Approaching its Secondary Listing in Hong Kong with a Market Cap Exceeding 500 Billion: How Has Luxshare Precision Regained Investor Trust?

06/30 2026

06/30 2026

426

426

Introduction: On one hand, the robust performance of its core business, and on the other, the vast potential of its optical module business, have propelled Luxshare Precision's valuation to surpass the 500 billion yuan mark.

Author: Li Ping | Produced by: Lishang Business Review

1. Countdown to Hong Kong Listing

Following in the footsteps of Lens Technology, another major 'Apple supply chain' player is set to list on the HKEX.

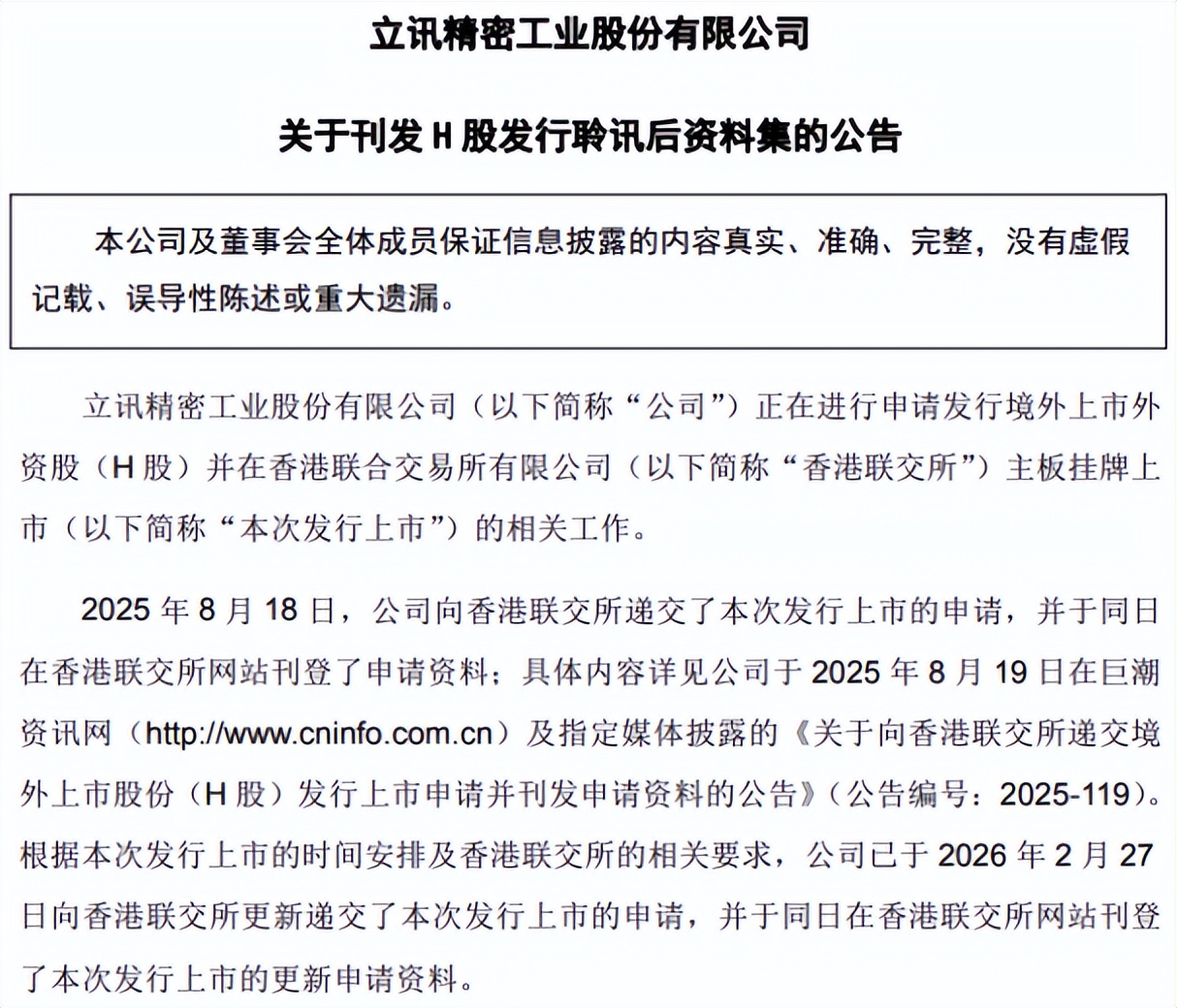

On June 23, the HKEX website revealed that Luxshare Precision, a consumer electronics manufacturing giant, had passed its listing hearing and updated its prospectus, marking the final stage of its Hong Kong IPO process.

Public information shows that as early as July 2025, Luxshare Precision's board of directors approved a resolution regarding its overseas listing, subsequently advancing all preparatory work for the Hong Kong listing. On August 18 of the same year, the company formally submitted its H-share application materials to the Hong Kong Stock Exchange and updated its application on February 27, 2026.

According to Frost & Sullivan, by revenue in 2025, Luxshare Precision ranked fifth globally and first in mainland China in the PIMS (Precision Intelligent Manufacturing Solutions) industry, holding leading positions in consumer electronics, automotive electronics, communications, and data centers. Specifically, the company ranked second globally and first in mainland China in the consumer electronics components and modules PIMS market, with a global market share of 11.2%.

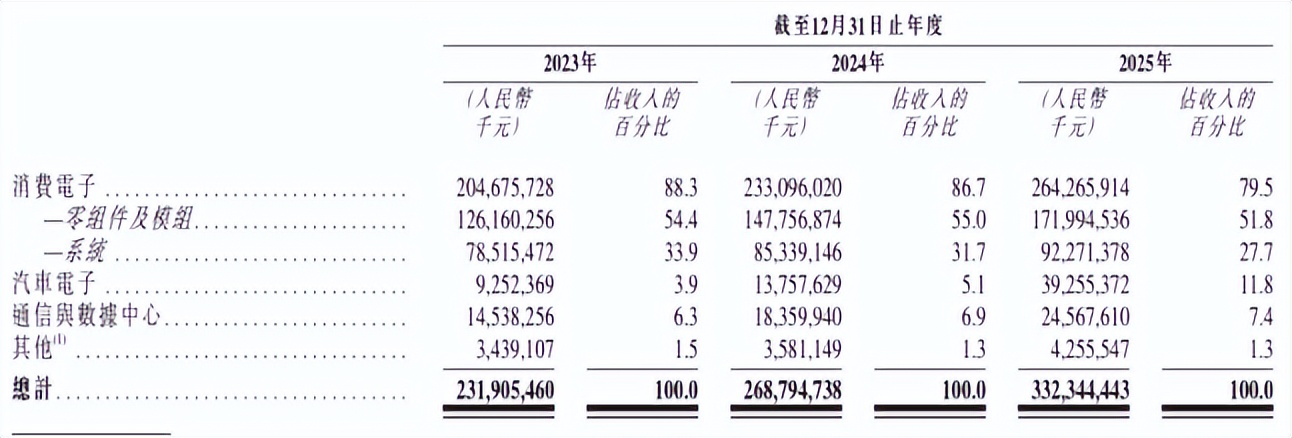

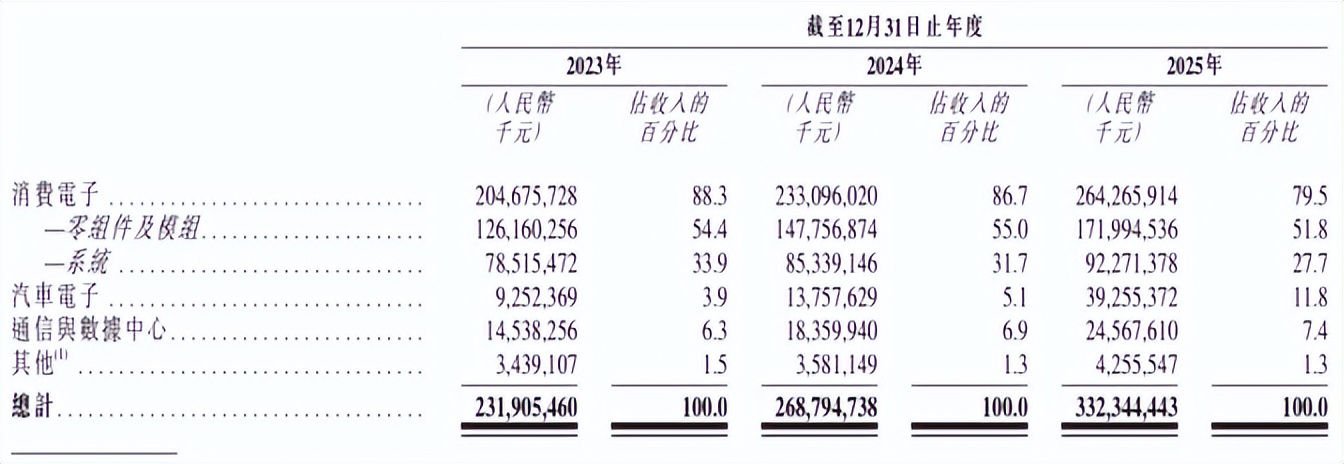

Financial data shows that in 2025, Luxshare Precision achieved total revenue of 332.344 billion yuan, up 23.64% year-on-year, with net profit attributable to shareholders reaching 16.6 billion yuan, up 24.2% year-on-year. By business segment, its traditional consumer electronics business generated 264.266 billion yuan in revenue, up 13.37% year-on-year, accounting for 79.52% of total revenue. Automotive electronics, communications, and data center businesses recorded revenues of 39.255 billion yuan and 24.568 billion yuan, up 185.34% and 33.81% year-on-year, respectively. Together, these segments accounted for over 20% of total revenue for the first time, signaling Luxshare Precision's preliminary formation of a 'consumer electronics + automotive electronics + data centers' triple-driven model.

Similar to its strategy within the Apple supply chain, Luxshare Precision has adopted an external acquisition approach to expand into automotive electronics and data center businesses, leading to a continuous rise in its debt levels. By the end of 2025, Luxshare Precision's total liabilities exceeded 200 billion yuan, up over 60 billion yuan from the previous year, with interest-bearing liabilities surpassing 100 billion yuan, both reaching all-time highs.

According to the latest report by IFR, a Reuters-affiliated media outlet, Luxshare Precision plans to raise $2-3 billion and aims to list in Hong Kong as early as July. The prospectus discloses that the company plans to sell approximately 441 million ordinary shares in its H-share offering. After deducting issuance expenses, the proceeds will be used for: capacity expansion and upgrading existing production bases, particularly focusing on global capacity expansion in automotive electronics and consumer electronics; investing in R&D to improve manufacturing processes and enhance smart manufacturing capabilities; investing in high-quality target companies in upstream and downstream industries or related sectors; repaying some existing interest-bearing bank loans; and supplementing working capital and general corporate purposes.

Notably, on the same day Luxshare Precision passed its HKEX listing hearing, Goldman Sachs publicly upgraded its outlook on the company's stock in a research report, sharply raising its 12-month target price for Luxshare Precision from 50.15 yuan to 106 yuan per share, implying a potential upside of 52.8%. Analysts including Verena Jeng stated in the report that Luxshare Precision's revenue is expected to achieve a compound annual growth rate (CAGR) of 22% from 2025 to 2028, reflecting expectations for robust growth in its data center business, automotive electronics, and expansion with overseas OEM clients.

On June 24, the day after Luxshare Precision updated its prospectus post-hearing, its stock price rebounded swiftly after hitting a low in the morning session, surging in the afternoon and touching the daily limit before opening slightly, closing up 8.2% for the day with a total market cap exceeding 550 billion yuan. Clearly, secondary market investors have already voted in favor of Luxshare Precision's Hong Kong listing.

2. Progress in 'De-Appleization'

In the A-share market, Luxshare Precision has long been known as the 'leader of the Apple supply chain.'

Public information shows that Luxshare Precision, founded in 2004, initially engaged in computer cable manufacturing. Its founder, Wang Laichun, was among the first 150 employees hired by Foxconn's Shenzhen factory in 1998. In 2010, Luxshare Precision successfully listed on the Shenzhen Stock Exchange, raising 1.261 billion yuan. After its listing, the company acquired stakes in Apple supply chain companies such as Kunshan Liantao Electronics, successfully entering Apple's supply chain. Through continuous expansion from single components to modules and eventually to full system assembly, Luxshare Precision gradually became a key supplier in Apple's ecosystem.

As the primary contract manufacturer for Apple AirPods, Luxshare Precision holds over 70% of the AirPods assembly market share, handling full-process production including acoustic module assembly and final testing. Meanwhile, it is the second-largest contract manufacturer for iPhones, with a market share of approximately 15-20%. Additionally, Luxshare Precision provides precision structural components for the Apple Watch Series 10 and serves as the exclusive assembler for Apple's first head-mounted display, Vision Pro, responsible for critical processes such as optical modules and sensor integration.

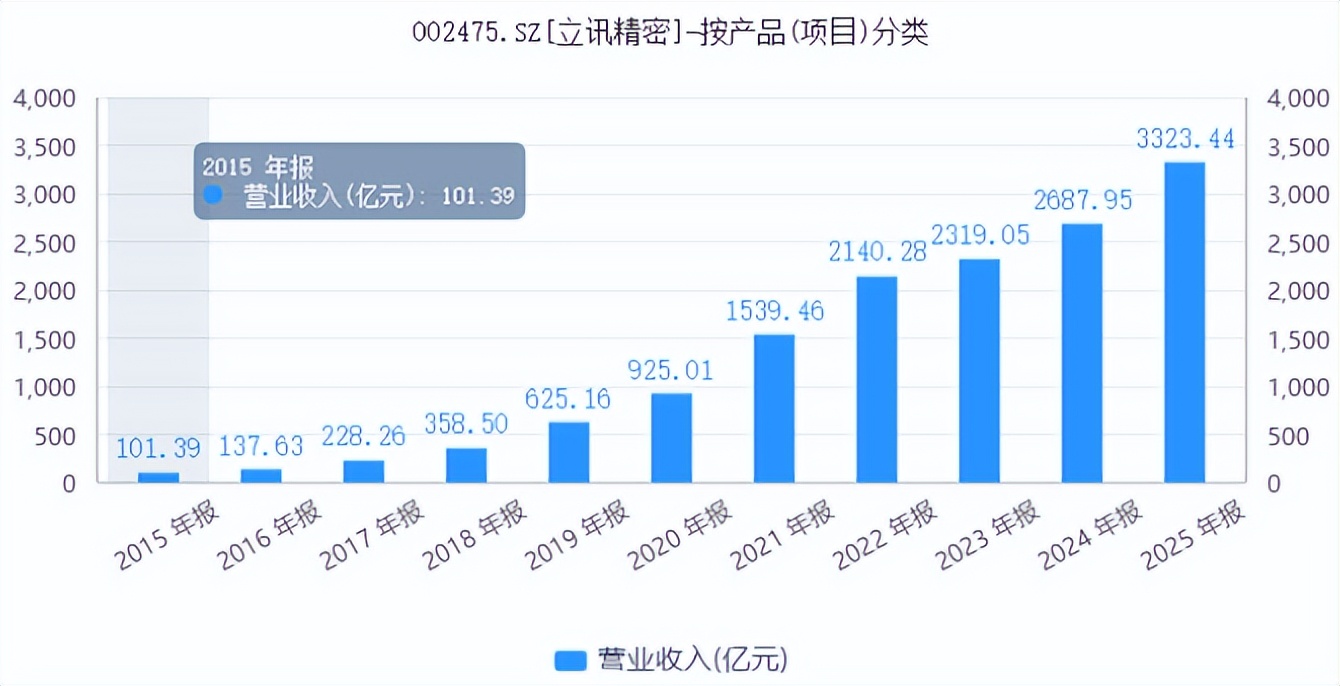

With a steady influx of Apple orders, Luxshare Precision achieved robust growth in its operating performance. Data shows that from 2015 to 2024, its revenue surged from 10.1 billion yuan to 268.8 billion yuan, a more than 25-fold increase over a decade. Within this, its largest business segment, consumer electronics, grew from 4.4 billion yuan to 233.1 billion yuan in revenue, a more than 50-fold increase over ten years.

However, while Luxshare Precision achieved rapid development through its partnership with Apple, it inevitably developed a severe 'major client dependency.' Data shows that from 2021 to 2024, revenue from Apple accounted for over 70% of Luxshare Precision's total revenue for four consecutive years, earning it the label of an 'Apple contract manufacturer' among investors.

Against the backdrop of ongoing U.S.-China trade tensions, Luxshare Precision, branded as part of the 'Apple supply chain,' has not been favored by A-share investors, with its valuation under continuous pressure. In April 2025, escalating U.S.-China trade tensions significantly impacted the consumer electronics sector, causing stock prices of 'Apple supply chain' companies, led by Luxshare Precision, to plummet. Data shows that from April 2 to April 9, 2025, Luxshare Precision's stock price fell nearly 30% in five trading days, at one point dropping below a market cap of 200 billion yuan.

On the other hand, due to the low gross margins of businesses like iPhone assembly, Luxshare Precision's overall profitability has declined noticeably in recent years. From 2020 to 2024, its gross profit margin fell from 18.09% to 10.41%, showing a clear year-by-year decline. Clearly, the narrowing profit margins in its core business have also been a significant factor weighing on Luxshare Precision's stock price.

In recent years, to reduce its over-reliance on Apple, Luxshare Precision has continuously expanded into emerging businesses such as automotive electronics, communications, and data centers, aiming to open up a second growth curve. In the automotive sector, Luxshare Precision focuses on core electronic energy transmission and signal interaction in vehicles, with products covering high- and low-voltage wire harnesses, high-speed wire harnesses, and high-speed connectors, extending to intelligent cockpits, ADAS domain controllers, AR-HUDs, and multi-in-one powertrains. Additionally, Luxshare Precision has established a joint venture with Chery Automobile, setting a goal to become a top-10 global Tier 1 supplier.

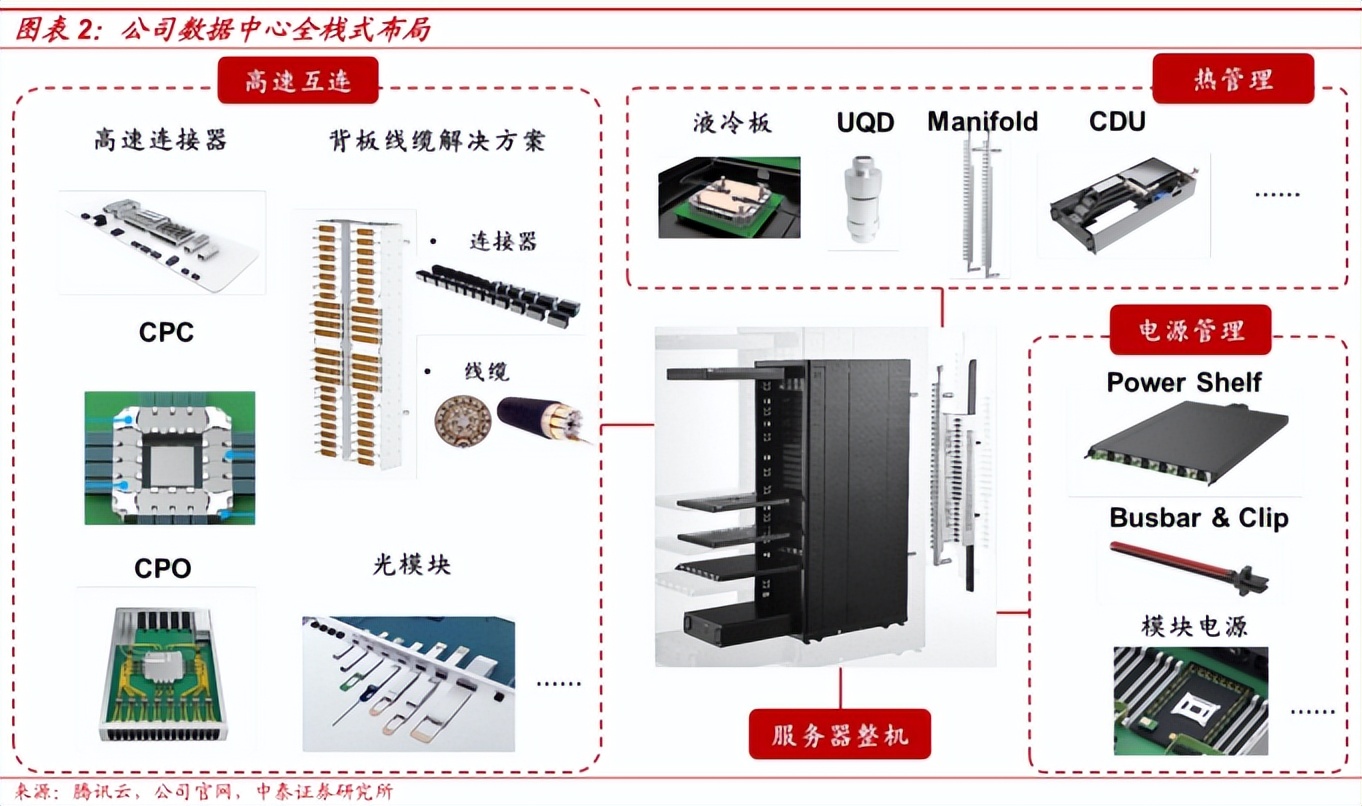

In the communications and data center sectors, Luxshare Precision has built an integrated solution based on 'three core systems (high-speed optoelectrical interconnects, power management, thermal management)' and 'two key dimensions (board-level interconnects, rack-level interconnects).' In communications networks, it focuses on core network equipment such as base station antennas and RF units; in data centers, it concentrates on core modules like high-speed copper/optical interconnects, thermal management, and power management, providing end-to-end solutions for AI computing clusters.

Previous annual report data shows that in 2025, Luxshare Precision achieved total revenue of 332.344 billion yuan, up 23.64% year-on-year. By business segment, automotive electronics, communications, and data center businesses recorded revenues of 39.255 billion yuan and 24.568 billion yuan, accounting for 11.81% and 7.39% of total revenue, respectively, with the consumer electronics business's share dropping below 80% for the first time. Additionally, revenue from Apple, its largest client, fell to 57% of total revenue, indicating initial success in its 'de-Appleization' strategy.

3. Optical Modules Drive Valuation Reshaping

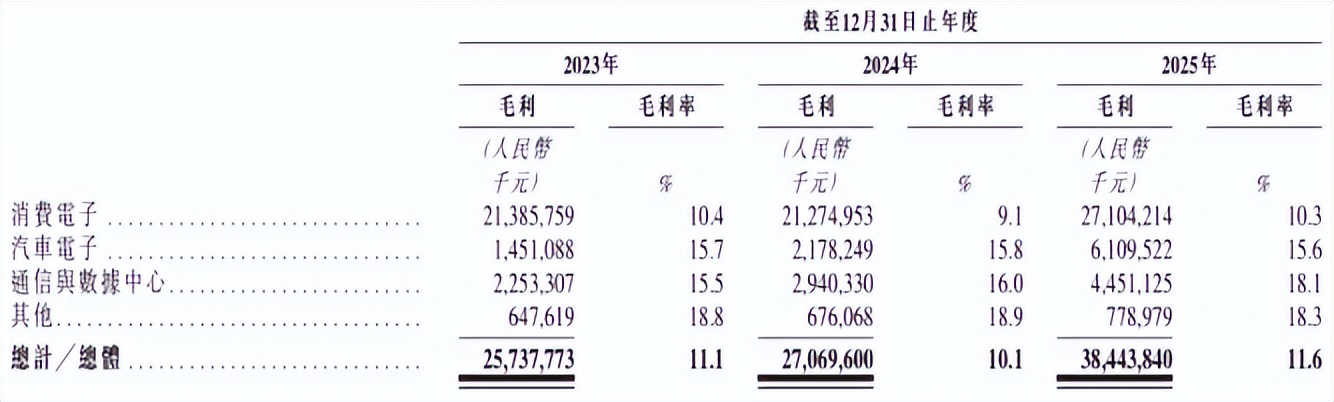

While promoting revenue diversification, Luxshare Precision's expansion into emerging businesses such as automotive electronics has also somewhat improved its overall gross profit margin. According to its Hong Kong prospectus, in 2025, the gross profit margins for its communications and data center, and automotive electronics segments were 18.1% and 15.6%, respectively, significantly higher than the 10.3% margin in its consumer electronics business during the same period.

Benefiting from the increased share of high-margin businesses, Luxshare Precision's overall gross profit margin reached 11.6% in 2025, up 1.5 percentage points year-on-year, initially reversing the multi-year downward trend in its margins.

In terms of revenue contribution, Luxshare Precision's automotive electronics business has surpassed 10% of total revenue and is viewed by many investors as its second growth engine. However, compared to automotive electronics, its communications and data center business boasts higher gross margins. Especially against the backdrop of strong global demand for AI computing power, the data center business, centered on optical modules, copper interconnects, and optical interconnects, has become Luxshare Precision's most promising future segment.

As early as 2020, Luxshare Precision began developing optical modules, achieving mass production of 400G optical modules in 2023 and launching 800G optical modules. To date, its 800G optical modules have entered mass production and shipment. Notably, Luxshare Precision's 800G optical modules have passed compatibility tests with switches from major overseas brands such as Nvidia, Arista, and Juniper, and demonstrated leading bit error rate performance compared to competitors in head-to-head evaluations for 800G solutions by top clients.

In April 2025, Luxshare Technology showcased a 1.6T optical module and copper interconnect full-link solution at OFC 2025, taking the lead in commercializing 1.6T optical modules, which are currently undergoing client validation. In terms of cutting-edge technology development, Luxshare Precision continues to advance R&D in frontier optical interconnect technologies such as LPO/CPO and has preemptively layout (pre-emptively layout ) 5nm-related product development.

While focusing on next-generation AI optical interconnect technologies, Luxshare Precision has also achieved breakthroughs in thermal management, power management, and other areas. In thermal management, its self-developed microchannel thermal management products successfully entered mass production in 2025; in power management, its 800-volt system products have been deployed in core client projects and achieved commercial applications.

Some analysts believe that with the large-scale construction of data centers worldwide, Luxshare Precision's data center business volume may see substantial growth in 2026-2027. In response, Goldman Sachs stated in a recent research report that due to Luxshare Precision's commercialization of layouts in high-speed copper interconnects, optical modules, and thermal management, its telecommunications and data center business is expected to achieve a CAGR of 67%, with sales revenue from this segment accounting for 19% of total revenue by 2028.

However, compared to leading companies like Zhongji Innolight and Eoptolink, Luxshare Precision's optical module business still lags significantly in terms of revenue scale and profitability. In 2025, Luxshare Precision did not disclose specific revenue figures for its optical module business. However, the company stated on an interactive platform that optical modules account for a very small portion of its communications and data center segment, with revenue contributing approximately 0.1% in 2025. Luxshare Precision also emphasized that its cooperation with North American CSP (Cloud Service Provider) head clients (top clients) in the optical module business is still in the early stages of engagement, and previous market reports claiming 'Luxshare Precision secured 10 million optical module orders from North American clients' were false.

Additionally, from a supply chain perspective, Luxshare Precision's optical module business mainly focuses on supporting manufacturing and system integration, while upstream core technologies such as optical chips and high-speed signal processing remain in the hands of professional optical module manufacturers and upstream chip companies. In comparison, Zhongji Innolight has successfully developed key components such as high-precision lasers and microlens arrays, leading to a significant gap in profitability between the two. Data shows that in 2025, Zhongji Innolight's optical module business achieved a gross profit margin of 42.61%, while Luxshare Precision's overall gross profit margin in communications and data centers was only 18.4%.

Overall, Luxshare Precision's optical module business is still in its early stages in terms of revenue scale, core technologies, and business models, and has not yet fully emerged. However, this very 'ambiguity' has become the strongest catalyst for Luxshare Precision's valuation surge, fueling bullish sentiment in the capital markets. Meanwhile, Luxshare Precision is actively seizing the current 'expectation premium' window in the capital markets to accelerate its Hong Kong listing process, aiming to transform this 'ambiguity' into a capital engine supporting its globalization strategy.

-

![]()

5G Standalone Private Network Policy Breaks the Ice, Creating an Exclusive 'Nervous System' for Physical AI in Industrial Scenarios

-

![]()

Two Investments Totaling 700 Million Yuan! Sunny Optical Sets Its Sights Beyond Lens Supply, Launching a Strategic Move in the XR Optics Arena

-

![]()

Xianyu Initiates Internal Testing of 'Yu Maimai' and 'Yu Maimai': Can AI Revolutionize Secondhand Transactions?

-

![]()

The Dullest 618 in History, with AI Being the Busiest

-

![]()

Shenzhen’s Most Mysterious Robot Startup Secures 1 Billion Yuan in Funding, Targeting a 150 Billion Yuan Market

-

![]()

Why Are Celebrities So Keen on Diving into the AI Realm?

-

Can WeChat AI Sidestep the Quandary Faced by Doubao Phone?

-

![]()

Luxury Lineup, Highly Anticipated! The Pioneer of Physical AI Gears Up for Hong Kong Stock Exchange Debut!