May Auto Sales Insight: Joint Ventures Falter, New Entrants Rise, with Exports Lending Support?

06/08 2026

06/08 2026

482

482

The Chinese automotive market in May presented a somewhat paradoxical scenario. Retail sales across the entire passenger vehicle sector witnessed a month-on-month uptick but suffered a year-on-year downturn, plummeting nearly 20% compared to the same period last year. This trend underscores a diminished enthusiasm among consumers for car purchases. Nevertheless, amidst this backdrop, new energy vehicles (NEVs) managed to elevate their retail market penetration to 63%, marking a historic peak.

Within this evolving landscape, joint venture brands are bearing the brunt. Toyota has experienced a nine-month consecutive sales slump in China, while Honda's sales plummeted by 21% in May. Their once-celebrated reputation, built on robust engines and transmissions, now appears misaligned with the burgeoning trends of electrification and intelligent driving. It's not that joint ventures are averse to change; rather, their product development cycles are sluggish, and their pricing lacks the requisite competitiveness.

Turning our attention to independent brands, BYD stands out prominently. In May, BYD sold 383,500 NEVs, finally breaking free from a period of stagnant sales growth. This year-on-year and nearly 20% month-on-month surge propelled its monthly sales back to the 400,000-unit mark. The primary catalyst for this resurgence is the largely concluded phase of model renewal, coupled with the introduction of new flash-charging models that are starting to gain significant traction.

Chery, too, had a notable month, selling 247,000 units in May, up over 20% year-on-year, with exports playing a pivotal role—over 180,000 units shipped in a single month. This statistic underscores a glaring reality: domestic competition is fierce, making overseas expansion a crucial driver of growth.

Geely also maintained a steady course. Its total sales reached 237,600 units in May, marking year-on-year and month-on-month growth for three consecutive months. Its NEV penetration has surpassed 56%, and the Zeekr brand continues to ascend. Geely's strategy is evident—a multi-brand approach encompassing hybrid and pure electric models, ensuring it caters to diverse consumer preferences.

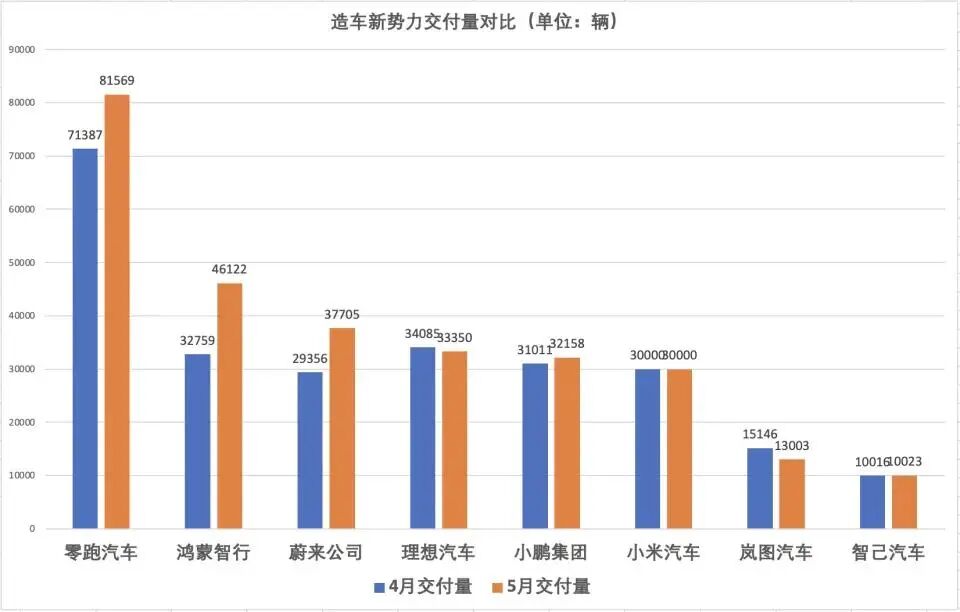

However, the most staggering figure in May emerged from Leapmotor. With 81,500 units delivered in a single month, it shattered the previous monthly sales ceiling for new entrants, which hovered around 30,000-40,000 units, propelling it to over 80,000 units. Regardless of one's perception of the brand, this achievement signifies its arrival at the mainstream table.

In contrast, Li Auto delivered 33,300 units in May, experiencing a slight year-on-year and month-on-month decline. NIO, on the other hand, delivered 37,700 units, rapidly closing the gap. Harmony Intelligent Mobility is also rebounding swiftly. Now, within the 30,000-40,000 unit range, several brands are locked in fierce competition.

These figures convey a clear message: new entrants selling fewer than 30,000 units per month are at risk of falling behind. Market barriers are escalating rapidly—it's no longer just about the ability to manufacture a car but also about scaling up swiftly, controlling costs, and compelling consumers to choose your brand amidst a plethora of options.

Another stark reality is the overall decline in retail sales, indicating that consumers are either adopting a wait-and-see approach or exercising greater caution in their spending. Price wars continue to rage, and competition in intelligent driving is intensifying, squeezing automakers' profit margins. For second- and third-tier new entrants still reliant on financing and lacking self-sustaining capabilities, the upcoming months will be exceptionally challenging.

Fortunately, exports are gaining momentum. Companies like Chery, BYD, Geely, and SAIC are inundating overseas markets with their vehicles. Geely's exports surged 184% year-on-year in May, while Chery exported over 180,000 units in a single month.

These exports not only offset the weakness in the domestic market but also demonstrate that Chinese cars are no longer synonymous with cheap products. The product strength brought about by new energy and intelligent driving technologies can hold its own on the global stage.

In summary, the auto market in May was characterized by a sluggish overall performance but a surge in NEVs; independent brands were on the offensive, while joint venture brands were on the defensive; strong players continued to strengthen, while weaker ones accelerated their exit. With a 63% penetration rate, the market is no longer about "whether to switch to new energy" but "whether you can keep up." Those who fail to do so will be swiftly eliminated. The brutality of the upcoming months in 2026 will only surpass that of May. Who will emerge victorious in the end? Let's wait and see!

In summary, the auto market in May was characterized by a sluggish overall performance but a surge in NEVs; independent brands were on the offensive, while joint venture brands were on the defensive; strong players continued to strengthen, while weaker ones accelerated their exit. With a 63% penetration rate, the market is no longer about "whether to switch to new energy" but "whether you can keep up." Those who fail to do so will be swiftly eliminated. The brutality of the upcoming months in 2026 will only surpass that of May. Who will emerge victorious in the end? Let's wait and see!

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?

-

![]()

Why Can Vision-Language-Action (VLA) Models Enable Autonomous Driving to Understand the World?

-

![]()

A National Benchmark and a Listing Milestone: Redefining the Humanoid Robot Industry’s Growth Trajectory

-

From Handcrafting to Mass Production: What China's Commercial Space Industry Lacks Is Not Factories