Chinese Cars: Germany's 'Praise' Amidst US Fears

07/01 2026

07/01 2026

334

334

Lead-in

Introduction

The global automotive market is experiencing a significant transformation in its entry criteria.

The German government is in a state of panic, desperately seeking assistance from Chinese automakers. Recently, Volkswagen was reported to be contemplating drastic cost-cutting measures and layoffs, potentially affecting up to 100,000 employees and leading to the closure of four factories in Germany.

As the situation unfolded, the German Metalworkers' Union and Volkswagen's General Works Council issued a joint statement vehemently opposing the plan, vowing to "exhaust all means to halt it" if implemented.

In response, a German government spokesperson also commented, stating that the government aims to prevent domestic factory closures. To maintain normal factory operations, several government officials have suggested collaborating with Chinese automotive companies.

Stephan Weil, the Prime Minister of Lower Saxony, Germany, proposed that Volkswagen could manufacture models co-developed with Chinese partners like Xpeng and SAIC in its German factories, thereby augmenting capacity and enhancing utilization rates for German automakers' facilities instead of relocating production elsewhere.

Tilo Pant, Saxony's Economics Minister, recommended introducing Chinese automakers to establish production at Volkswagen's Zwickau factory, stating, "We must keep pace with the times. China represents an opportunity for Zwickau."

History has repeatedly demonstrated that "taking over" often entails inheriting underlying issues. The German invitation is not merely an "enhanced willingness to cooperate"; a more pressing concern is that the German automotive industry is transitioning from an "era of expansion" to an "era of overcapacity."

When factories cease to operate at full capacity, the issue transcends market competition and becomes a matter of workers' livelihoods. Chinese automakers taking over will no longer be mere vehicle exporters but will become "capacity supplement providers" in Germany.

Meanwhile, across the Atlantic, the US automotive market has witnessed a different development. The US Department of Commerce, citing the "Connected Vehicle Principles," denied Polestar's application for a business permit to operate in the United States, meaning the 2027 Polestar model will not be available for sale in the US.

Yes, we are referring to Polestar, the Nordic-style brand controlled by Geely, which has exited the Chinese market and achieved localized production in the United States.

The so-called "Connected Vehicle Principles" were formally implemented during the Biden administration, prohibiting connected vehicles containing Chinese or Russian software or hardware from entering the US market. Surprisingly, Volvo, also controlled by Geely like Polestar, has secured corresponding "exemptions."

The closed nature and uncertainty of the US automotive market are evident.

At this juncture, whether a vehicle can enter the US market hinges not on whether it is electric or gasoline-powered, nor on its affordability or performance leadership, but on whether it meets US requirements, such as so-called data and software security.

Amid significant upheaval in the global automotive market, these two events occurred almost simultaneously—one seemingly "opening the door" while the other "tightens the borders." These are the challenges Chinese automakers face when expanding overseas.

However, the crux may not lie in which market is more open but rather in the fact that the global automotive market is undergoing a redefinition of entry rules.

01 'Prying Open' a Crack in the European Market

Firstly, it must be acknowledged that Chinese automakers cannot overlook the European market when expanding overseas. Europe, home to Germany, is the world's third-largest automotive regional market, trailing only China and the United States—a substantial market share.

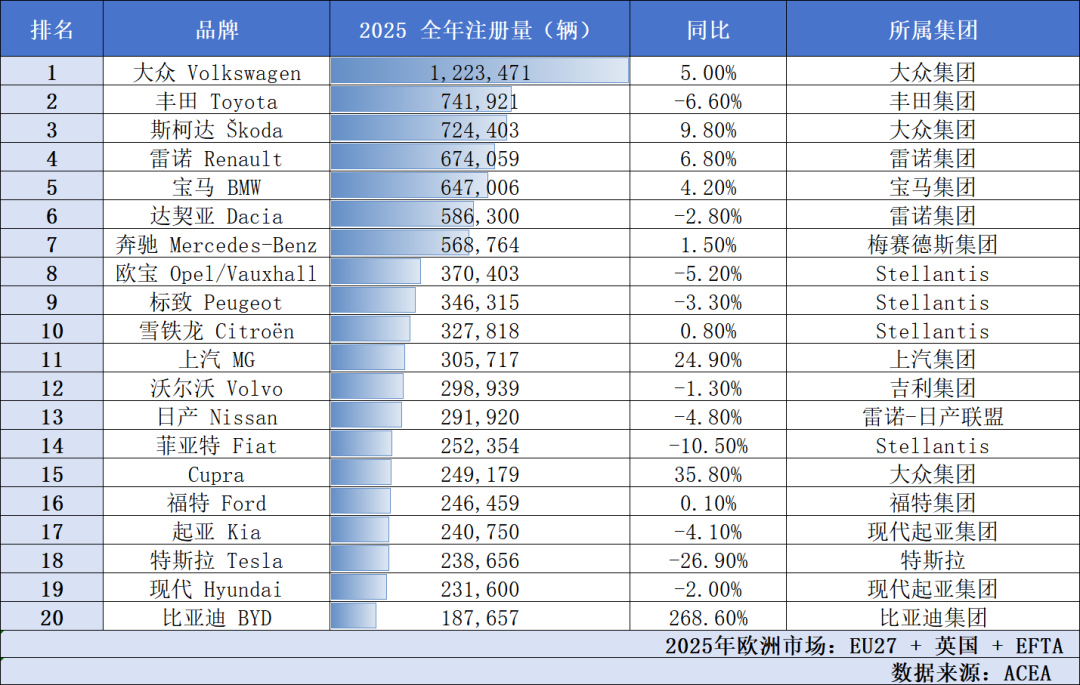

According to official data from the European Automobile Manufacturers' Association (ACEA) for the full year of 2025, total sales in the EU-27 + UK + EFTA markets reached 13.271 million units, with new energy vehicles (BEV + PHEV) accounting for 3.8582 million units, representing a 29.1% market share.

Among the top 10 automotive brands by sales in 2025, the European market remains dominated by local European automakers, with Volkswagen firmly at the top, followed by Toyota, Skoda, Renault, BMW, and Mercedes-Benz.

SAIC MG sold 305,700 vehicles in the European market for the full year, up 24.9% year-on-year, ranking 11th; BYD sold 187,100 vehicles in the EU market for the full year, surging 271.8% year-on-year, ranking 20th. Even Tesla only managed to rank 18th.

Clearly, the European automotive market is no simple arena. Taking the EU-27 as an example, attitudes toward Chinese automobiles vary widely among countries.

Germany's three major automakers—Volkswagen, BMW, and Mercedes-Benz—account for one-third of their global sales in the Chinese market and are deeply integrated with the Chinese supply chain. Hungary, lacking domestic automotive brands, relies entirely on foreign manufacturing to drive its economy and leverages China's new energy vehicle supply chain to boost employment and tax revenue.

Thus, it is unsurprising that "pragmatic cooperation" factions led by Germany and Hungary explicitly oppose "imposing tariffs on Chinese electric vehicles" and actively attract investment and welcome capacity cooperation.

Conversely, France's local brands, Renault and Stellantis, have minimal market share in China, while Chinese electric vehicles are heavily encroaching on their domestic and Southern European markets, creating significant industrial competition pressure. Italy's numerous small internal combustion engine automakers and parts suppliers are vulnerable to risks, leading the government to fully support tariff barriers to protect local small and medium-sized manufacturers.

Therefore, "European automotive sovereignty" factions led by France and Italy are heavily influenced by geopolitical considerations, hoping to use tariffs and technical regulations to delay the expansion of China's new energy advantages.

However, all stances are not set in stone; everything can be compromised for practical interests. For example, Stellantis's cooperation with Leapmotor and its new investments in the Chinese automotive market have shaken France's position.

Faced with such a European automotive market landscape, automakers like Xpeng and SAIC can, after comprehensive evaluation, leverage Volkswagen's layoffs to further deploy factories and achieve localized production.

However, this does not mean there are no risks. After all, Chinese automakers expanding overseas are still in the "pioneering era." Overseas markets can be enticing honey, but they may also turn into deadly poison.

Of course, Chinese automakers, having been tempered in the domestic market, whether purely electric or hybrid, are undoubtedly capable of competing head-on with Japanese and Korean vehicles in the European market. So why not set a small goal first: Replace half of the market share of Japanese and Korean automakers by 2026, selling an additional 1 million vehicles.

02 The US Market: No Room for Trial and Error

Unlike the logic of the European automotive market, the US free market is not truly free. The example of Polestar shows that the US automotive market is not simply an open market in the traditional sense; it is even a unique form of "isolationism." The American people are being deprived of the right to affordable new energy vehicles because of this "closed-off" approach.

