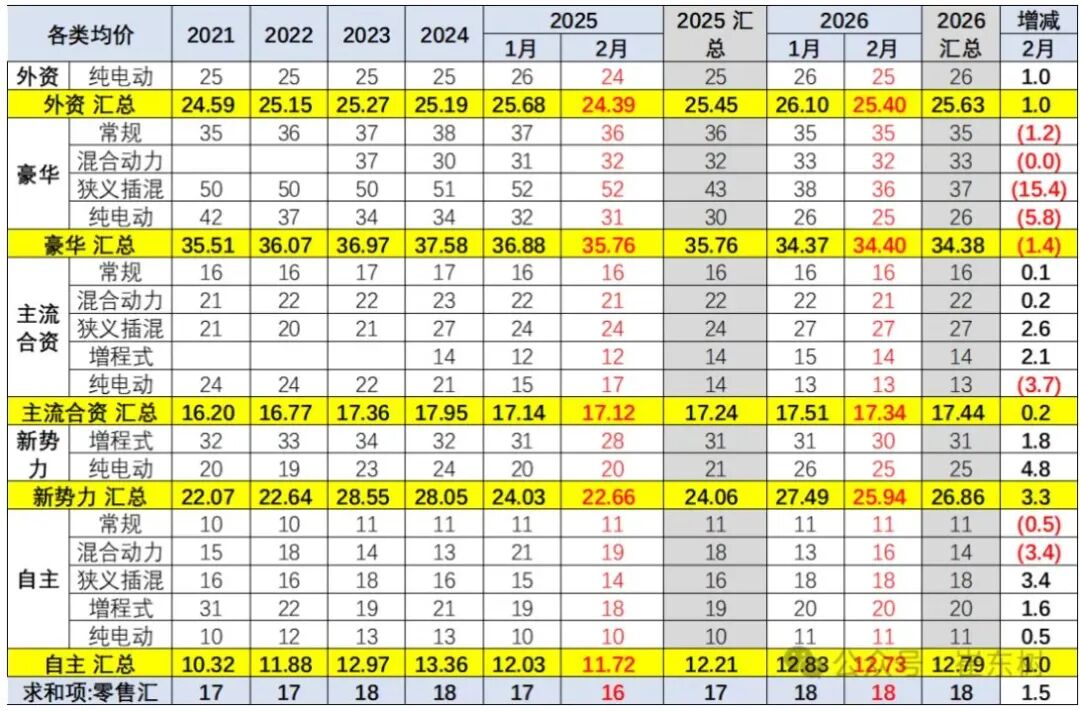

On one side, sales volumes decline; on the other, prices stabilize and quality improves. The average revenue per vehicle in Q1 increased from RMB 333,000 year-on-year to RMB 369,000. Terminal discounts narrowed significantly, and the number of price-cut models plummeted by 70% year-on-year.

Pain is inevitable, but radical reform is essential. This sharp pain signals structural optimization and the dawn of a more sustainable market.

01 The Coldest Q1 in a Decade

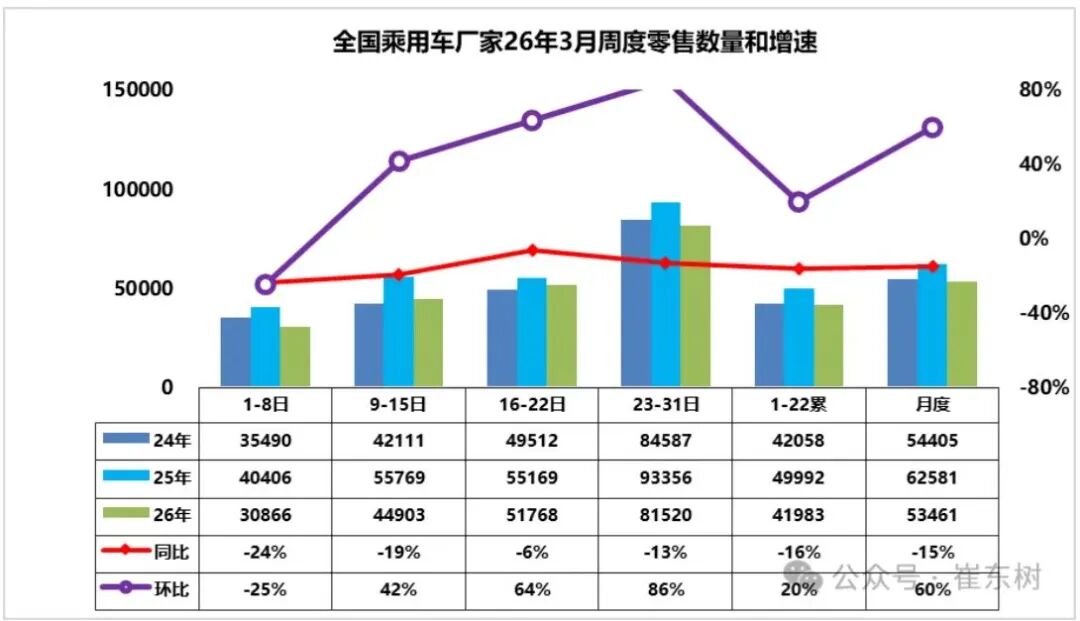

According to the CPCA’s latest weekly analysis, retail sales in China’s auto market reached 4.236 million units in Q1 2026, down 17.4% year-on-year.

How severe is this decline? Auto Business Review compiled historical passenger vehicle retail sales data for March and Q1 (excluding wholesale figures, which include exports and dealer deliveries, as well as overall sales including commercial vehicles), revealing this to be the coldest first quarter in a decade (excluding the pandemic-hit 2020).

Overall, Q1 2026 closely resembled Q1 2023’s 4.27 million units, when post-pandemic recovery efforts were still underway, and only exceeded 2020’s 3.016 million units. Pre-pandemic figures typically surpassed 5 million units.

Dialectically, March offered slight relief compared to the quarter as a whole: while falling short of the CPCA’s 1.7 million-unit forecast, it outperformed March 2020, 2022, and 2023, nearing March 2024 levels.

Why did the decline accelerate in January-February but ease in March?

On one hand, local subsidy policies were rolled out in February-March. On the other, the replacement of fuel-powered vehicles by NEVs played a role.

Traditionally, January-February coincide with the Lunar New Year, when “buying a car for the holidays” drove demand, and cold weather favored fuel-powered vehicles. After NEVs captured half the market, this seasonal surge naturally faded.

Specific data shows NEV retail sales hit 784,000 units in March, down 21% year-on-year; Q1 totaled 1.844 million units, a 24% plunge. NEV penetration stood at 47.3%, down sharply from Q4 2025’s peak of over 50%. This suggests the tax exemption policy’s 2025 exit triggered far stronger-than-expected preemptive consumer spending. In February, BEV retail sales dropped 35%, PHEVs 31%, and ERVs 16%—a full-scale retreat.

For major automakers, many “sales pillars” faced product refresh cycles.

BYD, a frequent champion over the past five years, delayed 2026 product refreshes to build momentum for “flash charging” and second-gen blade batteries. Huawei-empowered high-end NEV brands also saw potential buyers awaiting mass production of 896-line LiDAR.

The wholesale side fared no better. Q1 wholesale volumes hit 5.813 million units, down 8% year-on-year. March wholesale reached 2.32 million units, a 4% decline. Though the final week saw 6% year-on-year growth, this stemmed from quarter-end push rather than demand reversal.

More alarmingly, this downturn reflects a global auto market slump, not just China.

Worldwide vehicle sales grew just 0.1% in January-February 2026, with China’s market shrinking 9% and its global share dropping from 35.4% in 2025 to 29.7%. While exports remained robust—1.55 million units in January-February, up 61%—domestic demand gaps persist.

02 Embrace the Pain: Profit Margins Under Pressure

Focusing solely on sales figures misses the adjustment’s true significance. The Q1 auto market’s keyword is not “collapse” but “rejuvenation.”

First, falling volumes but rising prices: structural optimization or forced price hikes?

A striking contrast emerges: Q1 retail volumes dropped 17%, yet average revenue per vehicle rose from RMB 333,000 year-on-year to RMB 369,000, adding RMB 36,000. Per-unit costs increased RMB 35,000, taxes RMB 4,000, and gross profit RMB 11,000 (down RMB 3,000 year-on-year), but the overall price level shifted upward.

What does this mean? Sold vehicles are pricier.

This isn’t automakers raising prices against the trend but the market structure self-optimizing. In 2025, unprecedented policy incentives and discounts—especially for low-priced compact cars under “trade-in” programs—drove explosive sales growth.

That was a classic “policy-driven market”—subsidy-fueled prosperity essentially predated future demand. In Q1 2026, as policies retreated, sales of these low-priced models collapsed, while mid-to-high-end models’ share rose. Thus, overall volumes fell but average prices climbed.

Think of it as shedding flabby fat—what remains is leaner but stronger.

Meanwhile, narrowing discounts signal an end to price wars.

Another positive sign: terminal discounts are easing. In 2025, price wars raged, with fuel-powered vehicle promotions hitting a record 24% and NEVs above 10%.

By 2026, price-cut models plummeted—just six models in February versus 21 a year earlier. NEV promotions stabilized around 10.4%, while fuel-powered vehicle discounts dipped slightly from 23.5% to 23.3%.

This isn’t automakers suddenly turning benevolent but a consensus forming against “involution.” When all realize endless price wars lead the industry to ruin, rationality becomes the only path.

In February, average price cuts for new NEV models stood at RMB 354,000, with an average reduction of RMB 48,000 (13.5%); fuel-powered vehicles averaged RMB 371,000, with RMB 46,000 cuts (12.5%). While significant, these reflect guide prices normalizing, not vicious competition.

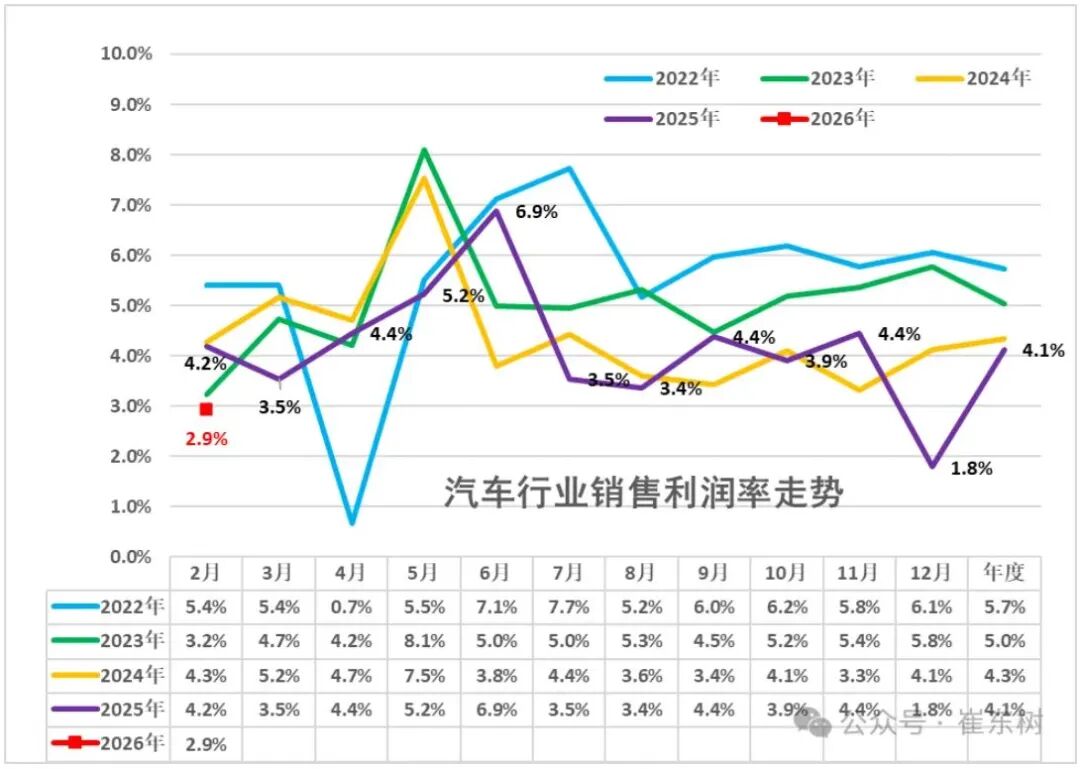

Behind these shifts lies a critical figure: 2.9% profit margins.

In January-February 2026, the auto industry earned RMB 1.4824 trillion in revenue, down 0.9% year-on-year; costs rose 0.2% to RMB 1.3147 trillion; profits crashed 30% to RMB 43.5 billion. Profit margins sank to 2.9%, compared to 5.8% for downstream industrial firms.

What does 2.9% mean? Even bank deposits offer higher returns. Non-ferrous metal mining boasts 39.4% margins, oil extraction 30.2%. In the real economy, miners and drillers earn tens of times more than automakers.

More worrying is the trend: 4.3% in 2024, 4.1% in 2025, and 2.9% in early 2026. Lithium carbonate prices doubled, commodities stayed high, and mid-to-downstream cost pressures mounted. Automakers are squeezed between raw material price hikes upstream and consumer hesitancy downstream, all while managing dealer survival crises.

This isn’t a “small profits but quick turnover” issue but a “even high turnover yields little profit” dilemma. When selling a car earns less than a smartphone, can the industry stay healthy?

03 A “Three-Step” Recovery Path

When will this “debt repayment” end? Is there hope for H2 2026?

The answer: short-term policy support, mid-term product innovation, long-term market consolidation.

Short-term: Local policies pick up the baton.

Media reports show local governments offered RMB 3,000–15,000 in subsidies in January-February, with efforts intensifying in late March.

On March 21, multiple Jiangsu cities launched new auto subsidies, with Nanjing, Suzhou, and Wuxi offering RMB 3,000–7,000 per vehicle.

Guangdong, Hunan, and Sichuan are preparing similar policies. Expect more local incentives this year.

These “local coupons” lack national policy scale but offer precision, propping up the market. Unlike last year, subsidies now target fuel-to-NEV swaps for mid-to-high emission vehicles, not blanket incentives. This shifts policy from “universal benefits” to “targeted guidance,” boosting efficiency and reducing side effects.

Mid-term: New growth drivers from segmented markets.

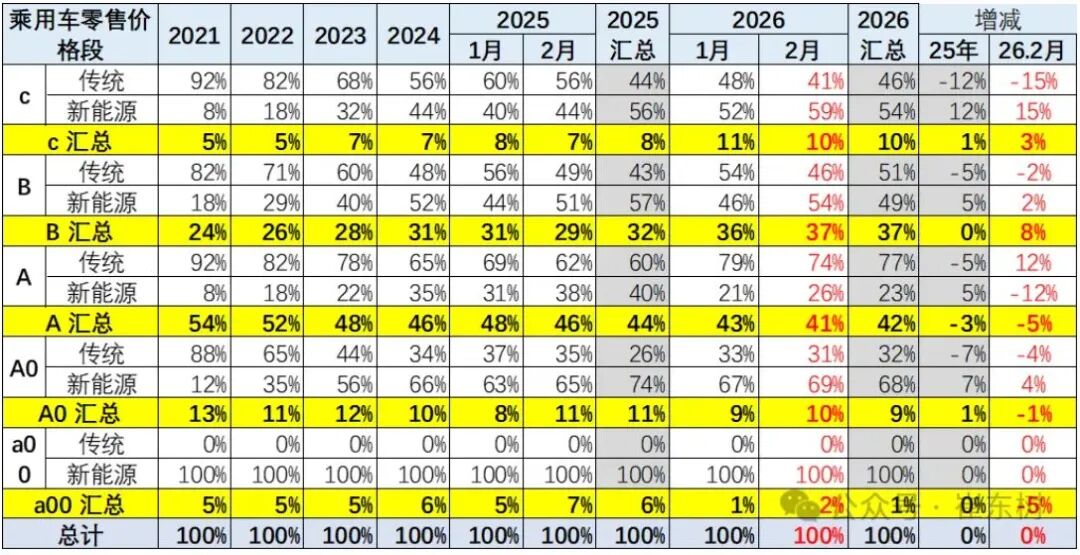

In January-February, price bands told a stark story: 200,000–300,000-yuan models barely declined, with NEVs in this range even growing—a sharp contrast to the 75% collapse in the sub-50,000-yuan segment.

The 200,000–300,000-yuan BEV segment emerges as an underrated blue ocean.

Why this band? Features like front trunks, 800V high-voltage platforms, and advanced driver-assistance systems (ADAS) are shifting from “premium exclusives” to “mainstream standards.” Consumers now get three-year-ago 400,000-yuan experiences for 200,000-plus yuan, with product leaps translating into purchase intent.

Take the Li Auto i6. Priced from RMB 249,800, this mid-size BEV SUV secured over 30,000 orders in its debut month, with deliveries surging. Its success is no accident—precise pricing, proven extended-range tech adapted to BEVs, and Li Auto’s brand reputation combined synergistically.

Another standout is the Denza Z9GT. Despite its higher (300,000-plus yuan) positioning, orders remain strong. This proves consumers will pay for compelling products. The 200,000–300,000-yuan BEV market is transforming from a “red ocean” of competition to a “blue ocean” of value. Whoever differentiates here will capture the next wave.

In the 400,000-yuan segment, NIO ES8 and Seres M8 BEVs have already proven this market’s “fertility.” Remember, “blue oceans” are dynamic—each era has its sweet spot.

Meanwhile, exports remain an unignorable second front.

If domestic demand is “debt repayment,” exports are “expansion.” China exported 1.55 million vehicles in January-February, up 61%; NEV exports surged 88% to 670,000 units.

From Brazil to the UK, Belgium, and the UAE, Chinese cars are conquering global markets. In February, BEVs accounted for 28% of exports, PHEVs 15%, HEVs 8%, and fuel-powered vehicles 37%—clear NEV momentum.

Lithium battery exports also impressed: USD 14.2 billion in January-February, up 46%, with price declines narrowing from 22% last year to 10%. This shows global reliance on China’s NEV supply chain is deepening, not waning.

The EU accounted for 43.1% of demand, up 2.6 percentage points year-on-year; the U.S. shrank to 9.7%. Amid geopolitical shadows, China’s NEV industry is pivoting from “single-market dependence” to a “diversified global footprint.”

04 Conclusion

The 17% Q1 decline marks a necessary “debt repayment” period for China’s auto market—repaying policy overreach, price wars, and low-quality competition. The process is painful, but only by purging the sores can the body regenerate.

We need not overanxiety about short-term sales. Rising average vehicle prices, narrowing discounts, local policy support, export surges, and the 200,000–300,000-yuan BEV boom matter more than raw sales figures.

Risks remain. At 2.9%, profit margins

-

![]()

AI Gives Volcano Engine a Chance to 'Change the Table'

-

![]()

A Smart Parking IPO Emerges in Xiamen with a 204% Surge on the First Day of Listing

-

![]()

Alibaba Exits Gaming Industry: A Strategic Move Forward?

-

![]()

New Car Model Faces Unprecedented Negative Campaign; Leapmotor Navigates Through Challenges Amid Profitability Concerns

-

![]()

Overnight Vanishing Act: 1.8 Trillion Gone! Silicon Giants Are Splurging While Carbon-Based Consumers Are Priced Out

-

![]()

2026 China GEO Industry Application Scenario Maturity and Supplier Selection Analysis Report (Part 1)

-

![]()

Fresh Air in Healthy Cabins Starts with a CO2 Sensor

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade