Xpeng: Has the Turning Point Arrived? Can the 'Tesla of the East' Story Continue to Shine?

05/29 2026

05/29 2026

432

432

Xpeng released its Q1 2026 financial results after the market closed in Hong Kong and before the market opened in the U.S. on May 28, 2026, Beijing time. Overall, Xpeng's performance exceeded expectations set against a backdrop of low anticipation, with particularly strong showings in its core vehicle gross margin and Q2 guidance, signaling the emergence of a turning point in its new vehicle cycle:

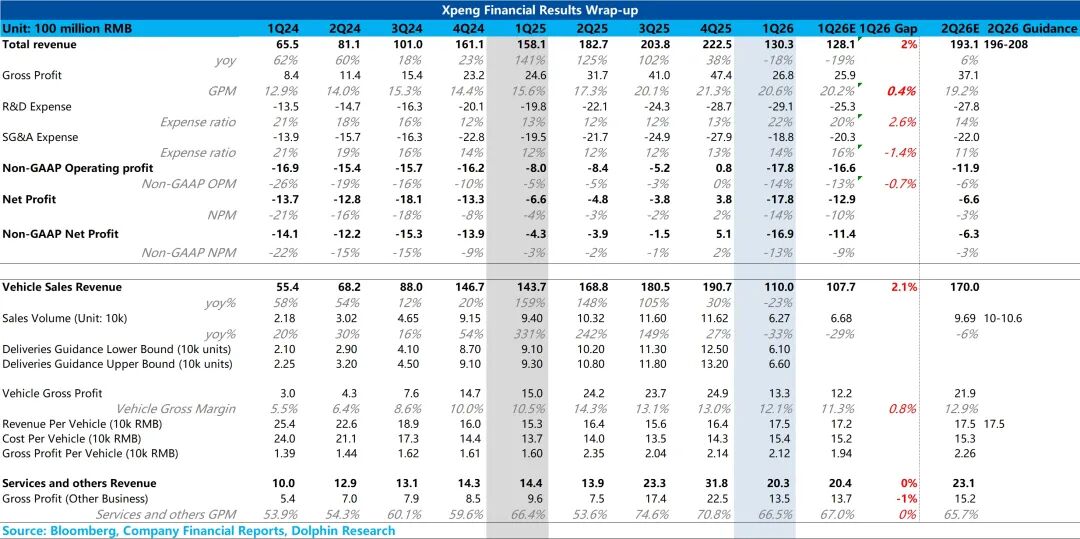

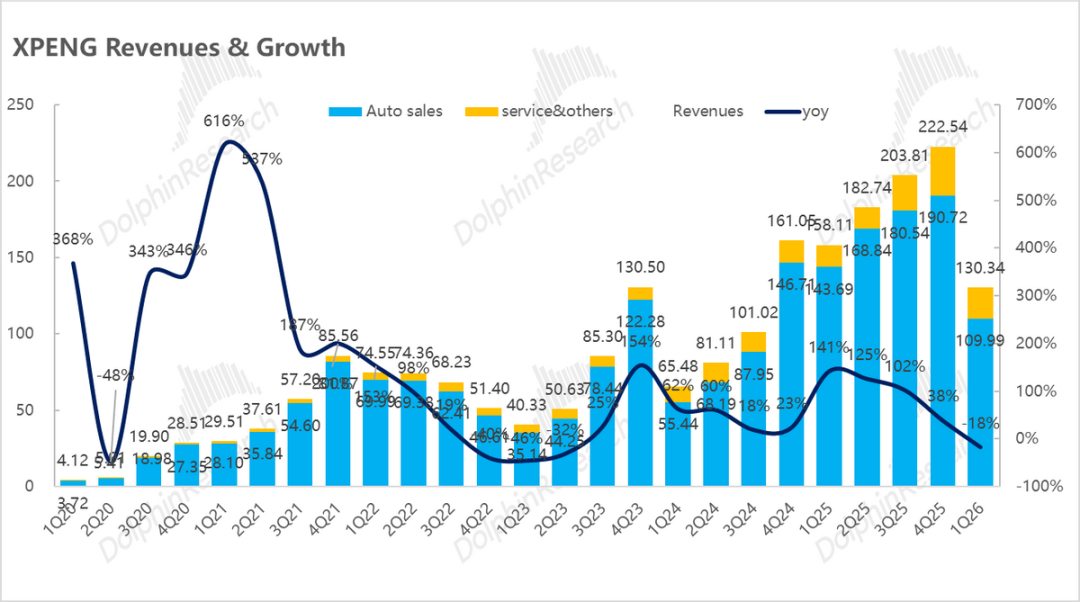

1) Total revenue exceeded expectations, but 'services and other revenue' saw a seasonal decline: Total revenue for the quarter reached RMB 13 billion, surpassing market expectations of RMB 12.8 billion, primarily due to higher-than-expected vehicle sales revenue.

However, 'services and other revenue' amounted to only RMB 2.03 billion, a decrease of RMB 1.15 billion from RMB 3.18 billion in the previous quarter. This decline was mainly due to the achievement of a significant milestone in the electronic and electrical architecture technology R&D service collaboration with Volkswagen in the previous quarter, which resulted in a high base of incremental licensing revenue. This quarter, revenue returned to normal levels. Additionally, there was no contribution from additional carbon credit business revenue generated by overseas expansion in this quarter.

2) Vehicle sales revenue exceeded expectations, with ASP (Average Selling Price) rising against the trend due to structural optimization: Vehicle sales revenue for the quarter was RMB 11 billion (a 23% YoY decrease but exceeding market expectations of RMB 10.8 billion). The ASP reached RMB 175,000, continuing to rise by RMB 11,000 from the previous quarter and surpassing market expectations of RMB 172,000. The upward trend in ASP was primarily driven by an increased proportion of high-priced X9 models and high-margin overseas sales, successfully offsetting pricing pressures.

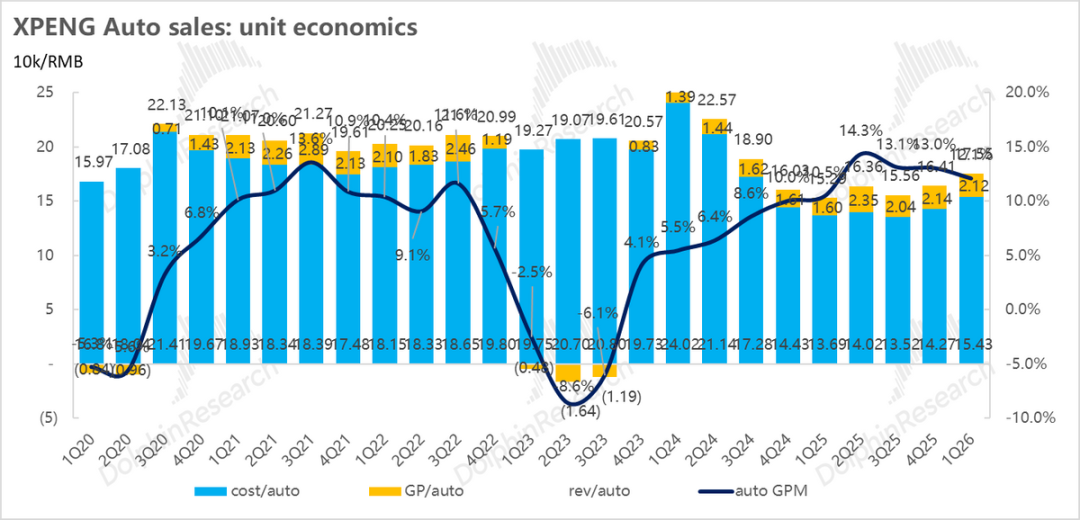

3) Vehicle gross margin 'slightly surprising,' with product mix improvements effectively countering cost pressures: Xpeng's Q1 deliveries were sluggish (a significant 33% YoY decrease to 63,000 units). Additionally, the inherent high BOM (Bill of Materials) costs of the X9, the inability to dilute factory depreciation and amortization due to decreased sales, and early-stage ramp-up costs for the super extended-range version, along with rising prices of core raw materials (batteries, chips, aluminum), led to a substantial increase in unit costs by RMB 11,000 to RMB 154,000.

Despite aggressive pricing strategies ('enhanced features without price increases') and declining sales, which led the market to expect a sequential decline in vehicle gross margin to 11.3%, the actual Q1 vehicle gross margin was 12.1% (only a 0.9 percentage point sequential decline), exceeding market expectations. Unit gross profit remained at RMB 210 million, essentially flat sequentially.

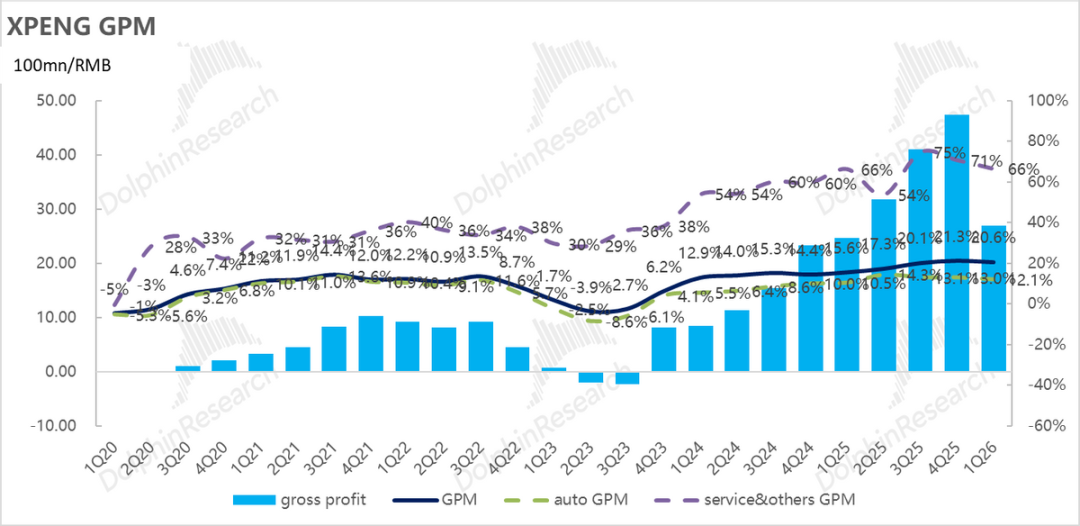

4) Overall gross margin exceeded expectations, primarily driven by better-than-expected vehicle gross margin: The Q1 overall gross margin reached 20.6%, surpassing market expectations of 20.2% and Xpeng's guidance of 20%. Unlike previous reliance on software licensing to drive margins, this time, the Exceed expectations performance in overall gross margin was mainly due to the strong performance of the automotive business. In contrast, the gross margin for the 'services and other' business declined to 66.5% this quarter, slightly below market expectations of 67%, due to a lower proportion of high-margin technology R&D services and carbon credit revenue.

