Li Auto Suffers 2.3 Billion Yuan Loss in Q1: Can the L8 Turn the Tide?

05/29 2026

05/29 2026

542

542

What's Ailing Li Auto?

Today, Li Auto released its Q1 2026 performance report, which left the market in a state of collective stunned silence.

On one hand, vehicle deliveries saw a slight uptick of 2.5%, propelling Li Auto back to the top of the sales charts for domestic new energy brands priced above 200,000 yuan. On the other hand, the company reported a staggering net loss of 2.3 billion yuan and a gross margin that was halved.

(Image Source: Li Auto)

Following the release of the financial results, Li Auto's U.S.-listed shares plummeted by more than 5% in pre-market trading!

(Image Source: East Money)

Today, amidst an intensifying price war in the new energy sector, the once most profitable new player is also navigating through its most challenging product transition phase.

(Image Source: ChatGPT)

(Image Source: ChatGPT)

This may mark the ugliest quarter for Li Auto's profitability since its public listing.

The financial report reveals that in Q1, Li Auto's total revenue reached 23 billion yuan, down 11.4% year-on-year and 20.1% quarter-on-quarter.

Core vehicle sales revenue stood at 21.5 billion yuan, marking a 12.7% year-on-year decline and a 21% quarter-on-quarter drop.

The most striking issue is the gross margin:

The overall gross margin took a nosedive from 20.5% in the same period last year to 7.9%, a direct decrease of 12.6 percentage points.

The vehicle gross margin was a mere 6.1%, 10.7 percentage points lower than the 16.8% recorded in Q4 last year.

A straightforward calculation: Last year in Q1, for every 100 yuan worth of cars sold, Li Auto could rake in nearly 16 yuan; this year in Q1, selling 100 yuan worth of cars only yields 6.1 yuan, almost selling at cost.

(Image Source: Generated by ChatGPT)

Why did sales revenue and gross profit take such a substantial hit?

The financial report states: "The decrease in vehicle sales revenue compared to Q1 2025 was primarily attributable to a lower average selling price resulting from a different product mix."

Li Auto's CTO, Li Tie, also commented in the financial report: "Our Q1 gross margin reflects the impact of user-centric delivery initiatives for the Li Auto i6, raw material price fluctuations, and the product transition cycle."

(Image Source: Li Auto)

In a nutshell: Product transitions + lower average product prices + supply chain fluctuations + delivery issues with the i6 series have had a quadruple impact.

Previously, the main L-series models were nearing the end of their lifecycle, with consumers holding out for the new generation and manufacturers clearing inventory.

The volume-selling i6, priced primarily in the 200,000-300,000 yuan market, was already priced lower than the L-series. Coupled with user compensation for the delayed release of the CATL version models earlier this year and subsequent investments to ensure supply, not only did total revenue decline, but the gross margin also contracted significantly.

For Li Auto, Q1 was arduous, but the company has maintained its composure. It is economizing where appropriate and continuing to invest where necessary without resorting to blind cost-cutting.

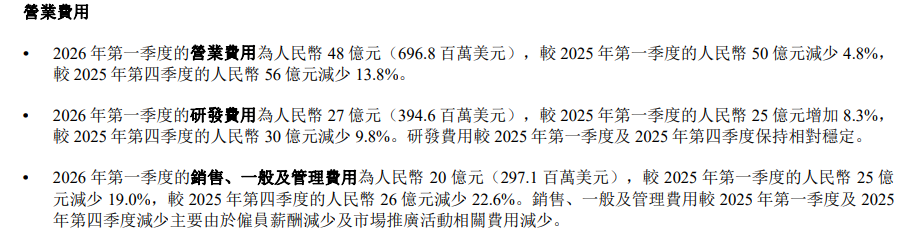

From Li Auto's operating expenses, it is evident that Q1 was indeed a cost-saving quarter. Total operating expenses amounted to 4.8 billion yuan, down 4.8% year-on-year and 13.8% quarter-on-quarter. Sales and administrative expenses decreased by 19%, from 2.5 billion yuan last year to 2 billion yuan, primarily due to optimized staff salaries and unnecessary marketing promotions.

However, R&D investment remained robust: Q1 R&D expenses were 2.7 billion yuan, up 8.3% year-on-year.

This investment was primarily directed towards self-developed chips and large models. The new L9, released in May, comes standard with the self-developed Mach M100 chip and Mach VLA large model, which are Li Auto's trump cards for distinguishing itself from competitors and establishing its tech brand image.

(Image Source: Li Auto)

Despite the significant losses in Q1, with a net outflow of 6.1 billion yuan from operating activities and a free cash flow of -7.4 billion yuan, Li Auto still boasted 94.3 billion yuan in cash reserves as of the end of March.

With ample cash on hand, there is no need for panic. A single quarter of losses is insufficient to derail Li Auto. In fact, the company can even afford to allocate 1 billion USD for share buybacks to bolster market confidence.

In reality, Li Auto's current losses are more indicative of a short-term setback rather than a sign of imminent peril or a life-and-death situation.

Throughout Q1, Li Auto delivered 95,000 vehicles, up slightly by 2.5% year-on-year, and sold 34,000 vehicles in April alone. The market still acknowledges the Li Auto brand and its products.

Had these challenges befallen a less financially robust brand, it might have faced dire consequences. However, for Li Auto, which remains relatively strong, these are more likely short-term pains. And change is already afoot.

In mid-May, the all-new Li Auto L9 was officially launched, and deliveries commenced, with the Ultra version priced at 459,800 yuan and the Livis version at 509,800 yuan, bringing the price back to the high-end segment above 450,000 yuan.

(Image Source: Generated by ChatGPT)

More significantly, the all-new Li Auto L8 is also slated for release. As the successor to the old L7, the L8 will become Li Auto's future flagship model, potentially driving a direct recovery in overall average selling price and gross margin.

According to Li Auto's financial guidance, Q2 deliveries are expected to range between 95,000 and 100,000 vehicles, with revenue projected between 24.1 and 25.4 billion yuan. While year-on-year declines are still anticipated, the short-term pressure has not yet abated.

However, for Li Auto, this pain is necessary. Rather than clinging to outdated models for quick profits, it is wiser to complete product and technological upgrades during this market adjustment period. After all, in the latter half of the new energy era, self-developed capabilities and high-end product strength are the true competitive advantages.

Now, the spotlight is on the market performance of the new L9 and L8. If these two models can sustain sales, Li Auto will likely rebound to profitability in the second half of the year. If not, the company may confront even stiffer challenges.

Li Auto Financial Report Automotive

Source: Leikeji

Image credits: 123RF Licensed Image Library Source: Leikeji

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building

-

![]()

Half Flock In, Half Flee Out: The Dual Dynamics of Singapore as an AI Hub