End of CATL's Exclusive Supply! Reflections Behind HIMA's Signing with Three Battery Makers

06/23 2026

06/23 2026

494

494

In the MIIT's 408th batch of new vehicle declaration announcements, many noticed a key change on the information page of the updated AITO M6 BEV model: for the first time, Yichun Gotion High-Tech appeared in the column for power battery manufacturers.

This was no ordinary component switch. From Seres signing a five-year strategic cooperation with CATL in 2022 to the establishment of CATL's dedicated 'factory-within-a-factory' production line at the Chongqing AITO plant, HIMA's flagship models had long relied on CATL as the exclusive supplier. Gotion High-Tech's official inclusion marks the end of nearly four years of exclusive supply, ushering in a diversified adjustment.

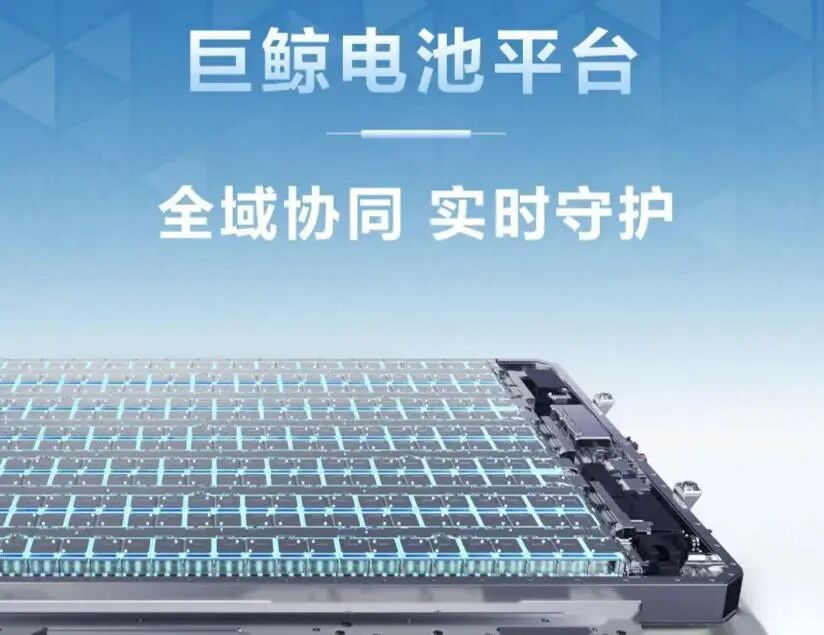

Subsequent industry developments confirmed this direction. At the 2026 Guangdong-Hong- KongMacao Greater Bay Area Auto Show, both Gotion High-Tech and CALB entered HIMA's exclusive exhibition hall as 'co-builders of the Whale Battery Platform.' According to various media reports, the Luxeed brand has added Gotion High-Tech and Sunwoda to its existing supplier base, while the Shangjie brand also plans to introduce Gotion High-Tech's LFP battery packs. Except for the ultra-high-end MAEXTRO, whose sales volume has not yet warranted adjustments, nearly all of HIMA's main brands are advancing supply chain diversification.

Much public discussion has focused on whether this signals a shift in cooperation between the parties. In reality, it is more about routine supply chain optimization driven by industry-scale development rather than a change in the cooperative relationship. This adjustment is fundamentally a highly pragmatic industrial move, driven by three core objectives: cost control, risk hedging, and production capacity support, ultimately affecting the entire lifecycle of consumer vehicle purchase, usage, and second-hand transactions.

Scaling Growth Demands Refined Management

Power batteries account for 30% to 50% of a new energy vehicle's total cost, making them a critical focus for cost control. Zeng Qinghong, Chairman of GAC Group, stated at a public industry forum that the high cost proportion of power batteries is a common challenge for the entire industry. Public financial reports show that in the first quarter of 2026, CATL's net profit reached RMB 20.738 billion. The scale effects and profitability of leading battery companies are at industry-leading levels, drawing more attention to cost optimization opportunities for vehicle manufacturers.

During the exclusive binding phase, HIMA had relatively limited bargaining flexibility in procurement pricing. A research report on the lithium battery industry by Soochow Securities estimated that the unit cost difference between cells from leading battery companies and second-tier manufacturers is approximately RMB 0.05 to 0.06 per Wh. While a few cents per Wh may seem insignificant, when applied to an 81kWh vehicle battery pack, the procurement cost per vehicle can differ by RMB 4,000 to 5,000. Scaled to annual sales of one million units, this represents cost optimization opportunities worth billions of yuan.

After introducing three new suppliers, HIMA gained more bargaining leverage. With four battery manufacturers forming healthy internal competition, the brand can split orders according to model positioning, using large-scale orders for entry-level models to drive suppliers to offer more competitive cooperation plans. This explains why the AITO M6 BEV can lower its starting price to RMB 229,800—optimization of battery procurement costs is one of the core supports for this terminal price reduction.

It is important to clarify that supply chain diversification does not mean lowering quality control standards. All suppliers entering the HIMA ecosystem must pass the unified technical review of the Whale Battery Platform, adhering to standardized BMS management protocols, safety testing standards, and warranty rules. Essentially, Huawei sets a unified technical baseline, and suppliers produce according to these standards, significantly reducing the adaptation costs associated with supply chain switches.

Zhu Jiangming, Chairman of Leapmotor, has summarized the core value of a multi-supplier model: it allows access to more cost-effective cells while balancing production capacities among suppliers, ultimately achieving controllable quality, cost, and risk. This logic applies equally to HIMA today.

Securing Supply Chain Autonomy

If cost reduction is the most immediate objective, dispersing supply chain risks represents a more fundamental strategic consideration. In recent years, the new energy industry has seen multiple cases where battery manufacturer production line maintenance or raw material supply fluctuations directly impacted the production schedules and delivery timelines of partner automakers. Under a single-supply model, capacity adjustments by suppliers can directly affect terminal users' vehicle delivery efficiency and purchase experience.

Cui Dongshu, Secretary-General of the China Passenger Car Association, has publicly analyzed that the widespread push by new energy automakers toward battery supplier diversification is an inevitable optimization direction as the industry enters large-scale development at the million-unit level. While a single-supplier model offers advantages in rapid R&D adaptation and low management costs during a brand's initial growth phase, its suitability for capacity flexibility and risk resistance declines once sales volumes surpass critical thresholds. A multi-supplier layout essentially trades moderate management investment for long-term supply chain stability and development autonomy.

HIMA employs a clear tiered supply strategy: high-end long-range versions and flagship models still prioritize CATL's ternary lithium batteries to maintain technological benchmark positioning, while entry-level high-volume LFP versions are split among Gotion High-Tech, CALB, and Sunwoda to distribute capacity pressure from large-scale orders. The geographical distribution of different manufacturers' production lines across regions also mitigates regional production fluctuations caused by extreme weather, regional power restrictions, or logistical disruptions.

Official data shows that from January to May 2026, HIMA's cumulative sales grew by 26.5% year-on-year, with an annual sales target set at 1 to 1.3 million units. Relying solely on a single supplier's capacity would struggle to support such rapid growth. A multi-supplier system adds multiple layers of protection to the supply chain—if one supplier faces capacity constraints, others can quickly step in, preventing terminal users from enduring long waits or missing market windows due to insufficient capacity.

Bidirectional Optimization of Consumer Experience and Industrial Ecosystem

Supply chain adjustments ultimately impact consumers' actual experiences. Many vehicle owners are most concerned about whether switching to different battery brands will lead to noticeable differences in usage experience, warranty policies, or second-hand vehicle residual values.

First, regarding basic vehicle usage and warranties, users need not worry excessively. HIMA offers unified lifetime warranties for the three electric systems (battery, motor, and electronic control) across all models, with no differences based on battery suppliers. The unified BMS management system also minimizes most cell performance variations, with CLTC range differences among similarly configured models typically controlled within 15 kilometers and fast-charging peak power largely consistent. In daily commuting scenarios, ordinary users are unlikely to perceive significant differences.

The real area of difference lies in second-hand residual values. Currently, the domestic second-hand vehicle market generally holds CATL cells in higher regard, with industry surveys showing that about 38% of second-hand new energy vehicle buyers prioritize models equipped with CATL batteries. In the short term, when reselling similarly conditioned vehicles, those with CATL batteries are likely to command a small premium of RMB 3,000 to 6,000. However, for vehicles held for over five years, supported by unified warranty policies, the residual value gap will gradually narrow.

For CATL, this adjustment does not signify a weakening of its core cooperative relationship, but the proportion of exclusive supply models in the industry is gradually declining. Not only HIMA but also mainstream new energy brands like Tesla, Li Auto, and XPENG have fully adopted multi-supplier strategies. The model of a single automaker exclusively binding with a leading battery manufacturer is gradually exiting the mainstream market. In the short term, CATL's order share within the HIMA ecosystem will decline, prompting further optimization of its pricing system to remain competitive. In the long term, collective decentralized procurement by automakers will drive the industry's supply-demand relationship toward greater equilibrium, while second-tier manufacturers can leverage supply chain endorsements from leading automakers to unlock more market opportunities.

Looking back at this supply chain adjustment, rumors of a cooperation breakdown do not hold water. It resembles a routine optimization move that leading automakers undertake as the new energy industry enters a phase of Stock competition (stock competition). From early-stage binding with leading battery manufacturers to rapidly complete product ramp-up, to later-stage pushing for supply chain diversification after sales momentum builds, regaining cost and risk autonomy—this path taken by HIMA has already been traveled by Tesla, Li Auto, and XPENG.

From CATL's perspective, a decline in exclusive supply proportions is not necessarily negative—industry competition ultimately hinges on technology and cost. The era of single exclusive cooperation as an industrial phase is gradually fading, with Multi dimensional collaboration (multi-faceted collaboration) becoming the new industry norm. For ordinary consumers, there is no need to overly fixate on cell brands—under the premise of meeting unified safety standards and consistent warranty policies, more affordable versions offer better cost-effectiveness. What consumers should focus on is whether automakers provide transparent disclosure of supplier information, granting users full right to know (right to information) and option (right to choose).

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry