Mixed Fortunes: The Ongoing Transformation of the Automotive Industry's Value Landscape

05/27 2026

05/27 2026

550

550

Introduction | Overview

In recent years, the domestic automotive market has witnessed heightened competition, with price wars becoming increasingly prevalent. Recently, leading automakers such as Tesla, BYD, Xiaomi, NIO, and XPeng have adjusted their pricing strategies, either by directly increasing official prices or by reducing purchase incentives and financial benefits. The price war for New Energy Vehicles (NEVs) has come to an abrupt halt, and industry competition has officially transitioned from a focus on low prices to a focus on value. What are the reasons behind the concentrated price increases by automakers?

This article is produced by | Heyan Yueche Studio

Written by | Zhang Dachuan

Edited by | He Zi

Full text: 2,619 characters

Reading time: 4 minutes

Recently, the domestic NEV market has experienced a wave of price hikes, with over 15 mainstream automakers simultaneously raising prices or reducing benefits. The industry's pricing trend has shifted from prioritizing volume at the expense of price to emphasizing value appreciation.

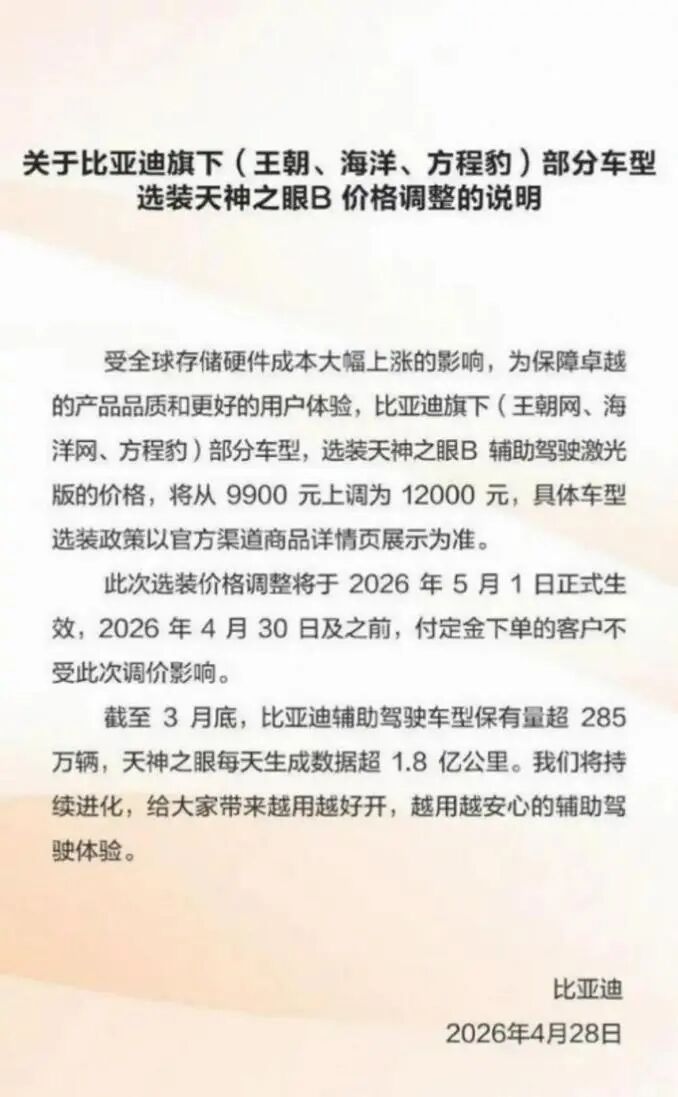

Among these, Tesla has implemented the most significant price increases: starting May 1, the Model Y Long Range version increased by RMB 18,000, and the Performance version by RMB 20,000, marking the highest single-model price hike in this wave. Simultaneously, Tesla tightened its financial interest-free policy, increasing the implicit cost of purchasing. BYD adopted a differentiated approach to price adjustments, announcing on April 28 that starting May 1, the optional package for the "Divine Eye B" assisted driving laser version would increase from RMB 9,900 to RMB 12,000, a RMB 2,100 increase. The Xiaomi SU7 saw across-the-board price hikes of RMB 4,000, covering the Standard, Pro, and Max versions. NIO adjusted prices for popular models such as the 2026 ES6 and ET5 on May 10, with increases ranging from RMB 5,000 to RMB 10,000, and canceled the basic free battery swap benefits, further raising long-term ownership costs for users. By late May, this round of price hikes had encompassed mainstream independent brands, new forces, and some joint-venture NEV models, with both overt and covert increases, indicating a clear pricing trend in the domestic NEV market.

△ Over the past two months, the domestic NEV market has seen a concentrated wave of price hikes.

Why are NEVs raising prices?

The current round of NEV price hikes is not a short-term marketing ploy but an inevitable consequence of dwindling industry profits and soaring costs across the board.

Data indicates that the overall profit margin of the domestic automotive industry in the first two months of 2026 was only 2.9%, recovering slightly to 3.2% in the first quarter, far below the historical average of 6% in the manufacturing sector. Over 70% of automakers are operating at a loss or with meager profits. The long-standing strategy of prioritizing volume at the expense of price has pushed profit margins to their limits, making it difficult for automakers to absorb cost fluctuations in the supply chain alone. Price hikes have become inevitable, and in the first half of 2026, multiple cost pressures erupted simultaneously, leading to the current wave of price increases.

The primary driver of these hikes is the soaring price of raw materials for power batteries. The price of lithium carbonate, a core battery material, surged from RMB 75,000 per ton in July 2025 to nearly RMB 200,000 per ton in May 2026, an increase of over 167%. Power batteries account for 30%–60% of a vehicle's cost, and the lithium price increase alone has directly raised battery costs per vehicle by RMB 3,000–6,000, completely eroding automakers' already thin profit margins.

△ In less than a year, lithium ore prices have surged by 167%.

The second major factor is the uncontrolled rise in automotive-grade chip prices, including memory chips. In 2026, global AI computing power construction surged, with AI data centers prioritizing advanced manufacturing capacity, severely squeezing chip supplies for the automotive industry. Data shows that automotive-grade DRAM prices have risen by about 180% in the past three months, with DDR5 spot prices surging past 300%. UBS estimates that the storage chip price hikes alone have added RMB 3,000–7,000 to the cost of models equipped with intelligent driving systems. Models with higher intelligence levels are more severely impacted, with new forces and premium brands facing particular pressure.

△ Automotive-grade chip prices have surged uncontrollably.

External inflation and geopolitical conflicts have further amplified cost pressures. Since late February 2026, the escalation of the U.S.-Iran conflict has disrupted shipping in the Strait of Hormuz, driving up global energy and commodity prices. Raw material prices for vehicles, such as copper, aluminum, plastics, and rubber, combined with rising international logistics costs and labor expenses, have continued to push up vehicle manufacturing costs. Meanwhile, industry regulation and market logic are undergoing qualitative changes. Relevant national departments and industry associations have begun cracking down on "cutthroat price wars," explicitly opposing loss-leading strategies and vicious competition, and guiding the industry back to reasonable profit margins. The past model of relying on subsidies and losses to gain market share is no longer sustainable, and automakers must maintain reasonable pricing to sustain R&D investment and a healthy supply chain.

Fuel Vehicles Struggle to Halt Decline

While NEV prices steadily rise, the fuel vehicle market is mired in a pricing slump. Currently, domestic fuel vehicles generally offer discounts ranging from RMB 30,000 to RMB 100,000, with mainstream models averaging a 17.2% price reduction. Several luxury flagship models have seen price cuts exceeding RMB 300,000, an unprecedented level of market concessions.

Market sales data reflect this downturn, with fuel vehicle retail sales dropping 37.2% year-on-year in April, and market share shrinking to 38.6%. Only the Geely BinYue, a fuel vehicle, made it to the top ten sales list for the month. Industry inventory pressures remain high, with the overall inventory coefficient ranging between 1.8 and 2.0, well above the safety warning line of 1.5. Joint-venture brands face an even higher inventory coefficient of 2.24, with high inventory levels further driving normalization of price cuts and promotions.

△ In April's top ten sales list, only the Geely BinYue, a fuel vehicle, made the cut.

Multiple negative factors continue to squeeze the living space of fuel vehicles. Currently, the average price of 92-octane gasoline remains steady at RMB 8.2 per liter, making the annual ownership cost of a household fuel vehicle far exceed that of an equivalent electric vehicle. The industry's three-year average residual value has dropped to 46%, a significant decline from two years ago. Combined with the consumer psychology of "buying high, not low," over 60% of users are choosing to wait and see, further narrowing the market for fuel vehicles.

The pricing trends of these two vehicle types present a stark contrast, with NEVs seeing an average price increase of 5.8% due to rising lithium ore prices. Fuel vehicles, unaffected by fluctuations in mineral raw material costs and with intelligent configuration adoption rates below 30%—far lower than the over 80% for NEVs—lack the core support for price increases, leaving limited room for future price hikes.

Should You Buy a Fuel Vehicle or an NEV?

Both the price hikes for NEVs and the price cuts for fuel vehicles are temporary and time-sensitive.

If costs for lithium ore, battery raw materials, or chips decline later, NEV prices will likely follow suit. Conversely, with the implementation of new emission standards, the current level of discounts for fuel vehicles may not be sustainable in the future. Of course, in a market economy, supply and demand ultimately determine price trends. In the long run, if the issue of overcapacity in the domestic automotive industry is not resolved, automakers may still resort to price wars to survive and capture market share.

However, in the short term, the choice between an NEV and a fuel vehicle still depends on specific circumstances.

Currently, fuel vehicles are generally more cost-effective, especially for users with annual mileage below 10,000 kilometers or those lacking convenient charging options. For these users, a fuel vehicle is a more stable and hassle-free choice. However, it's important to note that once China implements the "China VII" emission standards, the residual value of current fuel vehicles may decline further.

△ Fuel vehicles still have a certain market demand.

For users with annual mileage exceeding 20,000 kilometers, NEVs offer a more significant advantage in ownership costs, with lower electricity and maintenance expenses compared to fuel vehicles. Additionally, with "equal rights for fuel and electric vehicles" becoming a trend in China, policies such as NEV purchase tax exemptions may gradually phase out. Therefore, purchasing an NEV during the current policy window could be a wise choice. However, the rapid technological iteration of NEVs and frequent new model releases may also impact residual values. Thus, when purchasing a vehicle, it's essential to consider usage scenarios, travel needs, and budget comprehensively.

△ For users with annual mileage exceeding 20,000 kilometers, NEVs offer a more significant advantage in ownership costs.

Commentary

The price hikes for NEVs and significant price cuts for fuel vehicles essentially reflect the structural differentiation as China's automotive industry enters a deep transformation phase. NEVs, still in their technological upgrading and industrial expansion stage, are influenced by battery, chip, and intelligence costs, resembling "tech products." In contrast, fuel vehicles are gradually entering an era of stock competition, forced to rely on heavy discounts to maintain sales amid rising NEV penetration and emission upgrade pressures. Behind this "oil-electric price war" lies the restructuring of the automotive industry's value system—traditional fuel vehicle technological barriers are being replaced by intelligence, battery technology, and supply chain capabilities. In the short term, fuel vehicles still hold a pricing advantage; in the long term, NEVs becoming the industry mainstream is an inevitable trend.

(This article is original to Heyan Yueche and may not be reproduced without authorization.)

Heyan Yueche is now available on the following platforms:

Tencent | Yiche.com | Chejiahao | Toutiao | Sina KanDian | Sohu Account

Xiaohongshu | Dayuhao | Sina Weibo | Yidian Zixun | Baijiahao

NetEase Account | Qiche Toutiao | Cheyouhao | Pacific Auto

-

![]()

Europe's Q1 Smartphone Market Shipments Revealed: Samsung Holds Firm at First Place, Honor Surges Over 60%

-

![]()

Mixed Fortunes: The Ongoing Transformation of the Automotive Industry's Value Landscape

-

![]()

Germany Launches Electric Vehicle Subsidy Applications, Chinese Automakers May Benefit

-

![]()

Struggling to Keep Pace with 618 in 2026? The Reality is More Intricate

-

![]()

JD May Be Cracking the Key Challenge of Physical AI

-

Computing Power Crisis: Four Major Forces Enter Token Service Market

-

![]()

Agnes AI Releases Three Core Multimodal Models: Text, Image, and Video

-

![]()

Tesla Abandoned Radar Five Years Ago; Now, China’s Market is on the Verge of Delivering Its Verdict