Has the Microcar, Once a Market Pioneer, Now Reached Its Twilight?

06/15 2026

06/15 2026

525

525

From reigning as the new energy sales champion to fading into relative obscurity, microcars have certainly played their part in fulfilling the mission of their era.

In early June, amidst automakers flaunting their sales achievements, SAIC-GM-Wuling unveiled a poster that, while exuding pride, also unveiled the cutthroat nature of the new energy market.

The poster proudly declared that the Wuling Hongguang MINIEV had maintained its crown as the world's best-selling micro new energy vehicle, boasting cumulative sales exceeding 1.9 million units over 70 months.

However, within the domestic market, the Wuling Hongguang MINIEV has seen its influence wane in the new energy sector, with the spotlight now firmly fixed on mid-to-large-sized vehicles such as the Tesla Model Y, Xiaomi SU7, and Li Auto i6. Affordable microcars like the MINIEV are no longer the mainstays on the sales charts.

Statistics reveal that the Wuling Hongguang MINIEV sold a mere 36,000 units in the first quarter of this year, marking a staggering 74% year-on-year decline. Third-party data further indicates that sales in May plummeted to 18,308 units, a far cry from the previous monthly peak of 50,000 units.

The downturn in sales of the Wuling Hongguang MINIEV is not merely attributable to product evolution but rather mirrors a profound transformation in the domestic new energy market structure, with shifting market demands pushing a once-iconic vehicle to the periphery.

From Breakthrough to Maturity

Despite the years of development in new energy vehicles, it was the Wuling Hongguang MINIEV, a model beloved by the masses, that truly cracked open the market. Starting in 2021, A00-class models, epitomized by the Wuling Hongguang MINIEV, witnessed exponential growth, with their market share in the new energy vehicle sector once soaring to 20%.

It can be argued that low-priced microcars served as the gateway for many into the world of electric vehicles, playing a pivotal educational role in the market.

However, as new energy vehicles entered a phase of rapid expansion, the A00-class models that had initially blazed the trail began to lag. By 2025, statistics showed that the market share of microcars had dwindled to less than 10%. While new energy vehicle sales surged, A00-class model sales rapidly contracted.

Specifically, in 2025, the Wuling Hongguang MINIEV sold 430,000 units, retaining its title as the best-selling model in the A00 market. Meanwhile, Wuling, Changan, BYD, and Geely collectively captured 93.9% of the microcar market share.

Of course, apart from Wuling, the microcar sales of the other three automakers are also on the decline. Whether it's Changan's Lumin or Chery's QQ Ice Cream, their situations mirror that of Wuling.

Entering 2026, the sluggish state of the microcar market shows no signs of improvement. Data from the China Passenger Car Association reveals that from January to May 2026, wholesale sales of A00-class pure electric vehicles plummeted by 40%-55% year-on-year, with market share reverting to levels seen during the era of fuel-powered vehicles.

At the outset of their market entry, microcars wrested market share from fuel-powered vehicles. With precise market positioning, compact and agile body sizes, and affordable price tags, they swiftly achieved new energy replacement in the microcar market, reaching a 99% new energy penetration rate early on.

However, this rapid ascent came at a price, as the market matured too swiftly and reached saturation in a shorter timeframe.

From a global perspective, the microcar market remains niche, except in a few regions with policy protections. In 2025, 1.03 million microcars were sold domestically, representing a last-ditch effort spurred by policies.

Since entering a boom phase in 2020, the market, which was never vast to begin with, has been inching towards saturation after five years. The precipitous decline in the first quarter of this year underscores the issue.

Of course, the contraction of the microcar market is not solely due to market saturation but is also influenced by a multitude of factors.

Firstly, policy impacts loom large. In 2026, the purchase tax for new energy vehicles was halved, while subsidies shifted from fixed amounts to proportions based on vehicle prices, eroding the core price competitiveness of microcars.

Gone are the days when a car could be purchased for a mere 10,000 to 20,000 yuan with national subsidies.

Affected by price factors, A0-class models have begun to comprehensively supplant A00-class products. Even in Guangxi, a stronghold for microcars, this replacement has been completed, with A0-class market share now on par with that of A00-class.

In more economically developed regions like Zhejiang, A0-class model sales surpass those of A00-class by more than sixfold. At similar price points, space and configuration have become paramount to consumers.

Sales data clearly reflect this trend. In 2025, the Geely Starry Wish sold 460,000 units, and the BYD Seagull sold 310,000 units, signaling a market shift from A00-class to A0-class.

Of course, a more pivotal factor in the decline of the microcar market is the inherent limitations of new energy vehicles. Unlike fuel-powered vehicles, new energy vehicles necessitate larger batteries for extended range, naturally increasing vehicle size.

It can be said that microcars have fulfilled their crucial mission of boosting new energy vehicle penetration. Given the trend of market saturation, they can no longer shoulder the burden of incremental growth, and a return to maturity has become inevitable.

Turbulence in the New Energy Market

Of course, the contraction of the microcar market is not solely due to various objective factors but is also inextricably linked to changes in the overall new energy market. Entering 2026, the domestic new energy vehicle market is undergoing its most profound transformation yet.

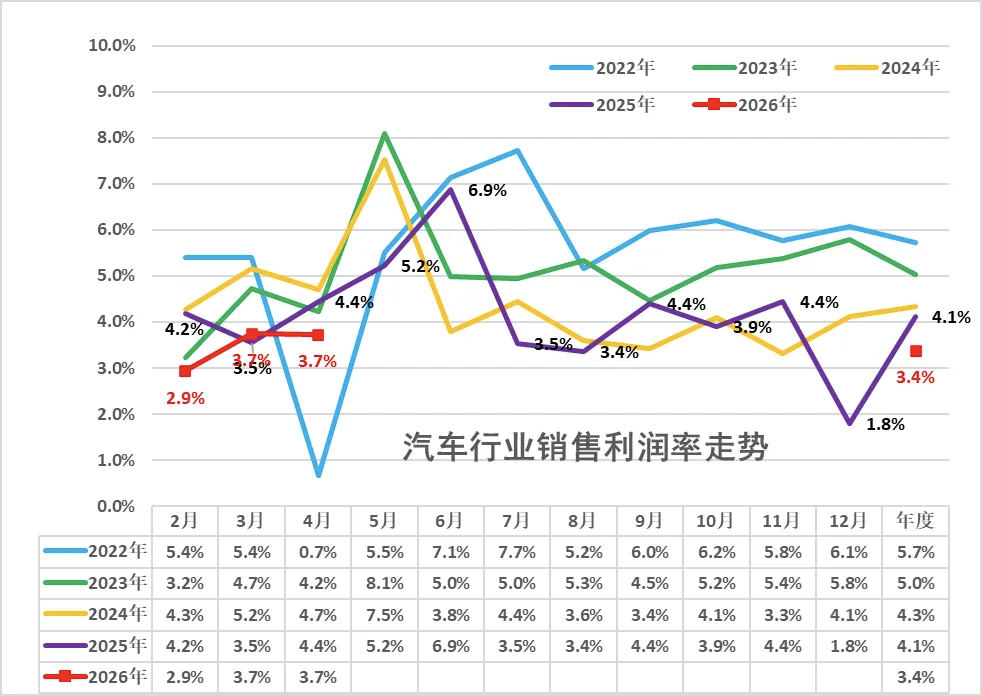

Firstly, operational pressures mount. In the first quarter, the profit margin of the automotive manufacturing industry stood at a mere 3.2%, with retail sales declining by nearly 20%. Automakers are now laser-focused on survival strategies.

The profit margins of microcars are already razor-thin. Statistics reveal that the gross profit margin of the Wuling Hongguang MINIEV hovers around 2%-3%, which is unsustainable for automakers.

Simultaneously, costs across various facets of new energy vehicles are on the rise. After years of decline, the price of lithium carbonate has rebounded. According to market quotes, the futures price of lithium carbonate surged to 175,000 yuan per ton in June. In terms of chips, driven by the AI wave, automotive-grade chip prices have skyrocketed by more than 100%.

The rise in raw material costs has been directly passed on to the market. This year alone, 20 brands have adjusted their prices, particularly for high-end intelligent driving versions, with price hikes exceeding 20%, marking the end of years of price wars.

The confluence of multiple factors has led automakers to pivot towards high-value products. Whether it's the MPV market or the competition between Series 8 and Series 9 models, behind these trends lies automakers' choice to enhance operations with high-value models.

In 2025, sales of new energy vehicles priced above 300,000 yuan surged by 47.2% year-on-year, far outpacing the market average growth rate of 18.3%. In May this year, wholesale sales of B-class pure electric models increased by 42% year-on-year, indicating a market shift towards high-value models.

After the electrification of vehicles, the demand for intelligence has become the linchpin of consumers' purchasing decisions. With escalating demands for space, range, configuration, and comfort, budgets have also ballooned. In 2025, the average transaction price of passenger vehicles dipped to 168,000 yuan but has since rebounded to 173,000 yuan in May this year, indicating that consumers' purchasing budgets have also increased under the influence of high-end new energy models.

With limited prospects in the domestic market, going overseas seems to be the only recourse for microcars.

The Wuling Hongguang MINIEV's eventual foray overseas was to the Indonesian market, with an annual production capacity exceeding 150,000 units at Wuling's Indonesian factory through CKD assembly.

Simultaneously, the Latin American market is gradually emerging as a new blue ocean. According to statistics, sales of Chinese electric vehicles in the Latin American market soared by more than 300% year-on-year in 2025. Experts predict that microcar exports will reach 183,000 units in 2026, marking a year-on-year increase of over 40%.

For the foreseeable future, the microcar market will exhibit a dual-track pattern of 'domestic marginalization and overseas growth-seeking.' In the domestic market, microcars will maintain a foothold through product stratification, channel expansion to lower-tier markets, and policy dependence. Internationally, they will seek new growth avenues through exports and local production.

The adjustment of the microcar market will propel the domestic new energy vehicle industry towards a more mature and sustainable development phase, shedding its ingrained image of being low-end and cheap and moving towards a more valuable market.

The decline of the microcar market represents a necessary transition for China's new energy vehicle industry towards maturity. When electrification no longer relies solely on cheap microcars to maintain scale, the entire industry can truly revert to the core trajectory of technological upgrading, value creation, and long-term profitability.

The new energy market should also transition away from an era of achieving sales through simplistic methods and towards a more complex but higher-value era. For automakers and the market, the time has come for new energy microcars to take a bow.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

AI Asset Spin-offs at Tech Giants: Is Kling Paving the Way for ByteDance and Alibaba?

-

![]()

Why Zhang Xue? Why HONOR?

-

![]()

Exclusive! Tencent’s ‘Tencent Drive’ with AI-Powered Asset Backup in the Works—A Game-Changing Move

-

![]()

Internal Upheaval in Initial Listing Days: SpaceX's AI Division Faces Accelerated Talent Loss, with 50+ R&D Staff Exiting in 2026

-

![]()

Price War Fails, Chinese Automakers Have No Retreat

-

![]()

Still in the Red but Outpacing Tesla: What Lies Behind SpaceX's $2.1 Trillion Valuation?

-

![]()

Humanoid Robots Go Global: From 'Actors' to 'Workers'

-

![]()

Still Incurring Losses Yet Outpacing Tesla: What Does SpaceX's $2.1 Trillion Valuation Signify?