China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

06/25 2026

06/25 2026

420

420

Analysys Insight: As the penetration and ownership of new energy vehicles (NEVs) continue to surge, China’s public charging market has transitioned into a new phase focused on “quality and efficiency enhancement.” Previously, the emphasis on rapid scale expansion over service quality led to issues such as “zombie charging piles” (underutilized or non-functional chargers) and “inefficient charging piles,” which impacted both corporate profitability and user experience. Today, operators’ competitiveness is increasingly determined by efficiency metrics, including actual charging volume, fast-charging availability, and the average number of vehicles charged per gun daily, rather than sheer scale.

Against the backdrop of the rising penetration and ownership of NEVs in China, the public charging consumer market has officially entered a phase of steady, high-quality development centered on “quality and efficiency enhancement.” Historically, industry evaluation standards prioritized “scale” over “service,” fostering a model of extensive development that blindly expanded the number of connected charging piles. This approach resulted in a proliferation of “zombie charging piles” and “inefficient charging piles.” Such a scale-centric evaluation system not only misguided corporate strategies and generated profitability pressures but also left users with a subpar charging experience, marked by frequent equipment failures and slow charging speeds.

Today, this model is undergoing a profound transformation. The core competitiveness and true market standing of charging operators are now assessed based on three key dimensions: actual charging volume, the proportion of fast-charging guns, and the average number of vehicles charged per gun daily (charging efficiency), rather than simply the “number of connected charging piles.” The latest research data released by Analysys sheds light on the current competitive landscape in China’s public charging market during this transformative period.

I. Charging Volume Landscape: Steady Growth with Didi Charging Leading at Over 34% Share

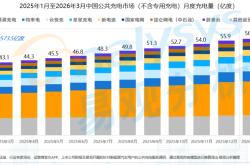

Charging volume is the most direct indicator of a charging network’s actual utilization and user loyalty. Data shows that by 2025, the cumulative charging volume in China’s public charging market (excluding dedicated charging for specific fleets) had surpassed 57 billion kWh, reaching approximately 57.35 billion kWh. Monthly trends indicate that, apart from a brief decline in February due to the Spring Festival holiday and seasonal factors (from 4.15 billion kWh in January to 4.00 billion kWh), the market maintained a steady month-on-month increase throughout the year, peaking at 5.59 billion kWh in December 2025. This growth momentum persisted into 2026, with monthly charging volumes reaching 5.69 billion kWh, 5.46 billion kWh, and 5.54 billion kWh in January, February, and March 2026, respectively.

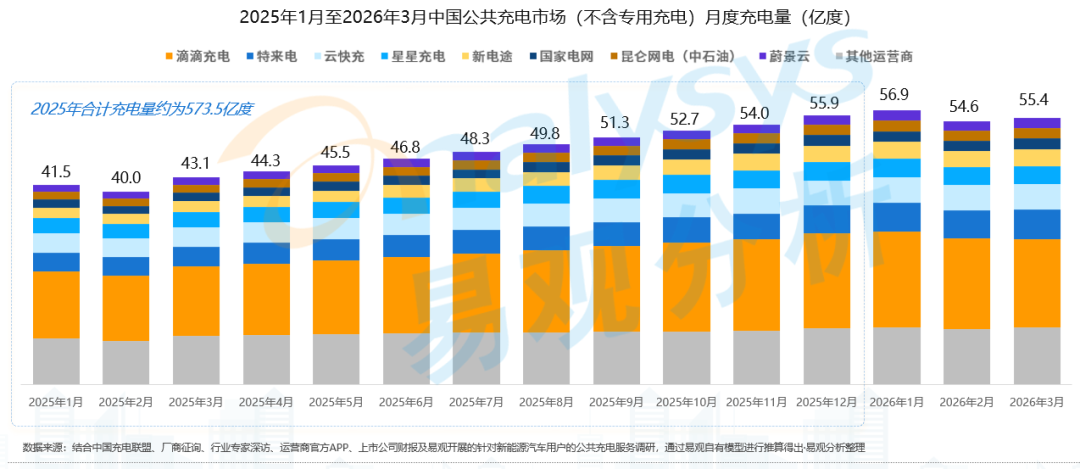

Within this expansive charging volume landscape, market share is consolidating among the leading players. As of March 2026, Didi Charging, leveraging its powerful platform aggregation capabilities and a large base of high-frequency users such as ride-hailing drivers, has secured a 34.22% market share, establishing an absolute leading position in the public charging market (excluding dedicated charging). It is closely followed by Teld (10.06%), Yunkuai (9.54%), and Xingxing Charging (8.42%), which form the second tier of the market. The remaining shares are distributed among Xindiantu (5.77%), State Grid (3.76%), Kunlun Net Power (PetroChina, 3.66%), Weijing Cloud (3.58%), and other operators (20.99%).

II. Fast-Charging Gun Ratio: Over 70% of Vehicle Owners Prefer Fast Charging, High-Power Energy Replenishment Becomes the Norm

The configuration ratio of fast-charging guns has become a critical indicator of an operator’s hardware competitiveness. With advancements in battery technology and the normalization of range anxiety among vehicle owners, rapid energy replenishment has become a rigid demand for users. Surveys indicate that over 70% of NEV owners prioritize fast-charging guns when charging, reflecting the normalization of demand for high-power, high-voltage fast charging. For public charging service operators, increasing the proportion of fast-charging guns is not only essential for meeting users’ core energy replenishment needs but also a vital strategy to adapt to vehicle model upgrades, enhance site operational efficiency and user satisfaction, and align with industry upgrade trends.

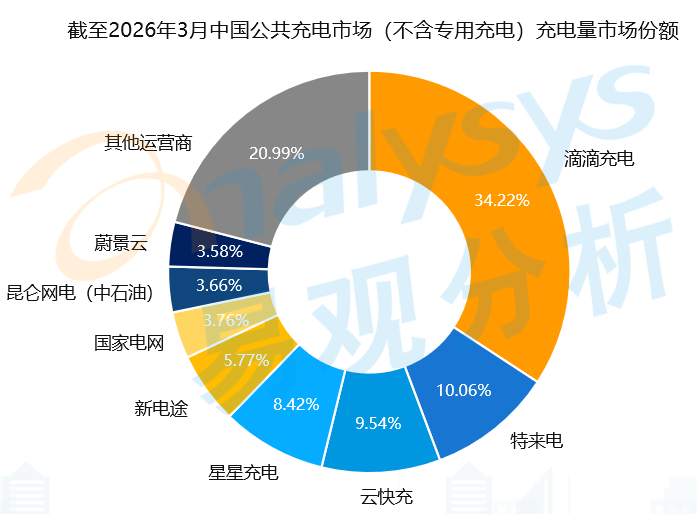

After excluding pile enterprise and OEM operators and screening operators with over 10,000 charging guns, as of March 2026, in the ranking of fast-charging gun ratios among China’s public charging service operators, Didi Charging tops the list with a 92.3% fast-charging gun ratio, showcasing its asset allocation strategy highly focused on fast-charging energy replenishment scenarios. Haihuide follows closely with an 89.8% fast-charging gun ratio, ranking second. Kaimaisi ranks third with an 85.5% ratio. Additionally, operators in the TOP 10 list include Xindiantu (81.6%), Kunlun Net Power (75.0%), Hengtong Renwochong (62.4%), Teld (59.9%), Kaixin Charging (57.4%), Yunkuai (52.6%), and Wanma Aichong (47.0%).

III. Charging Efficiency: Significant Variation in Average Daily Efficiency per Gun, Refined Operations Become Key to Breakthroughs

If charging volume and fast-charging ratio represent “scale and hardware,” then the “average number of vehicles charged per public charging gun daily” serves as a litmus test for measuring an operator’s “refined operations and profitability.” As a core indicator of the actual usage intensity of charging piles, this metric directly determines whether the revenue from a single pile can cover fixed costs such as depreciation, electricity fees, and operation and maintenance. It also accurately reflects user demand differences across regions, scenarios, and time periods, helping operators avoid blind expansion.

Among the leading operators with over 100,000 public charging guns nationwide, there is significant variation in the efficiency of the average number of vehicles charged per gun daily. Data as of March 2026 shows that Didi Charging leads the pack with an average of 7.7 vehicles charged per gun daily, far exceeding the industry average in operational efficiency. Teld and Yunkuai tie for second place with an average of 3.0 vehicles charged per gun daily. Xingxing Charging ranks fourth with an average of 2.9 vehicles charged per gun daily. Xindiantu ranks fifth with an average of 2.1 vehicles charged per gun daily.

China’s public charging service market has bid farewell to extensive scale expansion and entered a high-quality development phase focused on “quality and efficiency enhancement.” For operators, precisely shutting down inefficient charging piles and densifying high-demand areas to transition from “quantity-focused” to “efficiency-focused” operations has become an inevitable choice to remain competitive.

Research Notes

The industry analysis provided by Analysys is primarily based on industry macro data, quarterly surveys of end-users, historical vendor data, and quarterly business monitoring information of vendors. It employs Analysys’s industry analysis model, combined with market research, industry research, and vendor research methods, to reflect market status, trends, turning points, and patterns, as well as the development status of vendors.

Analysys believes that the data derived from the aforementioned industry research methods is within an industry-recognized acceptable error range and can accurately reflect industry trends and changes.

The research results obtained through professional research methods are intended for decision-making reference. For actual vendor data, please refer to the financial reports published by the vendors.

Copyright Notice

The third-party data and other information cited by Analysys in this article are sourced from public channels, and Analysys assumes no responsibility for them. Under no circumstances shall this article be used as a basis and shall only serve as a reference. The copyright of this article belongs to the publisher. Without authorization from Analysys, any reproduction, quotation, or use in any form of any content published by Analysys is strictly prohibited. Any authorized media, website, or individual must quote the original text in full and indicate the source when using it. The analysis and viewpoints shall be based on the official content released by Analysys, and no deletion, addition, splicing, interpretation, or distortion in any form shall be allowed. For disputes arising from improper use, Analysys assumes no responsibility and reserves the right to hold the relevant responsible parties accountable.

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’

-

Hao Jida, Apple Supply Chain Coil Supplier, Switches Brokerage and Revives IPO Amidst Customer Dependency and Compliance Challenges

-

![]()

Annual Advertising Expenditure of VOYAH with Yudeshui: A Deep Dive

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead