Three Major New Policies Come into Force on the Same Day, Revolutionizing the Growth Dynamics of China's Auto Market

06/24 2026

06/24 2026

558

558

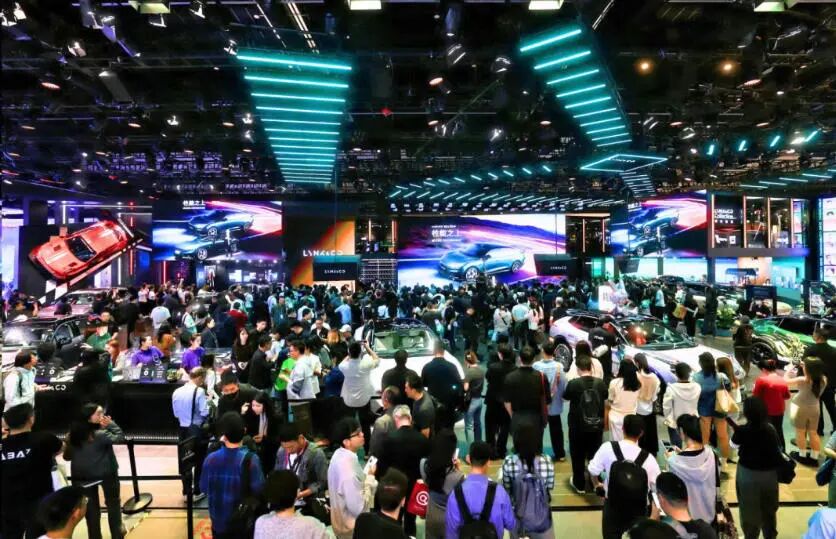

On June 23, the Information Office of the State Council convened a press conference to unveil measures aimed at boosting auto consumption throughout the entire supply chain. This was far from a routine policy announcement—it signified the simultaneous rollout of three significant policy packages. The Ministry of Commerce, in concert with several other departments, introduced pilot reforms for auto circulation and consumption, alongside new policies to foster aftermarket development. Meanwhile, the Ministry of Industry and Information Technology (MIIT) and the Ministry of Public Security optimized information sharing for vehicle certification. From purchasing and usage to automotive enthusiast activities and vehicle retirement, bottlenecks in consumption across the automotive lifecycle are being systematically dismantled.

Previous discussions on stimulating auto consumption often centered narrowly on new vehicle sales figures, with policies tailored for short-term sales support. This time, the approach is fundamentally different. It encompasses the entire vehicle lifecycle, from sale to retirement, effectively constructing a self-sustaining ecosystem for China's automotive market in the era of inventory management, rather than seeking one-time market surges.

Trade-ins Fuel Efficiency Improvements in the New Vehicle Market

The trade-in policy, now in its third year, remains the bedrock of new vehicle consumption. As of June 22, 2026, the program has facilitated over 21 million trade-ins, with average subsidies of RMB 14,000 per vehicle, accounting for 63% of the RMB 5 trillion total in consumer goods trade-ins nationwide—making it the most impactful stimulus measure across all categories.

The policy's industrial impact is equally pronounced. Official data reveals that trade-ins have supported the purchase of over 12 million new energy vehicles (NEVs). By 2025, NEV penetration in domestic passenger vehicles reached 53.9%, up 18.2 percentage points from 2023 levels. This trend accelerated in 2026, with April and May penetration rates hitting 61.4% and 62.9% respectively—surpassing 60% for two consecutive months. Domestic passenger vehicle retail sales reached a record high of 23.74 million units in 2025, with over 40% benefiting from trade-in subsidies. Replacement demand has emerged as the cornerstone of the new vehicle market.

Beyond financial incentives, the purchasing process has been streamlined. The MIIT and Ministry of Public Security's new policy for real-time certification information sharing enables domestic passenger vehicles to complete purchase and registration on the same day, benefiting over 20 million new vehicles annually.

Lower-tier markets are also being targeted through initiatives like the "Thousand Counties, Ten Thousand Towns" consumption campaign and ongoing NEV promotion in rural areas. Charging and after-sales networks are expanding into counties and townships, addressing long-standing service gaps in these regions.

In essence, the growth logic of the new vehicle market has undergone a profound transformation. The era of relying on new user acquisition for incremental growth is fading. Current growth is driven more by iterative demand within the existing vehicle stock, compounded by transactional efficiency gains from process optimization. For automakers, competing for new customers will become less cost-effective. The future competitive edge will likely depend on providing superior trade-in services and mastering replacement cycles.

Two-Way Circulation Between the Auto Market and Recycling

The breakthroughs in used cars and end-of-life vehicles represent the policy's most underappreciated long-term value. In 2025, used car transactions exceeded 20 million units for the first time, with inter-provincial transfers reaching 31.1%. More symbolically, the ratio of new vehicle sales to used car transactions approached 1:1, up from just 0.6:1 a few years prior.

This ratio reversal reflects years of policy liberalization in circulation. National cancellation of used car relocation restrictions, simplification of cross-provincial registration, "reverse invoicing" to optimize tax costs, and the gradual implementation of a national used car information platform have all dismantled long-standing regional barriers and trust issues. From January to May 2026, despite overall market pressure, used car transactions reached 8.1 million units, growing 2.3% against the trend—highlighting the resilience of the circulation sector.

The end-of-life recycling sector is also expanding. In 2025, 9.8 million vehicles were recycled, 4.7 times the 2020 volume. By the end of 2025, China had 1,996 licensed recycling enterprises, with over 75% capable of dismantling NEVs.

The trade-in policy alone has driven the recycling of over 8 million old vehicles, enabling the circular use of nearly 10 million tons of recycled materials. Recycling layouts for new components like power batteries are also advancing, complemented by crackdowns on illegal recycling. The entire system is transitioning toward refined operations.

In mature markets, used car transactions typically far exceed new vehicle sales. Having just crossed the 1:1 threshold, China still has significant room for growth. Improved efficiency in circulation and recycling will accelerate the vehicle replacement cycle, in turn sustaining replacement demand in the new vehicle market—a far more impactful outcome than one-time subsidies.

Aftermarket Consumption Shifts Toward Usage

While new and used vehicle policies stimulate transaction volumes, the aftermarket 2.0 policies unlock incremental consumption across the automotive lifecycle. Announced alongside the press conference were new aftermarket cultivation policies from nine departments and a list of 40 pilot cities for auto circulation and consumption reform, marking the sector's transition from top-level design to pilot implementation.

Industry data already underscores the aftermarket's explosive potential. The global automotive aftermarket has surpassed USD 1 trillion, with the Asia-Pacific region poised to become the largest market this year. Domestically, over 50% of passenger vehicles are now over seven years old, entering a period of rapid aftermarket growth. Compared to the 2023 version 1.0, the 2.0 policies cover six major areas—vehicle customization, RV camping, classic cars, maintenance insurance, auto racing, and car rental—with 17 specific measures addressing previous regulatory gaps and standardization issues.

The 40 pilot cities serve as policy testbeds with clear regional focuses: Beijing emphasizes vehicle customization, intelligent connectivity, and classic cars; Hangzhou and Shenzhen explore optimized vehicle purchase quotas; Baoding focuses on auto racing; Yangzhou develops RV camping; and Xiong'an innovates cross-city commuting through car rental models.

Additional pilot initiatives include bonded vehicle customization, classic car "bonded exhibition" models, "battery-as-a-service" insurance, and tiered customization management. Infrastructure optimizations for RVs and campsites are also planned. The 2026 Shanghai F1 Grand Prix, which attracted 230,000 spectators (16% international), exemplifies the cultural consumption potential of automotive events.

This represents a fundamental shift from "purchase management" to "usage management" in automotive consumption. With 370 million vehicles on the road, services, culture, and entertainment derived from vehicle usage constitute the next trillion-dollar growth sector. Aftermarket cultivation will not happen overnight—it requires synchronized development of standards, talent, and culture, testing the industry's long-term operational capabilities rather than short-term profit-seeking.

Overall, the policies implemented on June 23 are not aimed at achieving short-term sales spikes through heavy stimulus but at dismantling institutional bottlenecks across the supply chain through reform, creating a self-sustaining automotive ecosystem.

The fundamental drivers of China's automotive market remain robust, but the engines of growth have fundamentally shifted. The incremental gains from new vehicle adoption now give way to efficiency improvements in circulation and aftermarket expansion. Industry players who grasp this transition earliest will gain a competitive edge in the next phase.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?