Selling Cars No Longer Profitable: Guanghui Transforms into a 'Landlord'

07/01 2026

07/01 2026

417

417

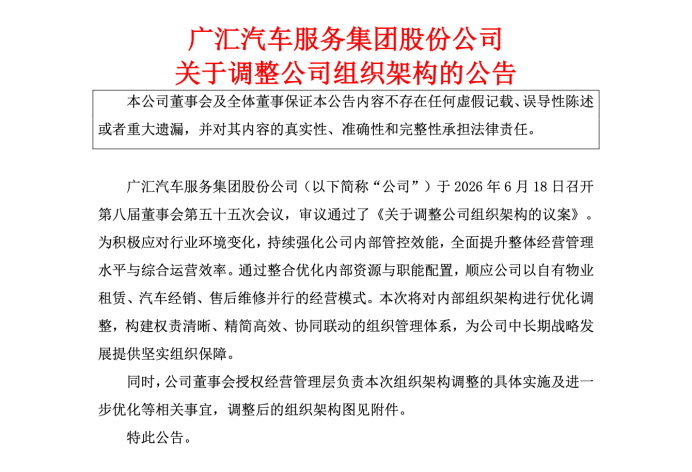

Recently, the news that "Guanghui Automobile, once a titan in the automotive dealership sector, has largely withdrawn from the new car sales business" has sparked considerable interest. According to Guanghui Automobile's announcement in June regarding its organizational restructuring, the company's current business model integrates self-owned property leasing, automotive dealerships, and after-sales maintenance services. At its zenith, Guanghui Automobile boasted over 700 outlets nationwide, representing 57 automotive brands, including BMW, Mercedes-Benz, Audi, and Buick. Today, of its more than 500 stores with self-owned land and buildings across the country, only over 30 remain in operation, primarily focusing on after-sales maintenance services and largely withdrawing from new car sales. The company's overall business model has now shifted to a blend of self-owned property leasing, automotive dealerships, and after-sales maintenance. Previously, a former Guanghui Automobile employee lamented, "There's no more Guanghui; there are no more Guanghui Automobile 4S stores now."

In fact, as early as August 2024, Guanghui Automobile was delisted from the A-share market after its stock price remained below 1 yuan for 20 consecutive trading days. Subsequently, major automotive brands revoked Guanghui Automobile's dealership authorizations. By August 2025, its number of outlets had dwindled from over 700 at its peak to just 218. Today, Guanghui Automobile no longer operates any 4S stores selling new cars. However, the company's board of directors has stated that it will not consider bankruptcy liquidation and hopes to re-enter the new energy vehicle sales and used car leasing sectors after reducing its debt. The survival struggles faced by Guanghui Automobile dealers are not unique. Previously, Pangda Group was delisted due to poor management. Against the backdrop of collective pressure on traditional fuel vehicle dealers, an increasing number of dealers are either "switching sides" or "closing shop," with dealers from nearly all brands affected. Transitioning to new energy brands has become the choice of more and more dealers.

The survival struggles faced by Guanghui Automobile dealers are not unique. Previously, Pangda Group was delisted due to poor management. Against the backdrop of collective pressure on traditional fuel vehicle dealers, an increasing number of dealers are either "switching sides" or "closing shop," with dealers from nearly all brands affected. Transitioning to new energy brands has become the choice of more and more dealers. Ultimately, the biggest challenge for these dealers is the severe price inversion in new car sales, compounded by sluggish terminal market demand. The relentless advance of the new energy wave is eroding the market share of fuel vehicles, forcing traditional luxury and joint-venture brands to rely on significant price reductions to maintain sales. However, the price war has not reversed the declining trend in fuel vehicle sales; instead, it has trapped dealers in a cycle of price inversion—"the more they sell, the more they lose." The fuel vehicle market is shrinking rapidly, leading to a sharp decline in sales for joint-venture and luxury brands that primarily rely on fuel vehicles.

Ultimately, the biggest challenge for these dealers is the severe price inversion in new car sales, compounded by sluggish terminal market demand. The relentless advance of the new energy wave is eroding the market share of fuel vehicles, forcing traditional luxury and joint-venture brands to rely on significant price reductions to maintain sales. However, the price war has not reversed the declining trend in fuel vehicle sales; instead, it has trapped dealers in a cycle of price inversion—"the more they sell, the more they lose." The fuel vehicle market is shrinking rapidly, leading to a sharp decline in sales for joint-venture and luxury brands that primarily rely on fuel vehicles.

From January to May 2026, Mercedes-Benz, BMW, and Audi sold 99,000, 139,000, and 139,000 vehicles in China, respectively, marking year-on-year declines of 51.8%, 37.15%, and 36.69%. During the same period, Toyota, Honda, and Nissan sold 579,400, 173,300, and 199,900 vehicles, respectively, with year-on-year declines of approximately 10%, 32.5%, and 11.4%. German luxury brands and Japanese joint ventures are experiencing a collective slowdown.

Behind the sales figures of BBA (Benz, BMW, Audi) and the Japanese Big Three lies real survival pressure for dealers. Guanghui Automobile is the most typical example—out of more than 500 self-owned stores, only over 30 remain operational, primarily focusing on after-sales maintenance. During periods of tight capital, wage delays at stores have occurred, with some employees reporting being paid only 40-60% of their salaries after two months of delays. From top-tier dealers to small and medium-sized stores, the struggles faced by joint-venture brand dealers have become an industry-wide phenomenon.

The difficulties faced by dealers stem from the shrinking market for fuel vehicles. In May 2026, the domestic retail penetration rate of new energy passenger vehicles climbed to 62.9%, a record high, surpassing 60% for two consecutive months. Meanwhile, retail sales of fuel-powered passenger vehicles plummeted by 39% year-on-year, with their market share shrinking to just 37.1%. The rapid contraction of the fuel vehicle market has directly impacted the dealer network, which primarily relies on traditional fuel vehicle sales. In fact, Guanghui Automobile has also attempted to transition into new energy brand dealerships. Since 2021, the company has been laying the groundwork for its new energy business. By the first half of 2024, it had secured authorizations for 70 new energy stores, with 55 already operational, partnering with brands such as Avatr, Voyah, XPENG, Zeekr, Ora, Geely Galaxy, Changan Deepal, and Xiaomi. However, Guanghui Automobile's vast network of over 700 outlets makes transitioning difficult. Fuel vehicles remain the mainstay of its sales, with new energy stores accounting for less than one-tenth of its total, and its transition speed lags far behind market changes.

In conclusion: Fuel vehicle dealers are collectively trapped in a cycle of price inversion and tight capital chains, prompting an increasing number of dealers to embrace new energy brands—a move driven by both survival necessity and proactive change. Today, Guanghui Automobile has largely exited new car sales, shifting its focus to rental income and after-sales services. The company states that it will not pursue bankruptcy liquidation and plans to re-enter the new energy sector after reducing its debt. However, whether this transformation and adjustment will succeed remains uncertain. (Images sourced from the internet; removal upon infringement notice)

-

Meituan Triumphs with Domestic Computing Power: Running a Trillion-Parameter Model, Exploration Initiated in 2023

-

![]()

Embodied Intelligence and Mobile Robots: Why the Intensified Focus on Factories This Year

-

"Chip" Radiance Persists: Is the Semiconductor Sector Still a Magnet for Investors?

-

![]()

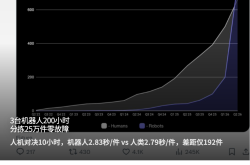

Robots Embark on 200-Hour Factory Trials: Is AI Truly Ready for Industrial Deployment?

-

![]()

Another Bionic Robot Company Secures $7 Million in Funding

-

![]()

UBTECH U1 Launch: Pre-sale Excitement Creates Unrealistic Hopes, Resulting in Disappointment at the Event

-

![]()

Accounting Manipulations Inflate Profits! 2 Billion Yuan Cumulative Loss Over Six Years—How Long Can the AI Narrative Sustain?

-

![]()

Food and Beverage Companies Rush to AI: Is It a Trend or a Pitfall?