Xpeng in Turmoil! Q1 Sees Record-High Gross Margin, Yet Net Loss Soars to 1.78 Billion

05/29 2026

05/29 2026

539

539

Authored by | Guanchejun

On May 28, Xpeng unveiled its financial results for the first quarter of 2026, revealing a tale of two contrasting narratives.

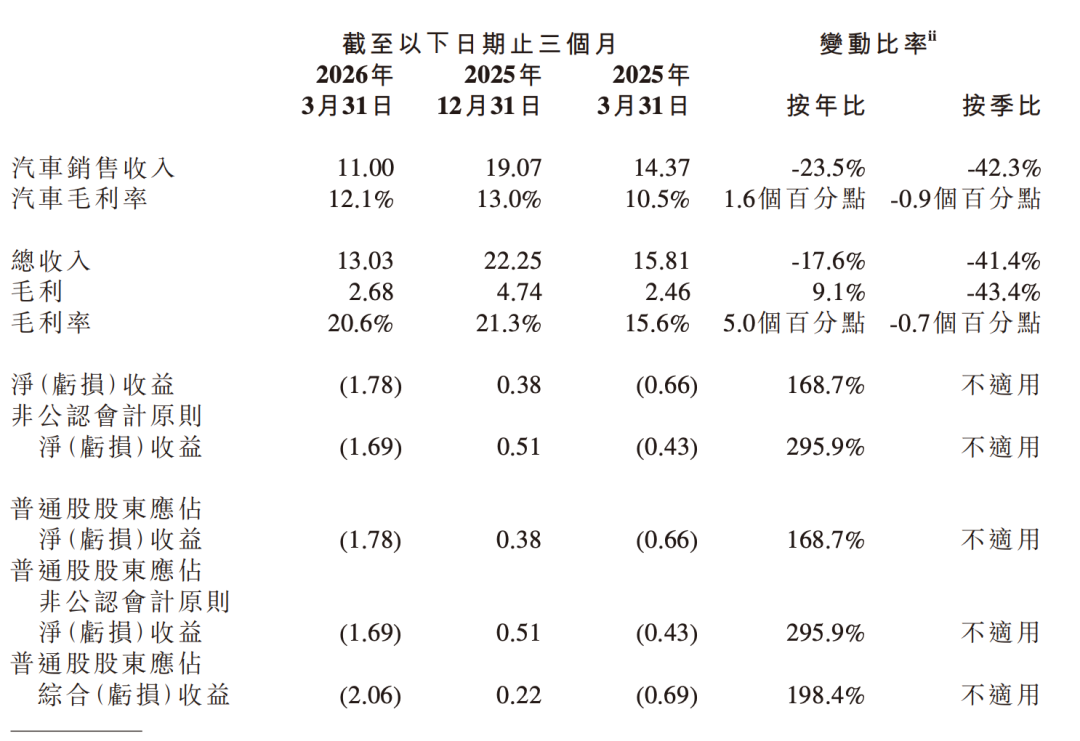

As Guanchejun delved into the financial report, two sets of data stood out in stark contrast. On one hand, the gross margin remained robust at 20.6%, marking a new high for the first quarter in recent memory. On the other hand, the net loss ballooned to 1.78 billion yuan, a staggering year-on-year increase of 168.6%.

This is no trifling sum. Xpeng had incurred a loss of 660 million yuan during the same period last year. So, what has caused this dramatic surge to 1.78 billion yuan this year?

Let's begin with the most straightforward data. In the first quarter of 2026, Xpeng delivered a total of 62,682 new vehicles, a significant drop from the 94,008 units delivered during the same period last year. This translates to a year-on-year decline of 33.3%, a shortfall exceeding 30,000 units.

This challenge is not unique to Xpeng. Traditionally, the first quarter is a sluggish period for the automotive industry. The Spring Festival holiday disrupts production capacity and reduces in-store foot traffic, while consumer enthusiasm for car purchases dips during this festive season. However, Xpeng's 33% decline is notably steeper than the industry average.

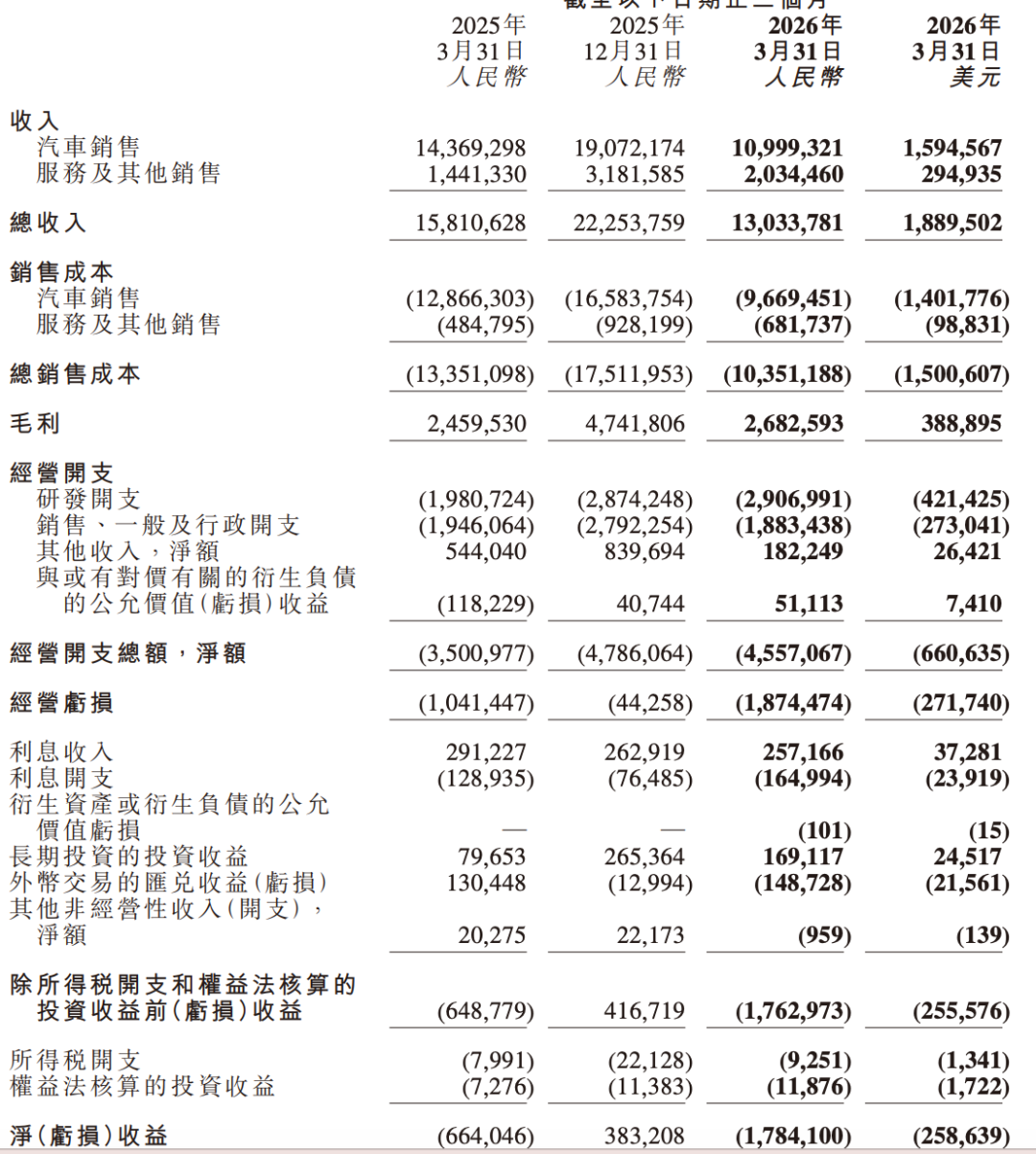

Nevertheless, Xpeng's automotive sales revenue decline in the first quarter (-23.5%) was less severe than the drop in delivery volume (-33.3%). This can be attributed to an increase in the average selling price per vehicle. Unfortunately, this price hike was insufficient to counterbalance the impact of the sales volume decline, resulting in automotive sales revenue plummeting from 14.37 billion yuan to 11.00 billion yuan.

The gross margin performance, however, was relatively commendable. Xpeng's overall gross margin for the first quarter stood at 20.6%, a significant 5 percentage point increase year-on-year.

Historically, Xpeng's gross margin consistently trailed behind that of Li Auto. Now, the tables have turned, with Li Auto's overall gross margin for the first quarter dipping into single digits, being outperformed by Xpeng.

What has driven this gross margin increase? The underlying reason remains consistent: Xpeng is selling more expensive vehicles, with a noticeable upward shift in its product mix. From the G9 to the X9, and now the latest GX, Xpeng's average selling price per vehicle has been on an upward trajectory.

Furthermore, Guanchejun observed that Xpeng's service and other revenue surged by 41.2% year-on-year in the first quarter, reaching 2.03 billion yuan. This revenue primarily comprises software services, supercharging services, and collaboration revenue with Volkswagen. While the absolute amount may not be substantial, both the growth rate and gross margin contribution are noteworthy.

The most conspicuous figure in the financial report is undoubtedly the R&D expenses.

Xpeng's R&D investment in the first quarter amounted to 2.91 billion yuan, a substantial 46.8% increase year-on-year. Compared to revenue of 13.03 billion yuan, the R&D expense ratio has soared to 22.3%. In simpler terms, for every 100 yuan in revenue, 22 yuan is allocated to R&D.

This figure is exceptionally aggressive for the entire automotive industry.

Xpeng has always been driven by technology, allocating funds to the development of new models, investment in AI-related technologies, and the expansion of the Robotaxi business.

However, Xpeng can afford to burn cash for the time being, with approximately 42.1 billion yuan in cash reserves as of March 31, 2026.

Finally, let's revisit the most attention-grabbing figure: a net loss of 1.78 billion yuan, a staggering year-on-year increase of 168.6%.

Breaking it down, Xpeng's operating loss in the first quarter was 1.87 billion yuan. This indicates that Xpeng's daily operations are already incurring losses.

More critically, this expansion of losses is not primarily due to poor gross margin performance but rather a significant surge in R&D expenses. In essence, Xpeng is actively burning cash.

Another factor that often goes unnoticed is net other income.

The financial report mentions that this item generated approximately 180 million yuan in revenue for Xpeng in the first quarter, a sharp decline from the 540 million yuan recorded during the same period last year. The majority of this income stems from government subsidies.

Looking ahead to the second quarter, Xpeng's financial report expresses a relatively optimistic outlook. It projects deliveries to range from 100,000 to 106,000 units, representing a year-on-year change of approximately -3.08% to +2.73% and a quarter-on-quarter increase of approximately 59.54% to 69.11%.

Revenue is expected to range from 19.6 to 20.8 billion yuan, marking a year-on-year increase of approximately 7.25% to 13.82% and a quarter-on-quarter increase of approximately 50.38% to 59.59%.

Given these projections, Xpeng's second-quarter data is certainly worth anticipating.

All charts in this article, unless otherwise cited, are sourced from publicly disclosed information from various channels. We hereby acknowledge and express our gratitude. The views expressed herein are for reference only and do not constitute investment advice.

This article is original content from Leverage Auto Observations and is prohibited from being reproduced without authorization. For reproduction, please obtain authorization. Additionally, when authorized for reproduction, please indicate the source and author at the beginning of the article. Thank you!

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building

-

![]()

Half Flock In, Half Flee Out: The Dual Dynamics of Singapore as an AI Hub