Has the Auto Market Reached Its Lowest Point and Started to Recover? CAAM: Domestic Demand Faces Pressure, but Foreign Trade Remains Robust

06/11 2026

06/11 2026

484

484

In the blink of an eye, half of 2026 has already elapsed. Although the semi-annual market data is yet to be released, it appears that the sluggish auto market may have begun to bottom out and show signs of recovery.

On June 10, the China Association of Automobile Manufacturers (CAAM) unveiled the production and sales figures for the automobile market in May, summarizing the overall market scenario as "domestic demand under pressure, yet foreign trade robust." According to CAAM's analysis, "In May, automobile production and sales saw a month-on-month increase but a slight year-on-year decrease. Influenced by various factors such as policy adjustments, shifts in market structure, and macroeconomic pressures, the domestic market continued to experience a double-digit decline year-on-year. However, exports remained strong and continued to grow rapidly... The industry is grappling with multiple challenges, including insufficient domestic demand, high costs, and external shocks."

The contrasting market conditions between "domestic demand" and "overseas" are not what everyone had hoped for. The slight month-on-month increase in CAAM's data is the "glimmer of hope" that everyone is looking for. Could it be that the auto market has hit its lowest point in May?

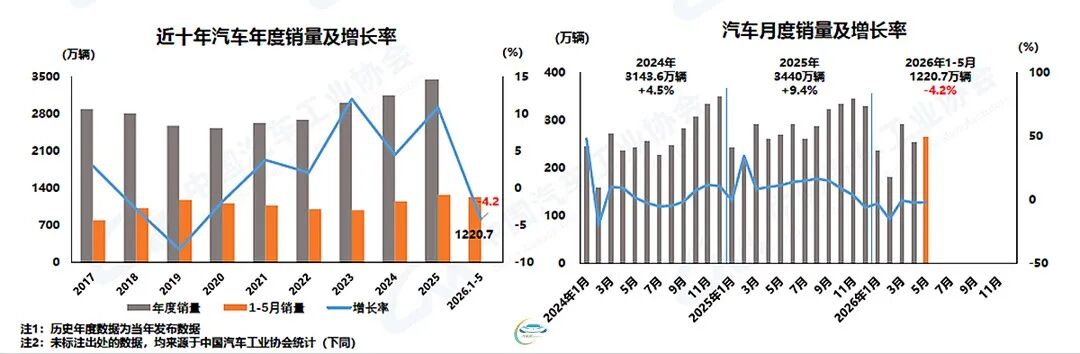

According to CAAM data, in May, automobile production and sales reached 2.616 million and 2.629 million units, respectively, marking a 1.6% and 4.1% increase month-on-month, but a 1.2% and 2.1% decrease year-on-year. Looking at the cumulative data from January to May, automobile production and sales stood at 12.235 million and 12.207 million units, respectively, down 4.6% and 4.2% year-on-year, with the decline narrowing further compared to the first four months.

Of course, this data encompasses the entire auto market, including the growing commercial vehicle and export sectors.

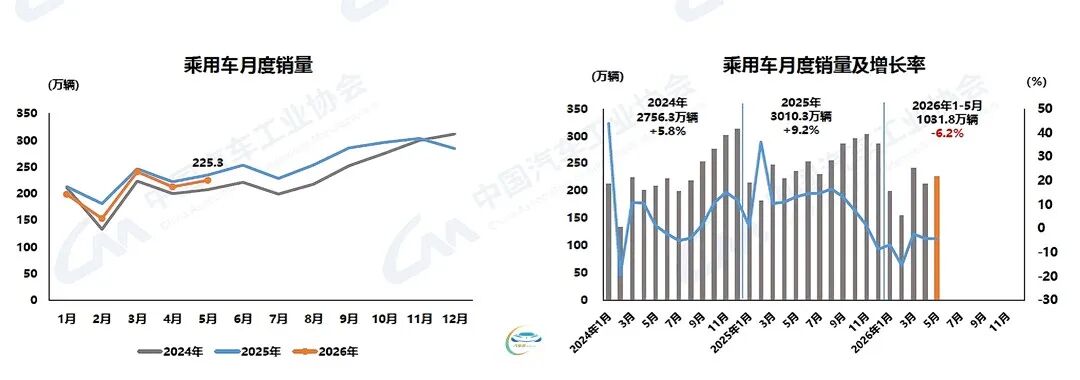

Focusing specifically on the passenger vehicle segment, which is the backbone of the auto market: In May, passenger vehicle production and sales reached 2.241 million and 2.253 million units, respectively, up 2% and 5.8% month-on-month, but down 3.1% and 4.2% year-on-year. From January to May, passenger vehicle production and sales amounted to 10.349 million and 10.318 million units, respectively, down 6.6% and 6.2% year-on-year.

Comparing the overall market data with that of the passenger vehicle segment, it is clear that the passenger vehicle market exhibits relatively greater volatility. Apart from the higher month-on-month increase in May compared to the overall market, the cumulative decline also surpasses that of the overall market—but this data includes overseas export volumes.

If we delve deeper into the domestic sales of passenger vehicles: In May, domestic sales of passenger vehicles reached 1.444 million units, up 8.2% month-on-month but down 23.4% year-on-year. From January to May, domestic sales of passenger vehicles totaled 6.791 million units, down 23.8% year-on-year. Compared to the 19.8% month-on-month decline in domestic passenger vehicle sales in April, the 8.2% month-on-month increase in May represents a nearly 30% swing, and the year-on-year decline has also narrowed slightly compared to the cumulative 24% decline from January to April, fueling hopes that the auto market has started to rebound...

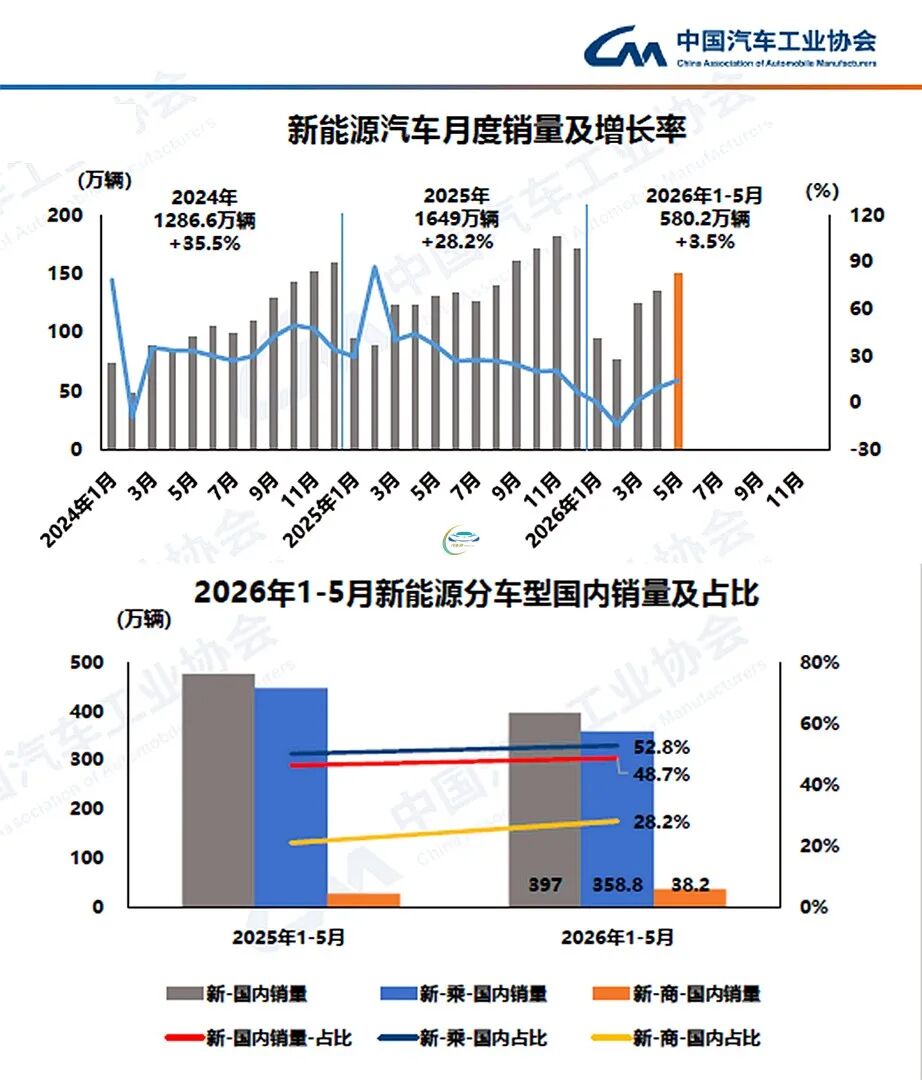

New energy vehicles continue to be a significant growth driver in the overall market data: In May, production and sales of new energy vehicles reached 1.554 million and 1.496 million units, respectively, up 22.4% and 14.4% year-on-year. From January to May, production and sales of new energy vehicles amounted to 5.841 million and 5.802 million units, respectively, up 2.5% and 3.5% year-on-year.

Incidentally, in May, new energy vehicles accounted for 56.9% of total new vehicle sales, and from January to May, they accounted for 47.5%.

Breaking down the domestic sales of new energy passenger vehicles: In May, domestic sales of new energy passenger vehicles reached 947,000 units, up 15.6% month-on-month but down 8.1% year-on-year. From January to May, cumulative domestic sales of new energy passenger vehicles totaled 3.588 million units, down 19.7% year-on-year.

Consistent with market trends, among the three types of new energy passenger vehicles, battery electric vehicles (BEVs) continued to grow, while plug-in hybrid electric vehicles (PHEVs) and fuel cell vehicles experienced varying degrees of decline in both monthly and cumulative year-on-year sales.

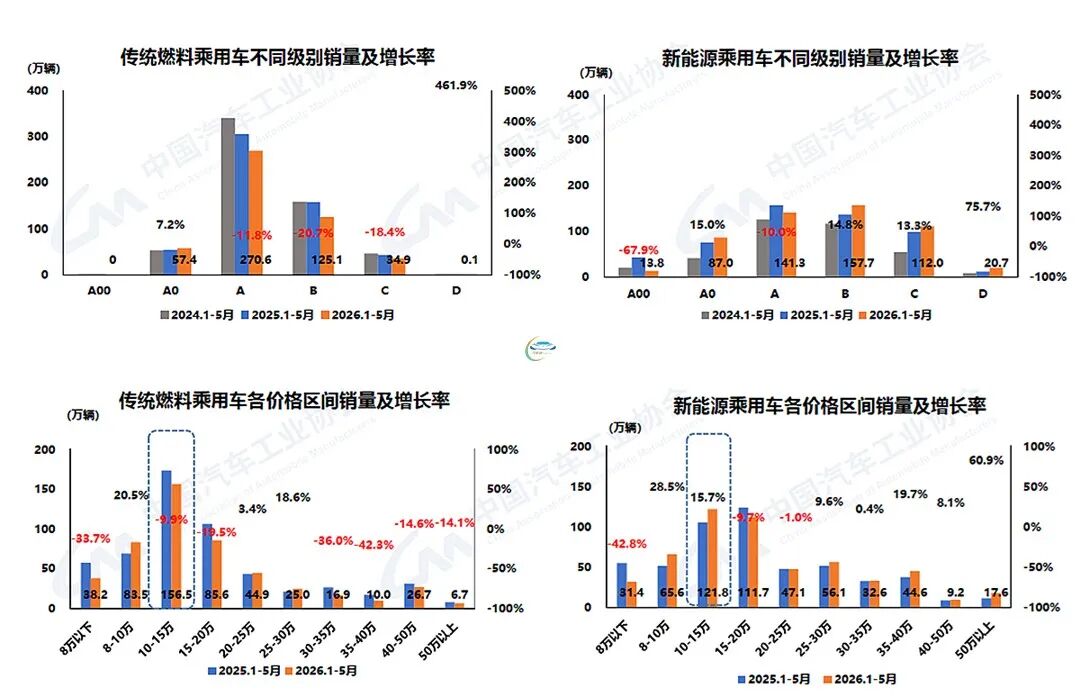

Of course, compared to new energy passenger vehicles, sales of traditional fuel-powered passenger vehicles continued to decline year-on-year, with a significant drop. CAAM data reveals: In May, domestic sales of traditional fuel-powered passenger vehicles reached 497,000 units, a decrease of 357,000 units year-on-year, down 3.5% month-on-month and 41.8% year-on-year. From January to May, domestic sales of traditional fuel-powered passenger vehicles totaled 3.203 million units, a decrease of 1.243 million units year-on-year, down 28%.

On a side note, the significant increase in oil prices this year has also had a noticeable impact on traditional fuel-powered passenger vehicles. From the consumer's perspective, acceptance of new energy passenger vehicles has also risen significantly.

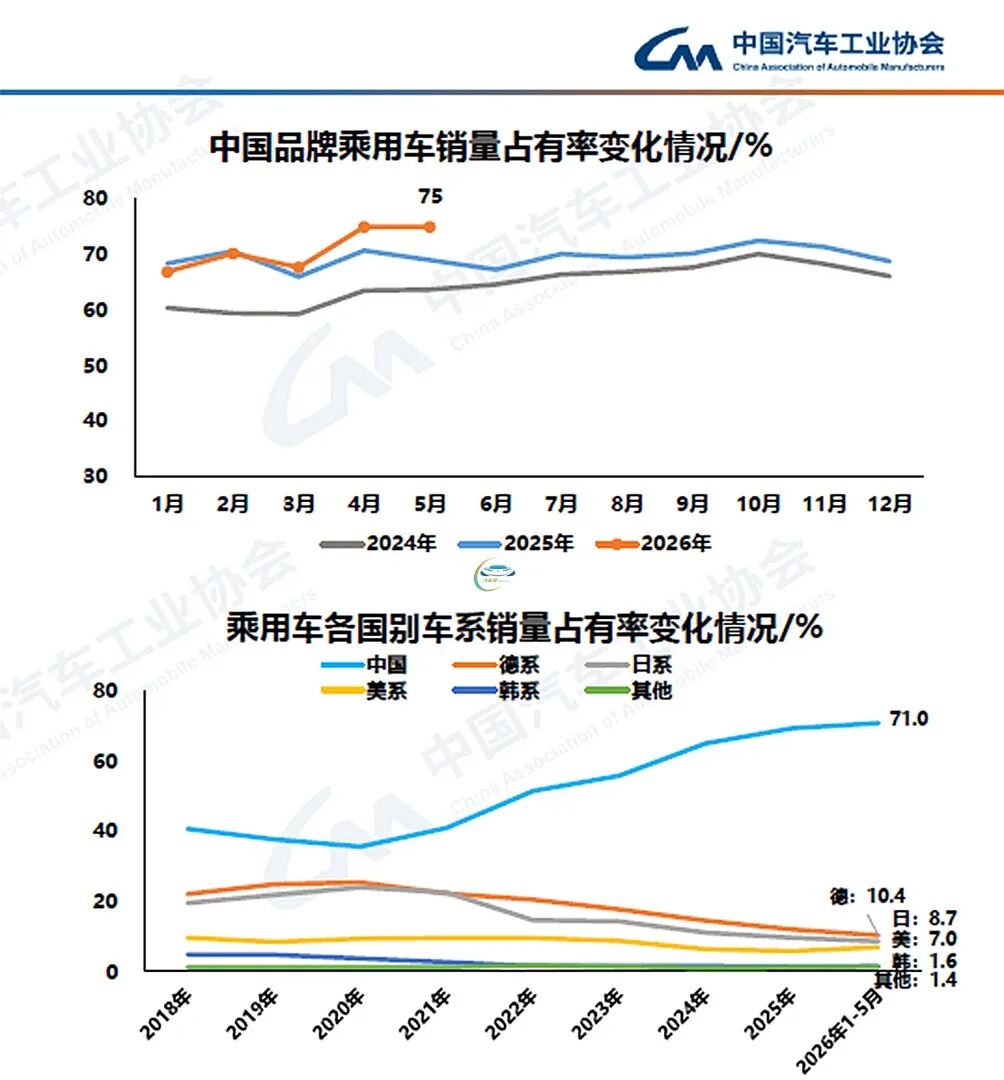

Correspondingly, the market share of Chinese brand passenger vehicles continues to climb. CAAM data shows: In May, sales of Chinese brand passenger vehicles reached 1.689 million units, up 4.2% year-on-year, with the market share increasing by 6 percentage points to 75%. From January to May, cumulative sales of Chinese brand passenger vehicles amounted to 7.326 million units, down 3.1% year-on-year, with the market share increasing by 2.2 percentage points to 71%—indicating a simultaneous increase in consumer acceptance of new energy passenger vehicles and domestic brands.

While everyone is hoping for a rebound in the domestic market, automakers are also stepping up their expansion into overseas markets. CAAM data indicates: In May, automobile exports reached 930,000 units, up 3.1% month-on-month and 68.7% year-on-year, with exports exceeding 900,000 units for the second consecutive month. From January to May, automobile exports totaled 4.059 million units, up 63% year-on-year.

Just as domestic consumers' acceptance of new energy vehicles has increased, overseas consumers' acceptance of Chinese new energy vehicles has also risen simultaneously: In May, exports of new energy vehicles reached 446,000 units, up 3.8% month-on-month and 1.1 times year-on-year. Exports of traditional fuel-powered vehicles reached 483,000 units, up 2.5% month-on-month and 42.6% year-on-year. From January to May, exports of new energy vehicles totaled 1.833 million units, up 1.1 times year-on-year. Exports of traditional fuel-powered vehicles reached 2.227 million units, up 36.2% year-on-year.

Breaking down the data into passenger vehicles and commercial vehicles: In May, exports of new energy passenger vehicles reached 435,000 units, up 3.4% month-on-month and 1.1 times year-on-year. Exports of new energy commercial vehicles reached 12,000 units, up 21% month-on-month and 48.1% year-on-year. From January to May, cumulative exports of new energy passenger vehicles totaled 1.792 million units, up 1.2 times year-on-year. Exports of new energy commercial vehicles reached 41,000 units, up 0.6% year-on-year.

The ranking of automakers in overseas exports has not changed significantly. However, from another perspective, for the healthy development of the automobile industry, both "domestic demand" and "foreign trade" need to be promoted simultaneously. Based on the current market situation, CAAM suggests: "On the consumption side, policies and market expectations should be stabilized, industry governance should be deepened, and restrictive measures should be introduced cautiously to maintain the stability of the consumption base. On the foreign trade side, international development should be deepened, various risks and challenges should be effectively addressed, and the stable supporting role of the international cycle should be strengthened."

-

![]()

Chinese Cars Seize Overseas Markets: The Advent of a Winner-Takes-All Era

-

![]()

Will WeChat Start Charging Fees?

-

![]()

Cross-border 'Golden Window' in 2026: Chinese Products Sweep Across Southeast Asia

-

![]()

BIWIN Storage, Betting 20 Billion on the Future with Hundreds of Billions in Market Cap

-

![]()

Jensen Huang: The Globetrotting Icon

-

![]()

Auto Retailer Rankings: January-May 2026 - Geely Leads, BYD Follows

-

![]()

199 RMB! Nokia Small-Screen Phone Review: WeChat Video Calls Add a Quirky Twist

-

![]()

2.27 Billion Shares Unlocked: Will Insta360 Face a Mass Sell-Off?