Sanhua Intelligent Controls: When Will Automotive Parts Rebound and Robots See Their 'Midsummer'?

05/09 2026

05/09 2026

546

546

On the evening of April 29 (Beijing Time), Sanhua Intelligent Controls (2050.HK) released its Q1 2026 earnings report. While overall performance slightly missed expectations, the return to positive revenue growth was primarily disrupted by exchange rates and non-recurring gains/losses:

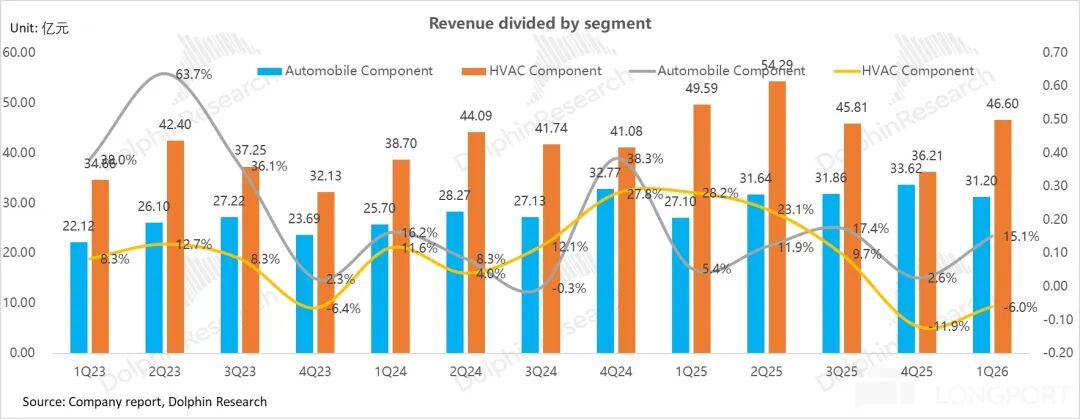

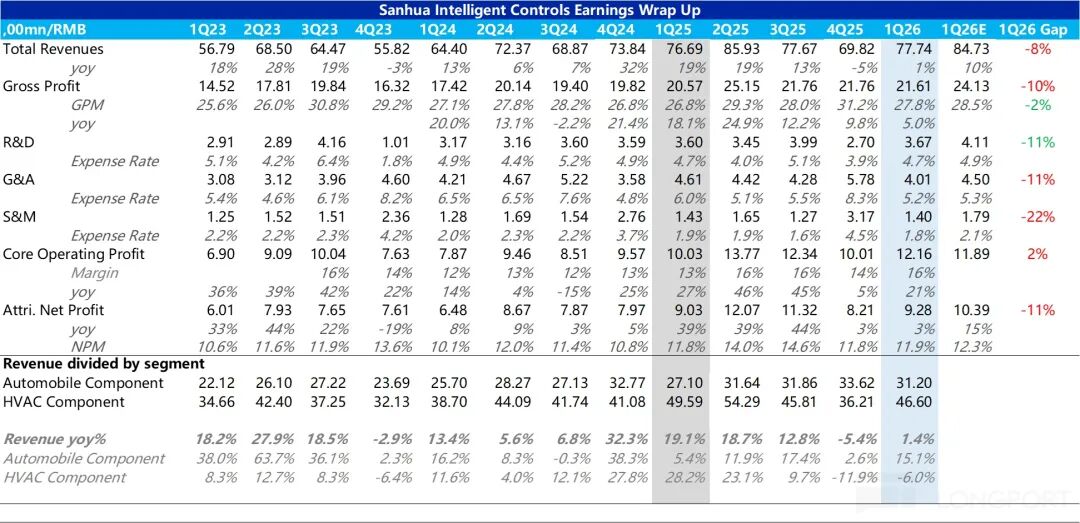

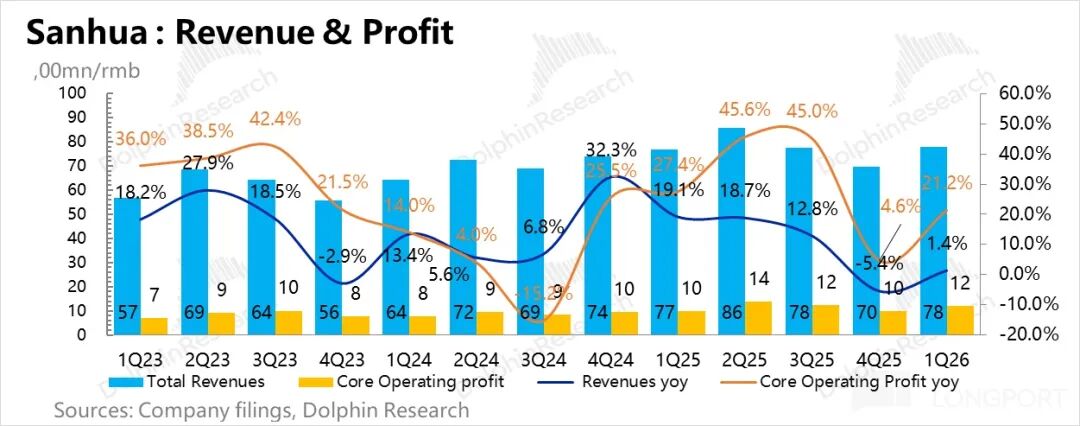

1. Q1 revenue finally returned to positive growth, with the automotive parts business's better-than-expected performance being the main driver: Sanhua's Q1 revenue reached RMB 7.77 billion, up 1% year-on-year, barely escaping the negative growth trap of the previous quarter, mainly due to the pull from automotive parts revenue. A breakdown shows:

① Automotive parts revenue exceeded expectations and was the main reason for the revenue turnaround: Revenue from this business segment reached approximately RMB 3.12 billion this quarter, achieving double-digit growth (around 15%) year-on-year. Against the backdrop of Q1 traditionally being a low season, the phase-out of purchase tax incentives for new energy vehicles (NEVs) led to a 5% year-on-year decline in overall NEV industry growth, and the combined sales of Sanhua's top two core automotive customers (BYD, Tesla) fell 21% year-on-year. Despite this, Sanhua achieved counter-trend growth, primarily due to:

a. Strong growth in China's NEV exports: The European energy crisis and the reinstatement of electric vehicle subsidies (€3,000-6,000 per vehicle) drove export demand. China's NEV passenger car exports reached 640,000 units in Q1, up 14.8% year-on-year.

b. Continuously diversifying customer base: The revenue share from major customers continued to decline, now at 20%-25%, while contributions from domestic new forces such as Xiaomi, Leapmotor, Geely, and Li Auto continuously improve (continued to increase).

② The refrigeration business once again dragged on performance: Refrigeration revenue reached approximately RMB 4.66 billion this quarter, down 6% year-on-year, marking the second consecutive quarter of negative growth. Reasons for the decline include:

a. High base effect: Q1 2025 saw elevated sales ahead of U.S. tariff hikes and peak national subsidies, creating a high comparison base.

b. Sluggish overseas markets: While China's total home appliance exports turned positive year-on-year in Q1, Sanhua's overseas refrigeration business underperformed. The company attributed this to weak consumption in the U.S. market due to extreme weather but guided for a rebound in the U.S. market in May.

c. Domestic subsidy phase-out: The 2026 national subsidy policy tightened significantly, covering only first-tier energy efficiency products, with the subsidy ratio dropping from 20% to 15% and the per-unit cap falling from RMB 2,000 to RMB 1,500, resulting in roughly flat year-on-year domestic home appliance retail sales.

However, the company guided for a return to growth in the refrigeration segment in Q2, primarily due to a. growth in North American business volume and b. domestic stimulus policies such as trade-in subsidies boosting internal circulation. Additionally, new product rollouts this year will gradually contribute incremental growth.

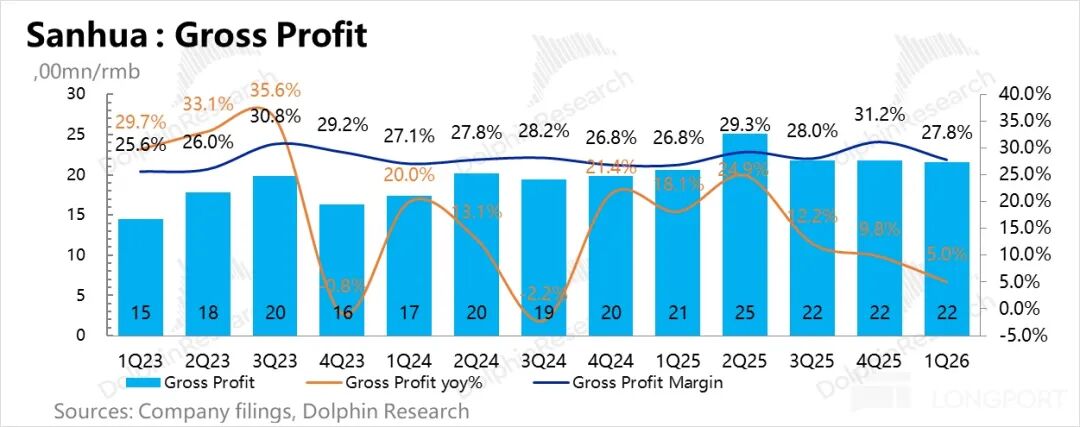

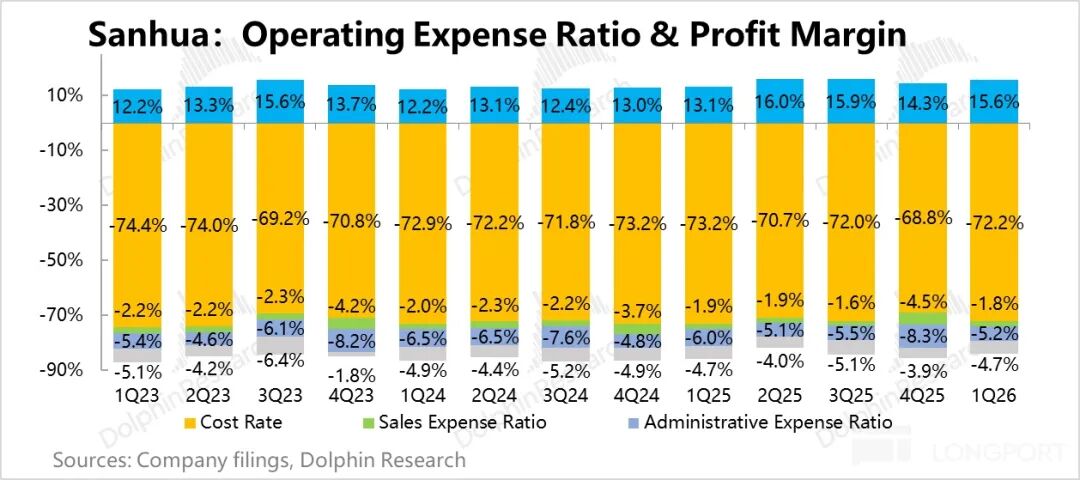

2. Gross margin declined quarter-over-quarter: Q1 gross margin was approximately 27.8%, down 3.4 percentage points from Q4 last year and below market expectations of 28.5%. The core reason for the decline lies in structural changes across business segments and differences in cost pass-through:

① The automotive parts segment was the primary driver of the gross margin decline: As aluminum—the core raw material for this segment—rose in Q1, and given the automotive parts industry's limited use of aluminum price linkage mechanisms (fixed pricing dominates), the company primarily hedged cost pressures through hedging.

However, hedging involves time lags. During quarters of rapid aluminum price increases, cost pressures are difficult to fully absorb in the same quarter, creating short-term pressure on gross margins.

② While copper price linkage in the refrigeration segment was effective, high-margin overseas business dragged significantly: The refrigeration segment's primary raw material, copper, generally employs price linkage with downstream customers (90% coverage), allowing relatively smooth cost pass-through. However, the segment's gross margin decline stemmed primarily from a shrinking revenue share in high-margin overseas markets (e.g., the U.S.) due to weak demand, which passively increased the proportion of low-margin domestic business, pulling down the segment's overall gross margin.

③ Additionally, the high Q4 gross margin base from the previous year impacted quarter-over-quarter figures. This was mainly due to Q4's rapid copper price surge (reaching RMB 100,000 per ton by year-end, with a quarterly average of RMB 87,000), where the company's sales pricing reacted quickly, while cost-end lags due to inventory valuation created an exceptionally strong Q4 gross profit performance.

④ USD depreciation also dragged on gross margins.

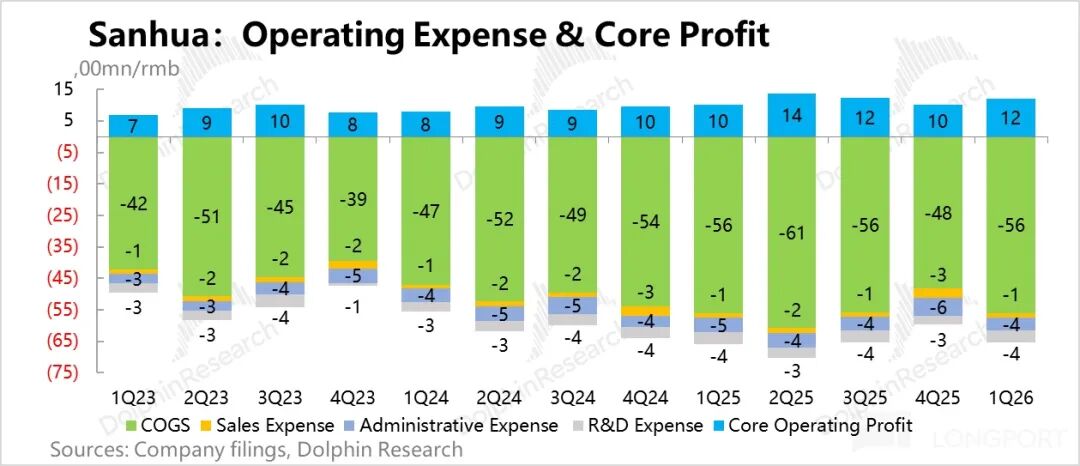

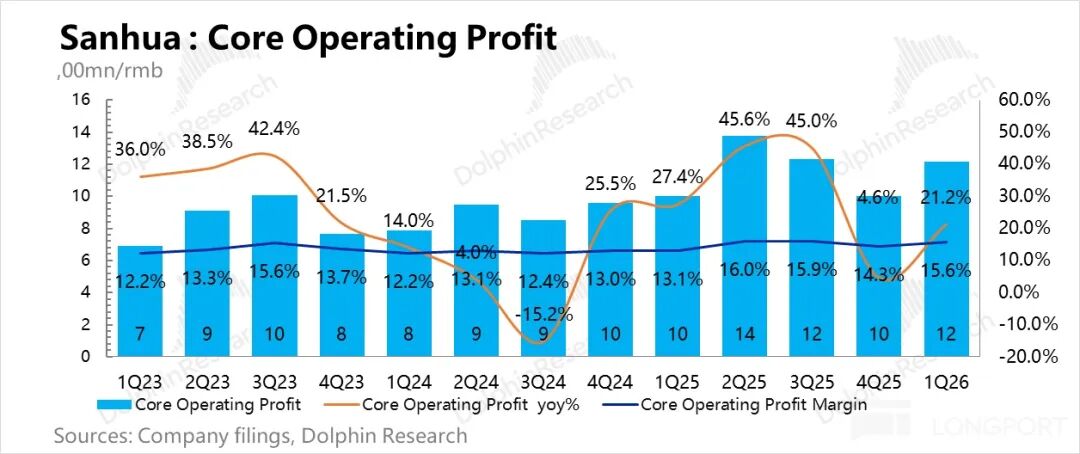

3. Operating profit exceeded expectations, primarily due to effective cost control: Q1 core operating profit reached RMB 1.22 billion. Despite sluggish revenue growth, the company significantly reduced selling and administrative expenses, driving core operating profit up 21% year-on-year and lifting the profit margin by 1.3 percentage points sequentially to 16%.

The better-than-expected core operating profit growth was mainly due to the company's strict control over selling and administrative expenses, which totaled just RMB 540 million in Q1, down 39.5% from RMB 900 million in the previous quarter. This was partly due to the high base in Q4 last year, when management accrued bonuses and increased new project development spending, and partly due to the company's shift from "rapid expansion" to "refined operations," strengthening expense control and optimization.

4. Net profit was pressured by the refrigeration segment, while automotive parts became the growth engine: Q1 net profit reached RMB 930 million, up just 3% year-on-year, primarily disrupted by exchange rate fluctuations and non-recurring gains/losses. Excluding these items, core net profit was RMB 990 million, up 15.5% year-on-year. A breakdown shows:

Refrigeration & intelligent control segment: Net profit in this segment fell approximately 12% year-on-year, primarily dragged down by revenue (down 6% year-on-year). While gross margin improved year-on-year (up 1.6 percentage points to 28%) due to the copper price linkage mechanism, the high base and weak overseas demand led to revenue declines, pressuring absolute profit levels.

Automotive parts segment: Net profit in this segment grew approximately 23% year-on-year, with profitability standing out amid double-digit revenue growth. While gross margin remained roughly stable year-on-year (aluminum price increases offset by internal efficiency gains), robust revenue growth (driven by China's NEV exports and customer diversification) remained the core driver of profit growth.

Dolphin Research's View:

Overall, Sanhua Intelligent Controls' Q1 2026 performance was mediocre. While reported net profit fell short of market expectations, the company escaped the "negative growth" trap of Q4 last year, with overall revenue returning to positive growth driven by automotive parts.

Despite exchange rate and non-recurring item disruptions, reported net profit grew just ~3% year-on-year. However, through cost reduction and efficiency gains, core operating profit (excluding exchange rates and non-recurring items) grew ~21% year-on-year, returning to normal growth trajectory.

While rising commodity costs (e.g., copper, aluminum) had raised concerns about Q1 gross margins, Sanhua maintained relatively stable margins through copper price linkage mechanisms, hedging, and global capacity layout (capacity deployment).

At the earnings call, management conveyed several key guidance points, adopting a generally optimistic tone:

a. Reiterated full-year net profit growth guidance of ~15% year-on-year. Given high macro and geopolitical uncertainties, the company employs rolling planning, implying potential acceleration in profit growth in the coming quarters.

b. Full-year guidance remains unchanged. Management indicated stable Q2 performance, with growth momentum skewed toward the second half of the year.

From a profit release perspective, management noted that Q2 would see steady rather than sharp rebound growth, primarily due to high bases and macro uncertainties, but sequential improvement is expected. In Q2, the refrigeration business's North American market is expected to warm up from May, coupled with domestic policy support such as trade-in programs, likely improving refrigeration performance. Meanwhile, the AIDC business will advance orderly throughout the year, providing clear incremental growth.

For the full year, automotive parts remain the core growth engine, while refrigeration is expected to remain relatively weak due to high base digestion and uneven U.S. consumption. If the aforementioned variables stabilize, the certainty of accelerated growth in H2 2026 will increase.

c. Sanhua's profit resilience remains stable: The refrigeration segment's copper price linkage mechanism, ongoing cost-reduction measures, and hedging/price-locking policies for other raw materials continue to support stable profitability.

For Sanhua's stock price, much depends on progress in its "imagination" businesses:

(1) Humanoid robots (bionic robots): The company did not separately disclose revenue from this business, aligning with market expectations. As Tesla's Optimus Gen3 has not yet finalized its design or entered mass production, most hardware technology routes remain iterative. At this stage, Sanhua's role is to collaborate with core customers on R&D and sample delivery.

Industry chain information indicates that Sanhua remains one of the strongest potential Tier 1 suppliers for Optimus's joint actuators and assemblies, with the core bottleneck lying in the customer's own production and launch timeline.

The company clarified that during this early "0 to 1" validation phase, its strategy is to concentrate resources on a few benchmark customers for deep binding and joint growth. Operationally, Sanhua is continuously investing, with its humanoid robot-related team expanding to ~200-300 people, and overseas factory construction proceeding as planned, focusing on actuator series and internal core components (including dexterous hands and body actuators).

Notably, Tesla's Optimus Gen3 launch and mass production timeline expectations have been revised again. The latest guidance suggests mass production will start in summer 2026 (~July-August), later than the previously expected 26Q1, which may temporarily suppress sector sentiment and the stock price.

However, the industry-wide mass production trend remains unchanged, with relevant PPAs (Production Preparation Agreements) beginning to land. As Sanhua has a clear position in actuators—the highest-value segment—it will be a core beneficiary once mass production begins.

Regarding production site diversification, the company is actively expanding overseas actuator capacity in Thailand, Mexico, and other locations to preemptively address trade barrier risks in the future mass production phase. We recommend closely monitoring progress in these capacities.

(2) Data center liquid cooling: The company has repeatedly emphasized progress in data center-related projects in its earnings reports. In 2025, revenue from data center liquid cooling reached approximately RMB 1.4 billion, with combined revenue from energy storage thermal management at ~RMB 2 billion (mostly included in the refrigeration segment and not separately disclosed).

AIDC/liquid cooling remains the most quantifiable short-term growth driver. The company maintains its 2026 full-year growth target of 50%-100% and expects this to contribute ~3-5 percentage points to total revenue growth. While its current scale's contribution to revenue growth remains limited, the growth rate is impressive, with significant strategic importance.

AIDC and energy storage thermal management products now cover multiple business units, including Microchannel, Commercial, and Xiantu Electronics, with dedicated teams driving progress. In North America, the company collaborates strongly with leading system integrators like Trane, fully benefiting from robust U.S. data center construction demand. In China, despite the industry being in its early stages, the company has established active partnerships with frontline integrators like Vertiv and Inspur.

A more detailed value analysis has been published in the Longbridge App's 「Dynamic-Depth」 section under the same article title.

However, it must be emphasized that:

a. The industry's overall mass production trend remains unchanged, with relevant PPAs beginning to land and supply chain preparations advancing.

b. The sector has already undergone a relatively deep correction, partially reflecting some pessimistic expectations.

c. Sanhua's strong position in actuators—the highest-value segment—remains clear. Once mass production truly begins, its status as a core beneficiary will not change.

Thus, while short-term stock price pressure exists objectively, if mass production accelerates and profits gradually release in H2 2026 (when the domestic refrigeration industry's high base issue no longer exists), the potential upside remains substantial. Investors could gradually focus on the official launch of Optimus V3 and PPA progress starting in Q2, which will be key catalysts for sentiment recovery.

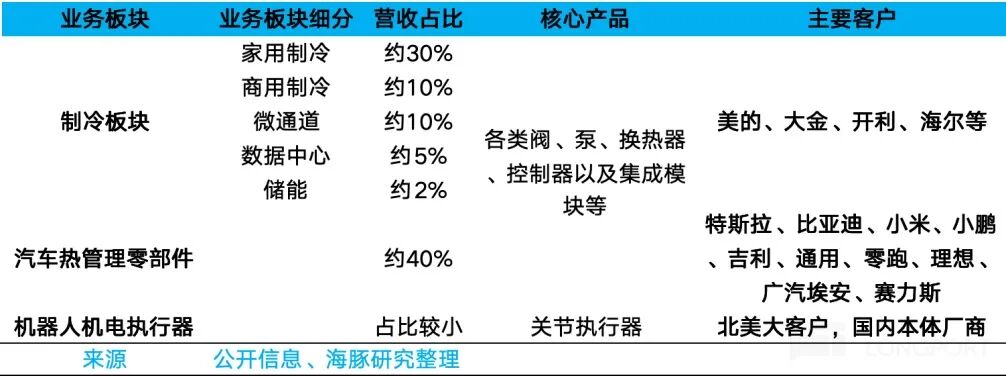

Overview of Sanhua Intelligent Controls' Main Businesses

Sanhua Intelligent Controls' business primarily consists of two major segments: refrigeration components and automotive parts.

The refrigeration components segment primarily serves refrigerators and air conditioners, representing a relatively mature and stable industry. However, certain sub-segments, such as commercial refrigeration in overseas markets, still have room for further penetration. Beyond this, the most market-focused area is the application of its valves, pumps, and other products in data center liquid cooling and energy storage thermal management.

The automotive parts segment is mainly used in thermal management for new energy passenger vehicles, with Tesla as its largest customer, though domestic customers like BYD are rapidly increasing their share. Benefiting from rising thermal management demands in NEVs, the per-vehicle value remains likely to increase, though it is temporarily affected by fluctuations in major customers' sales volumes.

Beyond these segments, the company has added a third major business: strategic emerging industries, focusing on data centers, energy storage, and bionic robots. Data centers and energy storage primarily supply thermal management components, generating ~RMB 2 billion in revenue in 2025. The robot segment mainly focuses on joint actuators. Given the industry is still in its early stages, revenue contributions are expected to be limited, but as one of the first companies to engage with North American major customers and possessing leading technical and production capabilities, it remains one of the most market-focused business segments.

For analyses of the company's businesses, see "Sanhua Intelligent Controls: An Unassuming Business, How Does It Always Catch the Wind?" and "Sanhua: In the AI Robot Era, Will the 'Seasoned Crossover Player' Have the Last Laugh?".

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general viewing and data reference by users of Dolphin Research and its affiliated entities. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with an independent professional advisor before making any investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibility or loss that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are provided for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, solicitation, or recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person or resident in any jurisdiction where such distribution, publication, provision, or use would be contrary to applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements in that jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to any other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Zhuo Li Han Guang Officially Competes in the 2026 Optical Industry Annual Innovation Product Awards

-

![]()

China Raytronics Secures Nomination for 2026 Optics Industry High-Growth Enterprise Award

-

![]()

A Regular and Periodic Exchange Mechanism to Be Set Up! North Opto-electronics and Costar Forge New Avenues for Intelligent Integration

-

![]()

After Joining NVIDIA’s Core Supply Chain, This Optical Company Secures Fresh Funding!

-

![]()

Quarterly Report | All-Channel Online Laptop Sales in China Plummet by 19% in Q1 2026; Lenovo, ASUS, Apple, HP, and Mechrevo Dominate with 80% Market Share

-

![]()

Who’s Encircling and Attacking OpenAI? A New Tech Giant War Has Begun

-

![]()

AI Application Integration Surges Eightfold in a Year! Your Job Might Be Vanishing Without Notice

-

![]()

Mobile Phone Manufacturers: The Time Has Come to Unveil True AI Phones