The Large Six-Seater SUV Market: Overhyped and Overrated

06/08 2026

06/08 2026

394

394

Lead-in

Introduction

The large six-seater SUV segment is no longer the golden opportunity it once seemed for all players.

Over the past two years, the pace of reshuffling in China's domestic SUV market has accelerated dramatically, far outpacing previous industry trends.

The traditional landscape of five-seater family SUVs and essential seven-seater models has been gradually disrupted. Large six-seater SUVs, offering flexible seating configurations and premium comfort, have swiftly risen to prominence as the most sought-after and fiercely contested segment among automakers.

Leveraging their spacious interiors, balanced practicality, and high-end features, these vehicles have quickly won over consumers looking to upgrade or expand their vehicle fleet. By 2025, domestic sales of large six-seater SUVs had surpassed the one million mark, with remarkable year-on-year growth, becoming a key pillar supporting the expansion of the mid-to-large-sized new energy SUV market.

These better-than-expected annual results have fostered a unanimous sense of optimism across the industry toward the large six-seater segment, directly triggering an unprecedented wave of new vehicle launches in 2026. As we entered 2026, nearly all manufacturers, from independent premium brands to mainstream joint-venture automakers, have designated large six-seater SUVs as their strategic models for the year, aiming to capitalize on new market opportunities in this positioning battle.

Five months ago, the industry widely predicted that the large six-seater market would continue its rapid expansion. However, real-world sales trends are gradually dismantling this optimistic consensus.

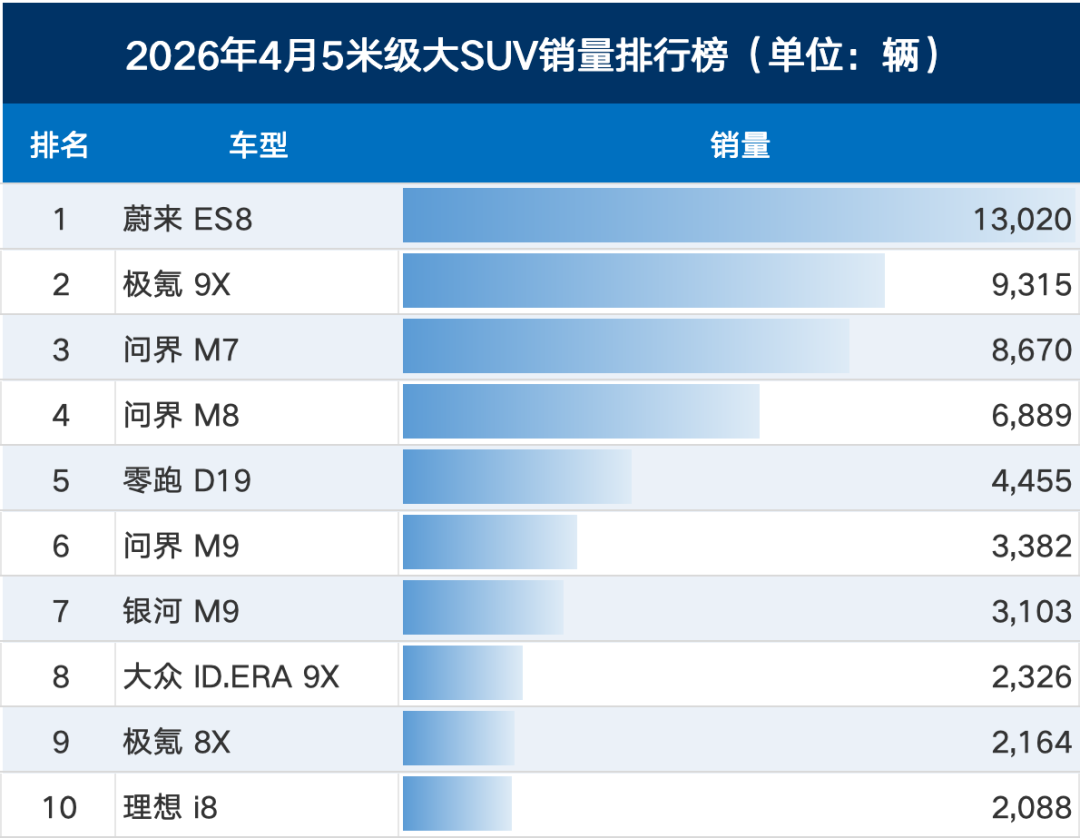

Based on the latest sales data from April 2026, signs of growth fatigue in the large six-seater SUV segment have become apparent, with market hype showing clear signs of being overblown. Data reveals that in April this year, only the NIO ES8 achieved monthly sales exceeding 10,000 units among large six-seater SUVs, while other popular models failed to achieve significant sales breakthroughs.

It is evident that despite the constant introduction of new large six-seater products and sustained media buzz, the overall segment size has stagnated, with growth reaching its peak. On one hand, automakers are increasing their investments and launching new models rapidly; on the other hand, terminal market growth has stalled, raising the question: Has the large six-seater SUV segment been overrated from the start?

01 Overall Cooling of the Large Six-Seater Segment

If we set aside media hype and automaker investment noise and focus on real terminal transaction data, the growth dilemma in the large six-seater segment has been periodically exposed.

In the first four months of this year, cumulative sales of large six-seater SUVs not only failed to grow compared to the same period in 2025 but also declined significantly. Public data shows that cumulative sales of large six-seater SUVs in the first four months of 2026 reached approximately 432,200 units, down 14.24% year-on-year. This indicates that despite strong performance in 2025, demand in 2026 has weakened, pushing the segment into overall negative growth.

Under these circumstances, while monthly sales of most large six-seater models like the Li Auto L8, NIO ES8, and Leapmotor C16 have maintained certain levels this year, their cumulative year-on-year growth rates from January to April have turned negative, signaling an industry-wide adjustment phase.

Taking the most recent April as an example, a closer look at the top 10 best-selling large six-seater SUVs reveals a growing trend of polarization, leaving little room for smaller players. Only the NIO ES8 achieved monthly sales exceeding 10,000 units, becoming the sole model to break this threshold. Moreover, only four models—the NIO ES8, Zeekr 9X, Aito M9, and Aito M8—surpassed 5,000 units in sales. The remaining models on the list showed "mediocre" sales, such as the Li Auto i8, which ranked tenth with monthly sales hovering around 2,000 units.

For a large six-seater SUV, such performance by leading models is severely mismatched with the market attention they receive, placing them in an awkward position.

However, the lackluster terminal sales contrast sharply with the industry's fervent new product launches. Since 2026, new large six-seater SUV models have been launching rapidly, with offerings such as the Volkswagen ID.ERA 9X, Wey V9X, Yijing X9, and XPeng GX spanning various price bands and powertrain types, attempting to fill every niche in the segment.

Not only have new models flooded the market in the first half of the year, but several heavyweight large six-seater SUVs are also poised to launch in the second half, further crowding this segment. According to incomplete statistics, in 2026 alone, the number of newly launched mid-to-high-end large six-seater SUVs priced above RMB 250,000 will exceed 20, setting a new record for annual new product launches.

Given the current situation, the large six-seater market has already attracted significant resources from mainstream domestic automakers. Leading brands such as Li Auto, Chery, BYD, XPeng, NIO, Leapmotor, Aito, and Voyah have all entered the fray, viewing large six-seater SUVs as their core growth segment for the year. In automakers' strategic plans, the large six-seater segment has become the most certain high-potential market, prompting them to invest heavily in R&D, production capacity, and marketing resources to compete.

However, the reality is that the market pie is no longer growing, yet more players are entering, leading to increased product saturation and continuous fragmentation of the limited existing market. The top four best-selling models dominate the majority of segment sales, leaving lower-ranked models to vie for the remaining scattered market share. Most new models struggle to gain traction upon launch, making it difficult to achieve significant sales breakthroughs.

This contradiction has caused the market hype around large six-seater SUVs to cool down temporarily, confirming that the industry's earlier optimistic predictions were detached from real terminal consumer fundamentals.

02 Competitive Logic Has Changed, Making Breakthroughs Even Harder

In fact, beyond the stagnation in market growth, the survival conditions in the large six-seater segment are even more severe than the data suggests. The industry has not only overestimated the segment's growth potential but also long overlooked the internal competitive risks within the segment.

Today's large six-seater market has moved far beyond the early stage where differentiation in design and unique configurations could guarantee success. In fact, the competitive logic of this segment has completely changed, with homogenization, endless price wars, and market uncertainty becoming major pain points restricting the development of the large six-seater market and all other niche markets.

At this year's Beijing Auto Show, some industry media jokingly remarked that "only one large six-seater SUV was actually launched at this year's show." This quip exposed a major flaw in the current large six-seater segment: severe product homogenization. A previous article by

Moreover, homogenization is not limited to exterior and interior similarities but extends to all aspects of the vehicle.

Currently, mainstream large six-seater SUVs on the market share almost no fundamental differences in core hardware and intelligent configurations: many uniformly adopt CATL's full range of battery cells, rely heavily on leading suppliers like Huawei and Momenta for high-level intelligent driving solutions, resulting in highly similar functions and interaction logic in their intelligent cockpits. Even core performance parameters such as zero-to-100 km/h acceleration, range, and overall vehicle energy consumption are largely on par.

For ordinary consumers, faced with a dazzling array of new large six-seater models, it is nearly impossible to find products with significant competitive advantages, making choices difficult. When the core product strengths of most models are on equal footing, competition in the large six-seater segment shifts entirely toward price-based internal competition—essentially, whoever offers a lower price has a better chance of selling well.

As a result, automakers can only compete for existing users through price cuts, value-added configurations without price hikes, and limited-time offers, continuously compressing the industry's overall profit margins and undermining a healthy ecosystem for product iteration and market competition.

Entering the second quarter of 2026, the internal competition in the large six-seater segment has further intensified, with price reductions reshaping the original premium market landscape.

Large six-seater models that once focused on premium capabilities and were concentrated in the mid-to-high-end market now feature numerous highly competitive models priced below RMB 200,000. Models like the Wuling Huajing S and Yipai M8, equipped with Huawei's full suite of intelligent cockpit and driving assistance "packages," have entered the market at affordable prices, offering superior configurations and extreme cost-effectiveness, posing a strong challenge to higher-priced large six-seater models.

To be fair, price reductions have allowed consumers to enjoy the dividends of industry internal competition, lowering the entry barrier for high-quality large six-seater SUVs. However, they have also made the already saturated and crowded segment even more disorderly, further increasing survival pressure on smaller players.

Under the combined effect of multiple industry variables, uncertainty in the large six-seater market continues to rise, shattering the industry's earlier confident high-growth expectations.

Of course, the cooling of hype does not mean the segment has completely lost its opportunities. The rigid demand for family travel with multiple occupants remains, and users' desire to upgrade their vehicles has not faded. However, from the current industry trends, the era of extensive dividends in the large six-seater segment seems to have ended.

The future of the segment will enter a brutal ultimate competition for existing market share, with the core focus shifting to the pure electric large six-seater SUV market in the RMB 200,000-500,000 mainstream price range.

Based on this, some industry insiders predict that going forward, whoever can establish a stable best-selling model with monthly sales exceeding 10,000 units across the four corresponding sub-price bands of RMB 200,000-500,000 will be more likely to break through. Of course, based on current performance, NIO, with its ES8, is temporarily half a step ahead, while Li Auto and Aito are also making sustained efforts and closing in.

In comparison, most other players in the segment have yet to form a stable system of best-selling products, making future breakthroughs even more challenging.

Editor-in-Charge: Li Sijia Editor: He Zengrong

THE END

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?