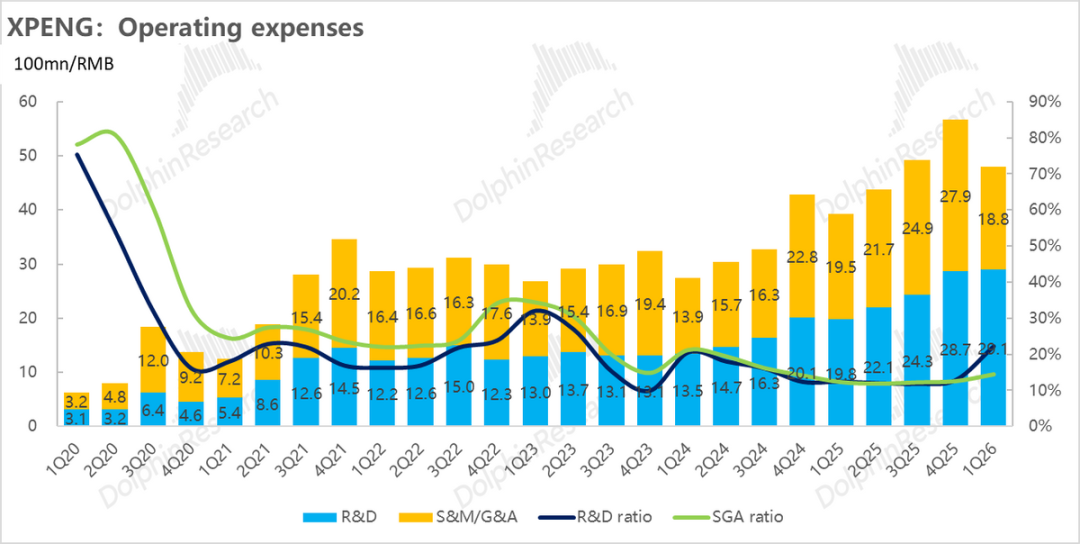

5) Significant increase in R&D expenses due to full commitment to AI and new vehicles, but sales and administrative expenses declined sequentially: To prepare for the 'product-heavy' year of 2026 and the AI ecosystem, Xpeng made substantial upfront strategic investments in R&D, with R&D expenses reaching RMB 2.91 billion (significantly exceeding market expectations of RMB 2.53 billion). These expenses were primarily allocated to intensive new product cycle investments in 'one vehicle, dual capabilities' (pure electric + super extended-range), self-developed 'Turring' chips and VLA 2.0 large model upgrades, as well as forward-looking investments in the 'Iron' humanoid robot (planned for mass production by the end of 2026 with a monthly production target exceeding 1,000 units).

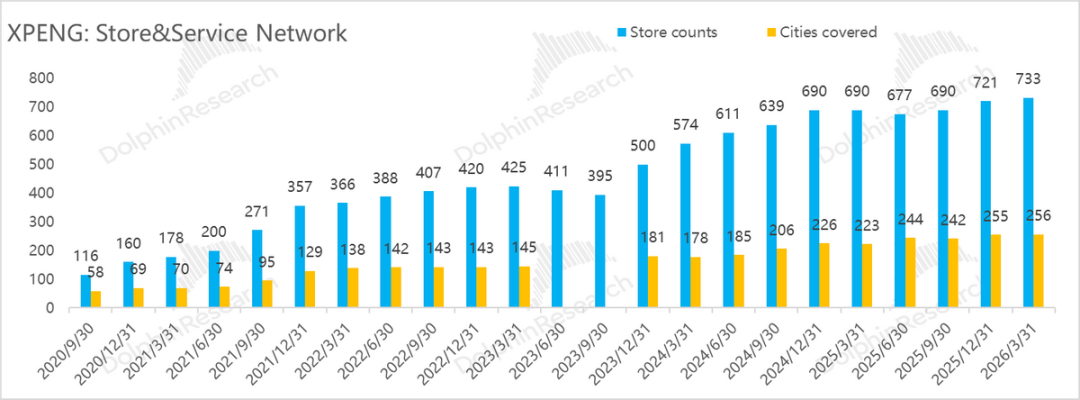

Sales and administrative expenses were only RMB 1.88 billion (below expectations of RMB 2.03 billion), a significant sequential decrease of approximately RMB 900 million, mainly due to reduced franchise store commissions resulting from lower Q1 sales. However, channel expansion continued, with a net increase of 12 stores in the quarter to a total of 733, preparing for future sales growth.

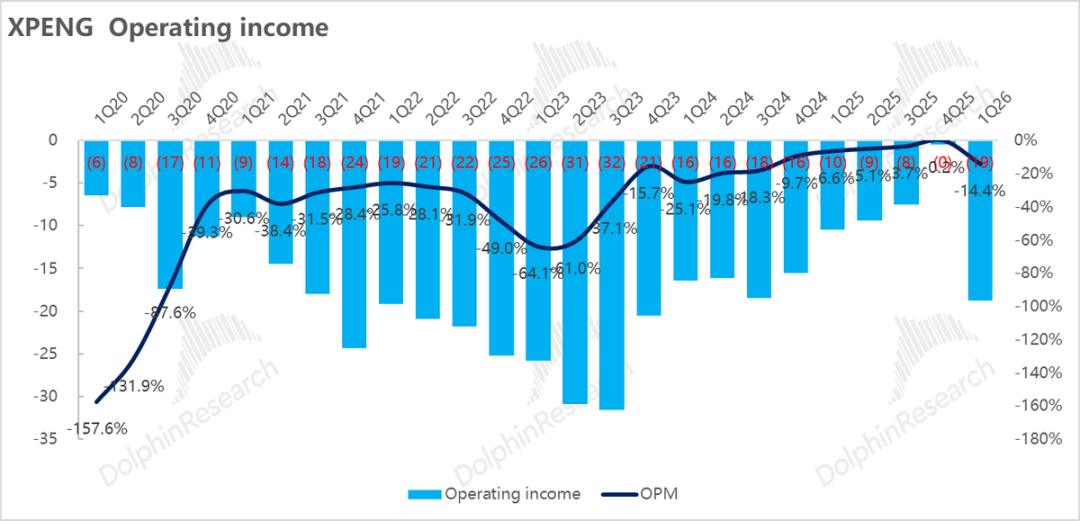

6) Losses widened, with the sales volume leverage effect yet to be realized: Xpeng's net loss for the quarter was -RMB 1.78 billion, exceeding market expectations of -RMB 1.3 billion, primarily due to high R&D expenses, a sequential reduction of RMB 660 million in one-time 'other income' such as government subsidies, and increased exchange losses.

From the perspective of core operating profit (gross profit - core operating expenses), which reflects the main business's ability to generate cash, Q1 saw a loss of -RMB 1.87 billion (an increase of RMB 1.83 billion from -RMB 40 million in the previous quarter). This indicates that sales failed to stimulate strong demand at the end-market as expected, resulting in the positive effects of operating leverage not yet being realized, and the core business continuing to bleed cash in the short term.

Dolphin Research View:

Overall, Xpeng delivered a performance that slightly exceeded expectations set against a backdrop of low anticipation. The higher-priced X9 drove the model mix upward, and an increased proportion of overseas sales raised the average selling price of vehicles sequentially, effectively offsetting the adverse impact of rising vehicle costs. Ultimately, both vehicle sales revenue and gross margin exceeded expectations.

However, Xpeng remained in a strategic investment phase of 'high investment for future growth' in Q1. The significant increase in R&D, coupled with the off-season for sales, led to a temporary expansion of operating losses.

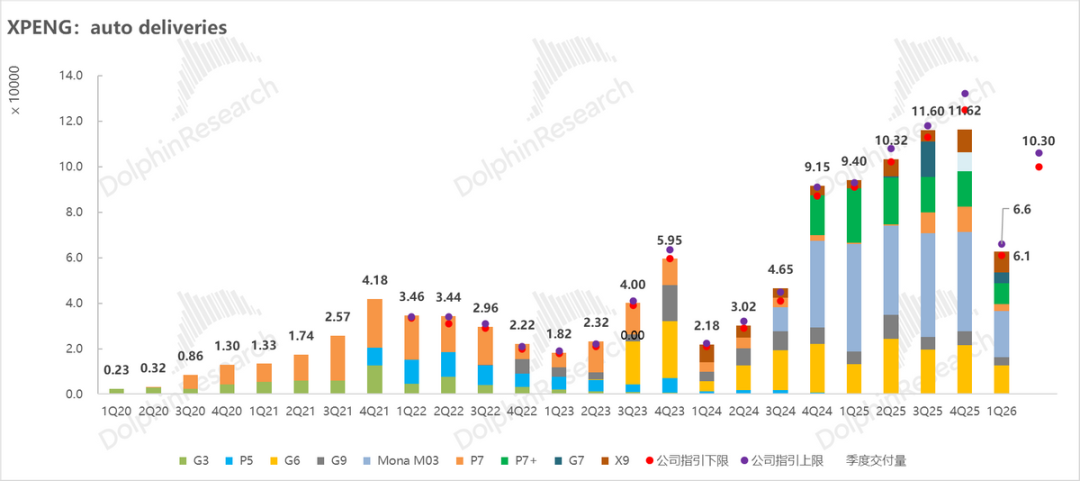

Meanwhile, Xpeng's vehicle sales volume in Q1 was 133,000 units, a 33% YoY decrease. Despite the company's dense launch of a product mix including the G7, P7+, G6, and G9, and the full implementation of the 'one vehicle, dual capabilities' strategy of 'pure electric + super extended-range,' the incremental release from older baseline models still fell short of expectations. The resulting market skepticism about Xpeng's new vehicle cycle's explosive potential has been fully reflected in the sustain decline of its stock price.

Nevertheless, as the downturn of Q1 has largely been priced in by the stock market, the market is clearly more concerned about Q2 guidance—especially given the phased pressure faced in advancing the 'one vehicle, dual capabilities' extended-range strategy in Q1. The Exceed expectations sales volume and revenue guidance for Q2 Exactly confirms that the 2026 MONA M03 facelift and the new full-size flagship SUV GX have the potential to gradually lead Xpeng out of its 'predicament.' Specifically:

a) Sales volume guidance exceeded expectations, with new models contributing the majority of the increase

Q2 sales volume guidance is 100,000-106,000 units, not only exceeding market expectations of 97,000 units but also remaining roughly flat YoY. Based on the 31,000 units delivered in April, the implied average monthly sales for May/June need to reach 34,500-37,500 units.

This increase primarily comes from two new models—the 2026 MONA M03 facelift (launched on April 2) and the new full-size flagship SUV GX (RMB 289,800-359,800, launched on May 20), directly confirming that these two new models have begun to assist Xpeng in reversing its downturn and overcoming the initial hurdles in advancing the 'one vehicle, dual capabilities' strategy.

b) Revenue guidance implies flat ASP sequentially, with high-priced GX offsetting increased proportion of MONA M03

Q2 revenue guidance is RMB 19.6-20.8 billion, also higher than market expectations of RMB 19.3 billion, primarily benefiting from higher-than-expected sales volume. The implied Q2 vehicle ASP in this revenue guidance remains at RMB 175,000, roughly flat with Q1.

Despite a significant sequential increase in the proportion of the low-priced MONA M03 model (price range RMB 119,800-151,800), the ASP remains at a high level, flat with Q1. This is mainly due to the significant pulling effect of the high-priced GX model (RMB 289,800-359,800) on the overall average price, effectively offsetting the downward pressure from the increased proportion of low-priced models.

② Looking at the full year of 2026:

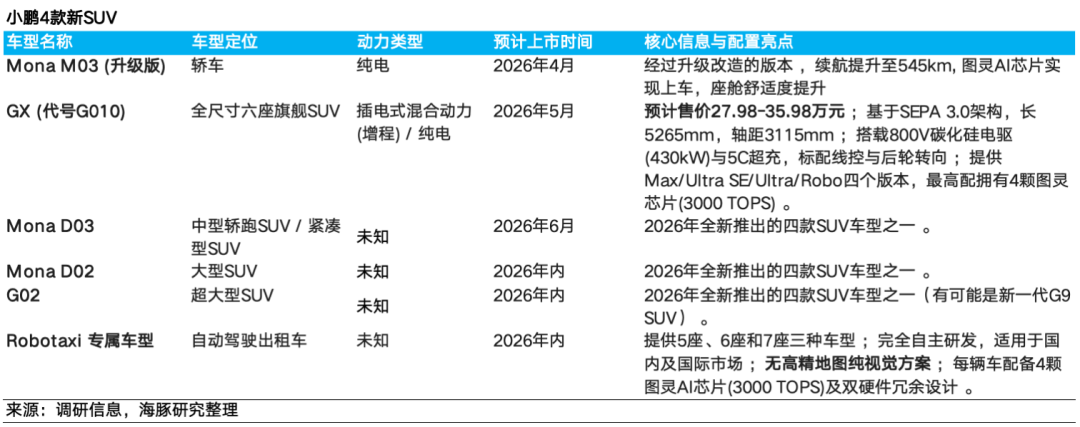

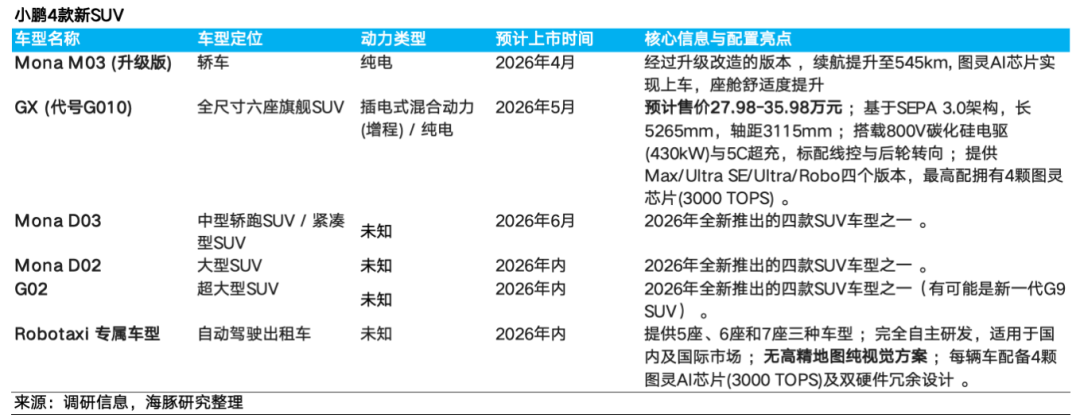

Although the 'one vehicle, dual capabilities' plan got off to a rocky start in Q1, Xpeng still has four new SUV models poised for launch in 2026, maintaining a strong new vehicle cycle. Additionally, overseas expansion is gradually becoming a core growth engine.

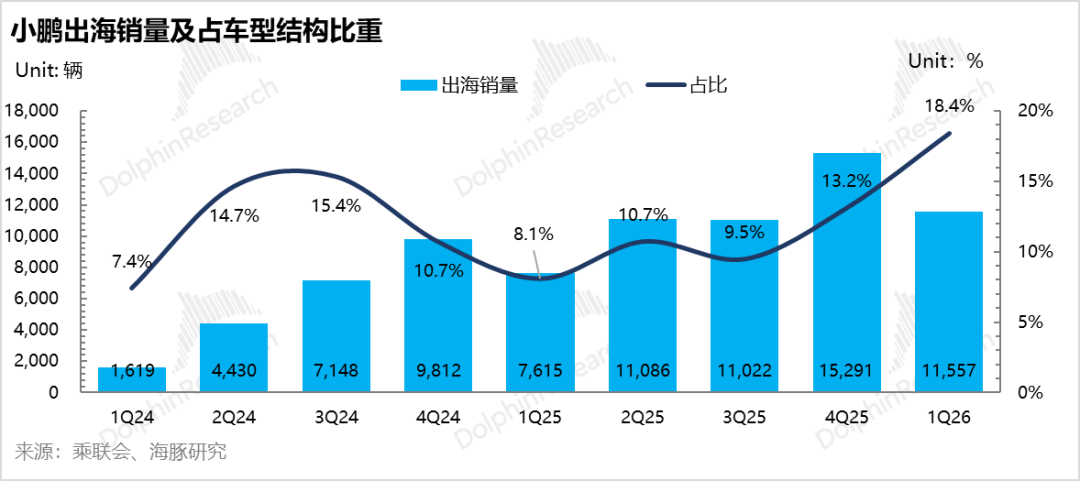

Overseas expansion as a core growth engine for sales volume: The company plans to double its overseas sales to 90,000 units in 2026. It will focus on expanding into the Israeli, German, Norwegian, Thai, and French markets and plans to extend its channel network to 680 stores, covering over 60 countries and regions.

With nearly 17,500 overseas sales in January-April, Dolphin Research believes the achievement of this aggressive target remains to be seen. Under a neutral assumption, overseas sales are expected to reach 80,000 units, a 78% YoY increase.

Domestic baseline supported by a 'major new vehicle cycle': Dolphin Research believes that with the contribution of two high-volume MONA platform new SUVs launching in Q2 and the second half of the year, Xpeng's domestic sales volume in 2026 is expected to increase by 9% YoY to 420,000 units, largely in line with industry growth.

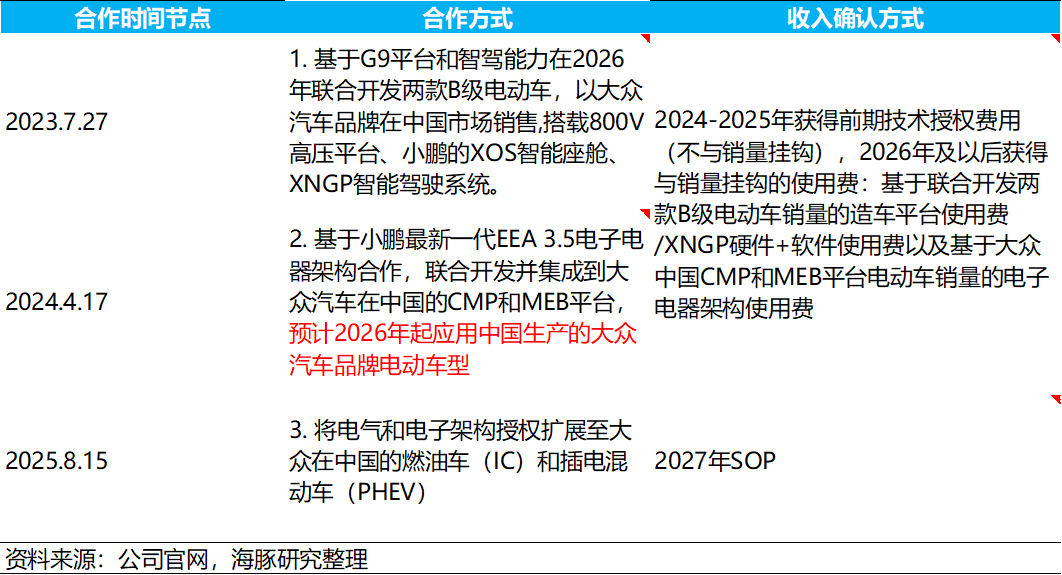

Regarding AI progress: Xpeng is accelerating the commercialization of its AI capabilities from R&D:

a. Intelligent driving foundation upgraded again: At the hardware level, the self-developed 'Turring' chip (750 TOPS per chip) has entered mass production across all models. At the algorithm level, the VLA 2.0 large model was released in March, adopting a 'visual direct-to-action' architecture and serving as a unified foundation for automobiles, Robotaxis, and robots. To accelerate integration, the company has established a new 'General Intelligence Center.'

b. Robotaxi acceleration: Xpeng plans to launch three models specifically designed for Robotaxis in 2026, equipped with four Turring chips (3,000 TOPS), and begin pilot operations while licensing software development kits to third parties.

c. Humanoid robot sprint: The new generation 'Iron' robot's R&D has entered a critical stage, featuring all-solid-state batteries, three Turring chips, and an integrated multimodal large model system, focusing on commercial, industrial, and household scenarios. Mass production is planned for the end of 2026, with a target monthly production capacity exceeding 1,000 units.

If AI businesses (Robotaxi pilot operations, humanoid robot mass production, etc.) progress steadily and deliver commercial value, they are expected to drive a reevaluation of Xpeng's valuation system by the market.

Below is the main text

I. 'Slightly Surprising' Vehicle Business Gross Margin

Since Xpeng's Q1 sales volume has already been announced, investors are more concerned about the automotive business's revenue and gross margin in this financial report.

Xpeng's Q1 deliveries were sluggish, with a significant 33% YoY decrease to 63,000 units. Given the weakened scale effect and upward pressure on raw material costs, the market expected Xpeng's vehicle gross margin to decline sequentially by 1.7 percentage points from 13% in the previous quarter to 11.3% in this quarter.

Xpeng's actual Q1 vehicle gross margin was 12.1%, higher than market expectations, primarily due to the continued unexpected increase in vehicle ASP driven by improvements in the model mix and an increased proportion of overseas sales.

From a detailed look at unit economics:

a) ASP: High-priced models and overseas expansion drive ASP upward

Xpeng's Q1 ASP reached RMB 175,000, continuing to rise by RMB 11,000 from RMB 164,000 in the previous quarter and exceeding market expectations of RMB 172,000. The upward trend in ASP was mainly driven by two factors:

① Increased proportion of flagship model X9: In Q1, the sales proportion of the high-priced X9 increased by 6 percentage points sequentially to 15%. Meanwhile, the proportion of the low-priced MONA M03, targeting the sink market, continued to decline sequentially by 5 percentage points to 33%. This shift resulted in a clear tilt of the domestic sales model mix toward higher price segments.

② Increased proportion of high-margin overseas sales: In Q1, Xpeng's overseas sales volume reached 11,600 units, a 52% YoY increase, while domestic sales volume declined by 41% YoY to 51,000 units. The proportion of overseas sales in total sales also increased sequentially by 5.3 percentage points to 18.4%. Due to higher pricing in overseas markets, the increased proportion of overseas sales directly raised the overall ASP.

③ Overall discounting increased significantly but was offset by improvements in the model mix and increased proportion of overseas sales

In Q1, Xpeng significantly increased its promotional efforts, offering cash discounts of RMB 5,000/8,000/17,000/8,000/8,000/5,000 for its G6/G7/G9/P7+/P7/Mona M03 models, respectively. It also continued offering 3-year interest-free/5-7-year low-interest financial plans for some models. The overall discounting intensity increased significantly compared to Q4 last year but was effectively offset by improvements in the model mix and increased proportion of overseas sales.

b) Unit cost: Weakened scale effect and rising raw material costs drive unit costs upward

In Q1, Xpeng's unit cost was approximately RMB 154,000, a significant sequential increase of about RMB 11,000 from RMB 143,000 in the previous quarter. The core drivers of this cost increase included:

① Inherent cost increases from high-priced models: Although the increased proportion of X9 models raised the ASP, as a large MPV, its unit BOM (Bill of Materials) cost is inherently high, structurally raising the average unit cost.

② Weakened scale effect: Total deliveries in Q1 were only 63,000 units, a 33% YoY decrease, falling toward the lower end of the previous guidance range of 61,000-66,000 units. The decline in sales volume meant that fixed costs such as factory depreciation and amortization could not be further effectively diluted.

Although Xpeng still faced pressure from the phase-out of industry purchase tax incentives in Q1 (with new energy vehicle industry sales volume declining by approximately 5% YoY), its sales volume declined at a faster rate than the industry average despite the dense launch of the 'one vehicle, dual capabilities' product mix including the G7/P7+/G6/G9.",

II. Q2 Guidance Exceeds Expectations, New Models Expected to Reverse "Dual Powertrain" Slump

Compared to Q1, when the "Dual Powertrain" range-extender strategy faced phased pressure, Q2's better-than-expected sales and revenue guidance confirms the potential of the 2026 Mona M03 facelift and the all-new GX model to gradually lift XPENG out of its "predicament." Details are as follows:

a) Sales guidance exceeds expectations, driven primarily by new models

In Q1, XPENG sold 133,000 vehicles, a 33% YoY decline. Despite launching a product blitz with the G7, P7+, G6, and G9, and fully implementing the "Dual Powertrain" strategy (BEV + range-extended), the incremental release from legacy models fell short of expectations. Market skepticism about XPENG's new model cycle momentum was reflected in its sustained stock price decline.

However, Q2 sales guidance of 100,000–106,000 units not only surpasses market expectations of 97,000 units but also remains roughly flat YoY. Based on 31,000 deliveries in April, this implies average monthly sales of 34,500–37,500 units in May/June.

This growth is primarily driven by two new models: the 2026 MONA M03 facelift (launched April 2) and the full-size flagship SUV GX (RMB 289,800–359,800, launched May 20). This directly confirms that these models are beginning to help XPENG reverse its "slump" and overcome early hurdles in the "Dual Powertrain" strategy rollout.

b) Revenue guidance implies flat ASP YoY, high-priced GX offsets rising MONA M03 share

Q2 revenue guidance of RMB 19.6–20.8 billion also exceeds market expectations of RMB 19.3 billion, primarily due to better-than-expected sales. This guidance implies a Q2 average selling price (ASP) of RMB 175,000, roughly flat with Q1.

Despite a significant sequential increase in the share of the lower-priced MONA M03 (RMB 119,800–151,800), ASP remains high and flat with Q1. Dolphin Research attributes this to the strong pull-through effect of the higher-priced GX (RMB 289,800–359,800), which effectively offsets downward pressure from the rising share of lower-priced models.

III. Gross Margin Exceeds Expectations, Driven by Strong Auto Gross Margin

In Q1, XPENG's total revenue reached RMB 13 billion (beating expectations of RMB 12.8 billion), with an overall gross margin of 20.6%, surpassing market expectations of 20.2% and the company's guidance of 20%. The margin beat was primarily due to better-than-expected performance in the automotive segment, while other business revenues largely met expectations.

① Revenue beats expectations, driven by strong auto revenue:

The automotive segment exceeded both revenue and gross margin expectations, primarily due to a sequential increase in ASP offsetting the negative impact of rising costs. Q1 automotive revenue was RMB 11 billion (down 23% YoY but beating expectations of RMB 10.8 billion), driven by a higher mix of the high-ASP X9 model and strong overseas sales.

Q1 "Services and Other Revenue" was just RMB 2.03 billion, down RMB 1.15 billion sequentially from RMB 3.18 billion in Q4. The sharp decline was due to two main factors:

a. In Q4, a major milestone was reached in the R&D collaboration with Volkswagen on electronic electrical architecture technology, resulting in significant incremental licensing revenue. In Q1, R&D service revenue returned to normal levels, declining sequentially.

b. Q4 benefited from additional carbon credit revenue due to rising overseas sales, but Q1 saw no carbon credit revenue contribution.

② Gross margin slightly exceeds expectations, primarily due to strong auto gross margin

Q1 auto gross margin was 12.1%, down 0.9 percentage points sequentially but still above market expectations of 11.3%. Despite weakening scale effects and rising raw material costs, the higher mix of high-ASP models effectively offset cost headwinds.

Services and other businesses gross margin was 66.5%, down 4.3 percentage points sequentially and below market expectations of 67%, primarily due to the declining share of high-margin R&D services and carbon credit revenue.

IV. OPEX Ramp-Up for "Dual Powertrain" and AI Ecosystem Weighs on Profit Release

XPENG has always positioned "intelligence" as its core moat, necessitating sustained high-intensity investment in AI autonomous driving and new platform R&D. In Q1, these strategic pre-investments for the 2026 "product supercycle" drove R&D expenses well above expectations, becoming the primary drag on core operating profit release this quarter.

1) R&D expenses: RMB 2.9 billion, well above expectations, continuing sequential increase, full bet on new models and physical AI

Q1 R&D expenses reached RMB 2.91 billion, significantly exceeding market expectations of RMB 2.53 billion and increasing by RMB 40 million sequentially from RMB 2.87 billion in Q4. The sequential increase was primarily used for new model development and higher AI-related R&D spending, reflected in three areas:

① Upfront investments for the dense new product cycle: Starting in Q4 2025, XPENG officially launched its major "Dual Powertrain" product transformation, introducing range-extended versions for all existing BEV models and planning to launch four all-new SUV models in 2026. Q1 R&D expenses represent upfront investments for this dense (intense) new product cycle.

② ADAS technology upgrades: At the hardware level, XPENG's self-developed high-end "Turring" chip (750 TOPS per chip) has entered mass production across all models. At the algorithm level, the company's VLA 2.0 (Vision-Language-Action) large model was officially released in March 2026.

This model adopts an innovative "vision-direct-action" end-to-end architecture, eliminating the language translation layer in traditional architectures to reduce latency and improve decision efficiency. It will serve as a unified technical foundation for multiple intelligent agents, including vehicles, Robotaxi, robots, and flying cars. To accelerate this convergence, XPENG established a new "General Intelligence Center" integrating autonomous driving and smart cockpit R&D teams to build a unified AI base model and technology system.

③ Forward-looking investments in humanoid robots: XPENG's next-gen "Iron" humanoid robot has entered a critical R&D stage. The robot features industry-first all-solid-state batteries, three "Turring" AI chips (total 2,250 TOPS), and integrates a multimodal large model system combining VLT (Thinking), VLA (Action), and VLM (Interaction). Applications focus on commercial, industrial, and household sectors, initially providing reception, guidance, and retail assistance in Chinese and overseas stores and campuses. XPENG plans to start mass production of "Iron" by end-2026, targeting monthly capacity exceeding 1,000 units by year-end.

According to company guidance, XPENG's full-year 2026 R&D expenses are expected to grow ~26% YoY to RMB 12 billion, with ~RMB 7 billion for AI-related R&D and ~RMB 5 billion for vehicle R&D.

2) SG&A expenses: Sharp sequential decline due to lower sales commissions, but channel expansion continues

Q1 selling, general, and administrative (SG&A) expenses were RMB 1.88 billion, also below market expectations of RMB 2.03 billion and down ~RMB 900 million sequentially from Q4. The decline was primarily due to lower commissions paid to franchise stores amid a sharp sequential drop in Q1 sales volume.

Notably, XPENG continues to accelerate store openings to support the 2026 "Dual Powertrain" market penetration strategy and the arrival of four new SUVs. Q1 saw a net increase of 12 stores (total 733) covering one additional city (total 256), preparing channels for upcoming new model launches.

V. Operating Loss Widens, Sales Leverage Yet to Kick In

XPENG's Q1 net loss was -RMB 1.78 billion, worse than market expectations of -RMB 1.3 billion. Besides high R&D expenses suppressing profitability, a sharp sequential decline in "Other Income" (primarily one-time government subsidies, down RMB 660 million) and increased foreign exchange losses further dragged down net profit.

Looking at "Core Operating Profit" (Gross Profit - Core Operating Expenses), which better reflects core business profitability, Q1 was -RMB 1.87 billion, worsening by nearly RMB 1.83 billion from -RMB 40 million in Q4, primarily due to:

a. Sharp YoY sales decline (Q1 sales: 133,000 units, -33% YoY), failing to release scale effects: The sales drop left fixed costs per unit inadequately diluted, pressuring gross margins. Meanwhile, low sales volumes could not effectively absorb high operating expenses, preventing positive operating leverage from materializing.

b. Sequential increase in R&D expenses: R&D expenses rose further to RMB 2.91 billion from RMB 2.87 billion in Q4, continuing to suppress profit release.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general reference only, intended for users of Dolphin Research and its affiliates for general browsing and data reference. It does not consider any individual's specific investment objectives, product preferences, risk tolerance, financial situation, or special needs. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referring to the content or information in this report for investment decisions bears their own risks. Dolphin Research shall not be liable for any direct or indirect losses arising from the use of data in this report. The information and data herein are based on publicly available sources and are for reference only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of such information and data.

The information and views expressed in this report do not constitute an offer to sell or a solicitation to buy securities in any jurisdiction, nor do they constitute recommendations, quotations, or endorsements of securities or related financial instruments. The information, tools, and materials herein are not intended for distribution to, or use by, persons in jurisdictions where such distribution, publication, provision, or use would contravene applicable laws or regulations or require Dolphin Research and/or its affiliates or subsidiaries to comply with registration or licensing requirements in such jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliates.

This report is produced by Dolphin Research, with copyright reserved solely by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) reproduce, copy, duplicate, reprint, forward, or otherwise create copies or replicas in any form, and/or (ii) directly or indirectly redistribute or transfer to any unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building

-

![]()

Half Flock In, Half Flee Out: The Dual Dynamics of Singapore as an AI Hub