Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

06/25 2026

06/25 2026

433

433

"New Car Sales Peak, Industry Growth Shifts to Backend Vehicle Usage"

On June 23, the automotive industry received its most intensive round of policy combinations this year, with two national-level documents announced in a single day:

First, the Ministry of Commerce website reported that nine departments, including the Ministry of Commerce, jointly issued the "Notice on Several Measures to Foster and Expand Automotive Aftermarket Consumption," proposing 17 measures across six areas: vehicle modification, RV camping industry, automotive racing, car rental, and more.

Second, the "Notice from the General Offices of Eight Departments, Including the Ministry of Commerce, on Conducting Pilot Reforms in Automotive Circulation and Consumption" was released, identifying 40 pilot cities for automotive circulation and consumption reform, along with key reform and innovation directions.

On the same day, the State Council Information Office held a press conference where officials from the Ministry of Commerce, Ministry of Industry and Information Technology, Ministry of Culture and Tourism, Hangzhou, and Chengdu introduced measures to expand automotive consumption across the entire supply chain and interpreted relevant policies.

"The aftermarket formed around vehicle usage represents a trillion-dollar industry," said Sheng Qiuping, Vice Minister of Commerce, noting that the automotive aftermarket has become a new frontier for improving people's livelihoods and expanding consumption.

Statistics show that China's vehicle fleet has reached 370 million units, with auto sales ranking first globally for 17 consecutive years, solidifying its status as a major automotive nation. Over 50% of Chinese passenger vehicles are now over seven years old, indicating that the aftermarket's rapid growth phase has indeed arrived.

Sheng stated that the 17 specific measures aim to remove industry development barriers, solidify the industrial foundation, transform "niche hobbies" into "mass choices," and meet the public's multi-tiered, high-quality consumption demands.

Specifically, policies focus on aftermarket shortcomings such as vehicle modification, racing, RV camping, maintenance, rental, and classic cars, along with pilot reforms in 40 cities for automotive circulation and consumption. They also optimize RV traffic access and promote models like leasing with purchase options.

The dense policy rollout sends a clear signal: the automotive industry's growth focus is shifting comprehensively from frontend vehicle sales to backend vehicle usage.

"Among this round of automotive circulation and consumption reforms, policies upgrading the car rental industry represent the most intuitive and fastest-acting approach, effectively supporting domestic automotive demand in the short term," Lang Xuehong, Deputy Secretary-General of the China Automobile Dealers Association, told Bangning Studio.

She believes this round of automotive circulation reforms, which began early last year, marks a departure from simply "stimulating car purchases" to unblocking the full lifecycle circulation chain from purchase, usage, maintenance, to scrappage, progressively releasing previously restricted and suppressed consumption space.

Some industry insiders hold different views. "All these policies relate to the aftermarket and offer little help to automobile manufacturing or new car sales," said Zhang Yu, General Manager of automotive consultancy Autoforesight, who believes the stimulative effects on the aftermarket will only become visible after many years.

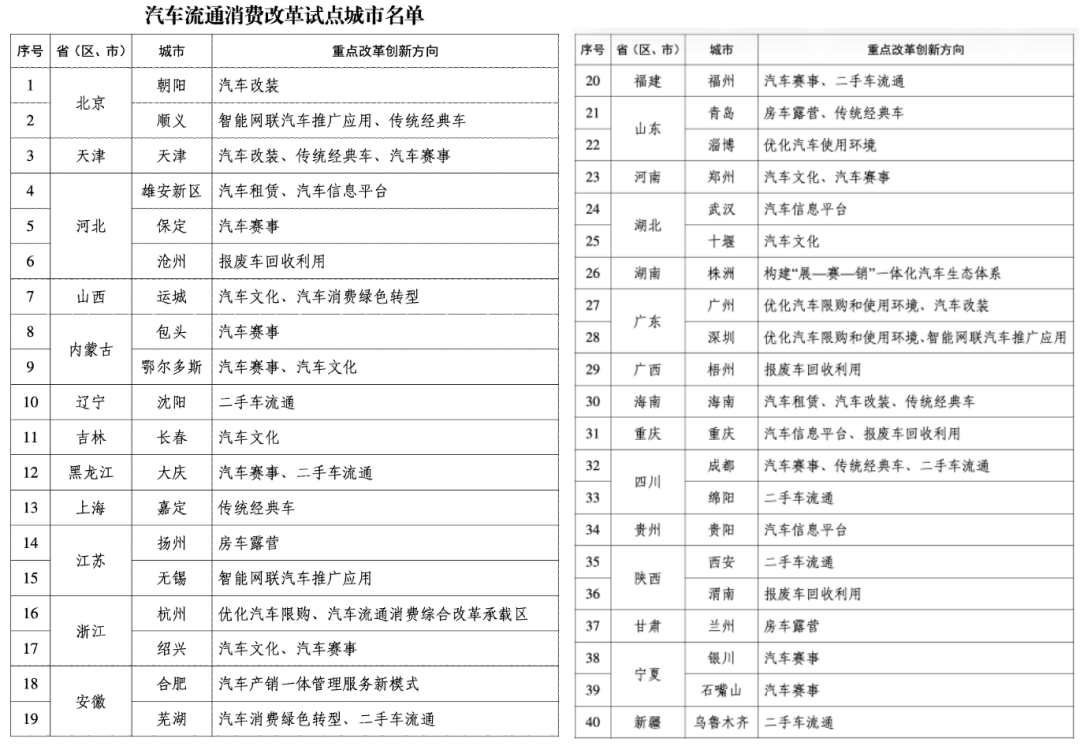

▍01 Pilot Reforms Launch in 40 Cities

First, the scope: 40 cities covering 27 provinces, autonomous regions, and municipalities nationwide, spanning first-, second-, third-, and fourth-tier cities, with third- and fourth-tier cities even forming the majority.

Previously, annual automotive consumption policies varied by city, but this marks the first national-level unified design with city-specific strategies, avoiding one-size-fits-all approaches and allowing each city to develop its own automotive consumption culture.

The policies also address the most sensitive issue: Hangzhou, Guangzhou, and Shenzhen are explicitly tasked with "optimizing car purchase restrictions and usage environments." While Beijing and Shanghai are not on the list, the explorations in these three cities should pave the way for Beijing and Shanghai.

After all, purchase restrictions have dragged on for over a decade, and whoever loosens them first gains the initiative in the next round of automotive consumption competition.

The reform content in the 40 pilot cities follows three main threads:

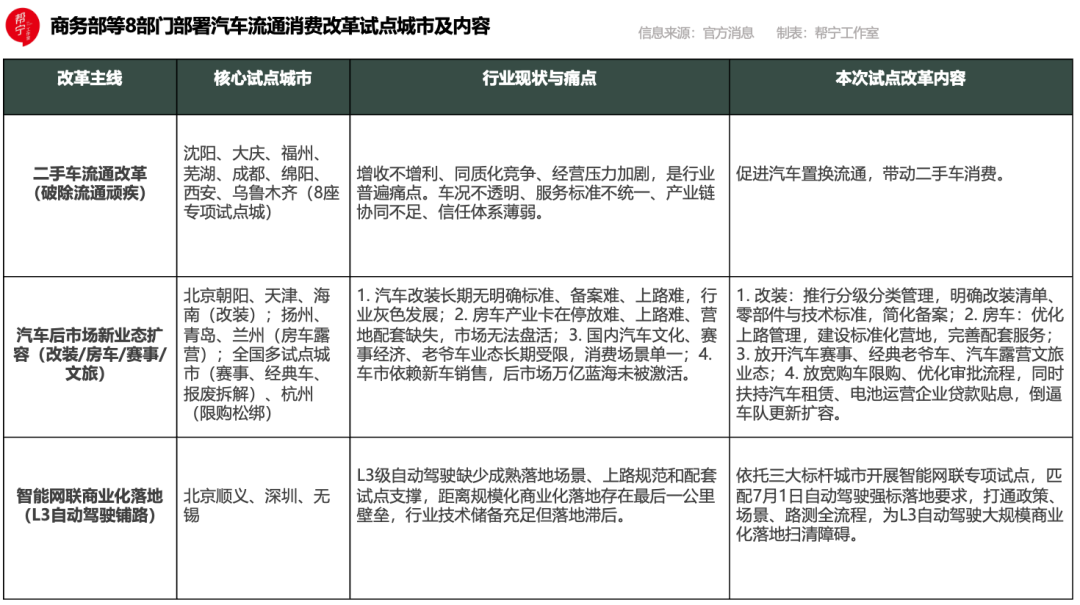

First, eight cities pilot used car reforms to address circulation challenges.

In mature markets, used car transactions account for over 70% of automotive consumption, but China's used car market has long been hindered by restrictions on relocation and cumbersome processes.

This time, eight cities—Shenyang, Daqing, Fuzhou, Wuhu, Chengdu, Mianyang, Xi'an, and Urumqi—focus on used car circulation reforms.

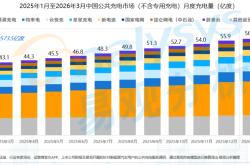

In April 2026, nationwide used car transactions reached 1.6712 million units, down 1.76% year-on-year; from January to April, cumulative transactions hit 6.4932 million units, up 2.93% year-on-year, an increase of 184,600 units compared to the same period last year.

"April 2025 transactions reached 1.7013 million units, a recent high for the same period," said Lu Guangzhi, Deputy Director of the Information Department at the China Automobile Dealers Association. "Despite this high base, April 2026 only saw a slight 1.7% year-on-year decline, with volume essentially flat compared to last year, indicating relatively robust market momentum."

But robust does not equal healthy.

In 2025, nationwide used car transactions exceeded 20 million units, with transaction value nearing 1.3 trillion yuan, entering an era of trillion-dollar stock competition.

Li Ting, Director of the Used Car Business Division at the China Automobile Dealers Association, judges that the used car industry is at a critical inflection point for Conversion of old and new kinetic energy , with transformation being the general trend.

The reality is that traditional profit models relying on vehicle price differentials and offline extensive operations are gradually failing, with common industry pain points including increased revenue without increased profits, homogeneous competition, and mounting operational pressures. Persistent issues like opaque vehicle conditions, inconsistent service standards, inadequate industrial chain coordination, and weak trust systems continue to constrain industry scalability and branding.

The original industrial logic and profit systems no longer fit the new stage. The industry consensus is clear: the core of reconstruction lies in breaking inherent barriers and abandoning outdated models.

Second, modifications, RVs, and racing are finally being taken seriously.

This represents the most project-dense area in the pilots.

For example, Beijing Chaoyang, Tianjin, and all of Hainan Province were selected as vehicle modification pilot regions. Beijing Chaoyang hosts the nation's largest modification market, and this pilot is expected to promote graded and categorized management, define modification project lists, and establish parts and technical standards. If Beijing allows modified vehicles to be easily registered for road use, it will provide a model for nationwide popularization.

Yangzhou, Qingdao, and Lanzhou focus on RV camping. Currently, the RV market's real issues are difficulty in road access, parking, and inadequate campground facilities, preventing the market from taking off. The Ministry of Commerce explicitly states: optimize road access management, build high-standard campgrounds, and improve water, electricity, and catering facilities.

Automotive racing and culture are included in the most pilot projects. In fact, racing, RVs, modifications, and classic cars are all components of automotive culture. Zhang Xue's motorcycle brand and Lynk & Co's consecutive championships in international top-tier events have ignited China's racing culture. Currently still in its infancy, this reform implies more policy liberalization for Chinese automotive culture.

"The new policies provide tangible support, allowing qualified car rental companies and battery operators to enjoy loan interest subsidies," said Lang Xuehong, who believes this represents substantial cost reductions rather than mere incremental benefits for the industry.

With reduced financial pressure, rental companies gain greater confidence to update their fleets, expand capacity, retire old vehicles, and purchase more new cars. As differentiated reforms roll out in 40 pilot cities nationwide, the boundaries of automotive consumption continue to widen.

Cities like Hangzhou have chosen to start by relaxing purchase restrictions, lowering barriers for residents to buy cars. More cities are targeting the vast blue ocean of the automotive aftermarket, liberalizing previously conservative areas. As a result, industries such as vehicle modification, classic car circulation, automotive racing, RV camping culture and tourism, and vehicle scrappage and dismantling are all entering a window for standardized and regularized development.

Third, paving the way for large-scale L3 autonomous driving deployment.

Beijing Shunyi, Shenzhen, and Wuxi have been designated as intelligent connected vehicle application pilots. With autonomous driving standards taking effect on July 1, L3 commercialization is imminent. These three city pilots represent the final stretch before L3 vehicles officially hit the roads.

Bangning Studio learned that the 2026 L3 policy rollout marks a core industry turning point, with the proliferation of high-level intelligent driving models set to drive a 151.8 billion yuan incremental hardware market.

▍02 Formation of a Unified National Market

Behind the dense policy rollouts lies a set of unavoidable, awkward data.

CAAM data shows that in May 2026, domestic passenger vehicle sales reached 1.444 million units, down 23.4% year-on-year. Among them, traditional fuel passenger vehicles sold only 497,000 units, plummeting 41.8% year-on-year.

From January to May, domestic passenger vehicle sales totaled 6.791 million units, down 23.8% year-on-year. Traditional fuel vehicle sales during this period reached 3.203 million units, a year-on-year decrease of 1.243 million units, or 28%.

Profit margins are also under pressure. From January to May, the automotive industry's total profit was approximately 178.1 billion yuan, down 11.9% year-on-year, with an industry profit margin of only about 4.3%, below the average for industrial enterprises.

Stimulating automotive consumption has thus become a policy priority.

Over the past few years, authorities have introduced multiple rounds of stimulative policies, including purchase tax exemptions, cars-to-the-countryside programs, trade-in subsidies, and energy-efficient vehicle subsidies, which temporarily boosted sales growth. However, as the market approaches saturation, the marginal effect of terminal cash subsidies is rapidly declining.

This time, the policy direction has fundamentally shifted—from the frontend market to the entire supply chain.

Whether through the 17 measures to activate the automotive aftermarket or the 40-city pilot reforms for automotive circulation and consumption, these are not simple stimulative measures but represent a systemic reconstruction of market institutions.

First, unified deployment coexists with pilot initiatives.

At the national level, the first step was to create a checklist of aftermarket areas long neglected or poorly managed, such as vehicle modification, automotive racing, RV camping, vehicle maintenance, car rental, and traditional classic cars, which have long suffered from inadequate regulatory systems, incomplete standard frameworks, and insufficient quality supply.

However, the new policies avoid a one-size-fits-all approach. The 40 pilot cities were selected through a " issue a public challenge for the best solution " (open competition) process, with each city exploring solutions tailored to its own shortcomings. This means a unified national market with unified directions but decentralized trial-and-error approaches.

Second, equal emphasis on revitalizing existing resources and optimizing new growth.

For existing resources, policies explicitly support the creation of new consumption scenarios leveraging existing facilities such as Vehicle companies (vehicle manufacturers), automotive markets, racetracks, and cultural and creative parks. Cities like Shanghai and Tianjin are already utilizing international racetrack resources to host events, linking commerce, tourism, culture, sports, and health to promote consumption.

More attention is warranted for new growth. Pilot cities like Guangzhou, Shenzhen, and Hangzhou are exploring optimized car purchase restriction measures to release pent-up demand. The Xiong'an New Area has taken a unique path by supporting relocated enterprises in bulk vehicle purchases, which are then leased to employees to meet commuting needs in the Beijing-Tianjin-Hebei region. These approaches essentially bypass purchase restriction barriers through institutional innovation.

Free trade zones and comprehensive bonded zones are also part of the strategy. New business formats such as bonded vehicle modifications, classic car "bonded storage + exhibition," and car rental are being piloted, aiming to grow distinctive industries rather than simply selling cars.

Finally, balancing effective regulation with flexible liberalization.

This represents the core logical shift of the entire policy suite—moving from purchase management to usage management.

"Effective regulation" means the state will implement graded and categorized management for vehicle modifications, not imposing outright bans but drawing red lines to guide standardized development, balancing development and safety, and providing the industry with a predictable institutional framework.

"Flexible liberalization" means the Ministry of Commerce will work with relevant departments to accelerate the relaxation of restrictions in areas such as used car transactions, RV camping, and pickup truck city access. Pilot cities are granted greater autonomy, such as streamlining land use approval processes for RV campgrounds to reduce corporate administrative costs.

Now that new car sales have peaked, the aftermarket has become the automotive industry's new trillion-dollar arena. To activate this market, subsidies alone are no longer sufficient; institutional reforms are needed—unifying rules to reduce transaction costs, lifting restrictions to release demand space, and using pilot mechanisms to encourage local innovation.

-

Hao Jida, Apple Supply Chain Coil Supplier, Switches Brokerage and Revives IPO Amidst Customer Dependency and Compliance Challenges

-

![]()

Annual Advertising Expenditure of VOYAH with Yudeshui: A Deep Dive

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket