Avita's Second Attempt at HKEX Listing: What Sets It Apart? | Auto Circle

07/13 2026

07/13 2026

489

489

The automotive industry is undergoing an unprecedented transformation, fueled by rapid advancements in new energy, autonomous driving, artificial intelligence, and chip technology. To stay abreast of these developments and explore market trends, LingTai LT has introduced the Auto Circle column. From a professional standpoint, this column monitors global automotive industry updates, major automakers' new product launches, technological innovations, and market performance. Through in-depth analysis, it reveals the underlying business logic and market patterns, demonstrating how these elements are reshaping the industry and influencing human mobility. This article, the 30th installment of the column, focuses on Avita's second attempt at listing on the HKEX and the strategies behind it.

Author: Zhang Qian

Editor: Hu Zhanjia

Operations: Chen Jiahui

Produced by: LingTai LT (ID: LingTai_LT)

Header Image: Publicly sourced online

On June 30, Avita submitted its application to list on the Hong Kong Stock Exchange (HKEX) for the second time. The following day, July 1, it secured an L3 autonomous driving test license. This transition of advanced intelligent driving from 'technology demonstration' to 'commercialization' is timely, seemingly addressing concerns in the capital market.

The success of this endeavor hinges on three key variables.

Three Curves on the Rise

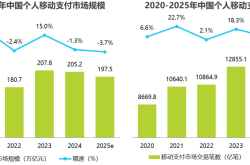

A closer look at the prospectus reveals three sets of figures that are trending upwards.

Revenue Growth:

Revenue surged from a mere RMB 28.34 million in 2022 to RMB 5.645 billion in 2023, RMB 15.195 billion in 2024, and is projected to reach RMB 25.631 billion in 2025. This represents a compound annual growth rate exceeding 300% over three years. Vehicle revenue alone grew from RMB 5.542 billion to RMB 23.902 billion, marking a 4.3-fold increase in the same period. More notably, non-vehicle revenue—comprising ecosystem and after-sales services—soared from RMB 103 million in 2023 to RMB 1.729 billion in 2025, with its share rising from 1.8% to 6.7%. This constitutes a nearly 17-fold increase in three years. With the vehicle fleet surpassing 200,000 units, revenue streams from software subscriptions, after-sales services, and ecosystem offerings are opening up. This signifies Avita's business model evolving from 'one-time vehicle sales' to 'recurring service fees,' thereby enhancing customer lifetime value.

Gross Margin Improvement:

The gross margin, which was -3% in 2023, turned positive to 6.3% in 2024 and further improved to 9.4% in 2025, marking a 12.4 percentage point increase over three years. With sales reaching 122,700 units in 2025, economies of scale reduced per-unit fixed costs, the proportion of high-priced models increased, and battery supply costs were contained. Avita's gross margin trend is upward, contrasting with many peers experiencing declines amid price wars—a stark difference that speaks volumes.

Operating Cash Flow:

Operating cash flow turned positive for the first time in 2024, reaching RMB 1.755 billion, and expanded to RMB 2.315 billion in 2025. Two consecutive years of positive cash flow indicate Avita's self-sufficiency through vehicle sales. Inventory turnover days decreased from 96 to 36, outperforming the industry average of 50—a reflection of improved channel efficiency and robust inventory management. In 2025, sales and marketing expenses were RMB 3.281 billion, and R&D spending was RMB 2.086 billion. These fixed costs were diluted over a larger revenue base, with operating leverage taking effect.

Securing the L3 license is another critical signal. It means Avita's advanced intelligent driving is no longer just a technical parameter showcased in presentations but a commercializable, user-chargeable product feature. Shifting from one-time vehicle sales to recurring software service revenue, if this business model transition succeeds, it will fundamentally alter Avita's profit structure.

Revenue, gross margin, and cash flow—all three curves are on the rise, coupled with the commercialization of the L3 license. Together, these four factors constitute the core evidence of Avita's 'turning point.'

But are these signals sufficiently promising? That depends on the next two variables.

Sales and Cash: A Race Against Time

Avita's total sales in the first five months of 2026 were 20,160 units, averaging 4,032 units per month. Comprehensive information from Tianyancha shows that leading new forces have raised their monthly sales threshold to 30,000 units. Li Auto, NIO, and Xpeng have met this benchmark, while Leapmotor has surged to 80,000 units. Avita's best monthly sales in May were 7,336 units, still short of the '10,000 units per month' baseline.

The direct consequence of insufficient scale is the inability to dilute costs. In 2025, sales costs accounted for 90.6% of revenue, with raw material costs at RMB 20.8 billion, or 89.6% of sales costs. The company admits in its prospectus: 'Our relatively small procurement volume limits our bargaining power with component suppliers.' For the same supply chain, larger automakers secure lower prices, while Avita must accept higher costs—an iron law of economies of scale.

At the cash reserve level, it declined from RMB 19.3 billion at the end of 2024 to RMB 9.7 billion at the end of 2025, and further to RMB 6.2 billion by the end of April 2026. Over 18 months, RMB 13.1 billion in cash was consumed, averaging over RMB 700 million per month. At this rate, the RMB 6.2 billion cash reserve won't last a year. In 2025, operating cash inflow was RMB 2.315 billion, but the same year's loss was RMB 3.489 billion—the self-financing gap persists.

Integration with Shenlan Automobile is a cost-reduction strategy being pursued by Changan Automobile. The two brands operate independently with differentiated positioning but deeply share technologies, supply chains, and systemic capabilities in the mid-to-back end.

The direction is correct—cost reduction, efficiency enhancement, and avoidance of internal friction. However, Shenlan S09, priced at RMB 259,900, encroaches on Avita's price territory, with significant overlap in the RMB 250,000–300,000 range. Consumers may ask: Why pay tens of thousands more for Avita when the technological foundation is the same? Avita needs to articulate its high-end positioning more clearly.

Integration also involves organizational aspects. Two brands, two channels, and two teams must achieve supply chain and R&D synergies, requiring the breaking down of departmental silos and coordination of interest distribution. This cannot be resolved with a single document; it demands time and management investment.

Industry concentration is accelerating. Comprehensive information from Tianyancha shows that in May 2026, the retail penetration rate of new energy passenger vehicles reached 62.9%, a record high, but incremental growth is primarily captured by leading brands. Data from the China Passenger Car Association indicates that from January to May this year, cumulative retail sales in the national passenger car market were 7.11 million units, down 19% year-on-year; automotive industry profits were RMB 144 billion, down 20%, with the profit margin dropping to 3.4%, the lowest for the same period in five years. Declining terminal sales and industry profits further compress automakers' profit margins.

Under such industry conditions, Avita has chosen to go public.

The Final Window of Opportunity

The rationale behind the second submission is straightforward: Avita needs to raise funds through listing to support its scale expansion. However, listing itself requires a compelling narrative. What does Avita have to offer?

The answer lies in the second half of the year.

The Avita 07L, a large five-seat luxury SUV, is scheduled to start pre-sales in Q3, equipped with the latest intelligent driving system and battery technology. A flagship large six-seat SUV, featuring CATL's condensed matter battery, will also launch by year-end. If these two new models gain traction in the market, sales could reach an inflection point. By 2030, Avita plans to launch 17 models covering sedans, SUVs, and MPVs across all categories.

The timing of the second submission aligns with the pre-launch of new models in the second half of the year. If the 07L and flagship large six-seat SUV generate strong order numbers post-launch, Avita can present the latest sales data to support its valuation during the HKEX hearing.

Overseas Markets: A New Frontier

Overseas markets provide another avenue for growth.

In 2025, overseas revenue reached RMB 1.398 billion, more than quintupling year-on-year, with the average selling price per overseas vehicle exceeding RMB 300,000, higher than domestic prices. Avita ranks first in Thailand's high-end pure electric vehicle sales and has captured over 10% of the high-end new energy vehicle market in the UAE. As of May this year, its business spans 43 countries with 95 overseas distribution outlets. The overseas segment has achieved stable profitability, acting as a buffer against domestic price war pressures. In the first five months of 2026, overseas sales surged 33.4% year-on-year, far outpacing domestic growth.

Avita's overseas strategy differs from most automakers—it doesn't rely on price cuts to gain market share but leverages high-end positioning for profitability. This 'high-pricing, high-recognition, high-profitability' model, if replicable in more markets, will become a key component of its long-term competitiveness. However, overseas expansion requires investment—channel construction, brand building, and localization adaptations—all demanding cash.

The product strength of the 07L will be a critical variable.

Comprehensive information from Tianyancha indicates that as Avita's first large five-seat luxury SUV, the 07L is positioned between its existing sedan and SUV lines, targeting family upgrade and additional purchase users—a demographic less price-sensitive and more focused on space, intelligent features, and brand experience. If the 07L can differentiate itself competitively in the RMB 300,000 price segment and contribute 5,000–8,000 monthly sales, Avita's monthly sales could jump from 4,000 to 8,000–10,000 units, crossing the survival threshold.

From the IPO timeline perspective, the HKEX's review cycle typically takes 6–12 months. Avita submitted its application on June 30; if materials are smooth and reviews proceed without obstacles, it could complete the hearing and listing as early as late 2026 or early 2027. This window aligns closely with the new model launch cycle in the second half of the year—essentially, Avita is using 'new model order data' as the core support for its listing valuation.

Thus, Avita is waging a time-difference battle: using new model volume growth and overseas expansion in the second half of the year to offset first-half sales declines and cash consumption, aiming to secure a listing before capital market doors close. The key to this push lies in whether second-half sales can truly surge, whether integration with Shenlan can quickly yield results, and whether the high-premium overseas model can be sustainably replicated. All three variables are indispensable.

Avita's story hasn't reached its conclusion. Some are willing to wait because they see a turning point.

For inquiries about this article, please contact

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming