‘Daily Payment as Low as 29 Yuan’ for Car Purchase: A Brief Appearance and Swift Exit

06/23 2026

06/23 2026

544

544

Competition Persists

Eye-catching promotional slogans like 'daily payment as low as 29 yuan', 'equivalent to the cost of a daily cup of milk tea', and 'monthly payment of 1,918 yuan' once slashed the car purchase threshold. Yet, within a mere few months, the 'seven-year low-interest' car financing schemes, heavily promoted by numerous auto companies, have quietly vanished from major official platforms.

Presently, the official websites of several automakers, including Tesla, Li Auto, and Xiaomi, have reverted the maximum loan term in their financial policies to 60 months (5 years), signaling the complete withdrawal of seven-year low-interest auto loans. According to informed sources, starting from late April, banks and auto company financial services have progressively tightened their policies, directly discontinuing seven-year products. Previously, several auto companies had explicitly stated that these policies would be valid until April 30, 2026, with no decision yet on whether they would be extended. Now, as the first half of the year draws to a close and another round of price reductions begins, seven-year long-term loans have yet to stage a comeback.

This promotional frenzy, ignited by Tesla and fervently followed by over 20 auto companies, lasted just four months from collective escalation to abrupt exit. What's even more surreal is that this industry-wide 'sudden stop' occurred without any explicit official announcement but was a 'tacit' collective 'withdrawal' among auto companies.

Inherent Risks

After years of rapid growth in the Chinese auto market, loan-based car purchases have become the preferred option for many consumers. According to terminal research by the China Automobile Dealers Association, the comprehensive penetration rate of auto finance in terminal retail has reached 65%-70%, with first-tier and new first-tier cities generally exceeding 70%. Market research in the first half of 2026 indicates that the young customer base has elevated the overall level of auto finance penetration.

For some consumers, the monthly payments for three-year or five-year auto loans are relatively high, while the seven-year plan effectively distributes the repayment pressure. Hence, the allure of 'daily payment as low as 29 yuan' is significant, effectively lowering the car purchase threshold and repayment pressure. Seven-year low-interest auto loans once served as a potent tool for auto companies to boost sales.

However, this seemingly popular financial promotion has harbored numerous hidden risks from the outset. According to the current 'Administrative Measures for Auto Loans', the maximum compliant term for individual conventional auto loans is capped at five years. The seven-year car purchase plans on the market, apart from those offered by designated cooperative banks of auto companies, are mostly facilitated through financial institutions using personal consumer loans, finance leases, and other methods.

The distinction between finance leases and bank auto loans lies in the nature of the contracts: auto loans are 'loans,' whereas leases are 'sale and leaseback.' Bank loan plans are governed by the Civil Code's regulations on loan contracts and security interests, featuring strong compliance in traditional credit and stable funding sources. Under the sale and leaseback model, the vehicle is registered under the user's name, and the green certificate is retained by the user, but the ownership of the vehicle remains with the leasing company. The user 'rents back' the vehicle and pays rent, with full settlement leading to the release of the lien and complete ownership transferring to the user. This implies that behind the 'sweet deal' of low monthly payments, consumers may shoulder some hidden risks.

Compared to banks' stringent risk control systems, finance lease approvals are often more lenient, with faster loan disbursement, possibly without requiring bank statements or income proofs.

However, on the one hand, there are the potential risks associated with the finance lease model, and on the other hand, there is the increasing difficulty in controlling consumer personal credit risk. Compared to three-year or five-year repayment cycles, the seven-year ultra-long loan cycle is fraught with more uncertainties. It is well known that new energy vehicle models undergo rapid technological iterations and experience significantly increased depreciation rates, leading to a high likelihood that the vehicle's residual value will be lower than the remaining loan principal by the end of the repayment period, with a high risk of negative equity and default.

For both financial institutions and consumers, the risk of bad debt is an unavoidable hidden peril. This collective 'withdrawal' of seven-year low-interest loans by auto companies can also be viewed as a pivotal turning point to bid farewell to blind financial competition and revert to rational competition.

Competition Persists

Does the disappearance of seven-year low-interest loans signify that auto companies will no longer engage in financial competition?

Since the beginning of this year, the prices of raw materials such as lithium phosphate, copper, aluminum, and memory chips have surged, driving up car manufacturing costs. Unlike the previous general phase of 'holding firm,' most auto companies now find themselves in a predicament where 'even the landlord has no extra grain,' making price hikes a 'necessary move.'

As of May, over ten auto brands, including BYD, Tesla, Xiaomi, NIO, XPENG, Zeekr, and Exeed, have successively issued price adjustment announcements or tightened terminal discounts. Simultaneously, more subtle 'price increases' are also occurring: reduced free charging benefits, decreased financial subsidies...

A more severe reality is that the stimulating effect of price wars appears to have reached a bottleneck, with the market 'overexerting itself' and prematurely exhausting potential car purchase demand. Data reveals that from January to May 2026, domestic passenger car retail sales totaled 7.099 million units, a significant year-on-year decline of 19.5%. During this automotive market downturn, consumers' wait-and-see attitude towards car purchases is relatively strong.

Under the combined pressures of rising prices of desired car models, tightened long-term loan policies, and increased monthly payment burdens, consumers are inevitably reverting to their real financial constraints and pondering: Can I truly afford this car?

Tesla, the pioneer of seven-year long-term loans, has introduced a new solution: Easy Loan. It combines low down payments, low monthly payments, low interest, and low balloon payments, while also offering a high residual value buyback option.

Image source: Tesla

After the collective disappearance of seven-year long-term loans, the financial plans introduced by various auto companies, despite efforts to lower the car purchase threshold, do not seem to have the same immediate impact as seven-year low-interest long-term loans.

Taking a five-year plan as an example, for the rear-wheel-drive Model 3 priced at 235,500 yuan, the minimum down payment is 55,900 yuan, with monthly payments of 2,193 yuan, an annual interest rate of 0.99%, and a balloon payment ratio of about 20% (45,500 yuan). Additionally, Tesla China offers 0-interest and ultra-low-interest loan plans, with down payments starting from 79,900 yuan and 45,900 yuan, respectively. Among them, the ultra-low-interest plan has a minimum annual fee rate of 0.5%, equivalent to an annualized interest rate starting from 0.92%.

Other brands have also swiftly introduced real-time replacement financial plans, with validity periods generally until the end of May: Li Auto and Xiaomi Auto primarily promote flexible combinations of three-year 0-interest and five-year low-interest plans; NIO offers 5-year 60-installment financing for new models like the ES8, with the first 3 years (36 installments) enjoying a 0% annualized fee rate and the last 2 years (24 installments) having an annualized fee rate of 3%, also supporting 0-down-payment car purchases; XPENG, in collaboration with multiple institutions, provides interest subsidy support, with some models offering up to 30,900 yuan in interest subsidies for three-year 0-interest plans, while also offering diverse plans such as '2-year 0-interest' or '3 to 5-year low-interest.'

Nowadays, financial plans have become a staple tool for auto companies to sustain sales momentum. June, as a month for sprinting sales in the first half of the year, Chinese brands such as BYD, Changan, Geely, Chery, and Great Wall have all introduced flexible financial plans featuring 0 down payment, 0 interest, and up to 5-year low-interest rates, covering their main models or even their entire lineup; joint venture brands like FAW Toyota, Dongfeng Honda, and SAIC General Motors Buick also offer financial policies applicable to their entire lineup, such as 2-year 0-interest and '1-yuan loan' plans.

Dealerships aim to convert orders, and financial plans are designed to reduce the down payment and monthly payments to levels that are easier to close deals, enabling customers who 'want to buy but can't pay in full' to complete the purchase. When 'price wars' can no longer effectively stimulate consumption, 'financial concessions' are gradually replacing direct price cuts, spreading out car purchase costs over a longer period, and becoming the next 'battleground' for auto companies to compete for.

This article is original to China Auto News. Friends are welcome to share it. If media outlets need to reprint it, please indicate the author and source at the beginning of the article. Any media or self-media is prohibited from using any content of this article to create video or audio scripts, and violators will bear legal responsibility.

-

![]()

When AI Dominates 618, Is Human Live Streaming the Ultimate Challenge?

-

![]()

Behind SpaceX's IPO: Musk, Boasting a Trillion-Dollar Net Worth, Still Grapples with a Severe 'Cash Crunch'

-

![]()

【OFweek Weike Cup】CASTECH Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Accelink Technologies Competes for 2026 Outstanding Optical Component Supplier in Optical Industry

-

![]()

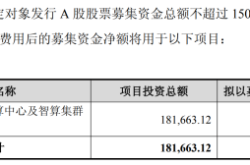

A Leading Computing Power Provider Secures 1.5 Billion Yuan in Private Placement, Expands Smart Computing Center to 12,000 Racks

-

![]()

【OFweek Weike Cup】Sundek Officially Enters for the 2026 Outstanding Contribution Award for Optical Industry Application Solutions

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul