Deciphering the European Market: Regional Dynamics, Investment Trends, and New Regulatory Compliance

06/11 2026

06/11 2026

480

480

Diverse Characteristics and Development Trajectories Across Europe's Four Key Regions

European regions exhibit significant disparities in resource endowments, religious beliefs, and development models. The EU core region, encompassing Germany and France, is marked by deep integration, a robust resource base, and a converging religious landscape. Western Europe, including the UK and Ireland, relies heavily on North Sea resources and displays varied religious structures. Central and Eastern Europe, featuring countries like Poland and the Czech Republic, showcases diverse resource endowments and complex ethnic-religious relations. Northern Europe, represented by Norway and Sweden, drives development through energy and mining, with a highly unified religious faith. This regional diversity serves as the foundational premise for understanding the European market landscape.

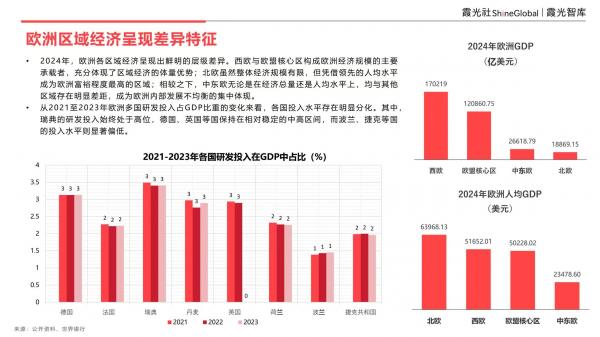

Pronounced Regional Economic Stratification: Northern Europe Leads in Wealth, Central and Eastern Europe Lags

Building on these regional characteristic differences, Europe's economic performance also displays distinct stratification. In 2024, Western Europe and the EU core region dominate Europe's economic scale, reflecting their regional economic advantages. Although Northern Europe has a relatively smaller overall economic size, its leading per capita income levels make it the wealthiest region in Europe. Central and Eastern Europe, however, exhibits significant gaps in both total economic output and per capita income compared to other regions, highlighting internal development imbalances within Europe. From 2021 to 2023, the proportion of R&D investment in GDP (unit: %) consistently remained high in Sweden, stable at mid-to-high levels in Germany and the UK, and notably lower in Poland and the Czech Republic, further confirming regional disparities in innovation capacity.

Chinese Investment in Europe Grows, with Distinct Flow and Stock Differentiation in Industry Layout

Against this backdrop of economic differentiation, Chinese investment in Europe demonstrates structural characteristics. In 2024, Chinese investment flows into Europe reached $12.49 billion, up 25.3% year-on-year, with a distribution covering Russia, the UK, Germany, and other countries. In terms of industry structure, investment flows into the EU are primarily concentrated in finance (71.9%) and manufacturing (48.2%), while stock investments focus on manufacturing (34.1%) and finance (19.3%), with Luxembourg and Germany serving as key hubs. This indicates a focused regional and industry distribution for Chinese investment in Europe.

Accelerating Aging: A Core Challenge for Europe's Macro Development

Beyond economic and investment patterns, demographic shifts are profoundly reshaping Europe's long-term development foundations. The median age across European countries is projected to continue rising from 2024 to 2050, with most countries reaching or exceeding 50 years by 2050. Some countries, such as Greece, will experience particularly sharp increases, jumping from 21.1 years in 2024 to 54.1 years in 2050. This means that for decades to come, population age structures will continue to tilt toward older age groups, intensifying pressure on pension and social healthcare resources and imposing long-term constraints on labor supply and economic vitality.

Energy Transition and Green New Deal: Driving Dual Progress and Accelerating Low-Carbon System Construction

Facing growth pressures from an aging population, Europe is reshaping its economic drivers through energy transition. The share of renewables in electricity consumption has risen steadily from 36% in 2021; clean hydrogen production has grown from less than 1 unit in 2021 to 19.2 by 2050, with carbon capture expanding rapidly in tandem. Europe is steadily advancing its shift from traditional to renewable energy sources, with the Green New Deal focusing on the engineering implementation of low-carbon technologies and the continuous intensification of carbon reduction efforts, forming a core practice of technological empowerment and upgraded carbon constraints.

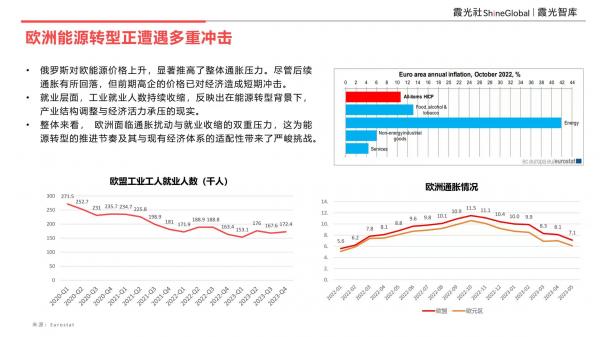

Energy Transition Faces Dual Shocks: Inflation and Employment Challenges

However, the energy transition process has not been smooth sailing. Rising energy prices from Russia to Europe have significantly driven up overall inflationary pressures. Although inflation subsequently declined, the initial price surge caused short-term economic shocks. Meanwhile, industrial employment has continued to contract, reflecting the realities of industrial restructuring and economic vitality under pressure. Europe faces dual pressures from inflationary disruptions and employment contractions, posing severe challenges to the pace of energy transition and its adaptability to the existing economic system.

GDPR Enforcement Varies: Complex Regulatory Landscapes Across Member States

Beyond transition pressures, data compliance represents another barrier to entering the European market. The EU's General Data Protection Regulation (GDPR) focuses on protecting personal data rights, but enforcement varies markedly across member states: Ireland imposes heavy fines and leads cross-border cases (approximately €652 million in fines, unit: euros), France emphasizes direct fines and institutional collaboration (approximately €55.2 million), Germany employs a federal-state dual-track enforcement approach (approximately €13.8 million), Denmark lacks direct fine authority and prioritizes compliance (approximately €2.98 million), and Luxembourg has no fine authority for certain institutions and focuses on procedural norms (approximately €23 million). Businesses must develop differentiated compliance strategies tailored to the enforcement characteristics of each country.

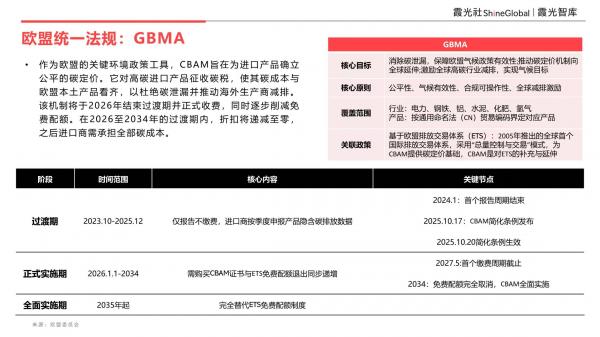

CBAM to Impose Fees Officially in 2026: Fully Internalizing Carbon Costs

Parallel to data compliance, the Carbon Border Adjustment Mechanism (CBAM) is restructuring trade costs. CBAM aims to impose carbon taxes on high-carbon imported products, aligning their carbon costs with those of EU domestic products. The mechanism will conclude its transition period and begin imposing fees in 2026, with discounts declining annually to zero from 2026 to 2034, after which importers will bear full carbon costs. Covered industries include electricity, steel, aluminum, cement, fertilizers, and hydrogen, requiring businesses to conduct carbon emission accounting and cost assessments in advance.

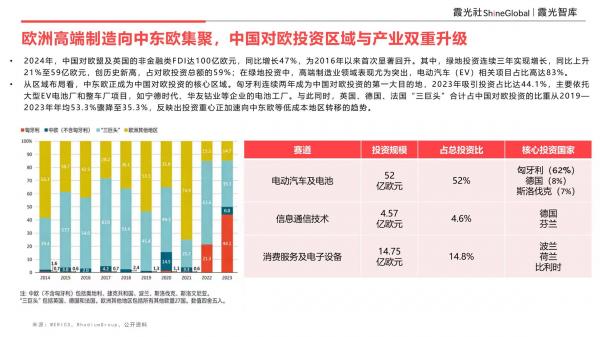

Chinese Investment in Europe Shifts Eastward: High-End Manufacturing Clustering

Under the dual constraints of compliance and carbon costs, the regional distribution of Chinese investment in Europe is undergoing structural shifts. In 2024, Chinese non-financial FDI into the EU and UK reached €10 billion, up 47% year-on-year, marking the first significant rebound since 2016. Greenfield investments rose 21% year-on-year to €5.9 billion, a record high, accounting for 59% of Chinese investment in Europe; electric vehicle-related projects in high-end manufacturing accounted for 83%. Hungary became China's top investment destination in Europe for the second consecutive year (44.1% in 2023), while the combined share of the UK, Germany, and France (the "Big Three") plunged from 53.3% to 35.3%, with the investment focus accelerating toward lower-cost regions like Central and Eastern Europe.

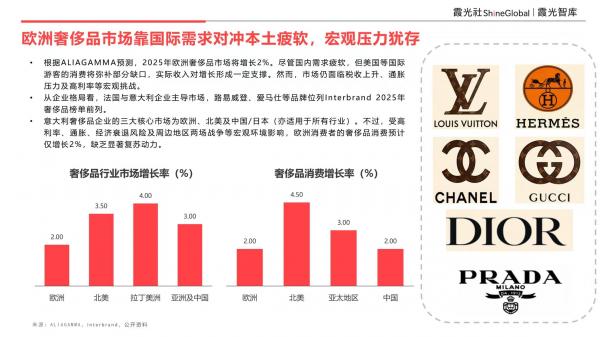

Luxury Market Offsets Domestic Weakness with International Demand, but Macro Pressures Persist

Unlike the booming manufacturing investment sector, Europe's consumer market remains sluggish. The European luxury market is expected to grow by 2% in 2025 (unit: %), with weak domestic demand offset by consumption from international tourists, particularly from the US. French and Italian firms dominate the market, with Louis Vuitton, Hermès, and others ranking high on Interbrand's 2025 luxury list. Italian firms' three core markets are Europe, North America, and China/Japan, but high interest rates, inflation, recession risks, and surrounding conflicts have limited European luxury consumption growth to just 2%, lacking significant recovery momentum.

Green Tech Industries Flourish: Varying Development Stages Across Countries

In the green transition sector, European countries exhibit significant differences in development stages. The EU Green Deal targets a 42.5% renewable energy share by 2030 (unit: %) and mobilizes at least €1 trillion in sustainable investment. Sweden, at 62.8%, far exceeds the target, serving as a technological pioneer; Germany and France, at around 22%, are the main battlegrounds for transition; Poland, at just 17.8%, shows strong growth potential as an emerging production hub. Investment projects cover five key areas: clean energy, circular economy, industrial energy efficiency, sustainable transportation, and building energy efficiency.

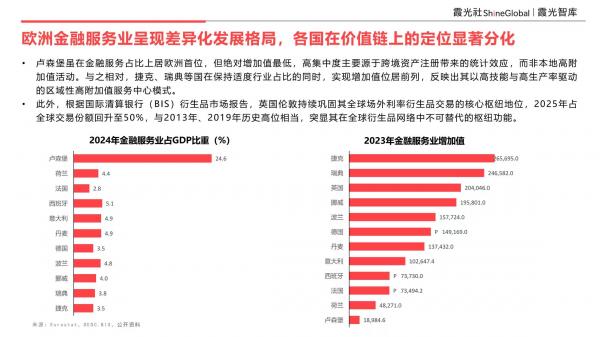

Financial Services Sector Positioning Varies Sharply: London's Hub Status Intact

In the services sector, European countries exhibit sharp differences in the value-added positioning of their financial industries. Luxembourg ranks first in Europe for financial services' share of the economy but has the lowest absolute value-added, with high concentration stemming from statistical effects of cross-border asset registration rather than local high-value-added activities. The Czech Republic, Sweden, and others maintain moderate shares while ranking high in value-added, reflecting a regional high-value-added service center model driven by high skills and productivity. Additionally, London continues to solidify its position as a global hub for over-the-counter interest rate derivatives trading, with its global market share rebounding to 50% in 2025 (unit: %), matching historical highs in 2013 and 2019.

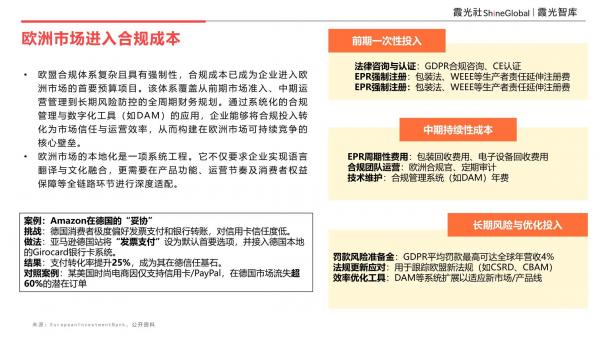

Compliance Costs: A Primary Budget Item for Entering the European Market

Whether in manufacturing, consumer markets, or finance, compliance has become a foundational requirement for entering Europe. The EU's compliance system is complex and mandatory, covering full-cycle financial planning from pre-entry access to mid-term operations and long-term risk prevention. In the German market, for example, Amazon boosted payment conversion rates by 25% (unit: %) by setting "invoice payment" as the default option and integrating with the local Girocard system, while a US fashion e-commerce platform supporting only credit cards/PayPal lost over 60% of potential orders. Through systematic compliance management and digital tools (e.g., DAM), businesses can transform compliance investments into market trust and operational efficiency.

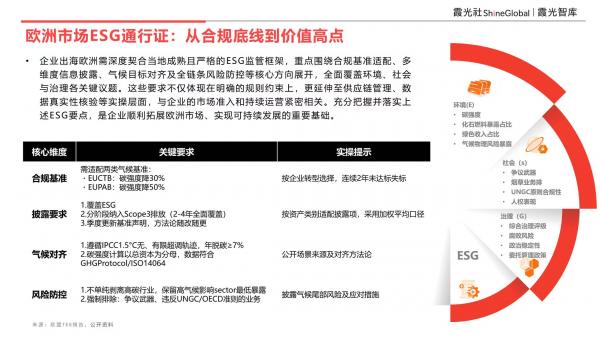

ESG Becomes a "Passport" for the European Market: Evolving from Compliance Baselines to Value High Ground

Building on compliance, ESG has become a core competitive factor for businesses entering Europe. Firms must focus on compliance baseline alignment, multi-dimensional information disclosure, climate goal synchronization, and full-chain risk prevention. Compliance baselines require a 30% or 50% reduction in carbon intensity (unit: %, per EUCBT or EUPAB standards); disclosure must cover ESG, phase in Scope 3 emissions (full coverage in 2-4 years), and update baseline statements quarterly; climate alignment must follow the IPCC 1.5°C trajectory, with annual decarbonization of no less than 7% (unit: %); risk prevention involves not just divesting from high-carbon industries but mandatorily excluding controversial weapons and businesses violating UNGC/OECD guidelines. Fully implementing ESG priorities is essential for successfully expanding into the European market.

Overall, the European market is undergoing multiple transformations, including regional landscape reshaping, accelerated energy transition, and upgraded compliance systems. Chinese firms entering Europe face structural opportunities from shifting investment focuses and green industry development but must also navigate systemic challenges such as aging populations, inflation, employment pressures, and high compliance costs. Xiaoguang Think Tank aims to empower Chinese firms' globalization by continuously producing industry research, market insights, and business strategies, providing one-stop services and business implementation solutions for overseas firms.

-

![]()

Chinese Cars Seize Overseas Markets: The Advent of a Winner-Takes-All Era

-

![]()

Will WeChat Start Charging Fees?

-

![]()

Cross-border 'Golden Window' in 2026: Chinese Products Sweep Across Southeast Asia

-

![]()

BIWIN Storage, Betting 20 Billion on the Future with Hundreds of Billions in Market Cap

-

![]()

Jensen Huang: The Globetrotting Icon

-

![]()

Auto Retailer Rankings: January-May 2026 - Geely Leads, BYD Follows

-

![]()

199 RMB! Nokia Small-Screen Phone Review: WeChat Video Calls Add a Quirky Twist

-

![]()

2.27 Billion Shares Unlocked: Will Insta360 Face a Mass Sell-Off?