Charging Industry Shifts from Quantity to User Experience as New Benchmark

06/24 2026

06/24 2026

420

420

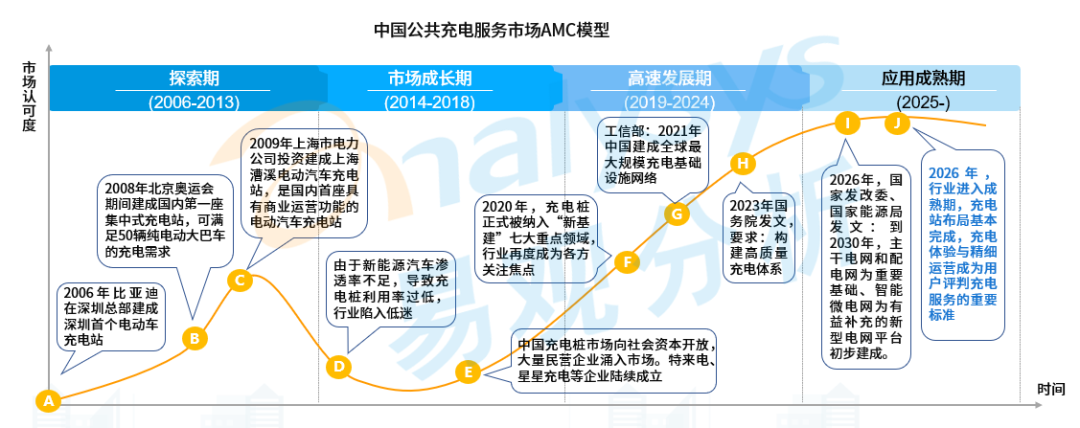

Analysis: The rapid advancement of China's new energy vehicle (NEV) sector is propelling the public charging service industry to a pivotal juncture. Reflecting on the growth of China's public charging services, the industry has transitioned through phases of exploration, growth, and rapid expansion. The State Council's directives to establish a high-quality charging infrastructure system signal China's public charging service market's entry into a mature phase by 2025.

Against this backdrop, a significant transformation has occurred in the supply-demand dynamics of public charging infrastructure. Data shows that as of March 2026, China's public charging guns have reached 4.863 million units. Analyzing the ratio of charging piles to vehicle increments, a key indicator of supply-demand balance, reveals a rapid optimization from 1:3.7 in 2021, 1:2.7 in 2022, 1:2.8 in 2023, and 1:2.7 in 2024, to 1:1.9 in 2025, and further to 1:1.4 in the first quarter of 2026. This indicates that China's public charging infrastructure construction can now generally keep pace with the rapid growth of NEVs, with the large-scale expansion of the supply side largely completed.

However, the abundance of total supply has not translated into a simultaneous improvement in user charging experience. Under the long-standing inertia of blind expansion in the industry, traditional evaluation systems have often focused solely on the number of connected charging piles and guns as the benchmark for measuring enterprise and industry development. This "quantity-only" evaluation system has led to severe industry imbalances, trapping the industry in a vicious cycle of extensive competition that prioritizes scale over service quality. To align with the trend of the public charging market transitioning from "scale expansion" to "quality improvement," there is an urgent need to reconstruct industry evaluation standards. A new evaluation framework centered on user charging service experience, encompassing industry, enterprise, and user dimensions, is emerging as a new guide for promoting high-quality development in public charging services.

I. Market Overview: Characteristics and Differentiation Among Three Types of Operators

As the industry matures and new standards are established, the competitive landscape of China's public charging service market has shown clear differentiation. Currently, the key players in the market are primarily divided into three categories: state-owned and central enterprise operators, such as State Grid (e-Charge), China Southern Power Grid (ShunYichong), PetroChina (Kunlun Net Power), and Sinopec (Shihua E-Power); automaker-affiliated operators, including Tesla, BYD, XPENG, and Li Auto; and third-party operators, encompassing asset-heavy operators like Teld, StarCharge, and Wanma Aichong, as well as asset-light operators such as Didi Charge (formerly Xiaoju Charge), Yunkuai Charge, Xindiantu, and Kuaidian. These operators each possess distinct characteristics in terms of asset models, network layouts, and operational strategies.

From a market share perspective, the leading player effect is highly pronounced. As of March 2026, the total number of public charging guns in China's public charging market has reached 4.863 million units. Among them, the top ten operators in terms of public charging gun stock collectively own 2.45 million units, accounting for approximately 50% of the total stock. The top three operators are Teld (480,000 units), StarCharge (380,000 units), and Didi Charge (370,000 units). In terms of charging volume, the total annual charging volume in China's public charging market (excluding dedicated charging) was approximately 57.35 billion kWh in 2025, showing a generally increasing trend on a monthly basis. Among the market shares of public charging volume as of March 2026, Didi Charge accounts for over 34%, followed closely by Yunkuai Charge, StarCharge, Teld, and Xindiantu. This highly concentrated market landscape imposes higher requirements on enterprises to compete in terms of efficiency and service quality.

II. Industry Level: Transition from "Scale Expansion" to "Quality Improvement"

From an industry perspective, the traditional "quantity war" has significantly hampered the healthy development of the public charging industry. Under the traditional evaluation standard centered on the number of charging guns, the industry evaluation system has become severely imbalanced, misguiding the development direction of enterprises and leading to substantial resource waste. Due to the lack of reasonable planning and guidance for refined operations, a large number of inefficient and "zombie" charging piles have proliferated in the market, occupying valuable land and grid capacity resources and resulting in a rough and disorderly overall industry development.

The reconstructed industry-level evaluation standard shifts its focus towards refinement and high-quality development. The new standard no longer solely counts the physical number of charging piles but places greater emphasis on the optimization of infrastructure layout, equipment operation and maintenance support, standardization and intelligent upgrading of services, and transparency of charging fees. In the mature phase of the industry, evaluating the energy replenishment network of a region or an operator hinges on its ability to promote standardized and refined industry development, effectively avoid resource waste, and guide the overall industry towards a sustainable development trajectory.

High-quality development at the industry level also necessitates deep integration of the energy replenishment network with the construction of a new type of power grid, facilitating the transition of the grid from "centralized regulation" to "source-grid-load-storage coordination" through digital aggregation and bidirectional energy interaction. The aggregation of massive charging loads and energy storage resources can form dispatchable virtual power plants, participating in electricity spot markets, demand response, and carbon trading, thereby opening up new revenue streams for energy services. Simultaneously, upgrading charging piles to V2G (vehicle-to-grid) nodes through bidirectional interfaces enables electric vehicles to serve as mobile energy storage units, discharging to the grid during peak load periods, thereby reducing grid expansion investments and enhancing the collaborative efficiency of the entire energy industry.

III. Enterprise Level: From "Quantity-Only" to "Efficiency and Profitability"

From an enterprise perspective, the traditional evaluation yardstick has led enterprises into blind heavy-asset expansion and vicious price wars. To gain an advantage in terms of the number of charging guns, enterprises have blindly expanded their scale while neglecting equipment reliability, operation and maintenance efficiency, and user experience. This has resulted in high equipment failure rates, slow service responses, and significant asset depreciation pressures and profitability challenges.

Guided by the new standards, the evaluation dimensions at the enterprise level have shifted towards profitability, single-pile operational efficiency, and core competitiveness. In this process, the average number of vehicles charged per charging gun per day and the ratio of fast-charging guns have become two key hard indicators for measuring enterprise operational quality. The average number of vehicles charged per public charging gun per day directly reflects the operational efficiency and actual usage intensity of a single pile, determining whether the revenue from a single pile can cover fixed costs such as depreciation, electricity fees, and operation and maintenance. This is crucial for enterprises to break free from price wars and enhance profitability. Simultaneously, this indicator can truly reflect demand differences across regions, scenarios, and time periods, guiding enterprises to precisely shut down inefficient piles and intensify deployment in high-demand areas, achieving a transition from "quantity emphasis" to "efficiency emphasis."

The new standard encourages enterprises from different camps to leverage their respective advantages and upgrade the single "electricity sales" model to a comprehensive "charging + commercial" service space through refined platform operations, membership subscriptions, co-branded subsidies, and other means. This involves overlaying services such as rest areas, dining, retail, and maintenance at charging stations to expand profit margins.

IV. User Level: Reshaping the Ultimate Value Yardstick with "Authentic Energy Replenishment Experience"

From a user perspective, traditional quantity indicators are completely detached from users' actual charging experiences. Prominent issues encountered by users during actual charging, such as frequent equipment failures, slow charging speeds, opaque pricing, and gasoline vehicles occupying charging spots, have been entirely overlooked in the traditional "quantity war," resulting in low user satisfaction levels.

The new standard places user charging experience as the ultimate evaluation yardstick. The 3,000 vehicle owner questionnaires conducted by Analysys in the top 30 cities in terms of NEV ownership provide detailed data support for the user-level evaluation standard:

Firstly, charging speed and efficiency. Over 70% of NEV owners prioritize fast-charging guns when charging, indicating that owners' demand for fast charging has become normalized. Reducing charging time and popularizing high-power ultra-fast charging to compress energy replenishment duration to the minute level are core elements for meeting users' fragmented energy replenishment needs and enhancing their time efficiency.

Secondly, charging stability and safety. Users expect operators to ensure the stability of power supply and facilities, eliminate equipment issues such as sudden disconnections and power outages, and ensure the certainty of energy replenishment. Simultaneously, safety protection needs to evolve from "basic compliance" to "comprehensive protection." Not only must the equipment itself be reliable, but it must also consider payment and data encryption security on the network side, as well as site monitoring, lighting, and other aspects to ensure the personal safety of vehicle owners, jointly building user trust in safety value.

Thirdly, economy and convenience. Reducing charging prices and improving APP operational experiences are the most urgent expectations of vehicle owners. Owners expect operators to lower actual electricity costs through refined operational methods such as membership systems and package plans (e.g., monthly cards, annual cards, fast-charging packages). In terms of APP usage, users expect further optimization of the operational experience to help them quickly locate the most cost-effective charging stations and improve information on supporting services at and around charging stations, eliminating concerns during the process of finding charging piles and waiting for charging.

Under these user-level evaluation indicators, the awareness and satisfaction levels of mainstream brands in the market also exhibit clear tiers. Surveys show that Didi Charge, Teld, and StarCharge are the top three brands in terms of user brand awareness, accounting for 44.1%, 33.7%, and 28.3%, respectively. In terms of comprehensive user satisfaction scores (including dimensions such as overall satisfaction, charging pile coverage, charging experience, charging speed, and charging safety), Didi Charge, Teld, and Yunkuai Charge rank in the top three. In terms of user recommendation rates, Didi Charge, Teld, and StarCharge occupy the top three positions. This indicates that enterprises capable of effectively addressing user pain points and providing efficient and stable services have already gained a first-mover advantage in the new user-level evaluation system.

New Standards Pave the Way for a New Future in Public Charging

China's public charging service market has bid farewell to the old era of blindly claiming land and building charging piles. The newly reconstructed evaluation standards are outlining a clear development blueprint for the entire industry from three dimensions: standardized and high-quality development at the industry level, improved operational efficiency and profitability at the enterprise level, and enhanced energy replenishment experience and service satisfaction at the user level.

Public charging service operators must closely follow this trend, shifting their development focus from scale expansion to refined operations. On the basis of ensuring equipment safety and stability, they should enhance charging efficiency, innovate business models, and thereby achieve true high-quality development in the mature phase.

Research Description

The industry analysis provided by Analysys is primarily based on industrial macro data, quarterly survey data from end-users, historical data from manufacturers, and quarterly business monitoring information of manufacturers. Utilizing Analysys's industry analysis model and combining market research, industry research, and manufacturer research methods, the analysis mainly reflects market status, trends, turning points, and patterns, as well as the development status of manufacturers.

Analysys believes that the data obtained through the aforementioned industry research methods accurately reflects industry trends and patterns within an industry-accepted margin of error.

The research results obtained through professional research methods are intended for decision-making reference. For actual manufacturer data, please refer to the financial reports published by the manufacturers.

Copyright Notice

The third-party data and additional information referenced by Analysys in this article are drawn from publicly accessible sources, for which Analysys bears no responsibility. Under no circumstances should this article be regarded as a definitive basis; rather, it is intended solely for reference purposes. The copyright of this article is held by the publisher. Any reproduction, quotation, or utilization in any form of content published by Analysys is strictly forbidden without prior authorization from Analysys. Should any authorized media, website, or individual wish to use this content, they must quote the original text in its entirety and clearly indicate the source. Furthermore, the analysis and viewpoints presented should strictly adhere to the official content released by Analysys, without any alterations such as deletions, additions, splicing, interpretations, or distortions. Analysys disclaims all responsibility for any disputes that may arise from the improper use of this content and reserves the right to seek recourse from the relevant responsible parties.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?