Tariffs Can't Stop Chinese Cars—EU Starts Rewriting the Rules: From Anti-Subsidy Duties to 'Made in Europe' and Beyond

06/08 2026

06/08 2026

522

522

A year and a half after the EU imposed tariffs on Chinese EVs, imports of Chinese cars have continued to rise rather than fall, while EU member states remain divided over whether to 'add another line of defense.'

The European Commission's latest and most ambitious response—the Industrial Accelerator Act (IAA)—seeks to link public subsidies to local content requirements in an effort to slow the influx of Chinese cars. However, a very real question remains: Even if implemented in its strongest form, this measure may not be enough to stop Chinese automakers.

This article provides an overall analysis of the current sales performance of Chinese automobiles in Europe based on the latest data and policy developments, and explores potential further measures that Europe may take.

I. Chinese Automobiles Advancing at Light Speed

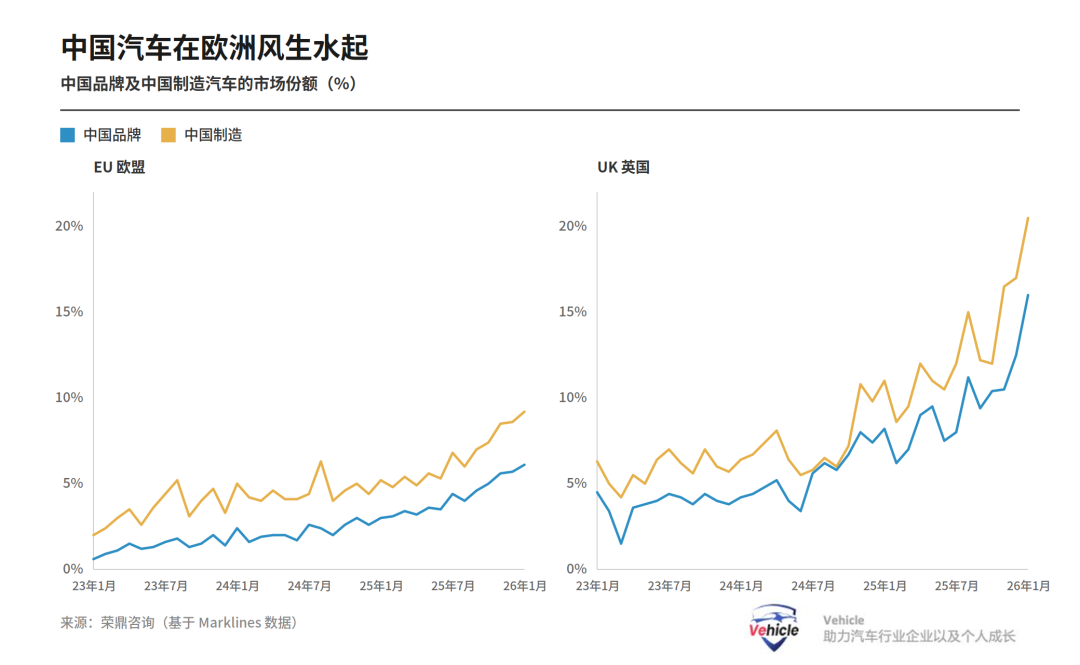

The Chinese auto market is fiercely competitive, as detailed in our previous article, 'The Truth About China's Auto Market in April: Sales Dip 2.5%, Exports Soar 74%, Profit Margins Drop Below 3.5%.' However, Chinese automakers are thriving in Europe. In December last year, a record 9.3% of new car sales in the EU were produced in China; in the UK, this figure reached an astonishing 20.6%. For the full year, Chinese-made models accounted for 6.4% of EU sales and 12.1% of UK sales.

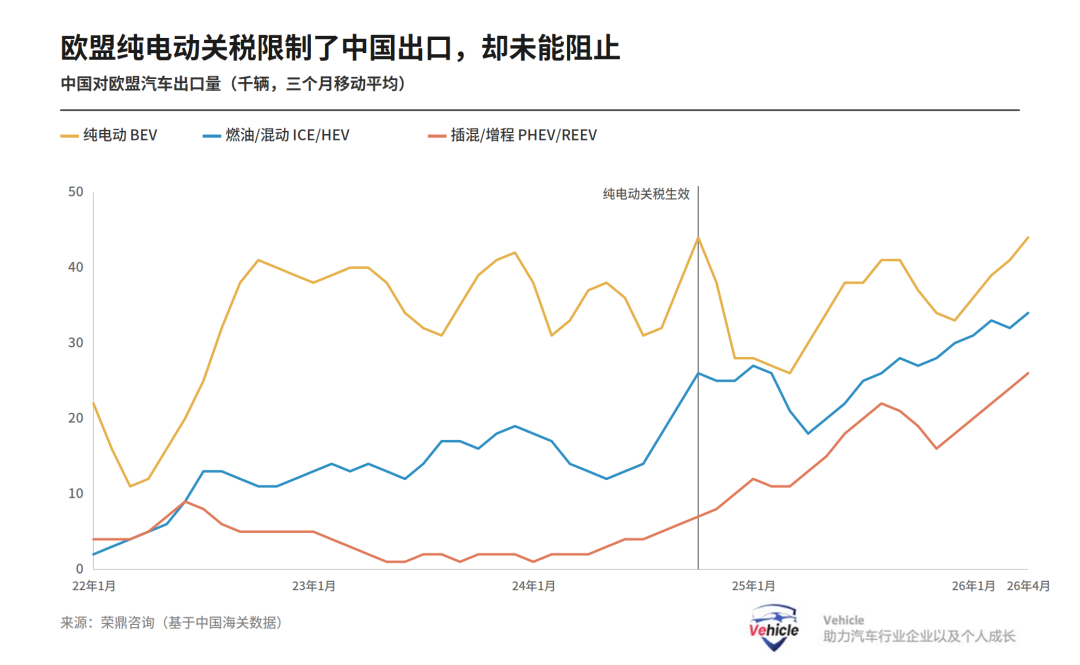

What is even more noteworthy is that these achievements were made despite EU anti-subsidy tariffs. The anti-subsidy duties on Chinese-made battery electric vehicles (BEVs) took effect in October 2024 and briefly slowed export momentum at the end of 2024, but shipments have since returned to pre-tariff levels.

Meanwhile, exports of internal combustion engine (ICE) vehicles and plug-in hybrid electric vehicles (PHEVs), which are not subject to the tariffs, have risen rapidly. As a result, total passenger car exports from China reached 922,000 units, up 29% year-on-year. In 2026, the momentum accelerated further—with 214,000 units exported in the first two months alone, a 62% year-on-year surge.

Rewriting the Rules of History

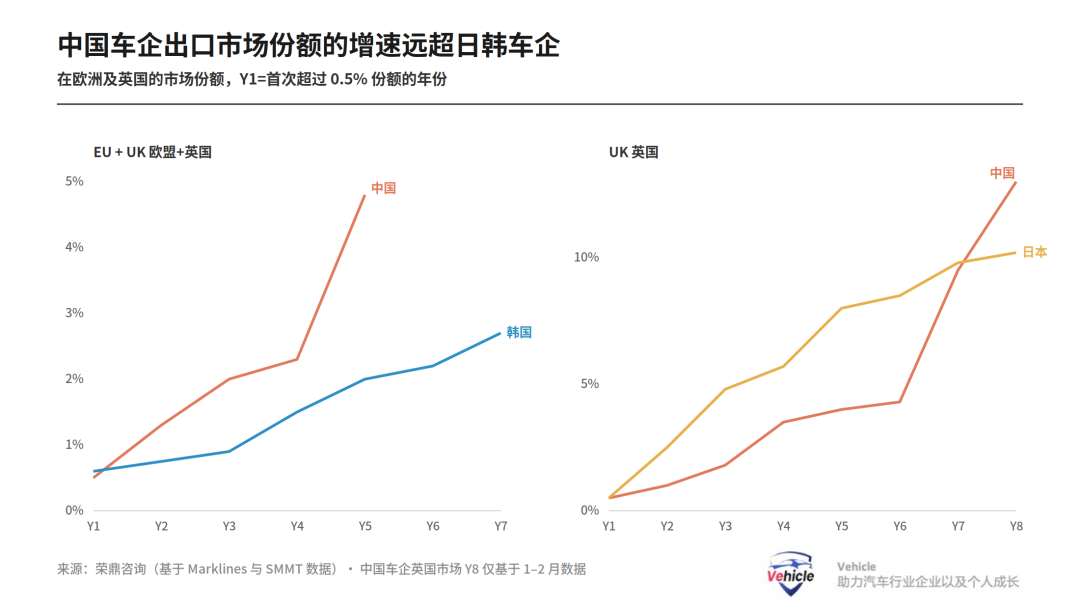

The speed at which Chinese automakers—particularly BYD, Chery, and SAIC—are gaining ground in Europe is unprecedented. It differs fundamentally from the paths taken by Japanese automakers in the 1970s and South Korean automakers in the 1990s when they entered the European market.

Several factors explain this acceleration.

First, the number of Chinese brands entering Europe simultaneously is far greater than that of their Japanese and South Korean counterparts in the past.

Second, Chinese automakers have much larger production capacities, enabling rapid scaling—especially against the backdrop of prolonged price wars in the domestic market.

Third, with the U.S. market largely closed to China, exports are concentrated on the more profitable European market. Additionally, EV subsidies in Europe provide an extra boost to Chinese manufacturers.

This trend is further amplified by the fact that not only East Asian automakers but also Western automakers are using China as an export base, increasing pressure on the European auto industry.

All of this weighs heavily on European automakers and suppliers—whose orders depend on the survival of local OEMs.

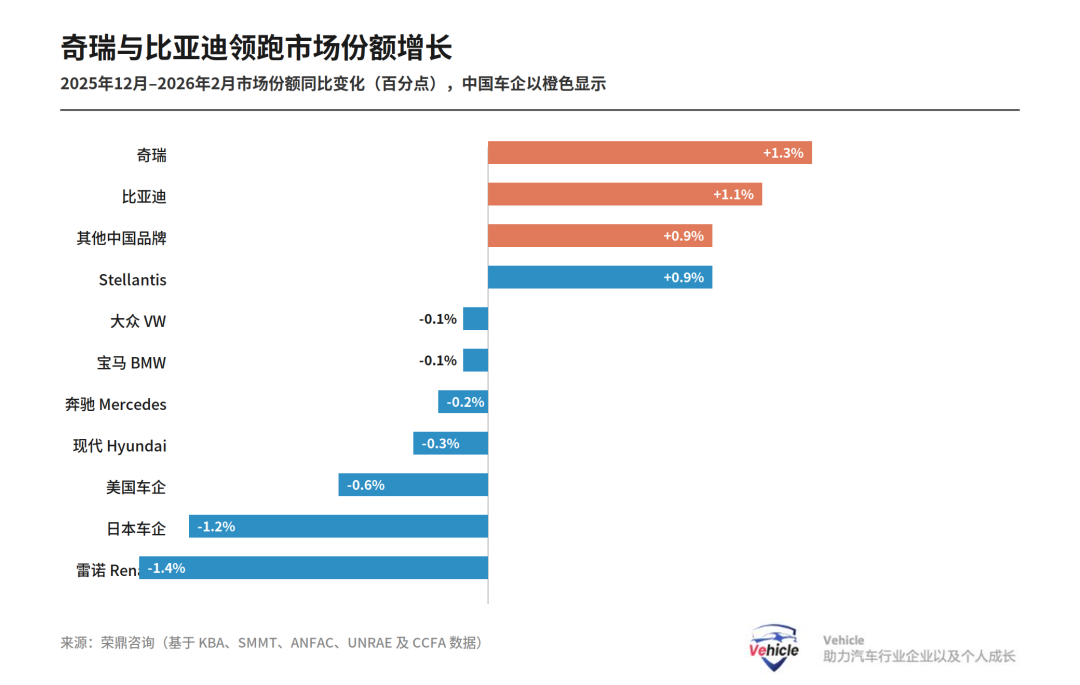

In Europe's top five markets (France, Germany, Italy, Spain, and the UK), Chinese brands gained 3.3 percentage points of market share in just three months (from December last year to February this year). Annualized, this equates to about 357,000 units, roughly the output of one and a half assembly plants.

Nothing Can Stop Them

What is even more unsettling for the European industry is that, without further policy action, there is little reason to expect a slowdown in Chinese exports in the short term.

China's domestic auto market is entering a phase of weakening growth, while production capacity remains high;

The Chinese yuan is weak against the euro, boosting the price competitiveness of Chinese cars;

Even with the EU's additional EV tariffs, these measures have failed to curb the pace of Chinese automakers going global.

Export momentum is clearly visible in corporate data. BYD's overseas sales recently surpassed its domestic sales for the first time. Seasonal factors such as the Lunar New Year may have affected the numbers, but the overall trend is clear: Chinese automakers are increasingly relying on overseas markets for growth.

At the same time, more Chinese automakers are including Europe in their export plans; even Japanese automakers like Nissan and Mazda are restructuring their Chinese operations to expand exports, with the EU as one of the destinations;

Some manufacturers are also establishing export platforms outside China—certain Chinese automakers have already started exporting complete vehicles from Thailand to the EU.

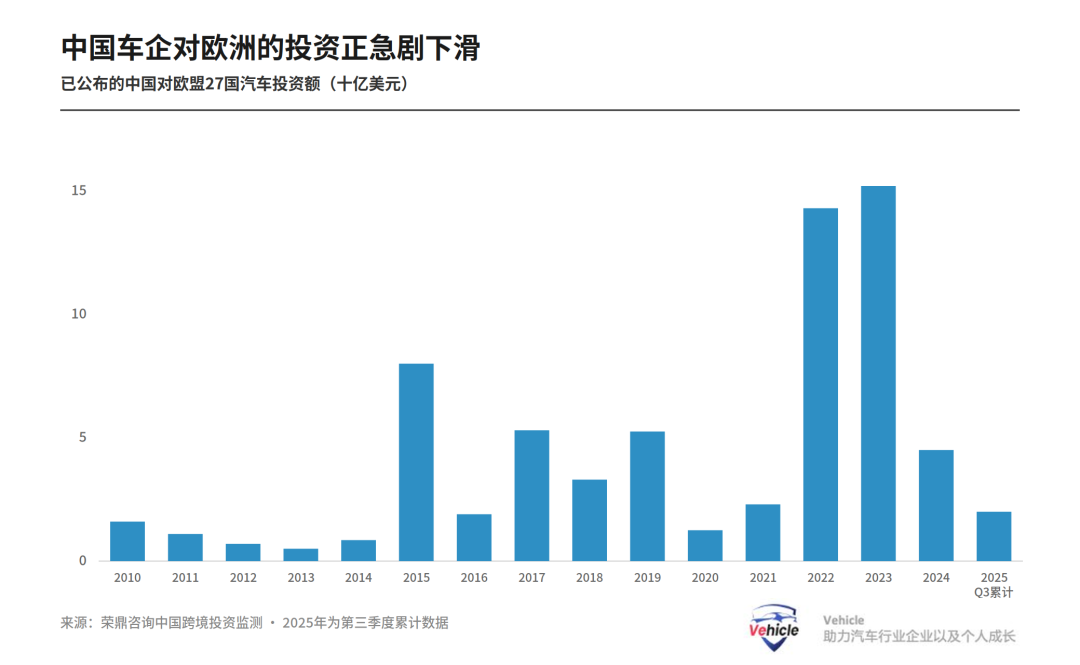

An interesting counter-signal is that Chinese complete vehicle (complete vehicle) investments in Europe are slowing down. After a flurry of new project announcements in 2022 and 2023, investment announcements have dropped sharply. The reason is that, given regulatory uncertainties within the EU, automakers view 'exports' as a more profitable and predictable entry strategy. Apart from BYD's Hungarian plant, which is expected to start production in the coming months, no other Chinese automakers have announced plans to build full-scale production bases in the EU.

In the future, automakers may prefer joint ventures or mergers and acquisitions over greenfield investments—given the overcapacity in the European auto industry, this makes economic sense and allows for faster market entry.

However, most of these efforts are still in their early stages: Geely is reportedly in talks with Ford about using its production capacity in Spain; Chery is exploring cooperation with Jaguar Land Rover (JLR) in the UK; although BYD has denied plans to buy Maserati or a Stellantis plant, such moves cannot be ruled out. Leapmotor has already formed a joint venture with Stellantis to utilize its production facilities.

Minimum Price Commitments Won't Change the Big Picture

There is concern that the European Commission may inadvertently open the door wider by providing guidelines for 'minimum price commitments' to Chinese EV exporters. However, this scenario is unlikely. The process began when Volkswagen Anhui—a Sino-foreign joint venture exporting the Cupra Tavascan model—applied for a review of EV tariffs. After consultations with China's Ministry of Commerce (which has consistently opposed 'enterprise-by-enterprise' price commitments), the Commission issued guidelines explaining how exporters could apply for minimum import prices (MIPs).

Volkswagen Anhui subsequently received a quota-limited MIP arrangement. However, it is unlikely that a large number of Chinese automakers will secure similar arrangements.

First, Chinese exporters value pricing flexibility in the European market and currently prioritize volume over profit margins; price commitments would restrict their ability to offer discounts and promotions. For example, BYD is currently offering significant discounts in Germany by combining national subsidies with manufacturer incentives; once a price commitment is signed, the manufacturer's suggested retail price (MSRP) and various discounts would need to be factored in, making such promotions unsustainable.

Second, European automakers like Volkswagen and BMW, which export only one or two models from China, are in a stronger position to negotiate price commitments than their Chinese counterparts—according to the Commission, the simpler the model lineup, the clearer the data, and the more sustained the investment in Europe, the easier it is to secure such arrangements. In contrast, Chinese exporters often have vast and complex model lineups and limited investment in Europe. Many Chinese companies export both BEVs and PHEVs, making it harder for them to obtain price commitments; the Commission is concerned about 'cross-subsidization'—using profits from PHEVs or ICE vehicles (which enter the EU at a 10% MFN tariff) to offset losses on EV exports. Therefore, while many Chinese automakers may attempt to secure price commitments, only a few are expected to succeed.

II. Why Europe's 'Local Content' Gambit May Also Fail

The automotive industry is a major employer, a key driver of R&D, an important investor, and a significant contributor to the EU's trade surplus. This weight is why the European Commission initially launched an ex officio investigation into Chinese EVs.

However, two years on, the consensus is that these traditional trade tools have been ineffective and risk escalating confrontation. As a result, the Commission has shifted toward more protectionist and broad-based industrial policies.

In March 2026, under the leadership of EU Commissioner Stéphane Séjourné, the proposed Industrial Accelerator Act (IAA) introduced local content requirements for a range of industries, including automotive. For details, see our previous article, 'A Deep Dive into the EU's Industrial Accelerator Act: Rewriting the Rules for China's Auto Industry Going Global.'

The core idea is to link public financial support for vehicle purchases to 'Made in Europe' (MiEU) standards. Certain 'trusted partners'—such as the U.S., UK, South Korea, and Japan—would be partially integrated into this framework, while China is clearly excluded.

In addition to putting Chinese-made models at a disadvantage in Europe, the local content push addresses a second concern: Europe's growing dependence on Chinese components for vehicle production. As Europe transitions to electrification and struggles to build a competitive battery industry, local automakers are increasingly sourcing from China—not just batteries and electric drivetrains but also a wide range of low- and medium-value components.

For example, Renault plans to produce its new E-Twingo in Slovenia using Chinese batteries and electric drivetrains, likely along with other electronic components sourced from China. Even Chinese automakers with factories in Europe (such as BYD) may have low local value-added if left unchecked—after all, this is the foundation of their competitive advantage. Compared to imports of finished vehicles, this gradual increase in component sourcing poses a more structural risk to Europe's supplier base.

The European Commission's Vision for Local Content in Autos

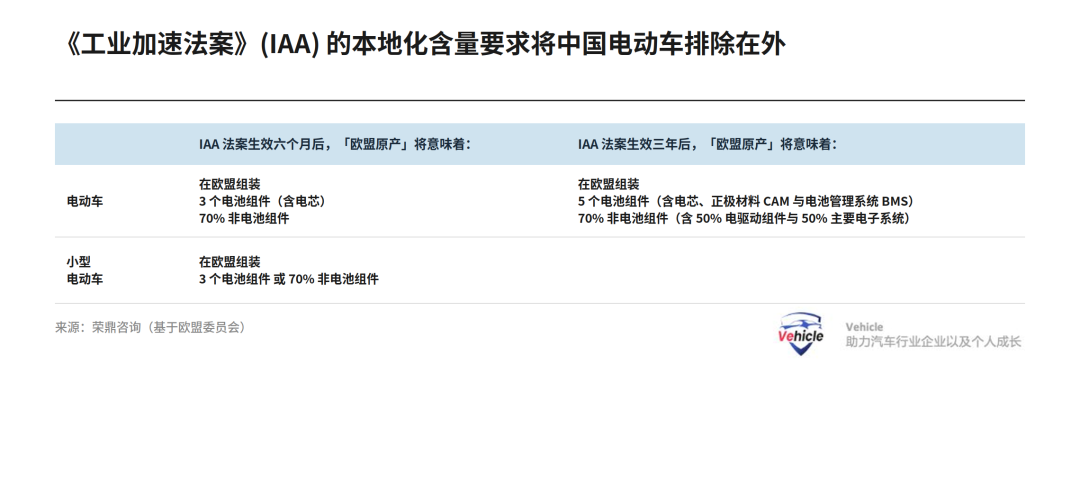

Essentially, the Commission aims to define 'what qualifies as a MiEU vehicle.' This framework applies to low-emission vehicles and sets a series of threshold requirements.

These thresholds would clearly exclude vehicles assembled in China and pose significant obstacles even for Chinese automakers producing in the EU.

Take BYD as an example: it has not yet announced plans to localize battery cell production in Europe and would likely fail to meet battery-related thresholds;

Chery's assembly operations in Barcelona and XPENG's and GAC's operations in Graz would also struggle to comply.

It is worth noting that many non-Chinese automakers would also find it difficult to meet these thresholds—which could render the entire framework meaningless.

Beyond setting content thresholds and defining 'who counts as part of the EU club,' the core challenge is how to enforce these requirements in the automotive industry. This is not straightforward. Since cars are primarily purchased by private consumers, the EU would find it difficult to prevent consumers from buying cheaper, non-compliant models if they are available.

Therefore, the Séjourné team has focused on 'linking incentives.' Once the IAA is finalized and the transition period ends, the EU will require member states to: procure only MiEU models for government fleets; limit fiscal incentives (including purchase subsidies and corporate fleet incentives) to MiEU models; and restrict CO super-credit benefits to MiEU small BEVs.

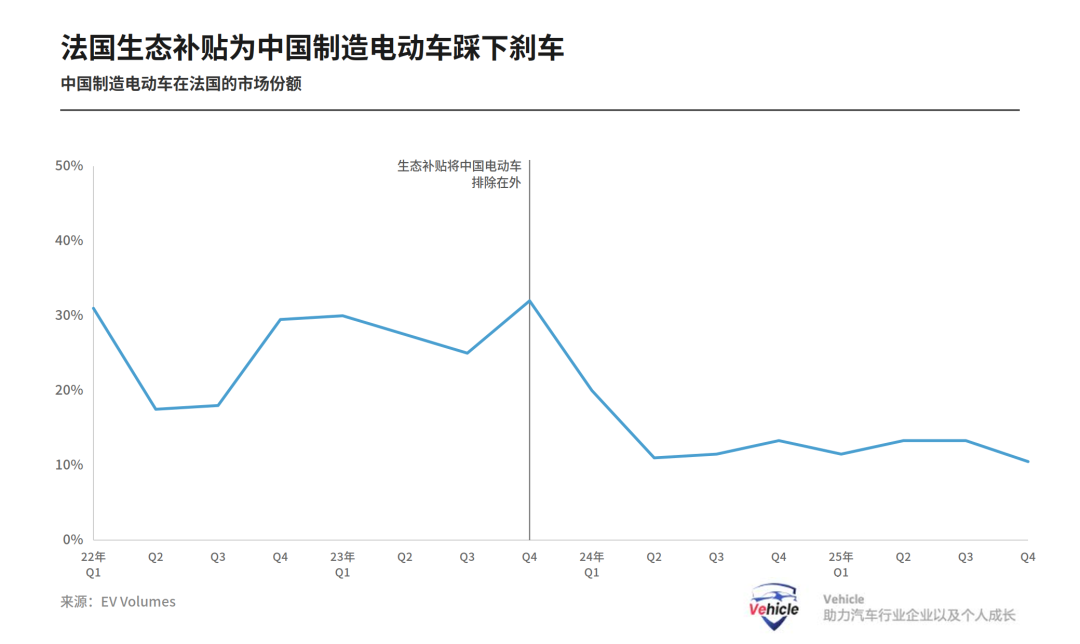

This would not drive Chinese (or other) automakers out of the European market but would exclude them from fiscal incentives, putting them at a clear disadvantage. If fully implemented, this would be a formidable barrier—much like France's 'bonus écologique,' which has excluded East Asian-produced EVs since December 2023 on the grounds of excessive emissions in production and transportation.

However, the IAA's effectiveness faces several key limitations—and these are precisely the 'windows of opportunity' that Chinese automakers should understand.

Firstly, timing. Even on an optimistic timeline, these measures are unlikely to take effect before mid-2027—or even 2028. That means Chinese exporters have at least 18 to 24 months of relatively unrestricted access to the EU market.

Second, many tools are limited in scale or irrelevant to Chinese players. Government procurement accounts for less than 2% of passenger-car demand, making it negligible for Chinese automakers. Small super-credits for zero-emission vehicles (ZEVs) and low-carbon steel requirements matter more to legacy European automakers than to Chinese firms, whose fleets are typically better balanced on carbon emissions and less reliant on super-credits. That said, not all Chinese players are equally insulated: SAIC MG and Chery, which still sell meaningful volumes of internal-combustion vehicles in the EU, may face greater pressure.

Third, private demand is only partially covered. Linking purchase subsidies to local content can be highly effective (France’s ecological bonus already proves the point), but only about half of EU member states offer such support; even in large markets, coverage is limited. The German government estimates its €3 billion electric-vehicle subsidy scheme from 2026—2029 will support around 800,000 vehicles, covering roughly 20% of private demand but only about 7% of total market demand. Conversely, that means 80% of private demand remains open to Chinese competitors—and such subsidies themselves are likely to be phased out over time.

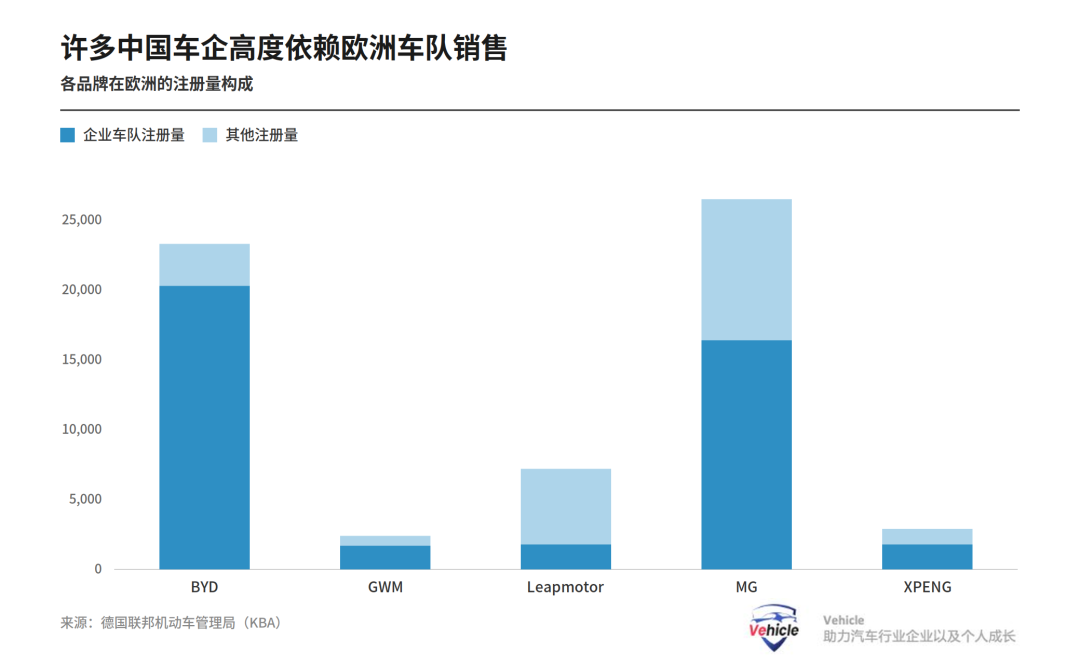

Fourth, the most impactful corporate-fleet scheme risks getting stuck in trilateral negotiations. Corporate fleets account for around 60% of new-car sales in the EU and enjoy generous fiscal incentives, with Chinese automakers relying heavily on this channel as an entry point.

Article 4 of the EU’s Corporate Fleets Proposal is particularly critical: from 2028, member states will only be allowed to provide financial support to corporate fleets if it backs low-emission, EU-made vehicles. If implemented as drafted, this will not lock Chinese exporters out of the largest demand segment entirely, but it will put them at a significant disadvantage. Transport & Environment estimates corporate tax incentives for electric vehicles are substantial: averaging around €1,500 per year in large member states and rising to roughly €3,500 per year in Germany.

The corporate-fleet scheme, however, faces strong opposition. Automotive leaders, including BMW chairman Oliver Zipse, have called it a “backdoor combustion-engine ban” and urged member states and the European Parliament to water it down; Germany’s VDA industry association has criticized the initiative as unrealistic. Automakers are especially opposed to mandatory quotas that require member states to accelerate low-emission fleet penetration by 2030 and 2035—such as Germany’s targets of 56% by 2030 and 95% by 2035. The Italian government and Germany’s center-right CDU are among the fiercest opponents.

Yet even now, around 30% of the market remains fully open. And even within protected segments, automakers will face higher costs to maintain subsidy eligibility—because of local-content requirements. Currently, fewer than two-thirds of vehicles produced by European automakers use EU-made battery cells, which will become a critical eligibility threshold.

This creates a clear trade-off: battery-cell production costs are roughly 30% lower in China; the International Energy Agency (IEA) estimates total production costs for a small battery-electric vehicle are nearly $10,000 lower in China than in Germany. Such cost advantages may well keep Chinese players exporting—even if they face tariffs and are excluded from fiscal incentives.

III. Head-on Collision: If the IAA Is Not Enough, What Else Is in the Arsenal?

If the Industrial Acceleration Act, along with the broader EU automotive policy toolkit, still fails to slow China’s market-share gains—and pressure on Europe’s auto manufacturing base keeps building—the likelihood of additional policy tools being deployed will rise.

Tool One: More Tariffs.

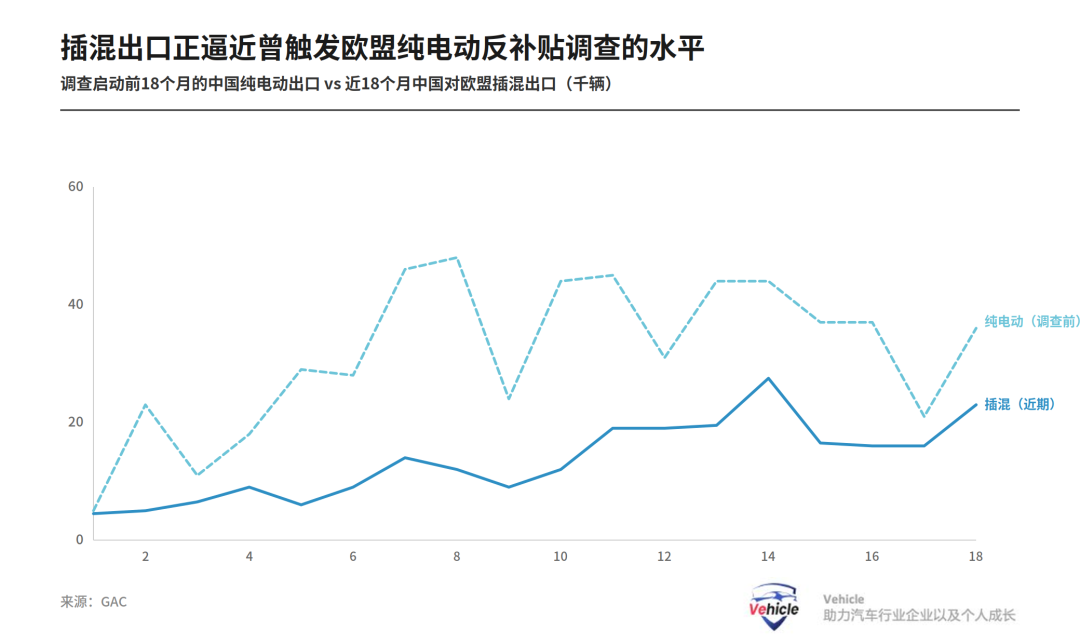

The Séjourné cabinet is already pushing for further trade-defense measures on plug-in hybrid electric vehicles (PHEVs), whose imports have surged in recent months. Resistance remains within the Commission, but it could fade if Chinese exports keep rising or if the IAA is weakened.

Several potential paths exist for PHEV imports, each with different legal thresholds, timelines, and political trade-offs:

Anti-circumvention measures: The Commission could argue that Chinese automakers are shifting to PHEVs to avoid pure-electric tariffs and extend existing pure-electric duties to these models. This would be the fastest route, but the Commission must demonstrate a link between “changed trade patterns” and the original duties. Given consumers may choose PHEVs for other reasons, such as range anxiety, this path is not straightforward.

New anti-dumping cases: Even if EU prices are higher than Chinese prices, the Commission could still construct a “normal value” using third-country benchmarks, as it has in past cases against China. This is legally viable but more escalatory—easily pushing duties into double or even triple digits.

Parallel countervailing duty (CVD) investigations: New CVD cases are also possible but time-consuming, and duties may be lower—since battery-related subsidies, which were central to the pure-electric case, matter less for PHEVs; moreover, some subsidies already addressed in the electric-vehicle case may not be reusable in a new investigation.

Safeguard measures: If a surge in imports can be proven, temporary duties could be imposed on all PHEV imports. But safeguards generally apply on a most-favored-nation (MFN) basis, hitting Japan, Turkey, and the U.S. as well—not just China (which accounts for roughly 45% of EU PHEV imports).

For now, though, the Commission is not united on further trade action. The electric-vehicle trade case against China was subsequently seen as politically costly and only partly effective: China retaliated against European dairy, pork, and cognac and holds leverage on critical raw materials. Meanwhile, although concerns over Chinese car imports are rising, PHEV imports have not yet reached the “surge” levels that triggered the pure-electric investigation—though they are very close.

Over-reliance: Resilience and Green Standards

Beyond local-content requirements, the Commission and member states can deploy other tools to constrain or disadvantage Chinese exporters. One is the use of environmental or resilience-related “non-price” standards. France and the U.K. have already tightened their electric-vehicle subsidy schemes based on environmental criteria. This approach is less targeted than local-content requirements but ultimately points to a similar outcome: favoring vehicles produced in Europe.

Under the EU’s Net-Zero Industry Act (NZIA), such non-price standards are no longer entirely optional. From 2026, member states must include a “resilience” test in public support schemes—that is, an examination of whether a technology’s supply chain is overly dependent on a single non-EU country. If more than 50% of EU supply for a given technology—or for key electric-vehicle components such as batteries, electric motors, or magnets—comes from the same country, governments must take this into account when granting support. In practice, this could limit or reduce subsidies for products highly dependent on that country, most obviously China.

If the IAA proves ineffective, the Commission and some member states, notably France, may push to apply these rules more broadly—including to schemes such as corporate fleets.

Cybersecurity as the “Nuclear Option”: The Atomic Bomb of Sniper Attacks

A final—and potentially far more restrictive—option is greater recourse to cybersecurity rules to limit Chinese automakers’ access to the European market. The U.S. has already gone down this path: through ICTS rules for connected vehicles, Washington will ban sales in the U.S. market from model year 2027 of vehicles produced in China, manufactured by Chinese automakers, or using certain Chinese components.

Related concerns are rising in Europe, too. Several EU member states have already excluded Chinese suppliers from their 5G telecom networks, and scrutiny of Chinese connected vehicles is intensifying. In 2026, Poland banned Chinese-made cars from certain military sites; a Norwegian public-transport operator, after discovering that Chinese-made electric buses could be remotely shut down by the manufacturer, announced tougher safety requirements—a move that triggered similar investigations in Denmark and the U.K.

The EU is seeking powers similar to the U.S. ICTS framework. In a proposal to revise the Cybersecurity Act (CSA), the Commission wants the power to “require member states to impose restrictions on high-risk suppliers, including in the connected-vehicle supply chain.” Given Chinese law requires firms to share information with the government, Chinese companies are likely to be viewed as less trustworthy. A cybersecurity risk assessment led by the Commission in February 2026 identified several risks linked to so-called “non-technical” factors—such as potential state interference or sabotage—and recommended that member states take steps to limit or exclude high-risk suppliers from critical supply chains.

The CSA remains only a proposal and is likely to take 18 to 24 months to take effect, if at all. As with the automotive policy toolkit and the IAA, strong opposition from member states is inevitable: governments are wary of the Commission encroaching on their national-security prerogatives and fear the economic costs of excluding Chinese suppliers, including the risk of Chinese retaliation.

That said, even if member states do not back the Commission’s current, aggressive draft, those with cybersecurity concerns may still grant the Commission greater powers to restrict high-risk suppliers—including tighter controls on cross-border data transfers and requirements that connected vehicles use “trustworthy” software and suppliers. Such measures would significantly weaken Chinese automakers’ competitiveness in Europe by raising the price of critical technology inputs.

The Commission could also use its powers over vehicle type approval—a technical certification process—to factor certain non-technical security-risk considerations into approval standards.

Finally, individual member states may act unilaterally. If restrictions are narrow (e.g., Poland’s limits to military facilities), the impact on the single market will be relatively limited; broader restrictions on Chinese-made vehicles or those using Chinese components, however, could fragment the EU automotive market and unravel the single market.

Final Thoughts

What the EU faces now is not just a question of whether Chinese cars are cheap, but whether Europe’s automotive industry can continue to set the rules.

If tariffs fail, local-content requirements will take center stage; if those are insufficient, PHEV tariffs, supply-chain resilience rules, and cybersecurity reviews could all be ramped up further.

But with each step forward, the EU will pay a higher price: pricier cars, slower electrification, and greater Sino-European friction. For Chinese automakers, the real window of opportunity is not “Europe has no defenses,” but “Europe has not yet figured out how to build them.” These 18 to 24 months may well be the critical period for Chinese cars to reshape the landscape in Europe.

Lastly, for inquiries regarding the impact of the IAA Act on Chinese automakers’ global expansion, feel free to contact Vehicle via our backend.

Source: This article primarily references Rhodium Group’s “Don’t Hold Me Back: Chinese Cars Are Making Waves in Europe,” with data and insights sourced from Rhodium Group.

*Unauthorized reproduction or excerpting is strictly prohibited.-

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?

-

![]()

Why Can Vision-Language-Action (VLA) Models Enable Autonomous Driving to Understand the World?

-

![]()

A National Benchmark and a Listing Milestone: Redefining the Humanoid Robot Industry’s Growth Trajectory

-

From Handcrafting to Mass Production: What China's Commercial Space Industry Lacks Is Not Factories