Changan's Zhu Huarong Reaches 'Li Shufu Moment'

04/22 2026

04/22 2026

522

522

Putting a Pause on Internal Friction

Is Zhu Huarong 'Borrowing' from Li Shufu's Playbook?

On April 21, Changan Automobile Group held a global strategy launch event. Zhu Huarong revealed after the event that the Avita and Shenlan brands would undergo strategic integration.

This plan is set to be implemented by the end of the year. The strategic integration will not affect brand independence but will focus more on technology and resource reciprocity, aiming to enhance efficiency. The goal is to create a mid-to-high-end brand matrix with 1.5 million units in shipments by 2030 (Avita targeting 500,000 units and Shenlan Automobile 1 million units).

This scenario seems familiar.

Previously, Geely's Lynk & Co and Zeekr underwent similar integration—under the 2024 "Taizhou Declaration," Geely Holding proposed five major initiatives, including "strategic focus and strategic integration," aimed at optimizing internal resources, reducing redundant investments, and resolving conflicts of interest. The merger of Zeekr and Lynk & Co was a key action to implement this strategy.

However, similar paths do not guarantee identical outcomes. After all, Shenlan is different from Lynk & Co, and Avita is not Zeekr.

01

Organizational Restructuring Driven by Sales Dilemmas

The merger of Avita and Shenlan brands can hardly be described as a "spur-of-the-moment" decision.

As a brand jointly created by Changan, Huawei, and CATL, Avita was born with a silver spoon in its mouth. Yet, this prince faced a rude awakening after entering 2026.

Affected by the phase-out of new energy vehicle purchase tax incentives and the collective sales push by automakers at the end of 2025, the beginning of 2026 has been tough for everyone. While setbacks can be a whetstone for success, Avita snapped when trying to prove its mettle.

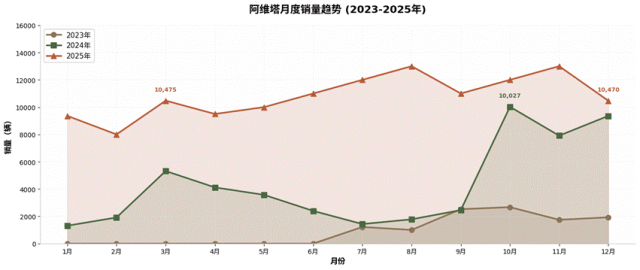

On April 2, Avita Technology released its March new vehicle delivery data. The figures showed that Avita delivered 5,016 new vehicles in March 2024, doubling from 2,457 units the previous month. From January to March 2024, Avita cumulatively delivered 14,532 new vehicles.

Notably, after hitting a delivery low of 1,432 units in July 2024, Avita began to surge in October of the same year. With the launch of the Avita 07 equipped with Huawei's ADS 3.0 intelligent driving system, monthly sales exploded to 10,027 units, breaking the 10,000-unit mark for the first time.

This event marked Avita's official entry into the scaling (scaled) development stage. After entering 2025, Avita maintained sales of over 10,000 units for 10 consecutive months, surpassing 120,000 units for the full year, solidifying its brand growth trajectory.

This seemingly strong momentum came to an abrupt halt in 2026.

Regarding the sharp decline in sales, a dealer in the Guangdong region revealed to Chaojiaojv: "Avita is a classic case of 'having no weaknesses but also no strengths.' Changan's driving control, Huawei's intelligent driving, and CATL's batteries are all competent. But we're no longer in an era where people buy cars based on ambient lighting and styling. In the inventory (mature) market, it's about hard power. Stuck in the middle, it's naturally hard to sell."

Besides its mediocre hard power, Avita still suffers from the inconsistent pricing of 4S stores reminiscent of the fuel car era.

A salesperson at a Shenzhen 4S store mentioned that sales have nearly halved in recent months. Now, reservations come with an 8,000-yuan discount on top of existing promotions, and immediate orders can even get an additional 2,000 yuan, totaling a 10,000-yuan reduction. This stands in stark contrast to the direct-sales models of NIO and Zeekr.

Regardless of the reasons, Avita showed clear signs of falling behind in the first quarter. If annual sales are extrapolated from Q1 figures, expected shipments would be less than 60,000 units, unbefitting of a "flagship" new energy brand from an established fuel car company. This may have been the trigger for the brand merger.

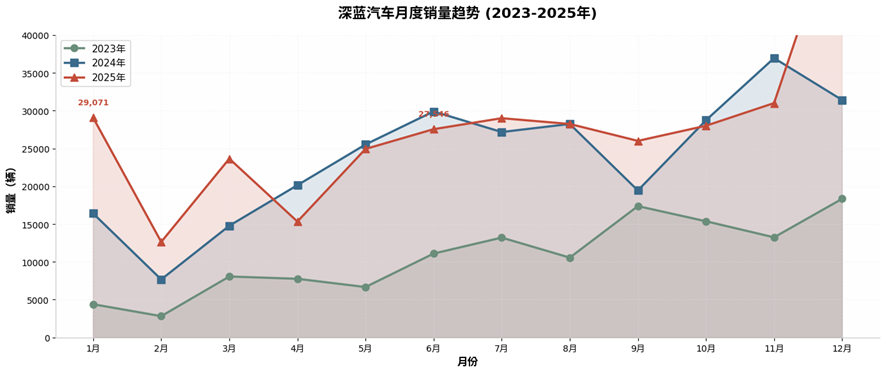

Shifting focus to Avita's sibling brand, the mass-market-oriented Shenlan, reveals a more prosperous situation.

Shenlan is a pure electric brand independently launched by Changan Automobile in 2022, targeting the mainstream mass market with intelligent electric vehicles priced between 150,000 and 300,000 yuan.

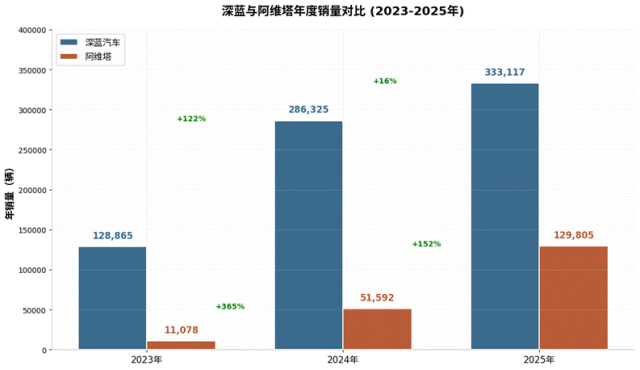

In 2023, Shenlan delivered a total of 136,900 units, with the SL03 contributing the majority. In 2024, with the launch of SUV models like the S7, Shenlan's sales rapidly grew to 286,300 units, a 122% YoY increase.

In 2025, Shenlan further expanded its product lineup, reaching 333,100 units in annual sales, a 16% YoY increase, becoming the core sales pillar of Changan's new energy sector.

From a revenue perspective, Shenlan achieved 50.24 billion yuan in operating income in 2025, a 35.0% YoY increase, growing into one of Changan's most important business units ahead of Avita.

Thus, the merger of the two brands becomes understandable. Shenlan has already achieved scale, and feeding its established channels, supply chain, and cost control capabilities back to the climbing Avita is a pragmatic choice for Changan at present.

Moreover, the price bands of these two sibling brands are distinct. Shenlan's main models are concentrated in the 150,000-250,000 yuan range, capturing market share through a cost-effectiveness strategy. Avita, on the other hand, focuses on the high-end market priced between 250,000 and 400,000 yuan, with Huawei's intelligent driving and emotional design as its core selling points.

This differentiated positioning was the original intent of Changan's "dual-brand" strategy but also laid the groundwork for subsequent integration. The two brands increasingly overlap in technology platforms, supply chains, and channel networks.

However, is Avita's precipitous sales decline truly due to a lack of support from Shenlan, despite Changan's full backing? What can Changan Automobile learn from the merger of Zeekr and Lynk & Co?

02

Brand Merger: A Temporary Fix, Not a Cure

The merger of Avita and Shenlan may give Avita a sales boost, as demonstrated by Zeekr and Lynk & Co.

In November 2024, Geely announced equity optimization for Zeekr and Lynk & Co; the equity transfer was completed in February 2025, with Zeekr holding a 51% stake in Lynk & Co, formally establishing the Zeekr Technology Group. The entire process took less than three months, showcasing Geely's efficient decision-making and execution capabilities.

The core objectives of Zeekr's merger with Lynk & Co can be summarized as "three integrations": integrated management to reduce operational costs, collaborative R&D to enhance technical efficiency, and differentiated positioning to avoid internal competition. Zeekr focuses on the high-end pure electric market, while Lynk & Co targets the mid-range new energy market, forming a clear brand hierarchy.

From an operational perspective, the effects of the Zeekr + Lynk & Co merger have been remarkable.

In terms of sales, the Zeekr Technology Group delivered a cumulative 245,000 units in the first half of 2025, a 14.5% YoY increase. Zeekr brand sales reached 134,000 units (+56% YoY), while Lynk & Co brand sales were 111,000 units (-14% YoY), highlighting the combined scale effect. Financially, Zeekr Technology achieved 35.5 billion yuan in revenue in Q2 2025, a 54% YoY increase, and turned operating profit positive for the first time in a single quarter.

Deeper efficiency gains are evident in R&D and management. Post-merger, R&D investment savings reached 10-20%, with the R&D expense ratio dropping from 11% to 6%. The number of organizational units decreased by 30%, and management efficiency improved by over 20%.

This is precisely what Shenlan and Avita lack.

Shenlan and Avita maintain separate R&D teams, technology platforms, and supply chain systems. Shenlan focuses on the EPA1 platform, while Avita is based on the CHN platform, leading to redundant R&D investments and a lack of synergy.

Simultaneously, the two brands have built independent sales and service networks, resulting in low channel investment return rates. This, in turn, leads to a decline in channel quality, as evidenced by the inconsistent pricing across multiple stores mentioned earlier.

Data shows that as of 2025, Changan's new energy channels exceeded 2,500, but the average sales per store were far below industry benchmarks.