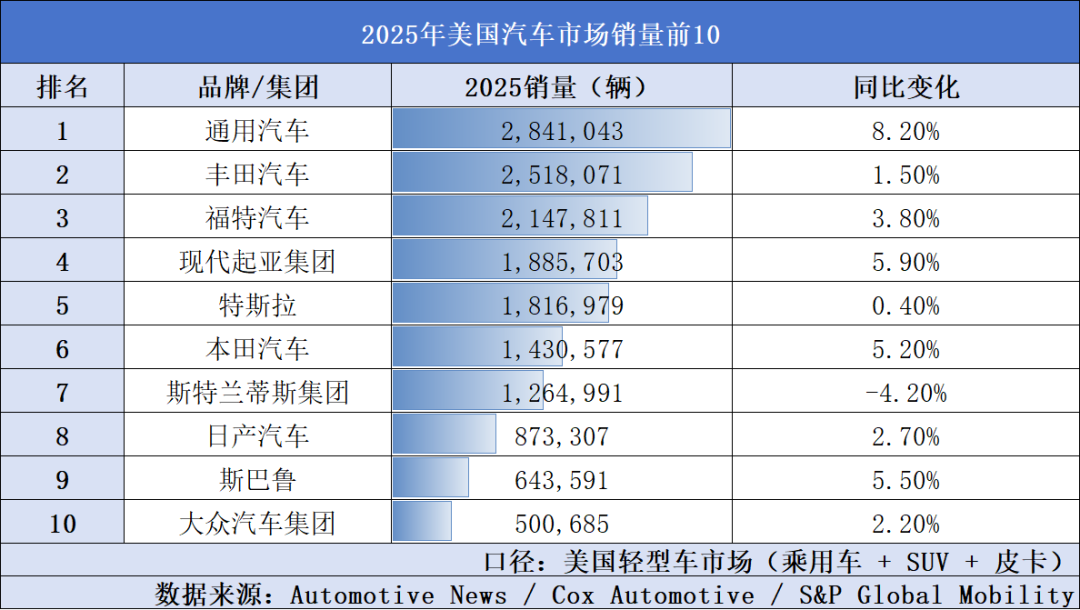

The structure of the US automotive market has remained unchanged for years, with domestic brands (Tesla, General Motors, Ford, Stellantis) forming the foundation, Japanese brands (Toyota, Honda, Nissan) providing strong supplementation, and European luxury brands (BMW, Mercedes-Benz, Audi) maintaining relatively fixed market segments.

On the surface, rankings may change, but the deeper structure remains virtually unbroken. The underlying logic is not complex: The US market aims to gradually "integrate newcomers into the system." Any external brand that rapidly expands in the US market will inevitably enter an adjustment cycle: stricter regulatory constraints, increased requirements for localized production, and rebinding of supply chain structures.

This is how Japanese automakers fared. When they first entered the US market, they quickly penetrated niche markets by relying on fuel efficiency and cost advantages. However, once their market share expanded to a certain level, changes in the external environment began to take effect.

The US market did not simply reject them but instead reincorporated their competitive methods into a regulatory framework through trade restrictions and localization requirements.

Times have changed. Previously, Japanese automakers entered a "manufacturing-focused America" where they could "sell vehicles first and adapt to regulations later." However, Chinese automakers now face a "data-driven + security-focused + rules-preconditioned America," where they must "pass regulations first before discussing entry" and may not even be given a chance to make mistakes.

In such a highly regulated and systematized market, any direct entry in its original form may face structural constraints or even restrictions at various levels, including political and tax-related ones, rather than pure commercial competition.

This is why the US market consistently exhibits a stable but highly closed structural characteristic—it allows participation but only on its terms. In other words, everyone must pay a sufficient "toll." In recent years, Japanese automakers have surrendered significant profits as a result.

In reality, there are not many Chinese vehicles in the US market, primarily existing in three forms: European brands controlled by capital, such as Volvo and Polestar; niche luxury brands like Lotus; and commercial electric vehicles like BYD buses. The mainstream passenger vehicle market remains structurally vacant.

Due to various factors, the taxes and fees for exporting Chinese vehicles alone are prohibitively high, while directly localizing production is too risky for Chinese automakers. Therefore, they can only adopt a circuitous strategy, leveraging supply chain companies like Fuyao Glass, Joyson Electronics, and CATL to first deploy the industrial chain before gradually making inroads.

There is no need to be discouraged. Chinese automakers expanding overseas will not halt due to "closed-off" policies in a single market, nor will they ignore risks for the sake of perceived benefits. As the global automotive industry's center of gravity shifts and the new energy vehicle era sweeps across the globe, the global automotive market has officially entered the "Chinese rhythm."

Editor-in-Chief: Yang Jing Editor: He Zengrong

THE END

-

![]()

Avita Reapplies for Listing: Reports 25.6 Billion Yuan in Revenue and 3.49 Billion Yuan in Net Loss for the Previous Year, with 182 Million Yuan in Dividends from Yinwang | MIRROR Pro

-

![]()

DataStory's Controversial Hong Kong IPO: 5 Billion Valuation Hangs in the Balance Amid 866 Million Debt Pressure

-

![]()

Apple’s Prices Skyrocket Up to 3,500 Yuan! Who Empowered Cook to Hike Prices?

-

![]()

ByteDance Executives Go Viral!

-

![]()

ByteDance Executives Dominate Headlines!

-

![]()

Perspective | An Ke Cashes Out from the Computing Power Support Sector Under His Flagship, Jin Jing New Energy Faces Four Real Challenges in Its HK$2.5 Billion Acquisition

-

![]()

Selling Cars No Longer Profitable: Guanghui Transforms into a 'Landlord'

-

![]()

Anchoring Physical AI, Momenta Passes Public Verification