Can't Create High-End Cars with Stacked Configurations Anymore

06/23 2026

06/23 2026

478

478

The More Flagships, the Fewer High-End Models.

Original content from Autopix (ID: autopix)

Just 20 days after the launch of the all-new Li L9 Livis, a video suddenly appeared on Li Auto's official WeChat Mini Program.

The footage showed a wavy paved road, with the all-new Li L9 Livis and the NIO ES9 driving over it in sequence. The suspension comfort modes of both vehicles were adjusted to "hardest" and "softest," respectively, with clear results: the L9 Livis maintained a stable body posture, while the ES9 showed noticeable swaying.

Several hours after the video went live, Li Auto quickly removed it from all platforms.

This was no ordinary competitor comparison. After the large six-seater flagship segment entered the red ocean, the pioneer was forced to re-prove itself for the first time.

Controversy quickly spread through the automotive review community. A few days earlier, Dongchedi had conducted a live broadcast comparing the full active suspensions of the Li L9 Livis and NIO ES9, reaching no one-sided conclusion. NIO Vice President Ma Lin also questioned on social media, demanding that Li Auto clarify the video's source, testing environment, and suspension settings.

Faced with these questions, Tang Jing, president of Li Auto's first product line, did not explain the testing details but instead posted a photo from the ES9 launch event, questioning why Li Bin would claim on NIO's launch event that the 48V solution is more advanced than 800V.

This argument left onlookers bewildered. Li Auto uses 800V high voltage for substantial support, while NIO uses 48V low voltage for high-frequency fine-tuning—two different engineering philosophies with no absolute superiority, only which tuning better suits which users. But once technical debate mixes with marketing, it becomes an unsolvable Rashomon.

Li Auto is one of the pioneers in the new energy large six-seater SUV category. Three years ago, it sold over 10,000 units monthly without answering to anyone; now, it must arrange its own tests to re-prove itself. This detail reveals more about the segment's current temperature than any sales figures.

More importantly, they're not arguing about "whose configuration is higher"—both vehicles have impressively long specs sheets—but rather about who is more advanced and who gets to define that.

This battle for interpretive authority was forced by a wave of "flagships."

01 When Flagships Fill the Shelves

As 2026 begins, SUVs over five meters long, with six seats, and labeled as flagships, flood the market as if by agreement.

In late May, Yu Chengdong stated at the new M9 launch event that after the previous M9, the industry had released over 40 "9-series" SUVs.

Above 500,000 yuan, the NIO ES9, refreshed Seres M9, Zeekr 9X, and Li L9 Livis compete fiercely; in the 300,000 yuan range, SAIC Volkswagen ID.ERA 9X, IM LS9, Voyah Taishan X8, Lynk & Co 900, and Deepal S09 crowd together.

Further down, the Leapmotor D19, Geely Galaxy M9, Wuling-Huawei collaboration Hua Jing S, and Fangchengbao Titan 7 bring the same size and configurations down to 200,000 or even 150,000 yuan.

By 2026, the market will have over 30 such flagship large vehicles simultaneously for sale, covering 150,000 to 600,000 yuan. This niche market, which sold just over 200,000 units annually three or four years ago and had lower priority than MPVs, sold 755,000 units last year and is heading toward a million this year, leading all passenger vehicle segments in growth.

This isn't because automakers suddenly became obsessed with the number 9. The real reason lies in supply-side changes.

When the M9 proved in late 2023 that "a 500,000 yuan domestic SUV could succeed," the technologies supporting its flagship status were capabilities only a few automakers could fully deliver: 800V, LiDAR, air suspension, large battery range extenders, advanced driver-assistance systems, and million-dollar or top-trim optional configurations.

Changes occurred from 2024 to 2025, when this configuration stack matured and reduced costs simultaneously. LiDAR prices dropped from tens of thousands to thousands of yuan, computing chip prices collapsed, and supply chains for air suspension and large battery range extenders expanded. Thus, M9-style vehicles became affordable and replicable for the first time.

The category was defined three years ago; now, supply chains make it replicable. Meanwhile, demand-side gates opened almost simultaneously.

New energy growth now relies mainly on fuel-powered vehicle (internal combustion engine vehicle) owners trading up, whose budgets naturally exceed their old cars. This wave of trading ICE for EV represents structural consumption upgrades, with money flowing to the pyramid's apex—large premium SUVs.

In Q1 this year, C-segment SUV retail sales grew 143.5% YoY, the fastest rate. Meanwhile, the 200,000 yuan mainstream market has been drained of profits by price wars, pushing any player still holding premium capabilities upward.

Moving up isn't a choice—it's an escape.

When these forces collide, more premium vehicles emerge this year, and the definition of "premium" gets fragmented and sold separately: advanced driver-assistance as one package, six-seat space as another, large battery range extender as another, flagship stance as another—all packaged into different price tiers from 150,000 to 600,000 yuan. The Wuling-Huawei collaboration Hua Jing S even brings "Huawei Qiankun Tech Flagship Large Six-Seater" down to the 150,000 yuan level.

Flagships have transformed from brand totems into volume-selling shelves. But crowded on these shelves, what each company wants varies.

The Li L9 and Seres M9 need to defend existing profits and definition rights. Volkswagen's ID.ERA 9X aims to set a benchmark, finding an anchor for the "Joint Venture 2.0" transformation, even if it means pricing rights and interests (benefits) at 300,000 yuan on launch day. Leapmotor's D19 chases volume, slashing flagship specs pricing to start at 219,800 yuan. Deepal's S09 and vehicles from state-owned enterprises aim to put out fires, meeting group volume and globalization targets.

Many other vehicles lack clear profit goals or brand stories but rush in anyway, seeing the segment too hot to miss—absence equals weakness.

These varied intentions will soon show in sales, as the track everyone floods into teaches its first lesson: entering and winning are two different things.

02 Configuration Specs Have Lost Their Power

May's large SUV sales rankings already split these vehicles in half.

At the top sits the NIO ES8 with 11,472 units, first place for the fifth consecutive month. What's emphasized isn't its high sales but its rare sustained stability amid shortening product lifecycles.

Next is the Zeekr 9X with 9,058 units, champion of the 500,000 yuan segment for over six months, averaging over 500,000 yuan and even facing order backlogs and delivery queues.

Third place stings more: Leapmotor D19 with 7,021 units, a vehicle priced just above 200,000 yuan, outperforming flagships priced 300,000 yuan and up.

On the other side, several vehicles labeled as flagships have nearly vanished from the rankings.

Deepal's S09, launched at 239,900 yuan last year, should have had room to maneuver but saw monthly sales drop to the hundreds. Lynk & Co 900, which sold 7,319 units last September, fell to just over 1,000 units from February to April this year, with terminal prices noticeably loosening.

SAIC's flagship IM LS9, built with group-wide resources, sells just over 1,000 units monthly, while its true hit is the 200,000 yuan-level LS6.

The SAIC Volkswagen ID.ERA 9X, a highly anticipated joint venture transformation anchor, didn't hold back on pricing—launching with rights and interests (benefits) priced around 300,000 yuan and potentially introducing lower trims later. It's not without brand backing, but in new energy's arena, Volkswagen's old trust must first undergo price translation.

Judging by specs alone, these vehicles are nearly indistinguishable. LiDAR, air suspension, large batteries, rear-wheel steering, advanced driver-assistance—none dare skimp.

But the market doesn't see them as the same.

In recent years, new energy automakers repeatedly claimed that new technology equals new luxury and that product quality can rewrite brands. But in the 9-series battle, the more similar the configurations, the starker the brand gaps become.

This held true when technology iterated rapidly and generational gaps were visible. Now, everyone buys the same stack from the same suppliers, narrowing the core config gap between 150,000 yuan and 500,000 yuan vehicles despite large price differences.

When configurations become standard, specs sheets no longer justify premium status. They shift from ceiling to floor.

Assembling the best parts from others and tuning them well remains a true skill, capable of producing flawless vehicles. The divergence happens afterward.

The top sellers win on factors beyond specs. Nine in ten NIO ES8 buyers choose BaaS, lowering the starting price to 298,800 yuan. Supporting this is NIO's seven-year, multi-billion-yuan nationwide battery swap network—something suppliers can't provide.

Zeekr 9X's average price just above 500,000 yuan reflects performance labels built through the 001 and 009 models and Geely's vehicle engineering expertise.

Leapmotor D19 brings large six-seater range extenders below 250,000 yuan through relentless focus on in-house R&D to cut costs. These aren't new technologies but years of accumulation that can't be bought off the shelf.

The underperformers lack nothing in specs but something else.

03 The Market Decides Brand Positioning

The June 5 wavy road video debate ultimately left no conclusion on whose technology was stronger. Both vehicles' parameters were too evenly matched to declare a winner. The real fight wasn't about chassis quality but who gets to define "better."

Rewind three or four years, and this scene would be nearly reversed. Back then, when NEV startups overturned BBA, they claimed "technology is the new luxury; good products transcend brands," as if branding no longer mattered.

In new energy's heyday, a brand's price tier was mostly self-determined.

Avatr declared itself "new luxury" at launch, pricing above 300,000 yuan; IM was SAIC's high-end hope; Deepal occupied the middle tier under Avatr and above Qiyuan.

Pricing resembled an open-ended question—you chose a tier, hung the corresponding badge, set a price, and the market gave you time to flesh out the story. Back then, positioning was a starting point.

The 9-series battle is changing this logic.

Now, the sales winners are those with years of accumulated brand and system strength. The same group that overturned BBA is now being re-stratified by the same forces, with harder results than before.

Flagships once crowned product lines, gilding (gilding) entire brands. But with over 40 crowns in one niche, they've become litmus tests instead.

Tossing a brand's most expensive, fully-loaded model into the 500,000 yuan arena reveals whether it has an uncopyable system beneath the specs or just good parts from shared suppliers.

This battle won't just leave sales rankings—it will redraw a price-tier map that's hard to alter.

China's dozens of NEV brands, once scattered across self-chosen tiers, will gradually be ranked. Some will be validated as premium, others pushed back to 200,000 yuan volume segments, and some stuck in the middle awaiting integration or downward shifts.

Pricing has shifted from a manufacturer-filled starting point to a market-stamped result.

Forty-plus brands, each sending their most expensive, representative model to the same litmus test, will find that after this round, their position won't be self-declared anymore. With flagships filling shelves, what's truly scarce is a brand subject recognized by the market.

This is original content from Autopix (autopix). Unauthorized reproduction is prohibited.

-

![]()

When AI Dominates 618, Is Human Live Streaming the Ultimate Challenge?

-

![]()

Behind SpaceX's IPO: Musk, Boasting a Trillion-Dollar Net Worth, Still Grapples with a Severe 'Cash Crunch'

-

![]()

【OFweek Weike Cup】CASTECH Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Accelink Technologies Competes for 2026 Outstanding Optical Component Supplier in Optical Industry

-

![]()

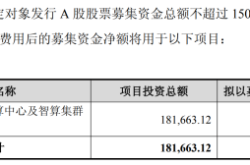

A Leading Computing Power Provider Secures 1.5 Billion Yuan in Private Placement, Expands Smart Computing Center to 12,000 Racks

-

![]()

【OFweek Weike Cup】Sundek Officially Enters for the 2026 Outstanding Contribution Award for Optical Industry Application Solutions

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul