UK Prime Minister Starmer Resigns: Will Chinese Automakers' 'British Springboard' Remain Stable?

06/25 2026

06/25 2026

480

480

On June 22, UK Prime Minister Keir Starmer announced his resignation as leader of the Labour Party and stated he would step down as Prime Minister after a new party leader is elected.

This marks the sixth UK Prime Minister to leave office prematurely since the 2016 Brexit referendum. For the British public, prime ministerial turnover seems to have lost its novelty. Following the news, UK media continued to humorously reference the well-known phrase, 'fluid prime ministers, steadfast Chief Mouser to the Cabinet Office.'

However, for Chinese automakers accelerating their European expansion, this seemingly familiar political transition is far from just a political anecdote for casual discussion.

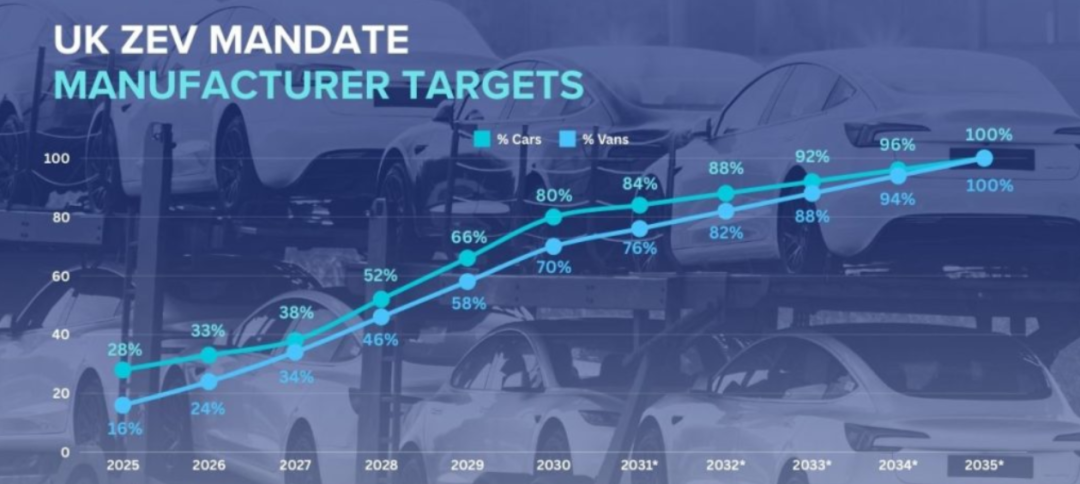

With Starmer's resignation, the pace of certain pending UK automotive industry policies has come under renewed market scrutiny. For instance, just a week before his resignation, UK media widely reported that his cabinet had planned to officially announce the relaxation of the 'Zero Emission Vehicle (ZEV) Mandate'—lowering the legally required minimum share of pure electric vehicles (EVs) in new car sales from the originally set 80% to 50% by 2030.

What lies ahead for this policy?

Yet this is merely the starting point for questions. A series of related inquiries follow: How will the UK's domestic automotive manufacturing industry respond to potential adjustments in the new policy pace? Will the strategic layout (layout) of Chinese automakers using the UK as a springboard into the European market remain valid? Will the special connection between 'Made in the UK' and 'Made in the EU' within the trade rule system be affected? Meanwhile, the European Commission is considering imposing anti-subsidy tariffs on Chinese plug-in hybrid electric vehicles (PHEVs). At such a delicate juncture, how will the UK's political transition influence this broader industrial and trade game theory (game)?

To answer these questions, it may be necessary to consolidate several events that have dense (intensively) occurred over the past three weeks and re-examine them.

Chery and Nissan: A Prudent Memorandum

Rewinding to June 3, nineteen days before Starmer's resignation announcement, Nissan Motor and Chery International UK signed a Memorandum of Understanding (MoU) to explore the possibility of Nissan's Sunderland plant in the UK contract manufacturing Chery's passenger vehicles, with production potentially starting as early as the 2027 fiscal year.

Cited by UK media with industry analysis, if the collaboration materializes, it would mark the first instance of a Chinese automaker engaging in large-scale contract manufacturing in the UK.

The industrial context at the time provided a realistic foundation for this cooperation. According to The Guardian and Nissan's official data, Nissan's Sunderland plant produced approximately 273,000 vehicles in 2025, significantly below its annual design capacity of 500,000 to 600,000 units. In May of the same year, Nissan announced further consolidation of its own models, such as the Qashqai and Leaf, onto the second production line, leaving the first line idle—a key opportunity for Chery to enter negotiations.

For both parties, this collaboration addresses practical needs. Chery can accelerate its localization strategy by leveraging an existing UK manufacturing system, while Nissan has the opportunity to improve plant capacity utilization, share fixed operating costs across its manufacturing base, and enhance the long-term sustainability of the Sunderland plant. Nissan also emphasized that plant ownership would remain 100% under Nissan, with related production line employees continuing to be employed by Nissan.

Chery's market performance in the UK also supports this collaboration. According to data from the UK's Society of Motor Manufacturers and Traders (SMMT), Chery's multiple brands (including Chery, Omoda, Jaecoo, etc.) accounted for approximately 6% of new car registrations in the UK during the first four months of 2026. Among them, Jaecoo registered over 20,000 units within seven years, ranking among the top three single-model registrations in the UK. As of May 2026, its brand dealership network covered 126 sales outlets across Great Britain.

Notably, Nissan's announcement retained significant commercial flexibility, explicitly stating that the 'MoU is non-binding, and negotiations between the two parties are ongoing.' For transnational manufacturing collaborations, such non-binding memoranda are standard industry practice, allowing room for adjustments in capacity planning, supply chain arrangements, and external policy environment changes. The policy pace changes resulting from Starmer's resignation represent one of the variables requiring ongoing assessment during the MoU's advancement.

In fact, Chery has previously utilized Nissan's existing manufacturing system to advance its internationalization strategy. In January of this year, Chery South Africa signed an agreement with Nissan to acquire assets of Nissan's vehicle assembly plant in Rosslyn, including land, factories, and stamping production lines, while retaining most of the original workforce. From Rosslyn, South Africa, to Sunderland, UK, these two collaborations, though in different markets, reflect a similar industrial logic: amid global automotive industry restructuring, Chery is accelerating localization through mature manufacturing systems, while Nissan is revitalizing existing manufacturing resources to find new growth opportunities for traditional production bases.

TCA Rules of Origin: The Threshold for the 'British Springboard'

Before discussing the potential impacts of UK political changes, it is essential to clarify the institutional foundation underlying this 'British Springboard' strategy. Some argue that the reason Chinese automakers view the UK as a critical node for entering the European market lies not in the UK itself but in the 'rules of origin' established by the UK-EU Trade and Cooperation Agreement (TCA).

According to TCA regulations, for vehicles manufactured in the UK to enter the EU market tariff-free, they must meet specific local value content requirements. From 2024 to 2026, a relatively lenient transitional arrangement applies: at least 40% of the vehicle's value and at least 30% of the battery's value must originate from the UK or EU.

However, this transitional arrangement represents the final extension previously negotiated between the UK and EU.

A report by the UK Trade Policy Observatory (UKTPO) states that starting January 1, 2027, the TCA will enter its final rule phase: at least 55% of the vehicle's value must originate from the UK or EU, while electric vehicle batteries must meet 'qualified battery' standards, meaning cathode materials—a critical component—must originate from the UK or EU. Simultaneously, the UK and EU have locked this rule framework until 2032, with no further adjustments in principle (in principle) expected before then.

This means a compliance threshold must be crossed through supply chain localization to 'assemble in the UK' and 'enjoy trade benefits associated with UK-made status.'

An analysis report released in April this year by UK Customs consultancy CSG points out that the most challenging link currently lies in cathode active materials (CAM). Accounting for over 35% of the value of lithium-ion battery cells, CAM represents one of the most difficult critical components to supply at scale within the UK and EU.

In other words, the TCA rules of origin constitute the core institutional constraint for Chinese automakers using the UK as a gateway to the EU market. This constraint will not change due to a prime ministerial resignation, nor will it loosen or tighten because of a political transition. For Chinese automakers planning to establish production in the UK, synchronously planning supply chain localization from the project evaluation stage is far more critical than speculating about the identity of the next UK Prime Minister.

SAIC MG's Alternative European Path

Around the same time as the Chery-Nissan MoU was signed in early June, SAIC MG announced plans to build its first complete vehicle (vehicle) factory within the EU in Galicia, Spain. The project involves an initial investment of approximately €200 million, with a planned annual capacity of 120,000 units, expected to commence production in 2028 and create over 2,000 local jobs.

According to CnEVPost, a key driver for this project is to address the EU's anti-subsidy tariffs imposed on Chinese pure electric vehicles. As one of the companies most affected by the highest tariff rates, SAIC's pure electric vehicles face a 10% standard vehicle tariff plus an additional 35.3% anti-subsidy tariff in the EU market, resulting in a combined tariff rate of 45.3%. In this context, relocating manufacturing directly into the EU represents the most straightforward compliance solution under existing trade rules.

Data supports this strategic choice. According to SAIC Motor, the MG brand sold 307,000 vehicles in the European market in 2025, up 26% year-on-year, becoming the first Chinese automotive brand to rank among the top 20 in European vehicle sales. Wang Hao, head of MG Europe, previously stated that surpassing 300,000 annual sales represents a critical economic feasibility threshold for initiating local factory construction.

The choice of Galicia also reflects clear strategic considerations. The region boasts mature port infrastructure and maintains convenient maritime links with the UK, MG's most important single market in Europe. According to information cited by Electrive, this was a key reason for selecting Spain over other candidate regions.

Thus, two distinct European paths have emerged: Chery leverages existing UK manufacturing systems and capacity resources to enter the market, while SAIC MG pushes further into local production within the EU. Facing evolving trade environments and regulatory pressures, leading Chinese automakers have not provided a unified approach but are instead identifying the most feasible localization methods under different institutional frameworks. These paths correspond to varying investment scales, implementation timelines, and risk structures, reflecting the trend of Chinese automotive globalization entering a deeper phase of localized competition.

The 'Whispered' PHEV Tariffs

Amid the UK's political changes, Germany's Handelsblatt reported that the European Commission is advancing a policy action with more direct implications for Chinese automakers' hybrid strategies: launching an anti-subsidy investigation into Chinese plug-in hybrid electric vehicles (PHEVs) and paving the way for subsequent anti-subsidy tariffs.

This policy shift was not entirely unexpected.

In October 2024, after the EU formally imposed anti-subsidy tariffs on Chinese-made pure electric vehicles, Chinese brands swiftly adjusted their export structures, shifting more resources toward PHEV models subject to only the standard 10% tariff. An assessment report by the Mercator Institute for China Studies (MERICS) approximately one year after the tariff implementation noted that Chinese brands' market share in the EU had effectively doubled, 'partly due to a quadrupling of PHEV exports.'

Market data further confirms the intensity of this shift. German media recently reported that in May 2026, BYD became the best-selling PHEV brand in the German market for the first time, with 4,290 monthly registrations. Its Seagull DM-i (overseas model name Atto 2 DM-i) and Seal U DM-i ranked first and second in sales, respectively.

According to Handelsblatt, citing senior EU officials, the European Commission plans to initiate anti-subsidy proceedings against Chinese hybrid vehicles 'within the coming weeks,' involving companies such as BYD, Chery, and SAIC. The report noted that preparatory work is largely complete and can proceed rapidly after securing qualified majority support from member states. Meanwhile, the Commission plans to submit a comprehensive review of trade defense tools in the third quarter of 2026 to provide a procedural framework for subsequent actions.

A detail disclosed by Electrive is particularly noteworthy: as recently as January this year, the European Commission publicly denied plans to take action against Chinese PHEVs; yet barely six months later, related investigations have entered the preparatory stage. For Chinese automakers, this means the PHEV pathway, previously serving as a buffer against BEV tariffs, is narrowing faster than market expectations. Regardless of the final tariff rates, a clear signal has emerged: the EU is gradually extending its trade defense tools from pure electric vehicles to hybrids, further compressing Chinese automakers' policy buffer space in the European market.

The Industry Cares More About Timelines Than Prime Ministers

Compared to the EU's PHEV tariffs, still in the 'whispering' stage, adjustments to the UK's ZEV mandate have a more direct impact on the local automotive industry. However, among the policy uncertainties triggered by Starmer's resignation, the truly noteworthy aspect may not be the identity of the next Prime Minister but the prolonged timeline for a policy adjustment yet to complete legal procedures.

According to some UK media reports, Starmer had internally approved a revised plan to lower the 2030 pure EV sales target from 80% to 50%, but this revision is not yet effective policy. It still requires initiating a statutory consultation process, which, under UK procedures, needs support from regional governments such as Scotland and Wales. Only after completing consultation and review processes can it be implemented nationwide. Therefore, the political transition period following Starmer's resignation directly extends the waiting time for initiating this process.

This impact is particularly tangible for Nissan. According to Car Dealer Magazine, citing the Financial Times, Nissan is currently negotiating a new investment plan for its Sunderland plant with the UK government but has explicitly stated it will not make a formal investment decision until the ZEV revision is finalized.

This means that the future capacity planning and investment arrangements for the Sunderland plant are still awaiting further clarity in the policy environment. Moreover, if the cooperation project between Chery and Nissan eventually materializes, the manufacturing system it relies on will also be influenced, to a certain extent, by the pace of this investment decision.

In fact, controversies surrounding the ZEV policy had already fully emerged before Starmer's resignation. The side supporting relaxed targets mainly consists of vehicle manufacturers and dealer groups. The UK's National Franchised Dealers Association (NFDA) explicitly welcomed the downward revision of targets, arguing that the 80% BEV requirement “does not reflect genuine consumer demand.” Sharon Graham, General Secretary of the Unite union, publicly stated that the current targets are “accelerating job losses in the UK automotive industry” and called for further reductions. On the other side, the debate primarily involves charging infrastructure companies and new energy investors. ChargeUK, a UK charging infrastructure association, warned that further weakening the ZEV mandate could “throw the entire electrification transition into chaos.” Some charging operators even jointly wrote to the government, stating that if targets were significantly reduced, they would reassess investment plans totaling over £2 billion. Research by ChargeUK indicates that maintaining the current mandate could create £15.5 billion in value for the UK economy and support approximately 71,000 jobs by 2035.

From a deeper perspective, the essence of the disagreement between these two sides reflects a clash of two business logics in the transformation of the UK automotive industry: one emphasizes traditional manufacturing competitiveness and employment stability, while the other highlights the long-term trends of the new energy supply chain and infrastructure investment... Therefore, regardless of who becomes the next UK Prime Minister, these two forces will persist and continue to compete in subsequent policy consultation processes.

For automakers planning capacity in the UK, the most critical time pressure comes from two parallel rule systems. On one hand, the TCA rules of origin will reach their final threshold in January 2027, with clear compliance requirements already established. On the other hand, the UK's ZEV amendment proposal is still awaiting the launch of formal consultation procedures. The former requires companies to accelerate local supply chain layout (localized layout), while the latter relates to the pace of electrification and investment return expectations in the future UK market.

When one set of rules is already locked in while the other remains uncertain, the difficulty of decision-making for companies regarding capacity allocation, supply chain construction, and capital investment naturally increases. This temporal misalignment may well be the most noteworthy risk window at the current industry level.

Preparing the Next Springboard

Combining the above clues, the UK's political transition has indeed added a temporal variable to certain industrial policies still under review or legislation. However, if the strategic layout (layout) of Chinese automakers between the UK and EU is primarily attributed to predictions about individual political figures, it would overlook a more fundamental reality: what companies truly face is an institutional framework composed of trade rules, rules of origin standards, and electrification targets.

For Chinese automakers, what truly requires continuous observation is whether the UK and EU can maintain sufficient continuity in trade rules, rules of origin systems, and electrification policies.

From this perspective, whether it is Chery's still-under-evaluation cooperation with Nissan in Sunderland or SAIC MG's push for localized manufacturing within the EU, both seem to reserve options for different policy scenarios rather than betting on a single outcome. The former retains ample exit and adjustment space under a non-binding memorandum framework, while the latter partially bypasses the transmission path of UK policy fluctuations by directly entering the EU manufacturing system.

The UK's new Prime Minister is still in the candidate selection process, and the European Commission's trade policies continue to evolve. However, for Chinese automakers making moves in Europe, what matters more than predicting the policy orientation of a specific government may be ensuring that, regardless of how rules are adjusted, they hold alternative paths to move forward. In other words, establishing a localized capability that can navigate political cycles, trade frictions, and regulatory changes. After all, in today's European market, what truly determines long-term competitiveness is never about betting on a single policy shift but having the next plan ready before each change arrives.

Image: Sourced from the Internet

Article: Auto Review

Layout: Auto Review

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!

-

![]()

NVIDIA-Backed AI Unicorn Secures $1.5 Billion Funding: Revenue Soars 2000%

-

![]()

Doubao Pro is Here: How Can Seed 2.1 Be Integrated into Real Processes?

-

"PCB Juice" Sees Four Consecutive Declines: Even Computing Power Material Suppliers Can't Lift This "Old Stock"

-

![]()

Potential 'Seismic Shift' in the U.S. TV Industry: Competition Shifts from Hardware Sales to Traffic Entry Points

-

![]()

Audi A6L's Defense in the Luxury C-Class Market: Following Huawei's Smart Driving Integration, Is Large-Battery HEV the Next Move?