Q1 Revenue Hits 13 Billion! He Xiaopeng: GX Performance Exceeds Expectations, Sales to Surge in Q3-Q4

05/29 2026

05/29 2026

538

538

"As of now, to be honest, the performance of the GX model has exceeded our expectations—it's been exceptional. We've seen some very interesting data, such as the fact that the current wait time for our pure electric flagship version has surpassed 30 weeks and is still growing rapidly," XPENG Chairman He Xiaopeng responded on May 28 during the Q1 financial results conference call, addressing the performance of the newly launched flagship GX model.

On May 20, XPENG launched its first full-size flagship SUV, the XPENG GX, offering both pure electric and range-extended powertrain options with limited-time promotional prices ranging from 269,800 to 349,800 yuan. Within just 12 hours of launch, the GX secured over 24,863 firm orders, with the Ultra flagship version accounting for more than 80% and pure electric models making up over half of the orders. Due to the surge in orders and delivery pressure, He Xiaopeng voluntarily gave up two delivery slots to allow customers to take delivery sooner.

He Xiaopeng noted that the flagship version remains the highest-selling variant, while the GX Max version accounts for less than 5% of sales. The range-extended version is gradually aligning with the pure electric version in popularity. Particularly after XPENG strengthened its marketing efforts in northern and western regions, sales have begun to rise. "We certainly expect the GX to rank among the top three in sales for premium new energy six-seater vehicles, creating a headline blockbuster in the 300,000-yuan-plus market," He said.

Furthermore, He Xiaopeng stated that the GX's gross margin has exceeded expectations. "When I spoke with media friends earlier, I mentioned that only one SKU's margin fell short of our expectations, but in reality, all variants are outperforming our overall gross margin," he said. As a result, the GX will become a key growth driver for XPENG in terms of both sales volume and profitability. "I believe that starting with the XPENG GX, we aim to achieve a better balance between commercial success and scale, as well as more sustainable long-term sales," He Xiaopeng said.

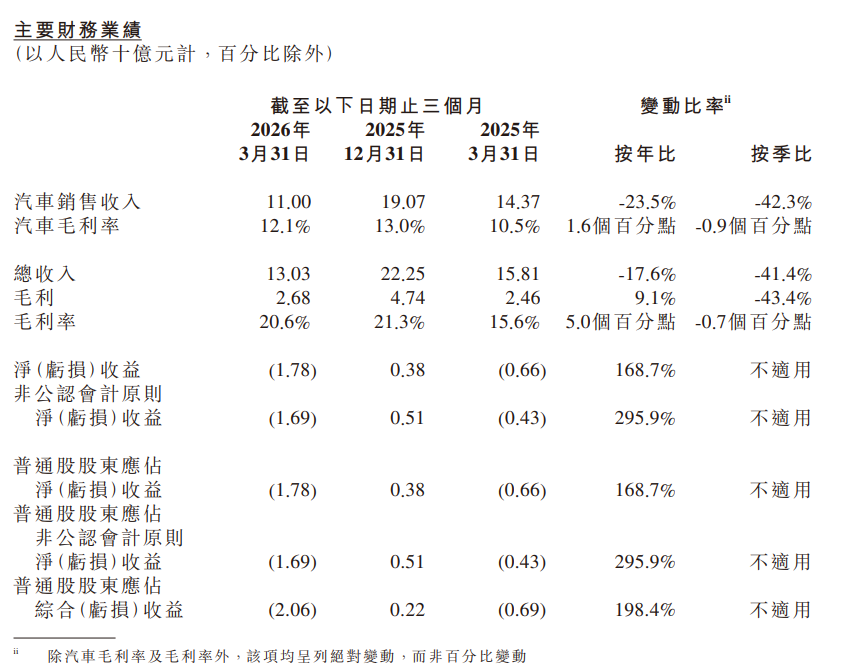

In Q1, the industry faced significant pressure, and XPENG was not immune to the overall market downturn. Deliveries reached 62,682 units, down 33.3% from 94,008 units in the same period in 2025. Total operating revenue for Q1 was 13.03 billion yuan, a 17.6% year-over-year decline, slightly below market estimates of 13.16 billion yuan. Operating loss stood at 1.87 billion yuan, while net loss widened to 1.78 billion yuan, up significantly from 660 million yuan in the same period last year.

Despite the decline in deliveries and revenue, profitability metrics showed improvement. The Q1 gross margin was 20.6%, higher than market expectations of 20% and up 5 percentage points from the same period in 2025. The automotive gross margin was 12.1%, a 1.6 percentage point year-over-year increase. As of the end of Q1, the company held 42.09 billion yuan (approximately 6.1 billion USD) in cash, down from 47.66 billion yuan at the end of 2025 but still at a healthy level.

In XPENG's financial results, software collaboration with Volkswagen remained the most significant profit contributor. Q1 automotive sales revenue was 11 billion yuan, down 23.5% year-over-year. Service and other revenue surged 41.2% year-over-year to 2.03 billion yuan, accounting for approximately 15.6% of total revenue, up from 9.1% in Q1 2025.

The growth in service revenue was driven by two main factors: first, increased revenue from technology R&D services, reflecting XPENG's commercialization of AI and intelligent driving technologies for external partners; second, growth in parts and accessories sales, closely tied to the expanding vehicle parc. This includes revenue from software collaboration projects with Volkswagen. It should be noted that service revenue in the previous quarter (Q4 2025) reached 3.18 billion yuan, primarily due to concentrated recognition of major milestones, and has now returned to normal levels. The service business gross margin was a remarkable 66.5%, more than five times that of the automotive hardware business.

Looking ahead to Q2, XPENG expects deliveries to range between 100,000 and 106,000 units, representing a quarter-over-quarter increase of approximately 60% to 69%, higher than Bloomberg's consensus estimate of 96,923 units. Total revenue is expected to be between 19.6 billion and 20.8 billion yuan, up approximately 7% to 14% year-over-year.

Regarding future development, XPENG emphasized three key areas: automotive products, robotics, and intelligent driving assistance. For automotive products, He Xiaopeng stated that starting this year, all new models will focus on two new aspects: first, determining configurations and pricing while pursuing appropriate commercial quality; second, avoiding high initial sales followed by declines, instead aiming for more stable sales by implementing new systems for modular supply chain management, ramp-up, and supply chain security.

Another focus is Robotaxi. He Xiaopeng said that XPENG will roll out VLA 2.0 in both Chinese and overseas markets and "make it a success." In China, XPENG will leverage its current vehicles for rapid R&D and testing. By 2027, XPENG plans to launch an affordable model to demonstrate and commercially validate Robotaxi services. He emphasized two key points regarding the Robotaxi business: first, XPENG will focus solely on product development and commission fees, avoiding direct operations; second, XPENG's Robotaxi efforts will primarily target the global market, which he believes holds tremendous commercial value.

He Xiaopeng believes that Robotaxi R&D will have a positive spillover effect on the consumer (C-end) business, with the B-end and C-end gradually diverging into separate segments.

Additionally, He Xiaopeng announced that XPENG's R&D for the new generation of IRON humanoid robots, aimed at mass production, is progressing smoothly and will soon enter the ET2 hardware-software integration phase, with a formal debut planned for Q3 this year. XPENG aims to achieve high-volume production of advanced humanoid robots by the end of this year, initially for trial commercial use in XPENG stores, followed by deliveries to commercial clients in China and overseas starting next year. From next year onward, hardware and AI model revenues from humanoid robots will become a significant driver of growth for XPENG's overall revenue and gross margin.

In terms of overseas strategy, He Xiaopeng stated that overseas sales will account for 50% of total sales within the next five years, with significant contributions to revenue and profit. Currently, overseas sales have already reached nearly 20% of the monthly total, with significantly higher profitability compared to the domestic market. He noted that XPENG has already initiated local manufacturing in Southeast Asia and Europe. This year, automotive R&D will focus on adapting hardware, software, channels, and service networks for overseas markets. He added that overseas expansion will accelerate significantly over the next three years.

With these collective efforts, He Xiaopeng expressed confidence in the future. "I believe our sales have bottomed out from the industry downturn, and with the delivery of four global models, ramping up production capacity, and rapid growth in international business, XPENG will continue to push for higher sales targets in Q3 and Q4," He said.

-

![]()

The Agent hasn't arrived yet, but Ascend has already paved the way from hardware to software.

-

![]()

In 71 years, He sold products to 100 million people

-

![]()

First-hand Practical Test! Opus 4.8 Vs ChatGPT 5.5 Vs Kimi 2.6: Which is the Most Usable?

-

![]()

Fourfold Uncertainty Challenges Facing China's Agent Industry - Interpretation of the 'Report' (Part Six)

-

Crazy Anthropic

-

![]()

CNPC’s Kunlun Model Advances with 152 Implemented Scenarios, Showcasing Proactive AI

-

![]()

Revenue Increases, But Profits Don't: Pinduoduo's Anxiety Amidst Billion-Dollar Brand Building

-

![]()

Half Flock In, Half Flee Out: The Dual Dynamics of Singapore as an AI Hub