It is foreseeable that even if the merger fails to boost sales, related operating expenses (SG&A) will see significant optimization in the short term.

However, Avita's issues may not lie in R&D or sales channels.

Selling cars ultimately comes down to product strength. A vehicle's success hinges on its product appeal; channels, marketing, and branding merely add icing on the cake. Without product strength, everything else is baseless.

Take the Li Auto L6 as an example. Its immediate success upon launch wasn't due to impressive specs but because it truly understood users—either delivering ultimate space and comfort for family travel or offering tech and cost-effectiveness that resonates with young buyers. Consumers' hard-earned money supports brands that "solve problems," not just those with "top-tier suppliers."

In contrast, Avita's product logic has always felt like a "self-indulgent" monologue. Unique styling, sophisticated ambient lighting, and Huawei's intelligent driving halo may shine brightly in PPTs but struggle to seal the deal in real purchasing scenarios.

Changan's leadership is not unaware of the issues, but performance pressures necessitate immediate actions to stabilize the market.

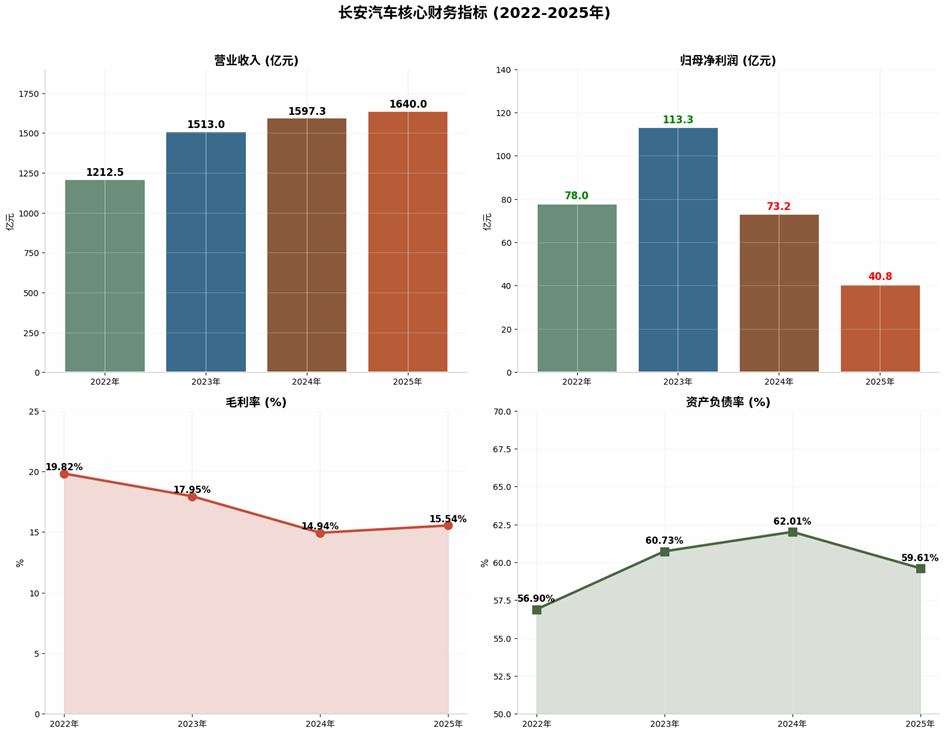

Financially, Changan Automobile reported 159.733 billion yuan in revenue in 2024, a 5.58% YoY increase. While new energy models contributed an increasing share of revenue, the new energy segment remained unprofitable overall.

In 2024, the Shenlan brand incurred a loss of 1.572 billion yuan, while Avita lost 4.018 billion yuan, with a combined loss of 5.590 billion yuan, becoming the primary drag on the parent company's profitability.

In 2025, while the company sold more cars, the boost to revenue and gross margin was limited. Revenue growth slowed significantly, gross margin only slightly rebounded after hitting recent lows, and net profit attributable to shareholders even reached new recent lows.

With poor performance and the flagship brand underperforming, inaction was not an option. Thus, Zhu Huarong took the path already traveled by Zeekr and Lynk & Co, which Avita and Shenlan were originally expected to follow in the future, and accelerated it to 2026.

However, this merger is ultimately just organizational surgery—it can address costs but not product strength.

Zhu Huarong may be "borrowing" from Li Shufu's resource integration and efficiency compression tactics, but the underlying logic behind Zeekr and Lynk & Co's post-merger success lies in their lineup of competitive products.

If Avita's product definition remains stagnant, merging the two brands will merely combine two challenges into a larger one, potentially even impacting Shenlan's development.

Fortunately, Avita has a strong foundation. After all, Changan's manufacturing system, Huawei's intelligent driving capabilities, and CATL's battery technology are all industry-leading. What Avita lacks is not hardware but a product logic truly centered on user needs.

Last year, Xpeng soared from the "ICU" to the "KTV" with a single MONA M03 model, proving that in the new energy market, hitting user pain points with one model can turn the tide in just a quarter.

If Avita can translate its technical reserves into user-centric language, its own version of the M03 may not be far off.

- END -

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’